With the price of oil closing at a low on Friday of $43.77, you?d think I might be concerned.

In actual fact, I could care less, am indifferent, unconcerned, and even could give a rat?s ass.

There?s nothing like seeing your long term forecasts vindicated.

When I warned the oil majors in the late 1990?s that fracking technology was about to change their world beyond all recognition, they told me I was out of my tree, in the politest way possible, of course.

Their argument was that the technology was untested, unproven, and a huge liability risk. If they accidently polluted underground fresh water supplies, the ambulance chasers would make a beeline towards the deepest pockets around, and that was theirs.

They were telling me this after I supplied them my data showing 17 consecutive successful wells drilled in the depleted oilfields of the Barnet Shale, in West Texas (in the old Comanche country).

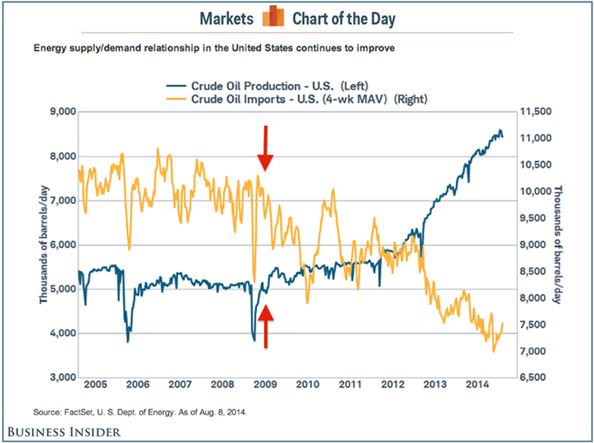

Today, I received the chart below from my friends at Business Insider. And guess what? Some 15 years later, and the energy industry has been changed beyond all recognition. The majors finally jumped in after building legal walls against the liability that so concerned them, and started fracking like there was no tomorrow.

The message is pretty clear. In the last five years, US oil production has skyrocketed from 8 million to 11.3 million barrels a day. America is now the world?s largest oil producer, eclipsing Saudi Arabia at 11 million b/d, and Russia at 10.5 b/d and falling.

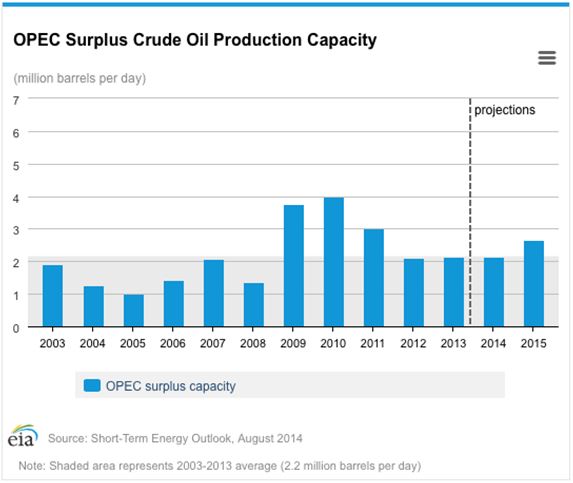

Oil imports have collapsed from 10.3 to 7 million barrels a day. The share coming from the volatile Middle East has shrunk to a miniscule 2 million barrels a day. Some 80% of Persian Gulf oil exports now go to China. OPEC surplus oil production capacity is soaring (see table below). It couldn?t happen to a nicer bunch of people.

The chart also predicts that the US will achieve energy independence within four years, or at least parity in its imports and exports or energy and distillates. The administration is doing what it can to help along this trend, permitting the first exports of distillates in half a century, to South Korea, it turns out.

Is it any wonder that President Obama is turning a blind eye to recent horrific developments in the Middle East? This explains why I really don?t care about oil prices anymore.

There is another upshot to all of this. About the time that America gets its energy independence, it should also get a balanced budget. That is coming primarily from the big cuts in defense spending. The twin deficits, energy and the budget, are intimately linked. It is no surprise, then, they will disappear together.

By the way, did I mention that this is all great news for the long term future for stock prices? The stock market certainly thinks so, with its stubborn refusal to fall substantially.

Just thought you?d like to know.

Do You Think there?s too Much?

https://www.madhedgefundtrader.com/wp-content/uploads/2014/08/Man-Oil-Bottles.jpg291399Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-08-10 01:03:572015-08-10 01:03:57Why I Don?t Care About Oil

The Berber tribesmen were upset that their WiFi wasn?t working.

I cannot think of a more dissonant statement to be made about the early 21st century.

So I told the front desk clerks in remote Ouarzazate, Morocco, on the edge of the Western Sahara Desert, that I would be happy to fix it for them. They looked at me suspiciously.

