Avoid the Softbank Vision Fund of Europe

Readers should stay away from investing in Prosus NV (PRX.AS).

Who is Prosus NV?

They are Europe's answer to Japan’s SoftBank (9984.T) and its Vision Fund, and they invest in tech startups all over the world including India, Latin America, and Europe.

To get more technical, they are essentially a registered Dutch company trading in Amsterdam as the international Internet assets division of South African multinational, Naspers.

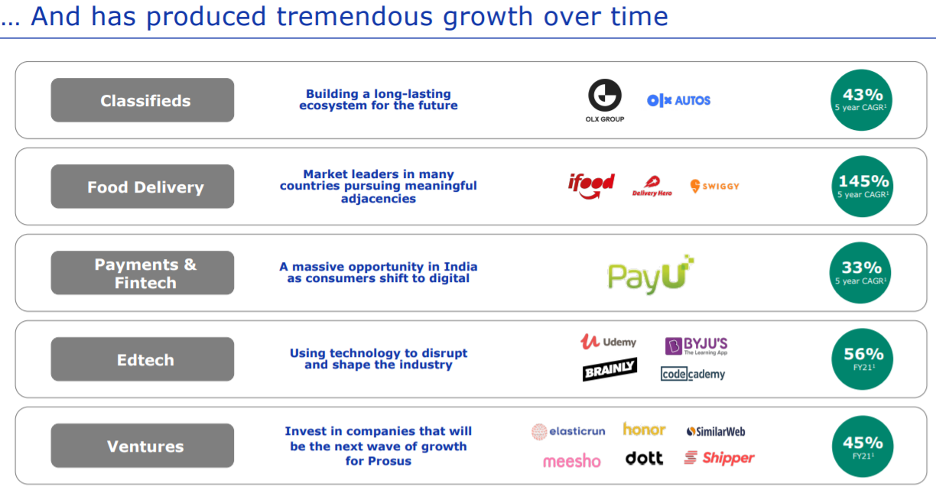

Naspers (NPNJn.J) spun out this division from South Africa in 2019 and owns stakes in consumer internet companies in online marketplaces, educational software, food delivery, and fintech.

They were once heralded for their 28.9% stake in China’s Tencent (0700.HK) but that investment has backfired as Chairman Xi has cracked down on local tech practices including data handling and youth video gaming.

Much like the Softbank Fund, which has seen its share of shocking investments, they are playing the long game through themes of accelerating artificial intelligence and achieving stakes before many companies ever go public.

Prosus has other meaningful investments in Russian tech services Mail.ru (LSE:MAIL), China’s Ctrip.com International Limited (CTRP), and Germany’s DeliveryHero.

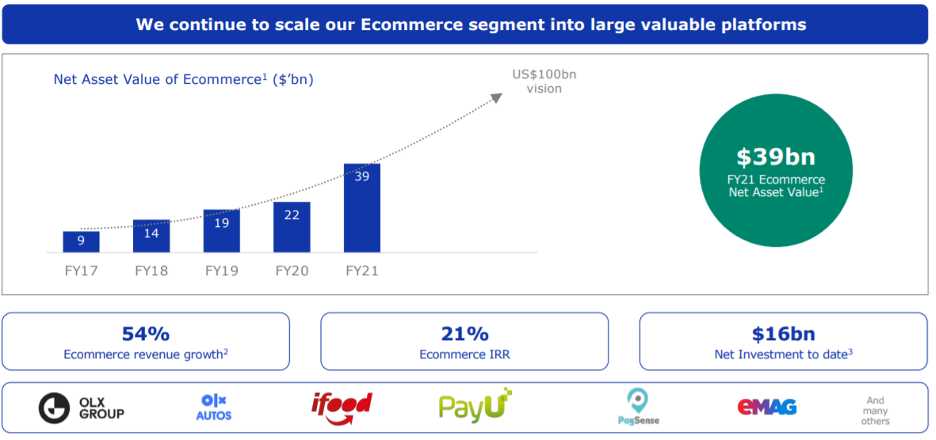

I can’t say I scratched my head when I heard that Prosus NV has agreed to acquire Indian online payments service BillDesk for $4.7 billion, making its largest global acquisition to date in the South Asian nation.

