If you have to ask what this classic phrase from Britain’s colonial past means, you are too young to know.

The stock market equivalent is that there is nothing to do. Just sit back and relax, watching the value of your stocks go up every day. Let the greatest monetary and fiscal stimulus work its inevitable magic.

When I said last week that stocks might go up every day in April, I wasn’t kidding. NASDAQ (QQQ) has gone up every day this month except one. The S&P 500 has seen only two down days when it was virtually unchanged.

And the best may be yet to come.

The mere prospect of a $2.3 infrastructure trillion budget is enough to keep stocks powering upward for the foreseeable future. Biden may have to negotiate the total down to get it through congress and that may be the cause of the next correction…in about three months.

What really had the phones buzzing on Thursday was the bizarre move in the bond market. After seeing spectacularly positive data, the Weekly Jobless Claims plunging by 200,000 and Retail Sales coming in at a prolific 9.8%, bonds should have crashed.

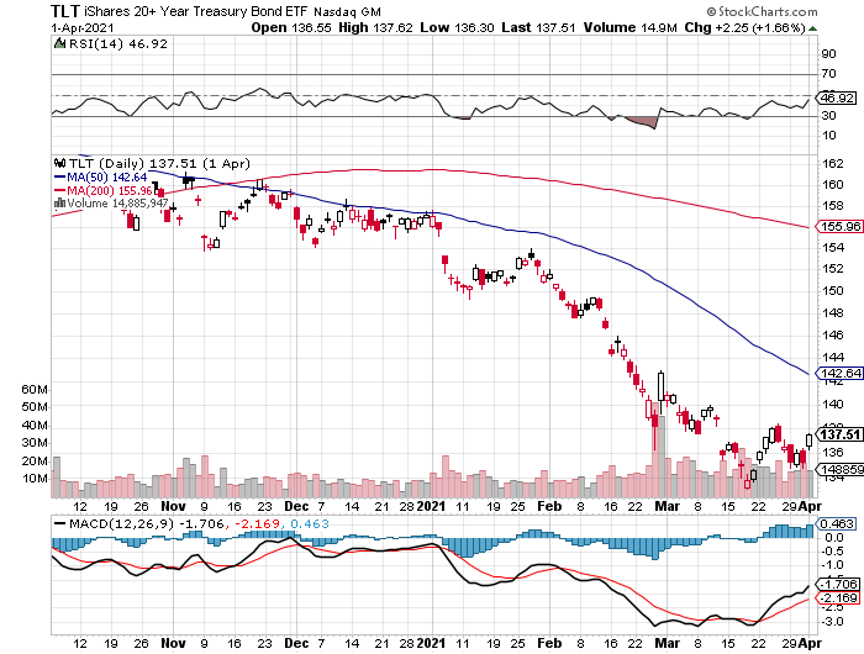

Instead, the (TLT) jumped by $2.60. That took interest rate and inflation fears packing and sent the indexes soaring to all-time highs once again.

It’s proof yet again that inflation is the boogie man that will never show. Despite the incredible strength of the economy, any time anyone tries to raise prices, another company comes along with a better product or service at half the price. Such is the relentless tide of technology.

In the meantime, Goldilocks has moved in, unpacked her bags, gotten comfortable, and has settled in for the duration. I have been so aggressive in trading the market for the last six months it is wearing me out.

So, I took a rare Saturday off, weeding the garden, setting up a new computer, and generally fixing things that I haven’t had time to attend to since last year. I lived almost normally….for a day.

One of the best Earnings Seasons in history started last week, with 25% growth expected at 81% beating forecasts. JP Morgan (JPM) and Bank of America (BAC) kicks off on Wednesday, with the big kahuna, Apple (AAPL) reporting on April 28. Expect stocks to rally until then. It may give us the first hint of the massive stimulus on the economy to come. Q2 and Q3 will be the monster quarters.

Equity Funds pick up a half trillion dollars in five months, more than they attracted over the last 12 years. It’s all rocket fuel for the ongoing market melt-up. With the Volatility Index (VIX) at a one-year low at $17, the best may be yet to come. Equity investors are the most bullish in years.

