Should I Buy Cloud Firm Okta in April?

The excess liquidity fueling the U.S. financial markets signal that investors are picking up the tab for heavy loss-making tech companies like never before.

Only in the U.S. can this happen at the scale it is happening as the U.S. controls its own currency, Central Bank, and possess the most reliable IPO process.

This phenomenon effectively supports a mindset of tech start-ups putting off profits for years and sometimes even decades.

Too much money chasing too few ideas and we have seen numerous examples of this with investors turning to ultra-leverage to figure out how to deliver real gains to investors.

Another heavy loss-making cloud company that I recommended buying “at the bottom” last March was identity-verification software maker Okta (OKTA) whose business was dramatically uplifted from the shift to remote work during the pandemic.

The recommendation worked like a charm with the stock essentially doubling from the time of that call.

But what’s in store for this password company moving forward?

First, let's rewind to the beginning of March when investors dumped the stock after a disappointing 2022 forecast and suffered from rumblings of the company paying too much to acquire Auth0 for about $6.5 billion.

The 30% sell-off was another example of growth companies’ ugly habit of volatility making it hard to time the entry points for heavy pocketed investors.

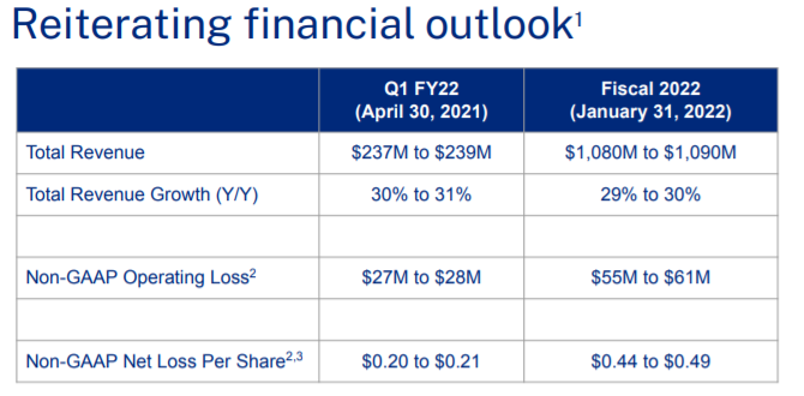

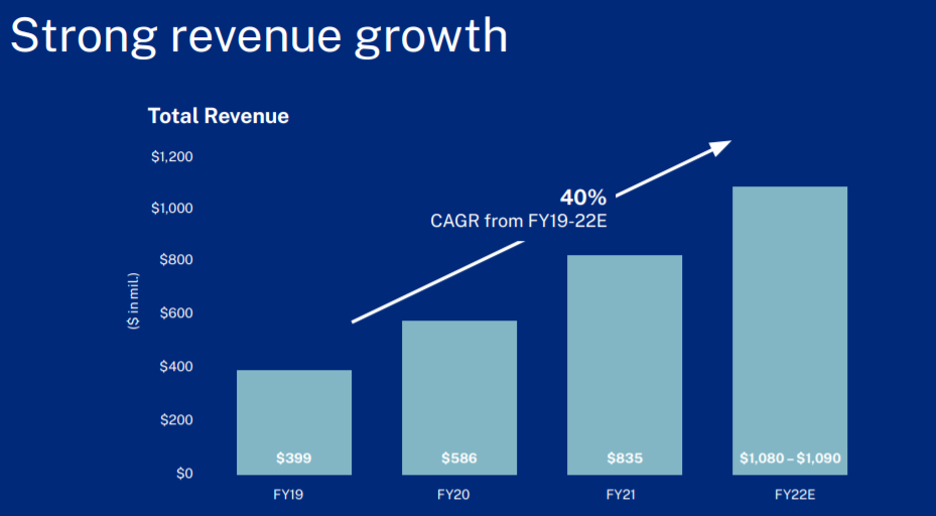

In the most recent analysts’ day, Okta projected sales will grow 30% in each of the next three years.

Revenue at the end of fiscal 2024 will be close to an annualized $2 billion, or about $500 million for the fourth quarter that year.

Yes, this is still a small company by any metric.

Demand for the software maker’s products, which help workers access corporate systems and consumers authenticate their identity online, has increased as more employees logged on from home in 2020.

For the 12 months through March 1, Okta was used more than 52 billion times to log into an app or website, almost 200% growth from the same period a year earlier.

Okta has retraced some of its losses when it announced it introduce 2 new products.

One, Identity Governance Administration, generates reports which show in an organization who has permission to see which parts of its systems.

The idea is to make sure people who’ve left the company or have changed roles don’t retain access to unauthorized areas.

Next, Privileged Access Management, governs who can view and change an organization’s critical systems.

The new areas expand the size of Okta’s total addressable markets to about $80 billion.

Management said these protections have become more critical as employees continue to work for home.

Many data breaches come down to server accounts that weren’t locked down when they should have been.

Admins change jobs at a rapid pace as companies look to poach talent more than ever now.

If it wasn’t the cause of the breach, it was a vector that the attackers used once they got in.

Being the cloud growth company it is, with only a market capitalization of $30 billion, the new announcements was the catalyst for Okta shares to surge 8% during intraday trading.

This is typical growth company price action.

The company is also dogged by persistent rumors it might sell to a larger tech company and I would say it’s a little surprising that the company is “buying growth” at such an early stage of its growth cycle.

But again, the subsidies keep flowing to these upstart tech guys because liquidity levels and bold risk appetites allow these types of aggressive financing that affect management decisions.

Overpaying to grow is where we are now in the tech cycle with the Central Bank effectively not allowing this bull market to die.

Okta CEO Todd McKinnon said he wants it to be one of five or six independent software clouds that every company needs.

And I also want to be one of five or six men in the world that every girl in the world wants to date.

I get it that McKinnon wants identity and access to remain Okta’s specialty rather than being subsumed into one of the other categories. Microsoft, which has identity software products that predate its cloud businesses, is already Okta’s main rival.

I would agree that Okta is prime for investors to buy the dip, but I would recommend traversing to higher waters because there are better cash burning, cloud names out there that are growing faster than Okta.

Honestly, Okta should be growing more for its small size, and “buying growth” seems like they are worried about an imminent collapse of growth which is a worrying sign.

Yes, I must agree that competition is stiff these days in the cloud ecosystem.

My conclusion with Okta is that any investor looking to buy Okta should instead buy communications-as-a-cloud firm Twilio (TWLO).

This is the communications platform operating behind the scenes of behemoths like Airbnb and Uber.

They have a 3-year revenue growth rate of 66% and grew 65% year-over-year last quarter.

That is what I call consistent!

And that is what I call cash-burning growth!

TWLO is also exactly double the size of OKTA at $62 billion and is predicting next quarter to grow 44% to 47%.

According to IDC, investments in digital transformation will nearly double by 2023 to $2.3 trillion, representing more than 50% of total IT spending worldwide, and it’s clear to me that more of this capital will flow into TWLO than OKTA.

OKTA is just a one-trick pony, but TWLO is a complex integrated system that Uber can’t live without. Many companies can live without Okta and plug in a substitute. The revenue is just way stickier with TWLO, and the strategic position is superior.

OKTA is a solid buy the dip candidate, but just buy TWLO instead.