October 25, 2023

(FINDING DEFENSIVE AND STABLE STOCKS AMONGST CHANGING GLOBAL FORCES)

October 25, 2023

Hello everyone,

There are many events taking place right now that will inevitably reshape the world in the near future.

Political instability, Climate change, advances in technology, government debt, and wars that may shift power dynamics amongst world powers are all playing out concurrently.

In five years, we could see a radically different world.

So, how do you cope with all these changes in relation to your stock market holdings?

You play defensive and lock in stable stocks. Let’s look at the three stocks here.

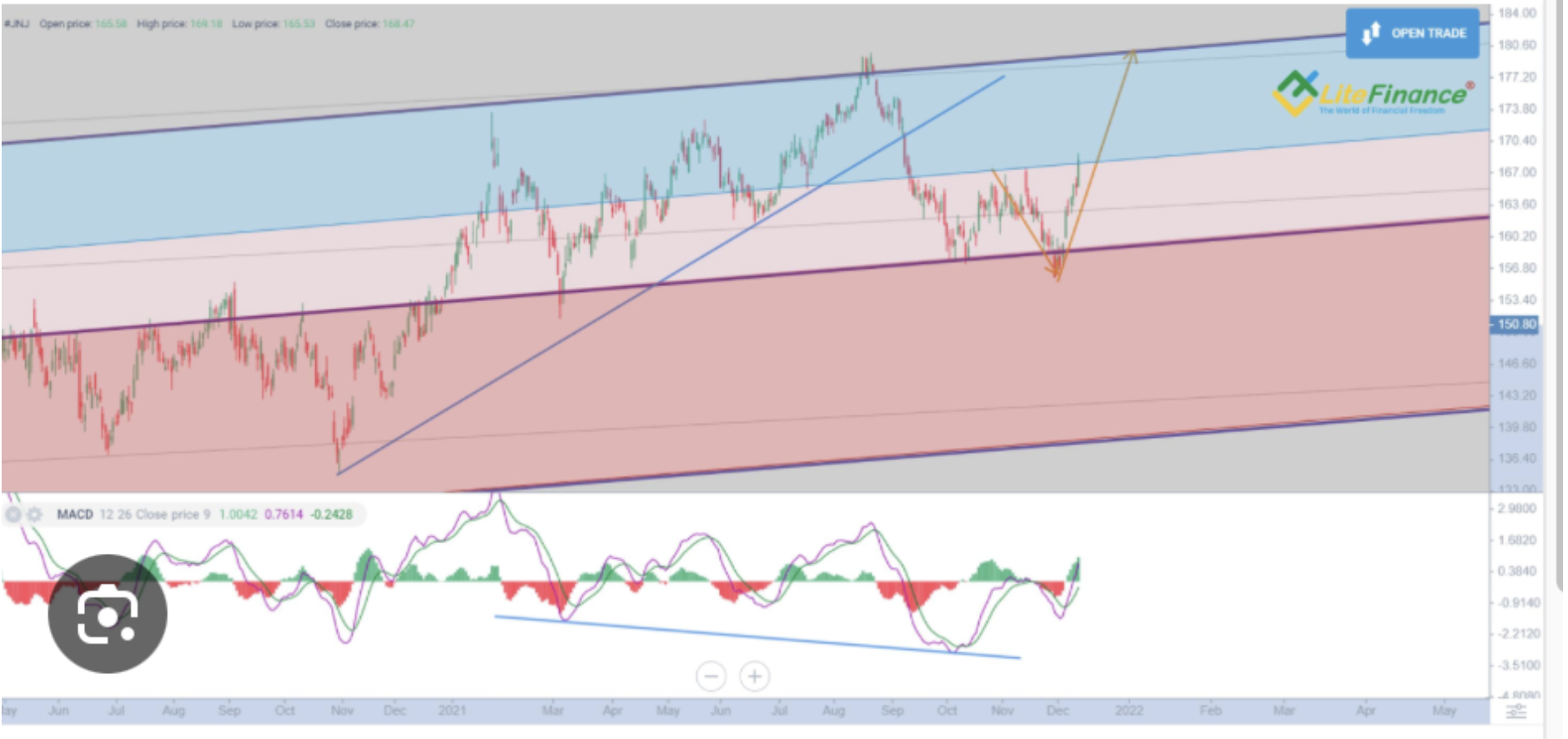

Johnson and Johnson (JNJ)

1/ It’s undervalued. 13% decline this year.