Tesla is upgraded to $1,071 per share by research firm Canaccord Genuity. The company is transitioning from low-volume high-priced cars to high-volume low-priced cars, as seen in the 47% leaps in sales during Q1. The stationary battery business is booming, thanks to a new generation of technology. Tesla is developing an Apple-type brand value in the energy market, which is worth a big premium, which competitors can’t match. Tesla has brought a machine gun to a knife fight. Global chip shortages are a risk. The stock jumped $25 on the news.

Consumer Price Index comes in muted at 0.6% in April and 2.6% YOY. The market had been fearing worse, sparking another leg up in technology stocks. Much of the gain was from a jump in gasoline prices, which are now falling. Food prices are also rising.

JP Morgan pops on upside earnings surprise, with Q1 profits soaring from $2.9 billion a year ago to an eye-popping $14.5 billion. Revenues were up 14% to $33.1 billion. Loan demand is weakening because so many people are getting government money for free. Credit card debts are being paid down.

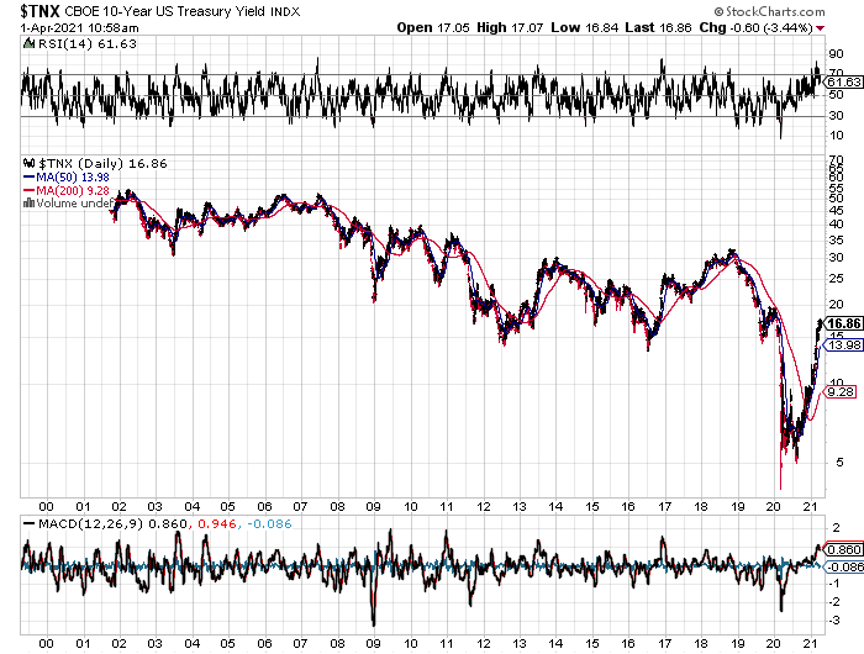

Retail Sales explode in March, up a staggering 9.8%. New spending at bars and restaurants was a major factor, and we haven’t even started yet! Stocks soar to new highs, and the bond market takes off like a scalded chimp, taking ten-year US Treasury yields below 1.57%. It confirms my thesis that when we see actual real numbers of an unprecedented recovery, we get another new leg in the bull market.

Weekly Jobless Claims collapse to 576,000, the lowest of 2021. That's down a massive 193,000 jobs from the previous week. Herd immunity is here! Keep getting those shots!

China’s (FXI) GDP grew by a staggering record of 18.3% in Q1 at an annualized rate YOY. Strong industrial production and exports were the leaders. It presages a similar explosive growth rate for the US in Q2. We won’t know until the end of July. Having your largest customers breaking growth records is great for your business too. Buy everything on dips.

Hedge funds nailed the Bond Crash, selling short some $100 billion in paper since January. It will be more than enough to cover their losses in equity shorts. When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Mad Hedge Global Trading Dispatch profit reached 7.17% gain during the first half of April on the heels of a spectacular 20.60% profit in March.

It was a very busy week for trade alerts, with five positions expiring at their maximum profit points in (TSLA) and the (TLT). It’s been so long since I’ve had a loss, I forgot what they looked like.

I used a puzzling $2.60 spike in the (TLT) to add to my already substantial short position in bonds (TLT) with a distant May expiration. Ten-year US Treasury yields fell all the way to 1.51%.

My 2021 year-to-date performance soared to 51.26%. The Dow Average is up 12.9% so far in 2021.

