Global Market Comments

April 27, 2015

Fiat Lux

Featured Trade:

(JUNE 29 LONDON STRATEGY LUNCHEON)

(JUMPING BACK INTO GOOGLE),

(GOOG), (AAPL),

(WHO WAS BEN BERNANKE?)

Google Inc. (GOOG)

Apple Inc. (AAPL)

Global Market Comments

April 27, 2015

Fiat Lux

Featured Trade:

(JUNE 29 LONDON STRATEGY LUNCHEON)

(JUMPING BACK INTO GOOGLE),

(GOOG), (AAPL),

(WHO WAS BEN BERNANKE?)

Google Inc. (GOOG)

Apple Inc. (AAPL)

Come join me for lunch for the?Mad Hedge Fund Trader?s?Global Strategy Update, which I will be conducting in London on Monday, June 29, 2015. A three course lunch is included.

I?ll be giving you my up to date view on stocks, bonds, currencies commodities, precious metals, and real estate. And to keep you in suspense, I?ll be throwing a few surprises out there too. Enough charts, tables, graphs, and statistics will be thrown at you to keep your ears ringing for a week. Tickets are available for $247.

I?ll be arriving an hour early and leaving late in case anyone wants to have a one on one discussion, or just sit around and chew the fat about the financial markets.

The lunch will be held at a private club on St. James?s Square, the details of which will be emailed to you with your purchase confirmation.

I look forward to meeting you, and thank you for supporting my research.

To purchase tickets for the luncheons, please go to my?online store.

Google?s earnings were terrible. Therefore, the stock is rocketing.

The fact that the earnings were not as bad as they could have been seems to be the twisted logic behind this rally.

You would think I have a hole in my head buying a stock that just got slapped with a massive antitrust suit in Europe, which could potentially result in a record $6 billion fine, and suffers from plunging profits.

Clearly, Europe suffers from a ?Not invented here? syndrome.

However, it is safe to say that these negatives are now in the price. Anti trust suits take decades to resolve, and always end with an out of court settlement agreeable to all when they are of this size. Remember IBM and Microsoft?

Traffic at Google actually rose, but the company suffered a hit from the weak Euro, as did most other multinationals. That is largely behind us (see the Friday letter about the tag ends of the Euro collapse).

But margins are stabilizing, and the erosion seen in previous quarters now appears to be a thing of the past.

What you will hear next is about how much revenue from Google?s mobile ads search is exploding. Profits from YouTube are also building, and is no longer the drag it once was.

Knock out their revenues, and the cost per click realized at Google is actually rising. These are all good things.

Investors are so desperate to find a laggard quality stock in a toppy market with decent future growth prospects that they are willing to give my next door neighbor, the Internet search giant, the benefit of the doubt.

There has been such an influx of money into ?safe? dividend paying, bond proxy stocks that companies which sell toilet paper now trade at 25X earnings, while growing technology stocks are valued at a sub market 15X earnings.

In that looking glass world, you always buy the technology stocks.

It?s either this, or buy more Apple (AAPL), which announces earnings on Monday. But you are probably already up to the gills with Steve Jobs? creation, that is if you have been reading the Mad Hedge Fund Trader?s research.

At the very least, (GOOG) shares have to play catch up with (AAPL), which is coming off its own torrid year.

This means that the shares have rock solid support at $520, and that the Google (GOOG) May, 2015 $520-$540 deep in-the-money vertical call spread makes all the sense in the world.

You can pay all the way up to $18.50 for this spread and it still makes sense, as the expiration is in a short 15 trading days.

If you can?t do the options, then buy the sock. It is headed north of $600 a share soon.

Global Market Comments

April 24, 2015

Fiat Lux

Featured Trade:

(WEDNESDAY APRIL 29 GLOBAL STRATEGY WEBINAR),

(THE RECESSION IS OVER!),

(PLEASE USE MY FREE DATA BASE SEARCH)

The earnings announced for Q1 so far have been miserable, pummeled by a weak Euro, terrible weather and the West Coast port strike. But rather than collapse, global equity markets have punched through to new highs.

It isn?t just the United States that is performing this magic trick. Most European indexes (HEDJ) have blasted through to new eight-year highs.

