Ominous Sign for Tech Earnings

A market nostrum I religiously follow of not catching a falling knife could not resonate more with the current situation at streaming giant Netflix (NFLX).

The stock has imploded from $690 to $330 in less than 6 months.

November 2021 represented the high-water mark for many tech growth stocks and NFLX has been dragged into this mess as institutions and hedge funds rush to de-lever their tech portfolio as the panic of higher rates sets into the trading environment.

Does this mark the end to the NFLX model that was the darling of this bull market for so long?

Investors must grapple with this salient question.

NFLX must tap into the bond market to secure funding in order to supply us with high-quality content, so this question is really the crux of the issue.

We are certainly reaching an inflection point where many questions are still in need of answers.

As we approach NFLX’s earnings report tomorrow, the bar has been set extremely low for NFLX.

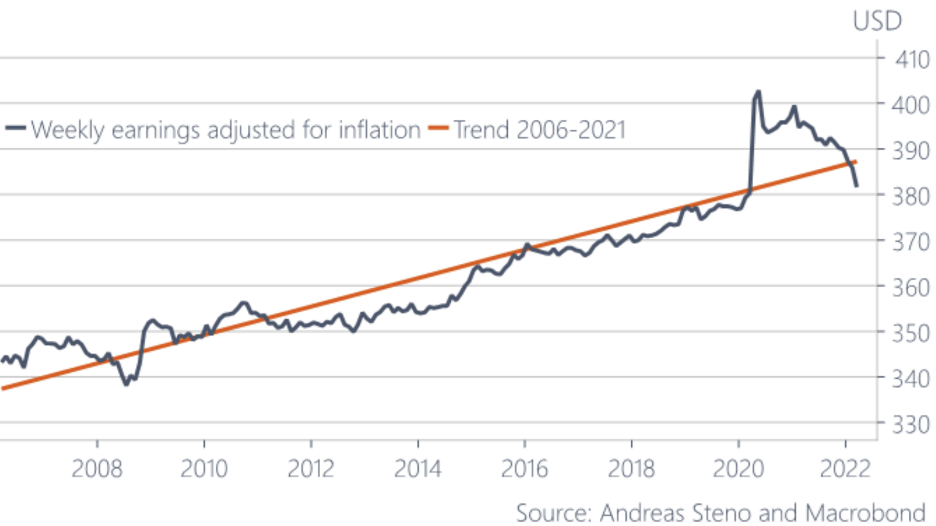

The backdrop is poor with weekly earnings adjusted for inflation decelerating at the fastest since the housing crisis of 2008.

There’s not a lot to look forward to in the tech world as higher expenses are destroying demand, delaying capital investments, and wage increases are depressing the bottom line at a time when supply chain bottlenecks are going from bad to awful.

NFLX is a product that isn’t essential to daily life like energy or food and non-essential services are the services that are getting cut in 2022.

NFLX also has a Russia problem as the company suspended operations in Russia on March 6 with no end in sight to when or if they might return.

Russia had 1 million NFLX subscribers which only represents a drop in the bucket of the 221 million total NFLX subscribers.

Therefore, I must say that the hit to the bottom line will be miniscule if anything.

However, this proves the point of NFLXs arduous slog through iterating in the emerging world. It’s not as easy when you enter a territory with different rules, currency, culture, and rule of law.

For instance, NFLX isn’t even allowed in China and India has fierce competition from local streaming bulwarks.

If they want to return to Russia, NFLX must first answer to breaking Russian law when they refused to abide by a new law that would require the streamer to include 20 "free-to-air" Russian State TV channels.

NFLX remains heavily focused on the emerging world as it looks to aggressively expand its footprint overseas. Four Russian originals were in the midst of production prior to the suspension. The projects have since been put on ice indefinitely.

Sadly, the saturation of NFLX’s cash cow in America and other rich Western democracies has reared its ugly head.

A multipronged revenue slowdown could spiral out of control.

The low-hanging fruit has been plucked and NFLX is still a model that relies on explosive growth to net the incremental subscriber.

It’s not working anymore and there is no plan B which could result in underperformance of the content quality.

Most of the bullishness in the stock’s price action coalesces around higher than expected subscription adds and without that, there is a dark future waiting for NFLX.

In addition to subscriber growth, analysts predict that management will have to answer other key questions, with a particular focus on business operations and profitability, the company's password sharing crackdown, gaming strategy, M&A, and more.

In the near term, NFLX’s guide is more important than ever.

In the heat of deglobalization, a leveraged globalized strategy triggers cognitive dissonance. A strategic reset is needed.

I can envision NFLX winning in some countries and losing in others, but to copy and paste that strategy to every emerging country, which usually has a weak rule of law, sounds like a recipe for continuous weak guidance in the new normal we are in.

Even more worrisome, as high inflation bites more at home, Americans might start to cut back on their NFLX and substitute it with free ads on YouTube and that’s the tail risk that’s not baked into the price of the stock yet.