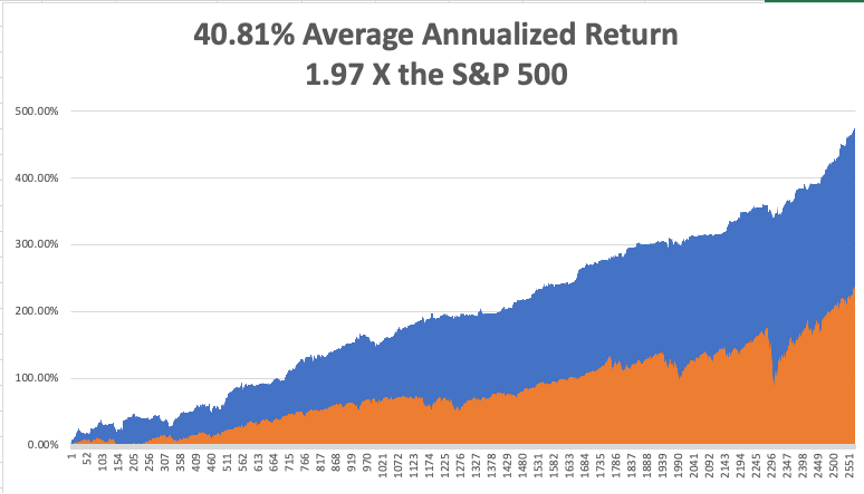

That brings my 11-year total return to 473.81%, some 2.00 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 40.81%, the highest in the industry.

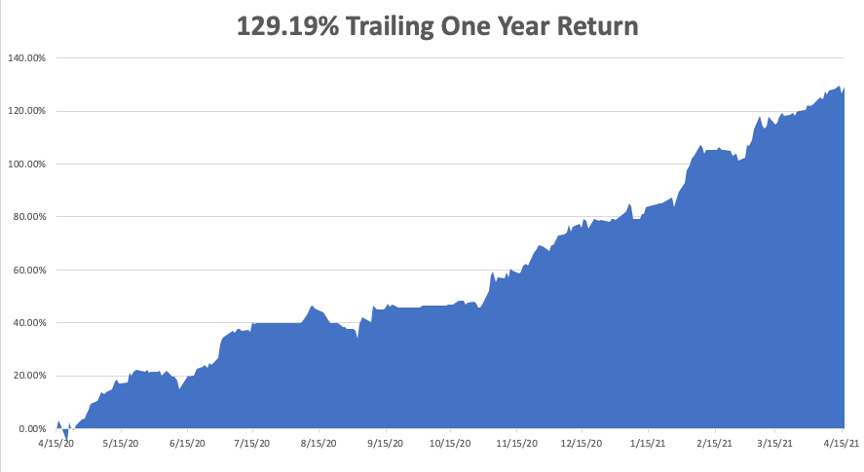

My trailing one-year return exploded to positively eye-popping 129.19%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives. Every time I think these numbers can’t be topped, they increase by another 10% during the following two weeks.

We need to keep an eye on the number of US Corona virus cases at 31.6million and deaths topping 567,000, which you can find here.

The coming week will be dull on the data front.

On Monday, April 19 at 11:00 AM, earnings for (IBM), Coka-Cola (KO), and United Airlines (UAL) are released.

On Tuesday, April 20, at 4:30 PM, API Crude Stocks are published. We also get earnings for Johnson & John (JNJ) and Netflix (NFLX).

On Wednesday, April 21 at 1:00 PM, there is a big 20-year US Treasury bond auction. Chipotle (CMG) and Verizon (VZ) earnings are out. On Thursday, April 22 at 8:30 AM, the Weekly Jobless Claims are printed. At 10:00 AM Existing Home Sales for March are announced. Snap (SNAP) and Intel (INTC) announce earnings.

On Friday, April 23 at 10:00 AM, we get the New Home Sales for March. American Express (AXP) and Honeywell (HON) release earnings. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, someone commented that I walk kind of funny the other day, and the memories flooded back.

In 1975, The Economist magazine in London heard rumors that a large part of the population was getting slaughtered in Cambodia. We expected this to happen after the fall of Vietnam, but not in the Land of the Khmers. So my editor, Peter Martin, sent me to check it out.

Hooking up with a right-wing guerrilla group financed by the CIA was the easy part. Humping 100 miles in 100-degree heat wasn’t.

