Featured Trade: (THE GREAT AMERICAN ROT IS ENDING), (SPY), (TLT), (FXY), (FXE), (USO)

SPDR S&P 500 ETF (SPY) iShares 20+ Year Treasury Bond (TLT) CurrencyShares Japanese Yen ETF (FXY) CurrencyShares Euro ETF (FXE) United States Oil ETF (USO)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-02-02 09:34:252015-02-02 09:34:25February 2, 2015

Featured Trade: (FEBRUARY 4 GLOBAL STRATEGY WEBINAR), (SIGN UP NOW FOR TEXT MESSAGING OF TRADE ALERTS), (QCOM), (SPY), (THE CHINA VIEW FROM 30,000 FEET) (FXI), (DBC), (DYY), (DBA), (PHO)

QUALCOMM Incorporated (QCOM) SPDR S&P 500 ETF (SPY) iShares China Large-Cap (FXI) PowerShares DB Commodity Tracking ETF (DBC) PowerShares DB Commodity Double Long ETN (DYY) PowerShares DB Agriculture ETF (DBA) PowerShares Water Resources ETF (PHO)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-01-30 01:07:462015-01-30 01:07:46January 30, 2015

It seems that the harder I work, the luckier I get.

Last week I made a bet that companies with a high share of international business would be punished severely during earnings season.

Specifically, I picked QUALCOMM (QCOM), the San Diego based maker of processors for cell phones, tablets, and laptops, because it had the highest percentage of foreign earnings among the S&P 500.

Three days later, after years of dawdling, the European Central Bank announced a particularly aggressive form of quantitative easing that sent the Euro crashing. You might as well have sent a torpedo directly into QUALCOMM?s bottom line.

The company?s Q4 earnings report, announced after the Tuesday close, confirmed my worst fears. While the earnings held up surprisingly well, the second half guidance was downright apocalyptic.

The stock immediately gapped down to $65 in the aftermarket, off some 8%, in a heartbeat.

Foreign earnings are a great place to hide when the greenback is soggy. It is a terrible place to be when the buck is moving from strength to strength, as it has for the past eight months.

It turns out that there is much more that is wrong under the hood at QUALCOMM than the recent collapse of the Euro and the Yen.

Much of the meteoric growth of Apple?s (AAPL) iPhone 6 sales in recent months has been at the expense of Samsung and other competitors. I hate to say ?I told you so? but I have been predicting this all along.

While QUALCOMM sells to both companies, particularly its Snapdragon 800 quadcore processor, it gets a lesser share of the profits on its sales to Apple. QUALCOMM is therefore, effectively, an indirect short position in Apple.

Oops!

I think you can take QUALCOMM?s woeful stock performance today as a warning that there is more suffering to come on the foreign earnings front by other companies yet to report.

For more depth on this, please read yesterday?s piece on ?The Unintended Consequences of the Euro Crash? by clicking here.

As for the happy holders of my recommended QUALCOMM (QCOM) February, 2015 $75-$80 in-the-money bear put spread, good for you! You have just made a nearly instant 2.25% profit on your total portfolio in a mere seven trading days. That works out to a gain of 22% on this single position.

There is no point in running this position the remaining three weeks into the February 20 expiration, as you have already reaped 95% of the potential profit. Better to free up the cash to roll into a new position, while simultaneously reducing your risk.

Or, you could simply take a long vacation from the miserable, unforgiving market.

There Goes QUALCOMM?s Earnings

https://www.madhedgefundtrader.com/wp-content/uploads/2015/01/Ship-e1422539739992.jpg262400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-01-29 09:10:192015-01-29 09:10:19Qualcomm Guidance Crushes Stock

Featured Trade: (THE UNINTENDED CONSEQUENCES OF THE EURO CRASH), (FXE), (EUO) (CAT), (PG), (MSFT), (M), (FDO), (COST), (TGT), (WMT) (RSP), (QQQ), (IWM) (WATCH OUT FOR THE HEAD AND SHOULDERS) (SPY), (QQQ), (TLT), (FXE), (FXY), (GLD), (SLV)

CurrencyShares Euro ETF (FXE) ProShares UltraShort Euro (EUO) Caterpillar Inc. (CAT) The Procter & Gamble Company (PG) Microsoft Corporation (MSFT) Macy's, Inc. (M) Family Dollar Stores Inc. (FDO) Costco Wholesale Corporation (COST) Target Corp. (TGT) Wal-Mart Stores Inc. (WMT) Guggenheim S&P 500 Equal Weight ETF (RSP) PowerShares QQQ Trust, Series 1 (QQQ) iShares Russell 2000 (IWM) SPDR S&P 500 ETF (SPY) iShares 20+ Year Treasury Bond (TLT) CurrencyShares Japanese Yen ETF (FXY) SPDR Gold Shares (GLD) iShares Silver Trust (SLV)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-01-28 11:36:082015-01-28 11:36:08January 28, 2015

For those of you who heeded my expert advice to buy the ProShares Ultra Short Euro ETF (EUO) last July, well done!

