October Nonfarm Payroll Surprise Points to Market Upside

The October nonfarm payroll came in at a pedestrian 80,000, compared to 158,000 in September, a rate that is somewhat less than what matches population growth. But it is the numbers behind the numbers that will deliver the big market impact. The headline unemployment rate came in at a nosebleed 9.0%.

August and September were revised up a whopping 102,000. This is final proof that the recession that the market was discounting over September and early October was never there, a point which I have been arguing about vociferously. The recession was only in the stock market.

What was particularly fascinating was the massive decline in the long term unemployed, by 366,000, the largest since records began in 1948. This took the expanded U-6 unemployment rate, which includes discouraged workers and those whose benefits have expired, from 16.5% down to 16.2 %. I have never seen anything like this, and have no idea what caused it. But the overall message about the economy has to be good.

October saw a pop of 104,000 in hiring by the private sector, partially offset by a loss of 24,000 government jobs, a continuation of what will be a decade long trend. Gains were seen by business and professional services (32,000), leisure and hospitality (22,000), and health care (12,000). Further losses of 20,000 were seen in construction. Since the beginning of 2010, an impressive 3 million jobs have been created by the private sector.

Another sobering statistic buried in the raft of figures was that, of the 80,000 hired, a shocking 42,000 were of people who were taking on second full time jobs! This is additional evidence that the only way that minimum wage workers can support families is by working 16 hours a day at two jobs. Even still, that only gets you earnings of $33,280 a year, pretax, and will certainly be more ammunition for the ?Occupy Wall Street? crowd.

Taken together with a sudden decline in weekly jobless claims to 397,000, and improvement in other employment data, an improving jobs market emerges out of the mist. They suggest an employment picture that has stopped deteriorating, is stabilizing, and beginning a modest upturn. These are economic conditions far better than the financial markets are currently discounting, and are consistent with the 2.0%-2.5% GDP growth rate that I have been sticking to all year.

At the beginning of the year I have been asserting that the economy was growing at a 2% rate, not 4%. Now I have to convince people that it is growing at 2%, not zero. This difference equates to about 300 points in the S&P 500.

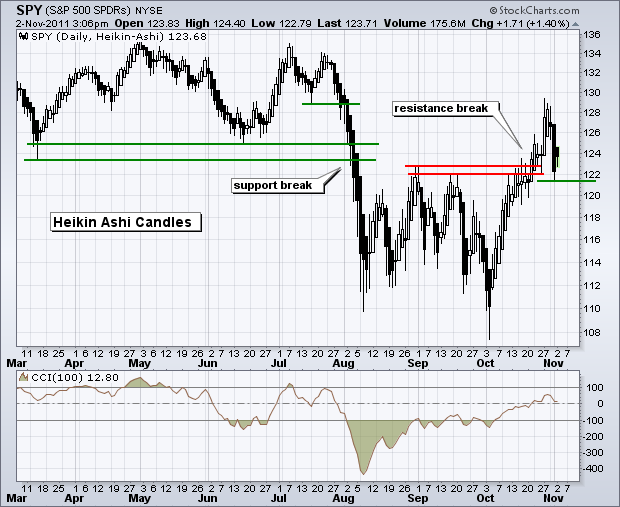

Take this data, and throw it in with fading turmoil in Europe and a budget Supercommittee surprise, and you will have a springboard for the S&P 500 to break through upside resistance at the 200 day moving average.