We eventually came to a large village that was completely deserted. Then my guide said, “Over here.” He took me to a nearby cave containing the bodies of over 1,000 women, children, and old men that had been there for months.

I’ll never forget that smell.

With the evidence and plenty of pictures in hand, we started the trek back. Suddenly, there was a large explosion and the man 20 yards in front of me disappeared. He had stepped on a land mine. Then the machine-gun fire opened up. It was an ambush.

I picked up an M-16 to return fire, but it was bent, bloody, and unusable. I picked up a second rifle and fired until it was empty. Then everything suddenly went black.

I woke up days chained to a palm tree, covered in shrapnel wounds, a prisoner of the Khmer Rouge. Maggots infested my wounds, but I remembered from my Tropical Diseases class at UCLA that I should leave them alone because they only ate dead flesh and would prevent gang green. That class saved my life. Good thing I got an “A”.

I was given a bowl of rice a day to eat, which I had to gum because it was full of small pebbles and might break my teeth. Farmers loaded their crops with these so the greater weight could increase their income. I spent my time pulling shrapnel out of my legs with a crude pair of plyers.

Two weeks later, the American who set up the trip for me showed up with cases of claymore mines, rifles, ammunition, and antibiotics. My chains we cut and I began the long walk back to Thailand.

It’s nice to learn your true value.

Back in Bangkok, I saw a doctor who attended to the 50 caliber bullet that grazed my right hip. It was too old to sew up so he decided to clean it instead. “This won’t hurt a bit,” he said as he poured in hydrogen peroxide and scrubbed it with a stiff plastic brush.

It was the greatest pain of my life. Tears rolled down my face.

But you know what? The Economist got their story and the world found out about the Great Cambodian Genocide, where 3 million died. There is a museum in Phnom Penh devoted to it today.

So, if you want to know why I walk funny, be prepared for a long story. I still set off metal detectors.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Doing Research

https://www.madhedgefundtrader.com/wp-content/uploads/2018/10/John-Thomas-rifle.png681477Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-19 09:02:542021-04-19 11:13:14The Market Outlook for the Week Ahead, or Lie Back and Think of England

Below please find subscribers’ Q&A for the April 14 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from Silicon Valley, CA.

Q: How do you choose your buy areas?

A: It’s very simple; I read the Diary of a Mad Hedge Fund Trader. Beyond that, there are two main themes in the market right now: domestic recovery and tech; and I try to own both of those 50/50. It's impossible to know which one will be active and which one will be dead, and some of that rotation will happen on a day-by-day basis. As for single names, I tend to pick the ones I have been following the longest.

Q: In my 401k, should I continue placing my money in growth or move to something like emerging markets or value?

A: It depends on your age. The younger you are, the more aggressive you should be and the more tech stocks you should own. Because if you’re young, you still have time to earn the money back if you lose it. If you’re old like me, you basically only want to be in value stocks because if you lose all the money or we have a recession, there's not enough time to go earn the money back; you’re in spending mode. That is classic financial advisor advice.

Q: When you say “Buy on dips”, what percentage do you mean? 5% or 10%

A: It depends on the volatility of the stock. For highly volatile stocks, 10% is a piece of cake. Some of the more boring ones with lower volatility you may have to buy after only a 2% correction; a classic example of that is the banks, like JP Morgan (JPM).

Q: Even though you’re not a fan of cryptocurrency, what do you think of Coinbase?

A: It’ll come out vastly overvalued because of the IPO push. Eventually, it may fall to a lower level. And Coinbase isn’t necessarily a business model dependent on bitcoin; it is a business model based on other people believing in bitcoin, and as long as there’s enough of those creating two-way transactions, they will make money. But all of these things these days are coming out super hyped; and you never want to touch an IPO—wait for it to drop 50%, as I once did with Tesla (TSLA).

Q: Please explain the barbell portfolio.

A: The barbell works when you have half tech, half domestic recovery. That way you always have something going up, because the market tends to rotate back and forth between the two sectors. But over the long term everything goes up, and that is exactly what has been happening.

Q: Is the ProShares Ultra Technology Fund (ROM) an ETF?

A: Yes, it is an ETF issuer with $53 billion worth of funds based in Bethesda, MD. (ROM) is a 2x long technology ETF, and their largest holdings include all the biggest tech stocks like Apple (AAPL), Microsoft (MSFT), Facebook (FB), and so on.

Q: Will all this government spending affect the market?