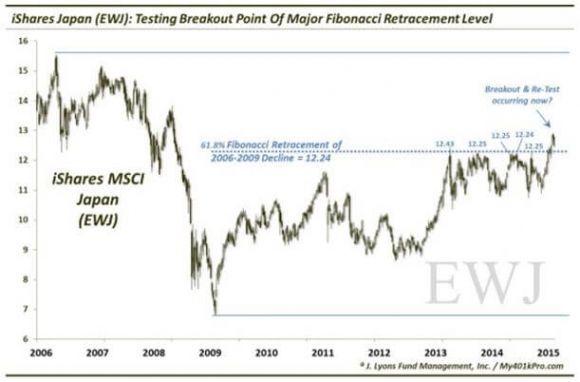

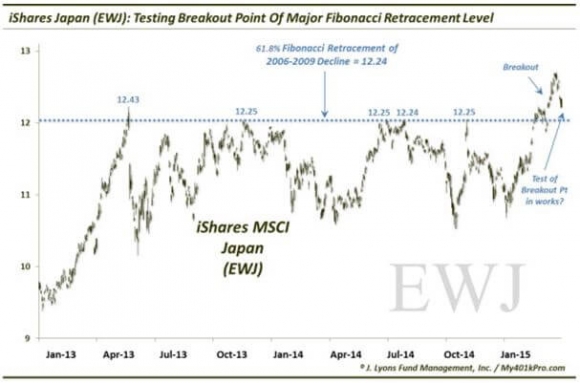

Even more impressive is the Nikkei average?s breakout to a new 15-year summit, making short work of key long-term Fibonacci levels that have been holding the Japanese stock index back for months.

That totally works for me, as I am keeping 10% of my model-trading portfolio in the Wisdom Tree Japan Hedged Equity ETF (DXJ), and another 10% short the Currency Shares Japanese Yen Trust ETF (FXY).

What gives?

The hard truth is that the American economy suffered a recession during January to March, and that recession is now over. Call it the mini recession that came and went so fast that you missed it if you blinked.

What happens next is that the weather improves and the men on strike go back to work. If the Euro does continue to fall, it will only be the last 10% of a 45%, seven-year move from $1.60 to $0.88. It is rather late in the game to sell short the Euro. In other words, it is almost over.

So, there is nothing left for stocks to do but discount a new economic recovery. In layman?s terms, that means ?Go up.?

For economic historians, such as myself, this was a most peculiar recession. For a start, no one knew it was happening. By the time they did, it was over. Interest rates never moved an iota. Unemployment fell. And stocks maintained their relentless push northward.

Man, this is my kind of recession!

So, what happens next?

Stocks go up more, but not by much. We haven?t had a clearing, capitulation type sell off since October. Since we never went down by more than 4% this year, that means the gains from here will be modest as well. I?m thinking that the S&P 500 (SPY) might reach $215 by June.

That?s why I took the bold move of buying the S&P 500 SPDR?s (SPY) May, 2015 $215-$218 in-the-money vertical bear put spread yesterday. As long as the index trades below $215 on the May 15 expiration day, in 15 trading days, I will get to keep the maximum potential profit or some 12.6% on the trade in only 3 weeks.

Not bad.

If you don?t believe me, then take a look at the price of Texas tea. Since it bottomed on March 17, the price of crude has rocketed by an awesome 37%, from $42.50 to $58, one of the sharpest moves in history.

This set energy stocks, and my favorite, solar shares, on fire, which played a major role in supporting the indexes at their lofty levels. At this point, the entire world is hoping to buy energy on the next dip and turn their holdings into energy portfolios.

Let me toy with your mind a little bit more. With another economic recovery on hand, the Federal Reserve is going to have to raise interest rates sooner or later (Hey Janet! Call me!).

However, just as this bull market is unlike any other, so may be the next interest rate cycle. When the headline unemployment rate hits 5% next year, the Fed will boost rates, but only by ?%. After that, we may see a second, and possibly a third ?% hike.

Then they will be done. Interest rates will peak at 1% and then a new recession, possibly only another ?mini? one, will prompt a rapid decent in interest rates down to zero. In other words, the next entire interest rate cycle may have Fed funds go from 0.25% to 1%, and then down to 0%.