You are up a massive 48%! This is on a move in the underlying European currency of only 18.5%.

My browsing of the Galleria in Milan, the strolls through Spanish shopping malls, and my dickering with an assortment of dubious Greek merchants, all paid off big time. It turns out that everything I predicted for this beleaguered currency came true.

The European economy did collapse. Cantankerous governments made the problem worse by squabbling, delaying and obfuscating, as usual.

The European Central Bank finally threw in the towel and did everything they could to collapse the value of the Euro and reinvigorate their comatose economies. This they did by imitating America?s wildly successful quantitative easing, which they announced with local variations last Thursday.

And now for the good news: The best is yet to come!

Europe is now six days into a strategy of aggressive monetary easing which may take as long as five years until it delivers tangible, sustainable results. That?s how long it took for the Federal Reserve?s QE to restore satisfactory levels of confidence in the US economy.

The net net is that we have almost certainly only seen the first act of a weakening of the Euro which may last for years. A short Euro could be the trade that keeps on giving.

The ECB?s own target now is obviously parity against the greenback, which you will find predicted in my own 2015 Annual Asset Class Review released at the beginning of January (click here).

Once they hit that target, 87 cents to the Euro will become the new goal, and that could be achieved sooner than later.

However, you will not find me short the Euro up the wazoo this minute. I think we have just stumbled into a classic ?Buy the Rumor, Sell the News? situation with the Euro.

The next act will involve the ECB sitting on its hands for a year, realizing that their first pass at QE was inadequate, superficial, and flaccid, and that it is time to pull the bazooka out of their pockets once again.

This is a problem when the entire investment world is short the Euro. That paves the way for countless, rip your face off short covering rallies in the months ahead. Any smidgeon or blip of positive European economic data could spark one of these.

Trading the Euro for the past eight months has been like falling off a log. It is about to get dull, mean and brutish. So for the moment, my currency play has morphed into selling short the Japanese yen, which has its own unique set of problems.

As for the unintended consequences of the Euro crash, the Q4 earnings reports announced so far by corporate America tells the whole story.

Companies with a heavy dependence on foreign (read Euro and yen) denominated earnings are almost universally coming up short. On this list you can include Caterpillar (CAT), Procter and Gamble (PG), and Microsoft (MSFT).

Who are the winners in the strong dollar, weak Euro contest? US companies that see a high proportion of their costs denominated in flagging foreign currencies, but see their incomes arrive totally in the form of robust, virile dollars.

You may not realize it, but you are playing the global currency arbitrage game every time you go shopping. The standout names here are US retailers, which manufacture abroad virtually all of the junk they sell you here, especially in low waged China.

The stars here are Macy?s (M), Family Dollar Stores (FDO), Costco (COST), Target (TGT), and Wal-Mart (WMT).

You can see this divergence crystal clear in examining the behavior of the major stock indexes. The chart for the Guggenheim S&P 500 Equal Weight ETF (RSP), which has the greatest share of currency sensitive multinationals, looks positively dire, and may be about to put in a fatal ?Head and Shoulders? top (see the following story).

The chart for the NASDAQ (QQQ), where constituent companies have less, but still a substantial foreign currency exposure, appears to be putting in a sideways pennant formation before eventually breaking out to new highs once again.

The small cap Russell 2000, which is composed of almost entirely domestic, dollar based, ?Made in America? type companies, is by far the strongest index of the trio, and looks like it is just biding time before it blasts through to new highs.

If you are a follower of my Trade Alert Service, then you already know that I have a long position in the (IWM), which has already chipped in 2.12% to my 2015 performance.

You see, there is a method to my Madness.