I went on to explain. I come from a far away land called ?California? in the fabled city on the Bay known as San Francisco. From a very young age we teach our children secret mystical languages, like Scratch, Java, and HTML.

They grow up to build magical devices with great powers, like iPhones, modems, and routers. They can fix these things too. I then crawled under their desk, found a mass of wires, and went to work.

Within three minutes I rebooted and reconfigured the wireless system and had it running. For good measure I also cleaned out the cookies and the cache from the PC. The network ran like greased lightning.

They now looked at me in awe. Not only was their PC working better than ever, they could now watch YouTube for the first time.

I left them clustered around the monitor, entranced by a video of a man in traditional Berber dress playing a gimbre, a guitar-like instrument made of mahogany, lemon wood, and ebony, with strings made of goat intestines.

Welcome to the Morocco of 2015.

I am writing this not because I know you will find this blend of the 14th and 21st century utterly fascinating. I am passing on my observations because they give great insight into the investment opportunities to be found in this storied North African country.

It also presents broader insights into the emerging markets space as a whole, and the risks therein.

I was here retracting my steps from a trip I took as a student in 1968, when Morocco was just entering the 20th century.

It had recently been freed from colonial rule, bringing to an end a century and a half of warfare between the French Foreign Legion and indigenous Berber tribes.

Then, many people walked across the desert sands barefoot. The roads were in a terrible state of repair, untouched since the 1920?s. Camel trains were still an important mode of transportation.

A half century later, I was whisked from Agadir to Marrakesh, Tangier, and Casablanca on brand new freeways with a Mercedes and driver (four wheel drive on the sand). A journey that once took days was completed in hours.

Berbers were no longer shooting at the tourists, but selling them rugs, ceramics, and guided tours, all at bargain prices. What they are losing in margins (by robbing victims) they are making up in volume.

Only a few mangy camels are available for pictures with tourists at $10 a pop (was I overcharged?).

Here is the really interesting thing about Morocco. Most of Europe tore down their city walls and medieval warrens during the 1700-1800?s, believing it a move towards modern civilization.

Morocco modernized so late, not until after independence in 1956, that their 1,000-year-old medinas were still standing. Today the country is parlaying them into a multibillion-dollar tourism industry that is pulling it into prosperity.

In recent years, the sightseeing dollar has eclipsed mining, agriculture, and fishing as the primary earner. A country that was once enriched by Trans Saharan trade in gold, ivory, sugar, and slaves now has package tours of Chinese paying the bills.

The truly stunning thing is how large the cities have grown. Casablanca and Tangiers have both grown twenty-fold since my first visit. Historic city centers are surrounded by massive high-rise suburbs housing millions. The resulting crush on the transportation system has been overwhelming.

Cities are now characterized by dawn to dusk traffic jams with honking horns as residents speed about their day in 20 cent per ride ?petite taxis.? The infrastructure has not been able to keep up with economic growth. It is a problem that I have found common in all emerging nations.

I took time during my stay in the Sahara to visit the famed Atlas Studios. Set up by a Moroccan entrepreneur during the 1980?s, it became the must-go to place for any film requiring a desert location. Local artisans build the sets and then work as extras, all at below union wages.

The Jewel in the Nile, The Mummy, The Sheltering Sky, and King Tut are some of the movies you may recognize that were shot here.

By the way, if anyone invites you to the Sahara during the summer, tell them you?re busy. At 110 degrees, I could only venture away from the air conditioning an hour at a time, and I grew up in the desert near Palm Springs!

When that hot desert wind rolls in during the evening, raising the temperature 30 degrees in five minutes, it literally slaps you in the face. It is an amazing natural occurrence to behold.

Crossing the High Atlas Mountains from Ouarzazate to Marrakesh was an experience and a half. After driving through five century old mud brick villages for hours, I ascended the 12,000? range on one of the worst hairpin roads I have ever seen.

Heavy trucks clogged the road in both directions. Spending a lifetime analyzing emerging economies, I learned that you can measure the health of a country?s economy by observing the number and condition of its trucks.

Lots of new trucks are proof of healthy growth. Few decrepit vehicles are a sign of no growth.

But spanking brand new trucks establish the presence of international aid institutions, which one finds only in the most desperate of economic conditions, countries earning $300 or less in per capita annual income.

Using that standard, I rank Morocco as post emerging or pre developing, not far behind countries like South Korea and Turkey.

If you want to summarize the Moroccan economy in a single line, it?s all about bringing in as many tourists as possible to pay for oil imports.

Morocco has the fifth largest economy in Africa, and is considered by many international agencies to be the most competitive.

Its $250 billion GDP ranks 61st in the world, and is expected to grow a healthy 5% this year.