2/ 3% dividend. 60+ years of dividend growth.

3/ Extensive portfolio of medicines & medical devices.

4/ Analysts predict JNJ stock price could reach $168 by October 2024 & $187 in 2028.

5/ For the 21st year in a row, Fortune has named Johnson & Johnson as a Top 50 All-Star on its list of the World’s Most Admired Companies.

What could go wrong?

JNJ is facing legal action on its talc powder, opioid drugs, and surgical mesh products that could cost the company a lot of money, and impact sentiment on the company.

Earnings results:

Topped quarterly earnings and revenue estimates.

EPS: $2.66 vs $2.52 expected

Revenue: $21.35 billion vs. $21.04 billion expected.

Lifts full-year guidance as MedTech and pharmaceutical sales jump.

Johnson and Johnson stock forecast & price prediction for 2023 & 2024 & beyond.

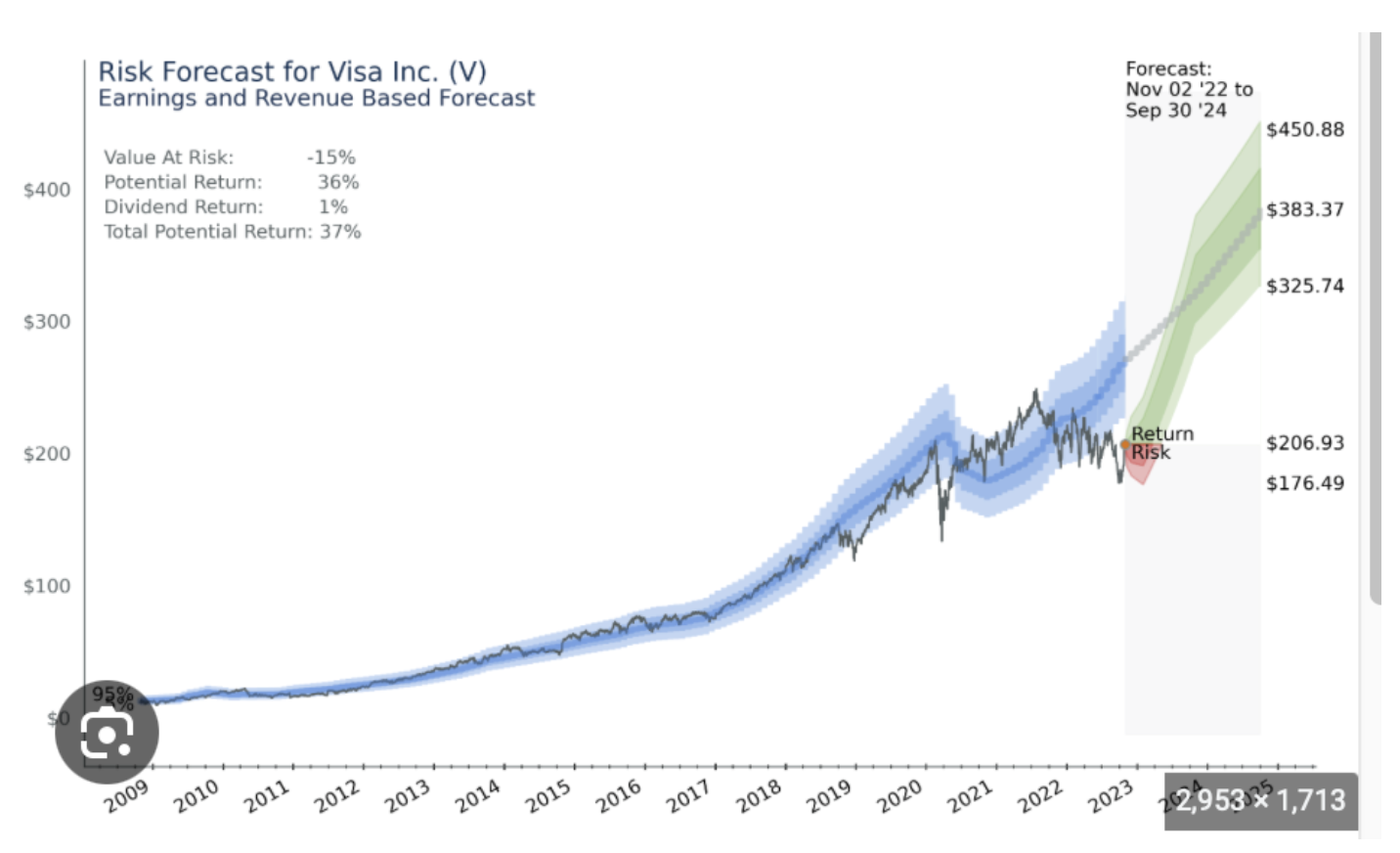

Visa (V)

1/ Dominant force in digital payments. Strong financial position. Healthy balance sheet.

2/ Proactively involved with fintechs.

3/ 0.76% dividend.

4/ 61% share of the credit card market.

5/ Visa is less volatile than 75% of U.S. stocks over the last three months.

6/ EPS have increased by around 20% a year over the last 5 to 10 years.

7/ Visa works with businesses in new and evolving industries, including fintech platforms, crypto projects, and content creators. These programs may help it find traction in new areas of growth.

8/ Credit and debit card penetration in emerging markets is still low, but disposable incomes are increasing. A possible growth opportunity for Visa.

7/ Analysts predict Visa stock price could rise to $250 by the end of 2024 and $300 by the end of 2025 and be at $500 in 2030.

What could go wrong?

- A severe recession resulting in lower payment volumes.

- Competing technologies taking market share from Visa.

- Growth opportunities missed due to regional networks/alternative payment systems.

- Regulators ending the Visa/Mastercard duopoly impacting fees.