Never Underestimate the Value of Research

https://www.madhedgefundtrader.com/wp-content/uploads/2015/01/John-Thomas1-e1422462857973.jpg302400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-01-28 11:35:022015-01-28 11:35:02The Unintended Consequences of the Euro Crash

Featured Trade: (MORE PAIN TO COME IN OIL) (USO), (XOM), (OXY), (COP), (DAL) (THE SERVICE JOB IN YOUR FUTURE), (MCD)

United States Oil ETF (USO) Exxon Mobil Corporation (XOM) Occidental Petroleum Corporation (OXY) ConocoPhillips (COP) Delta Air Lines, Inc. (DAL) McDonald's Corp. (MCD)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-01-27 10:54:442015-01-27 10:54:44January 27, 2015

There are very few people I will drop everything to listen to. One of the handful is Daniel Yergin, the bookish founder and CEO of Cambridge Energy Research Associates, the must-go-to source for all things energy.

Daniel received a Pulitzer Prize for The Prize: The Epic Quest for Oil, Money, and Power, a rare feat for a non-fiction book (I?ve never been able to get one).

Suffice it to say that every professional in the oil industry, and not a few hedge fund traders, have devoured this riveting book and based their investment decisions upon it.

Yergin thinks that the fracking and horizontal drilling revolutions have made the United States the new swing producer of oil. There is so much money in the investment pipeline that American oil production will continue to increase for the next six months, by some 500,000 barrels a day.

This new supply will run head on into the seasonal drop in demand for energy, when spring ritually reduces heating bills, but the need for air-conditioning has not yet kicked in.

The net net could be a further drop in the price for Texas tea from the present $45 a barrel, possibly a dramatic one.

Yergin isn?t predicting any specific oil price as a potential floor, as it is an impossible task. While OPEC was a monolithic cartel, the US fracking industry is made up of thousands of mom and pop operators, and no one knows what anyone else is doing. However, he is willing to bet that the price of oil will be higher in a year.

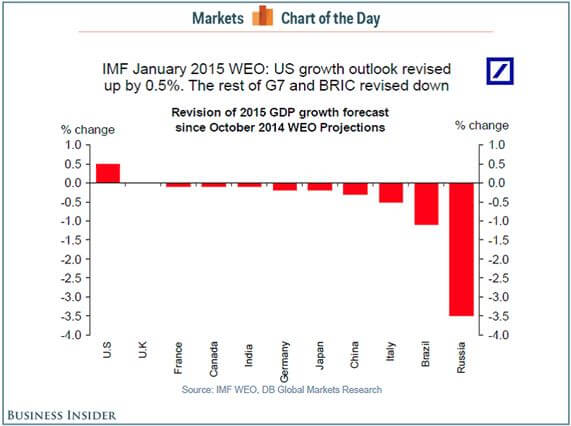

Currently, the 91 million barrel global market for oil is oversupplied with 1 million barrels a day. That includes the 2 million b/d that has been lost from disruptions in Libya, Syria and Iraq.

If the International Monetary Fund is right, and the world adds 3.8% in economic growth this year, we will soak up 1.1 million b/d of that with new demand. In the end, the oil price collapse is a self-solving problem. The new economic growth engendered by ultra low fuel prices eventually drives prices higher.

Where we reach the tipping point, and the oil market comes back into balance, is anyone?s guess. But when it does, prices will go substantially higher. The cure for low prices is low prices.

The bottom line is that there will be a great time to buy oil companies, but it is not yet.

What we are witnessing now is the worst energy crash since the 1980?s, when new supplies from the North Sea, Mexico and Alaska all hit at the same time. The price of oil eventually crashed from $42 to $8.

I remember it well, because Morgan Stanley then set up a private partnership that bought commercial real estate in Houston for ten cents on the dollar. The eventual return on this fund was over 1,000%.

This time it is more complicated. Prices lived over $100 for so long that it sucked in an unprecedented amount of capital into new drilling, some $100 billion worth. As a result, sources were brought online from parts of the world as diverse as Russia, the Arctic, Central Asia, Africa, the Canadian tar sands and remote and very expensive offshore platforms.

Yergin believes that Saudi Arabia can survive for three years with prices at current levels. After that, it will burn through its $150 billion of foreign exchange reserves, and could face a crisis. Clearly, the Kingdom is betting that prices will recover with its market share based strategy before then. They are playing for the long haul.

The transition of power to the new King Salman was engineered by a committee of senior family members, and has been very orderly. However, King Salman, a Sunni, will have his hands full. The current takeover of Yemen by a hostile Shiite minority, the Houthis, is a major concern. Yemen shares a 1,100 mile border with Saudi Arabia.