A: Yes, it will make it go up. All we’re waiting to see now is how fast the government can spend the money.

Q: What is the target for ROM?

A: $150 this year, and a lot more on the bull call spread. The only shortcoming of (ROM) is you can only go out six months on the expiration. Even then, you have a good shot at making a 500% return on the farthest out of the money LEAPS, the November $130-$135 vertical bull call spread. That's because market makers just don’t want to take the risk being short technology two years out. It’s just too difficult to hedge.

Q: There have been many comments about hyperinflation around the corner. Will we be seeing hyperinflation?

A: No, the people who have been predicting hyperinflation have been predicting it for at least 20 years, and instead we got deflation, so don’t pay attention to those people. My view is that technology is accelerating so fast, thanks to the pandemic, that we will see either zero inflation or we will see deflation. That has been the pattern for the last 40 years and I like betting on 40-year trends.

Q: When we get called away on our short options, is it easier to close the trade than to exercise your option?

A: No, any action you take in the market costs money, costs commissions, costs dealing spreads. And it's much easier just to exercise the option if you have to cover your short, which is either free or will cost you $15.

Q: Are you worried about overspending?

A: No, the proof in that is we have a 1.53% ten-year US Treasury yield, and $20 trillion in QE and government spending is already known, it’s already baked in the price. So don’t listen to me, listen to Mr. Market; and it says we haven't come close to reaching the limit yet on borrowing. Look at the markets, they're the ones who have the knowledge.

Q: My Walt Disney (DIS) LEAPs are getting killed. I don't understand why my LEAPS go down even on green days for the stock.

A: The answer is that the Volatility Index (VIX) has been going down as well. Remember, if you’re long volatility through LEAPS, and volatility goes down, you take a hit. That said, we’re getting close to the lows of the year for volatility here, so any further stock gains and your LEAPS should really take off. And remember when you buy LEAPS, you’re doing multiple bets; one is that volatility stays high and goes higher, and one is that your stock is high and goes higher. If both those things don’t happen, and you can lose money.

Q: How do you best short the (TLT)?

A: If you can do the futures market, Treasury bonds are always your best short there because you have 10 to 1 leverage.

Q: How would you do a spread on Crisper Technology (CRSP)?

A: We have a recommendation in the Mad Hedge Biotech & Healthcare service to be long the two-year LEAP on Crisper, the $160-$170 vertical bull call spread.

Q: When do you see the largest dip this year?

A: Probably over the summer, but it likely won’t be over 10%. Too much cash in the market, too much government spending, too much QE. People will be in “buy the dips” mode for years.

Q: Is the SPAC mania running out of steam?

A: Yes, you can only get so many SPACS promising to buy the same theme at a discount. I think eventually, 80% of these SPACS go out of business or return the money to investors uninvested because they are promising to buy things at great bargains in one of the most expensive markets in history, which can’t be done.

Q: What do you think about Joe Biden’s attempt to tame the semiconductor chip shortage?

A: Most people don't know that all chips for military weapons systems are already made in the US by chip factories owned by the military. And the pandemic showed that a just-in-time model is high risk because all of a sudden when the planes stop flying, you couldn't get chips from China anymore. Instead, they had to come by ship which takes six weeks, or never. So a lot of companies are moving production back to the US anyway because it is a good risk control measure. And of course, doing that in the midst of the worst semiconductor shortage in history shows the importance of this. Even Tesla has had to delay their semi truck because of chip shortages. Keep buying NVIDIA (NVDA), Micron Technology (MU), Advanced Micro Devices (AMD), and Applied Materials (AMAT) on dips.

Q: Do you see a sell the news type of event for upcoming earnings?

A: Yes, but not by much. We got that in the first quarter, and stocks sold off a little bit after they announced great earnings, and then raced back up to new highs. You could get a repeat of that, as people are just sitting on monster profits these days and you can’t blame them for wanting to pull out a little bit of money to spend on their summer vacation.

Q: Has the stock market gotten complacent about COVID risk?

A: No, I would say COVID is actually disappearing. Some 100 million Americans have been vaccinated, 5 million more a day getting vaccinated, this thing does actually go away by June. So after that, you only have to worry about the anti-vaxxers infecting the rest of the population before they die.

Q: Do you see any imminent foreign policy disasters in Asia, the Middle East, or Europe that could derail the stock market?