Per capita income stands at $7,350, compared to $11,850 in China and $48,374 in the US. That is astronomical compared to the $100 figure when I first arrived so long ago.

Far and away, its largest trading partner is France, a legacy from the colonial days.

The 51% of the economy that accounts for tourism is booming, with discount Chinese package tours starting to flood the country, as they are the rest of the world.

That?s a good thing, since the traditional foundation of the economy, phosphate from the Spanish Sahara, and agriculture, are fading, thanks to weak prices.

Another bright spot is manufacturing, which is surging, thanks to massive foreign capital inflows and rising consumer spending.

IT is another hot growth area, and almost everyone seemed to have a cheap Chinese tablet or cell phone.

Renault has recently completed a plant near Tangiers that aims to produce 200,000 cars a year and similar facilities are planned by Citroen and Ford (F). Chinese and Indian manufacturers say they will match the move.

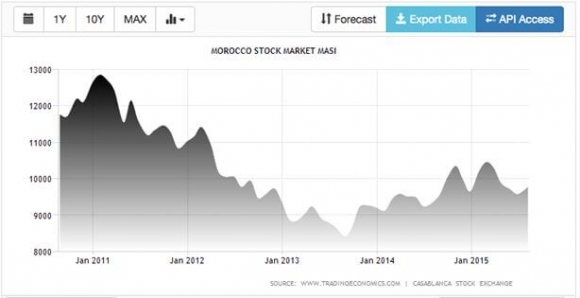

Casablanca boasts Africa?s oldest stock market. The MASI index, which has a heavy bank, insurance and construction weighting, is up 2% so far in 2015.

But foreign purchases of shares there is easier said than done. Better to gain indirect exposure through the Market Vectors-Africa ETF (AFK), where Morocco has a 10.8% weighting.

One cannot write about Morocco without mentioning the king, Mohammed VI, whose image seems to be ever present.

Said to be a direct descendant of the profit Mohammed, criticizing him is illegal. All government benefits are disbursed in the name of the king.

The 51 year old has a PhD in Law from the University of Nice and is a major general of the Moroccan Air Force.

He has been a reformer, improving rights for women, and placing a major priority on job and economic growth.

His family has been able to insert itself into every major profitable enterprise in the country. The family fortune is thought to exceed $2.5 billion. He is the country?s largest landowner.

As is common in Africa, corruption is pervasive at every level of government.

After spending two weeks in Morocco, I have to tell you that it was an amazing experience in a lifetime of amazing experiences.

Keeping one foot in the 14th century and another in the 21st certainly gives one a unique perspective.

You never feel at risk traveling in distant corners of the desert, from one oasis to the next. But then you never feel completely safe either.

You really get a sense of this when the female population, after remaining hidden all day, emerge en masse in the evening to attend the mosque.

The women were wrapped head to toe in cheap polyester djellabas, even on the hottest days. Bare ankles are forbidden. Their religion demands they do this to the point of fainting, which I witnessed on numerous occasions.

You feel like you are in a completely different world.

Yet, they had the latest in cell phones and other electronics.

Observing momentous change over 47 years really gives one a sense of living history. I can?t wait to see the outcome of the changes afoot when I come back in another half century.

A travel video of my Report from Morocco will post online as soon as the editing is finished in a couple weeks.

https://www.madhedgefundtrader.com/wp-content/uploads/2015/08/John-Thomas1-e1438895796499.jpg400296Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-08-07 01:03:172015-08-07 01:03:17Report from Morocco

?The lack of complacency is at odds with the view that the market has peaked?peaks are turned in when every last bear has thrown in the towel, and the bulls are screaming to buy from the roof tops,? said David A. Rosenberg, of research boutique Gluskin Sheff.

https://www.madhedgefundtrader.com/wp-content/uploads/2015/08/Bull-Bear-Statue.jpg245259Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-08-07 01:02:002015-08-07 01:02:00August 7, 2015 - Quote of the Day

Featured Trade: (LAST CHANCE TO ATTEND THE AUGUST 3 ZURICH, SWITZERLAND GLOBAL STRATEGY LUNCHEON), (WELCOME TO THE DEFLATIONARY CENTURY), (TLT), (TBT), (MY PERSONAL ECONOMIC INDICATOR), (HMC), (NSANY), (GM), (F), (TSLA)

iShares 20+ Year Treasury Bond (TLT) ProShares UltraShort 20+ Year Treasury (TBT) Honda Motor Co., Ltd. (HMC) Nissan Motor Co. Ltd. (NSANY) General Motors Company (GM) Ford Motor Co. (F) Tesla Motors, Inc. (TSLA)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-07-30 01:06:142015-07-30 01:06:14July 30, 2105

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.