Daniel says that a year ago, there was a lot of geopolitical risk priced into oil, with multiple crises in the Ukraine, Syria, Libya and Iraq frightening consumers, so trading levitated over $100 for years. Delta Airlines Inc. (DAL) even went to the length of buying its own refiner to keep fuel prices from rising further.

US oil producers have a unique advantage over competitors in that they can cut costs faster than any other competitors in the world. On the other hand, they are eventually going head to head against the Saudis, whose average cost of production is a mere $5/barrel.

A native of my own hometown of Los Angeles, Yergin started his professional career as a lecturer at Harvard University. He founded Cambridge Energy in 1982 with a $7.00 investment in a file cabinet at the Good Will. He later sold Cambridge Energy to the consulting group IHS Inc. for a small fortune.

To buy The Prize at discount Amazon pricing, please click here.

https://www.madhedgefundtrader.com/wp-content/uploads/2015/01/The-Prize-e1422373144707.jpg480320Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-01-27 10:53:482015-01-27 10:53:48More Pain to Come in Oil

I was fascinated by the recent comments made by Union Pacific (UNP) CEO, Jack Koraleski, about the current robust health of his company.

Fourth quarter profits rocketed by an amazing 22% and those stellar numbers look set to continue.

I love railroads, not because they used to belch smoke and steam and have these incredibly loud, romantic, wailing whistles. In fact, my first career goal in life (when I was 5) was to become a train engineer.

It turns out that the railroads are also a great proxy for the health of the entire US economy. They are, in effect, our canary in the coalmine.

Jack sees moderate economic growth in the US continuing. Demand for the heavy products the company shifts is booming. Construction products like stone, gravel, cement and lumber, are up 10%.

The dramatic plunge in oil prices brings positives and negatives. The boom in oil shipments from North Dakota has been a windfall for the railroads that may now ebb.

But if prices stay low enough for long enough, it will boost demand for everything else that the Union Pacific ships, including houses, furniture, cars and every other sweet spot for their franchise. (UNP), in effect, has a great internal hedge for its many businesses. When one product line weakens, another strengthens. This has been going on forever.

The company is watching carefully the construction of a second Panama Canal across Nicaragua (the subject of a future article, when I get some time).

If completed by its Chinese promoters within the next decade, it could bring a tiny incremental shift of traffic from the US west coast to the Gulf ports. Even this is a mixed bag, as this will move some business away from strike plagued ports that are currently causing so much trouble.

When I rode Amtrak?s California Zephyr service from Chicago to San Francisco last year, I passed countless trains heading west, hauling hoppers full of coal for shipment to China.

This year I took the same trip. The coal trains were gone. Instead I saw 100 car long tanker trains transporting crude oil from North Dakota south to the Gulf Coast. I thought, ?There?s got to be a trade here?. It turns out I was right.

Take a look at the charts below, and you will see that the shares of virtually the entire railroad industry are breaking out to the upside.

In two short years, the big railroads have completely changed their spots, magically morphing from coal plays to natural gas ones. You?ve heard of ?fast fashion?? This is ?fast railroading?.

Today the big business is coming from the fracking boom, shipping oil from North Dakota?s Bakken field to destinations south. In fact, the first trainload of Texas tea arrived here in the San Francisco Bay area only a year ago, displacing crude that formerly came from Alaska.

Look at the share prices of the major listed railroads, and it is clear they have been chugging right along to produce one of the best performances of 2013. These include Union Pacific (UNP), CSX Corp (CSX), Norfolk Southern (NSC), and Canadian Pacific (CP). In the meantime, competing coal shares, like Arch Coal (ACI) have been one of the worst performing this year.

Those of a certain age, such as myself, remember railroads as one of the great black holes of American industry. During the sixties, they were constantly on strike, always late, and delivered terrible service.

A friend of mine taking a passenger train from New Mexico to Los Angeles found his car abandoned on a siding for 24 hours, where he froze and starved until discovered.

New airlines and the trucking industry were eating their lunch. They also hemorrhaged money like crazy. The industry finally hit bottom in 1970, when the then dominant Penn Central Railroad went bankrupt, freight was spun off, and the government owned Amtrak passenger service was created out of the ashes. I know all of this because my late uncle was the treasurer of Penn Central.