Earnings Results:

Posted better than expected fiscal Q4 earnings and revenue as payments volume, cross-border volume, and payment transactions stayed resilient.

Visa boosted its dividend by 16%.

The company announced a $25 billion stock buyback.

Net revenue for the quarter climbed to $8.61B, topping the $8.55B consensus estimate.

Alphabet (GOOGL)

1/ Google has a monopoly on Search. At 93% worldwide market share, the company is well-positioned to profit from the search industry’s expansion in the coming years.

2/ The company has huge profit margins.

3/ Digital ad sales are set to rise. (Analysts argue that the digital ad market will grow by nearly 50% to $910 billion by 2027).

4/ Google Cloud will soon become a profitable vehicle. Google Cloud is the third largest provider of cloud infrastructure services, behind only Amazon Web Services and Microsoft’s Azure. Its highly regarded data analytics capabilities will advance Google Cloud’s growth. The cloud computing market is expected to exceed $1.5 trillion by 2030, according to Grand View Research, so Google Cloud is well positioned to be Alphabet’s next major profit driver.

4/ Stock buyback initiative.

5/ Analysts predict that the stock price could rise to around $490 by 2030.

What could go wrong?

a) Google faces headline risks over anti-trust lawsuits.

b) Regulatory challenges.

c) The company loses the AI war against rival Microsoft.

d) Google’s overreliance on advertising business (may soften during a recession)

Earnings Results:

11% revenue growth in the third quarter.

Shares dropped around 7% in extended trading – the cloud business missed analysts’ expectations. Cloud revenue came in below estimates at $8.41 billion, missing the mark by more than $20 million. Once Google Cloud becomes profitable it will propel the shares much higher.

Stock price forecasts for Google in 2023, 2024 and beyond.

Happy Wednesday to you all.

Cheers

Jacquie