What the Federal Reserve gave us on Wednesday with the release of their July minutes was decisive waffle.

On the one hand, steadily rising employment means an interest rate rise is close. On the other, the strong dollar, China, emerging markets, and the oil and commodity collapse is scaring the daylights out of them.

You can bet that every central banker in the world is calling up Janet Yellen begging her not to raise rates this year to save their own skins.

While the US economy is posting great numbers, especially in housing, autos, consumer spending, and anything that consumes energy, the rest of the world is going to hell in a hand basket.

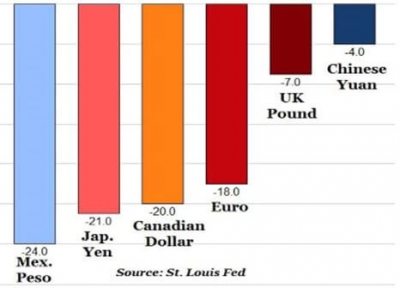

The melt down in emerging markets (EM) is especially egregious, with many currencies hitting all time lows against the greenback.

The markets responded in kind. The probability of a September rate hike has therefore gone from 80/20 to 50/50.

In other words, it?s a coin toss.

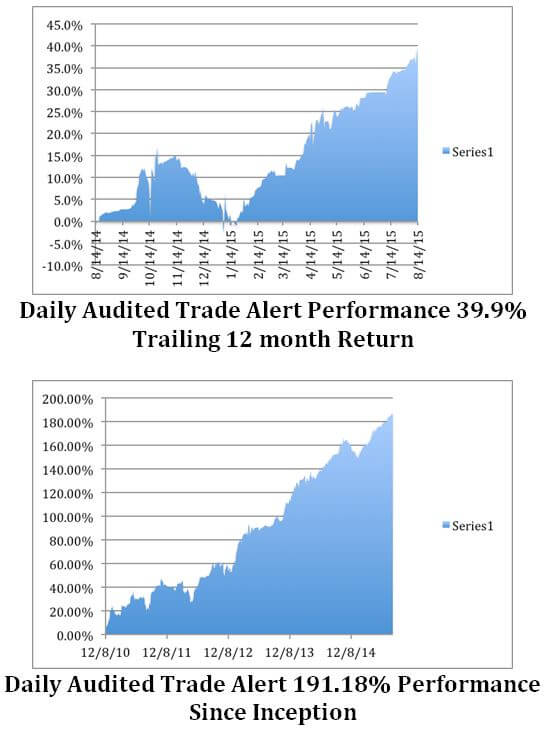

I?m not in the coin toss business. I?ll leave that to my competitors. That is, unless the coin is heavily weighted in my favor and has me come up a winner 95% of the time. That has been the recent success rate of my Trade Alert service.

So I am going to cut my long dollar position by half, selling my Currency Shares Euro Trust (FXE) September, 2015 $112-$115 in-the-money vertical bear put spread at $2.68.

Sure, it?s a small profit. But it is better than a poke in the eye with a sharp stick. This gives me the dry powder to resell the beleaguered Europe currency higher up if the current rally continues.

Don?t worry. I have not suddenly fallen in love with the Euro. This is just a tactical move. The long-term bull market for the US dollar is alive and well.

In any case, we amply squeezed the juice from the short Euro trade during the first half when it was in free fall with multiple Trade Alerts. Since then, its volatility has been muted.

As for the Japanese yen (FXY), (YCS), I am going to continue to run my short position there. The fundamentals there are so dire, and the quantitative easing so aggressive, that it pays to keep one finger in the pie.

I?m afraid that the Fed?s indecisiveness is going to pee on the parade for the entire rising interest play for the rest of the year. That includes long positions in financials (GS), (BAC) and shorts in the Treasury bond market (TLT), (TBT). Believers may have to wait until 2016.

The present trading conditions for all markets are among the worst I?ve ever seen. Not taking a quick profit is the same as leaving your wallet in the middle of New York?s Times Square at rush hour and expecting to find it there the next day.

There are a ton of other interesting things to do here. Oil (USO), commodities, and copper (FCX) are reaching multi decade lows.

Gold (GLD) looks like it may be awakening from a long slumber. A friend of mine bought $360 million worth of the barbarous relic just the other day, and he didn?t earn that much money by being a rotten market timer.

As a former student of the US Marine Corps Sniper School at Camp Pendleton, I can assure you that it is far better to lie back and take the careful, measured, precise shot than to engage in hand-to-hand combat with one hand tied behind your back.