Fast forward nearly half a century and what you find is not your father?s railroad. While no one was looking, they quietly became one of the best run and most efficient industries in America. Unions were tamed, costs slashed, and roads were reorganized and consolidated.

The government provided a major assist with a sweeping deregulation. It became tremendously concentrated, with just four roads dominating the country, down from hundreds a century ago, giving you a great oligopoly play. The quality of management improved dramatically.

Then the business started to catch a few lucky breaks from globalization. The China boom that started in the nineties created enormous demand for shipment inland of manufactured goods from west coast ports.

A huge trade also developed moving western coal out to the Middle Kingdom, which now accounts for 70% of all traffic. The ?fracking? boom is having the same impact on the North/South oil by rail business.

All of this has ushered in a second ?golden age? for the railroad industry. This year, the industry is expected to pour $14 billion into new capital investment. The US Department of Transportation expects gross revenues to rise by 50% to $27.5 billion by 2040. The net net of all of this is that freight rates are rising right when costs are falling, sending railroad profitability through the roof.

Union Pacific is investing a breathtaking $3.6 billion to build a gigantic transnational freight terminal in Santa Teresa, NM. It is also spending $500 million building a new bridge across the Mississippi River at Canton, Iowa. Lines everywhere are getting double tracked or upgraded. Mountain tunnels are getting rebored to accommodate double-stacked sea containers.

Indeed, the lines have become so efficient, that overnight couriers, like FedEx (FDX) and UPS (UPS), are diverting a growing share of their own traffic. Their on time record is better than that of competing truckers, who face delays from traffic jams and crumbling roads, and are still hobbled by antiquated regulation.

I have some firsthand knowledge of this expansion. Every October 1, I volunteer as a docent at the Truckee, California Historical Society on the anniversary of the fateful day in 1846 when the ill-fated Donner Party was snowed in.

There, I guide groups of tourists over the same pass my ancestors crossed during the 1849 gold rush. The scars on enormous ancient pines made by passing wagon wheels are still visible.

During 1866-1869, thousands of Chinese laborers blasted a tunnel through a mile of solid granite to complete the Transcontinental Railroad. I can guide my guests through that tunnel today with flashlights because (UNP) moved the line to a new tunnel a mile south to improve the grade. The ceiling is still covered with soot from the old wood and coal-fired engines.

While the rebirth of this industry has been impressive, conditions look like they will get better still. Massive international investment in Mexico (low end manufacturing and another energy renaissance) and Canada (natural resources) promise to boost rail traffic with the US.

The rapidly accelerating ?onshoring? trend, whereby American companies relocate manufacturing facilities from overseas back home, creates new rail traffic as well. It turns out that factories that produce the biggest and heaviest products are coming home first, all great cargo for railroads.

And who knew? Railroads are also a ?green? play. As Burlington Northern Railroad owner, Warren Buffett never tires of pointing out, it requires only one gallon of diesel fuel to move a ton of freight 500 miles. That makes it four times more energy efficient than competing trucks.

In fact, many companies are now looking to railroads to reduce their overall carbon footprints. Warren doesn?t need any convincing himself. The $34 billion he invested in the Burlington Northern Railroad two years ago has probably

doubled in value since then.

You have probably all figured out by now that I am a serious train nut, beyond the industry?s investment possibilities. My past letters have chronicled adventures riding the Orient Express from London to Venice, and Amtrak from New York to San Francisco.

I even once considered buying my own steam railroad; the fabled ?Skunk? train in Mendocino, California, until I figured out that it was a bottomless money pit. Some 50 years of deferred maintenance is not a pretty sight.

It gets worse. Union Pacific still maintains in running condition some of the largest steam engines every built, for historical and public relations purposes. One, the ?Old 844? once steamed its way over the High Sierras to San Francisco on a nostalgia tour.

The 120-ton behemoth was built during WWII to haul heavy loads of steel, ammunition and armaments to California ports to fight the war against Japan. The 4-8-4-class engine could pull 26 passenger cars at 100 mph.

When the engine passed, I felt the blast of heat of the boiler singe my face. No wonder people love these things! To watch the video, please click here and hit the ?PLAY? arrow in the lower left hand corner. Please excuse the shaky picture.

I shot this with one hand, while using my other hand to restrain my over excited kids from running on to the tracks to touch the laboring beast.

00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-01-26 01:04:452015-01-26 01:04:45Will the Oil Bust Kill the Railroads?

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.