It’s typical behavior from Prosus.

The rapid growth of the payments industry worldwide has been helped by rising demand during the pandemic.

PayU processed $55 billion in payments in the year ended March 31, 2021, a 51% increase on the previous year.

BillDesk processed $92 billion of payments in the same period suggesting an acquisition price of more than 100 times earnings.

Prosus plans to combine BillDesk with PayU, its existing global fintech and payments business, which already has a strong presence in India.

The issue I have with this is the price that was paid, and the lack of value received; and Softbank has been guilty of the same cocktail of crimes.

Overpaying for Indian fintech — at about 20 times revenues.

I just don’t get it, to be frank.

But there should be significant synergies in combining the two businesses, as well as relatively high growth to come, given the attractiveness of the Indian payment market.

The deal to buy BillDesk, which was founded in 2000, is subject to regulatory approvals, including by the Competition Commission of India.

And that’s the thing; Indian regulators have almost adopted a hostile attitude towards foreign tech acquisitions, and rightly so.

India, aside from China, boasts the biggest army of tech workers in the world and regulators are increasingly viewing foreign takeovers as foreigners hijacking a domestic growth story before Indians can harness tech they built themselves.

Deals that have been pulled off run into red flags right away just from the owners not being locals, and this risk is real.

Prosus said Tuesday's acquisition brings the total it had invested in the Indian market to more than $10 billion.

Doubling down right here I feel is a little tone-deaf as to what’s happening in the broader balkanization of the global internet.

But I am not surprised that it’s Prosus, because their most notable investment is Tencent Holdings Ltd., and getting in on an Indian payments arena on the cusp of taking off looks good from far, but is it really when the Chinese tech industry has been crushed short-term?

More than 200 million more people will adopt digital payments there over the next three years, fueling a 10-fold increase in annual transactions per person to 220, Prosus said, citing Indian central bank estimates.

Investor interest in India is accelerating as Beijing pursues a campaign to rein in tech sectors from online commerce and fintech to gaming.

Opportunities in online shopping are particularly attractive, as e-commerce accounts for less than 3% of retail transactions. Tech startups in India are still paying to build a supply chain and delivery networks.

India had a record $6.3 billion of funding and deals for technology startups in the second quarter, while funding to China-based companies dropped 18% from a peak of $27.7 billion in the fourth quarter of 2020, according to data from research firm CB Insights.

The 2020 U.S. market sell-off was met with a double for U.S. tech stocks and from that moment in time, Prosus went from a peak of €109 to €67, which is a drop of around 40%.

Even on news of this Indian takeover, there was a 5% pop met with a 5% sell the news reaction that took the stock back to 2-year lows.

Investors are not convinced of this tech start-up story and the stock has become a sell-the-rallies type of stock which is tough to shake off in the short term.

Overpaying for emerging tech while Prosus’ largest investment Tencent is down 35% from its February 2021 peak smacks of desperation and seems like they are grasping for straws.

Let me remind readers that the stock is only up 9% from its 2019 public listing and certainly when we cross-examine and compare this to U.S. tech, the only conclusion I can come up with is that performance is pitiful.

I would rather moderately overpay for Alphabet (GOOGL), Apple (AAPL), Microsoft (MSFT), and Facebook (FB), and Amazon (AMZN) than grossly overpay for Prosus.

The U.S. simply takes better care of its tech companies from a regulatory point of view, as well as stock market, business models, capital markets, desirability to be employed here, tax benefits, etc. And there’s a synergistic effect where the sum of the parts is times more.

The deal murderer is that we are inching towards a rising rate environment which couldn’t be a worse backdrop for these exotic tech investments in a murky regulatory environment.

Conversely, big tech will be able to stomach any rate rise on the backs of their robust balance sheets.

Avoid Prosus unless it drops to €50 — that’s another 19% from current prices — that would be only for a quick trade because I’m not sold on this company long term.