Pshaw! You may say. But consider this: Deflation is still everywhere. There is no hint of wage pressure whatsoever. Commodity prices have just staged a modest rally, but are still a fraction of their old highs.

And as long as Janet Yellen heads the Federal Reserve, which is another 4-9 years at the very least, there will be no interest rate increases until we have proof of real inflation. That leaves us with only the above-mentioned token interest rate rises for the foreseeable future.

Let me throw one more idea out there for you to chew over.

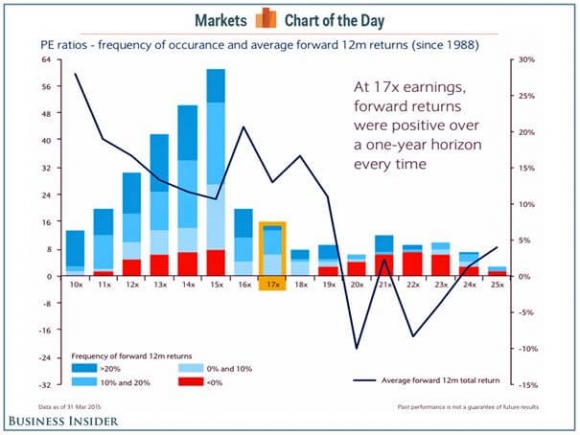

Take a look at the chart below from my friends at Business Insider. Every time stocks traded at a 17X multiple since 1988, shares generated a positive return over the following 12 months.

That certainly makes stocks look like a ?BUY? to me!

Stocks at These Levels Requires No Magic TrickGlobal Market Comments

April 23, 2015

Fiat Lux

SPECIAL BERSHIRE HATHAWAY ISSUE

Featured Trade:

(A CHAT WITH BERKSHIRE HATHAWAY?S WARREN BUFFET),

(BRK-A), (AXP), (WFC), (IBM), (KO), (GS), (AAPL), (UNP), (BAC)

Berkshire Hathaway Inc. (BRK-A)

American Express Company (AXP)

Wells Fargo & Company (WFC)

International Business Machines Corporation (IBM)

The Coca-Cola Company (KO)

The Goldman Sachs Group, Inc. (GS)

Apple Inc. (AAPL)

Union Pacific Corporation (UNP)

Bank of America Corporation (BAC)

Global Market Comments

April 22, 2015

Fiat Lux

Featured Trade:

(JUNE 29 LONDON STRATEGY LUNCHEON)

(THE TWO CENTURY DOLLAR SHORT),

(CNN?S JOHN LEWIS; THE DEATH OF A COLLEAGUE)

Global Market Comments

April 21, 2015

Fiat Lux

Featured Trade:

(JUNE 25 NEW YORK STRATEGY LUNCHEON)

(MY BRIEFING FROM THE JOINT CHIEFS OF STAFF),

(PANW), (PHO), (HACK), (FXI), (RSX),

(TESTIMONIAL)

Palo Alto Networks, Inc. (PANW)

PowerShares Water Resources ETF (PHO)

PureFunds ISE Cyber Security ETF (HACK)

iShares China Large-Cap (FXI)

Market Vectors Russia ETF (RSX)

Global Market Comments

April 20, 2015

Fiat Lux

Featured Trade:

(JUNE 22 WASHINGTON DC GLOBAL STRATEGY LUNCHEON)

(WHERE THE ECONOMIST BIG MAC INDEX FINDS CURRENCY VALUE),

(FXF), (FXE), (FXA), CYB)

(THE FALLING MARKET FOR KIDS),

(HOLLYWOOD CASHES IN ON WALL STREET TROUBLES)

CurrencyShares Swiss Franc ETF (FXF)

CurrencyShares Euro ETF (FXE)

CurrencyShares Australian Dollar ETF (FXA)

WisdomTree Chinese Yuan Strategy ETF (CYB)

Global Market Comments

April 17, 2015

Fiat Lux

Featured Trade:

(SPECIAL NOTE FOR MY APRIL 17 INCLINE VILLAGE GUESTS)

(LAS VEGAS WEDNESDAY MAY 8 GLOBAL STRAGEGY LUNCHEON)

(THE PORTFOLIO THAT WILL DOUBLE IN THREE YEARS)