A: I don’t, but then you never see these things coming. They always come out of the blue, they're always black swans, and for the last 40 years, they have been buying opportunities. So pray for a geopolitical disaster of some sort, take the 5-10% selloff and buy because at the end of the day, American stockholders really don't care what’s going on in the rest of the world. They do care, however, about increasing their positions in long-term bull markets. I don't worry about politics at all; I don’t say that lightly because it’s taking 50 years of my own geopolitical experience and throwing it down the toilet because nobody cares.

Q: Would you buy Coinbase?

A: Absolutely not, not even with your money. These things always come out overpriced. If you do want to get in, wait for the 50% selloff first.

Q: Is Canada a play on the dollar?

A: Absolutely yes. If they get a weaker dollar, it increases Canadian pricing power and is good for their economy. Canada is also a great commodities play.

Q: The IRS is using Palantir (PLTR) software to find US citizens avoiding taxes with Bitcoin.

A: Yes, absolutely they are. Anybody who thinks this is tax-free money is delusional. And this is one reason to buy Palantir; they’re involved in all sorts of these government black ops type things and we have a very strong buy recommendation on Palantir and their 2-year LEAPS.

Q: Are NFTs, or Non-Fundable Tokens, another Ponzi scheme?

A: Absolutely, if you want to pay millions of dollars for Paris Hilton’s music collection, go ahead; I'd rather buy more Tesla.

Q: When do you think you can go to Guadalcanal again?

A: Well, I’m kind of thinking next winter. Guadalcanal is one of the only places you can go and get more diseases than you can here in the US. Last year, I went there and picked up a bunch of dog tags from marines who died in the 1942 battle there, sent them back to Washington DC, and had them traced and returned to the families. And I happen to know where there are literally hundreds of more dog tags I can do this with. It’s not an easy place to visit and it’s very far away though. Watch out for malaria. My dad got it there.

Q: Walt Disney is already above the pre-pandemic price. Do you suggest any other hotel company name at this time?

A: Go with the Las Vegas casinos, Wynn (WYNN) and MGM (MGM) would be really good ones. Las Vegas is absolutely exploding right now, and we haven't seen that yet in the earnings yet, so buy Las Vegas for sure.

Q: Is the upcoming Roaring Twenties priced into the stock market already?

A: Absolutely not. You didn't want to sell the last Roaring Twenties in 1921 as it still had another eight years to go. You could easily have eight years on this bull market as well. We have historic amounts of money set up to spend, but none of it has been actually spent yet. That didn’t exist in 1921. I think that when they do start hitting the economy with that money, that we get multiple legs up in stock prices.

To watch a replay of this webinar just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2014/08/John-Thomas-Beach-e1416856744606.png400276Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-16 09:02:052021-04-16 16:13:56April 14 Biweekly Strategy Webinar Q&A

Stocks have risen at an annualized rate of 40% so far in 2021. If that sounds too good to be true, it is.

But then, we have the greatest economic and monetary stimulus of all time rolling out also.

Of the $10 trillion in government spending that has or is about to be approved, virtually none of it has been spent. There hasn’t been enough time. It turns out that it is quite hard to spend a trillion dollars. Corporate America and its investors are salivating.

The best guess is that the new spending will create five million jobs for the economy over eight years, taking the headline Unemployment Rate down to a full employment 3-4%. The clever thing about the proposal is that it is financed over 15 years, which takes advantage of the current century's low interest rates.

That is something many strategists have been begging the US Treasury to do for years. Take the free money while it is on offer.

There is something Rooseveltean about all this, with great plans and huge amounts of money, like 10% of GDP on the table. But then we did just come out of a Great Depression, with unemployment peaking at 25 million, the same as in 1933.

The package is so complex that it is unlikely to pass by summer. Until then, stocks will probably continue to rally on the prospect.

It makes my own forecast of a 30% gain in stocks and a Dow Average of 40,000 for 2021 look overly cautious, conservative, and feeble (click here). But then, you have to trade the market you have, not the one you want.

And here is the really fun part. After a grinding seven-month-long correction, technology stocks have suddenly returned from the dead. All the best names gained 10% or more in the previous four-day holiday-shortened week. Clearly, investors have itchy trigger fingers with tech stocks at these levels.

In the meantime, technology stock prices have fallen 20-50% while earnings have jumped by 20% to 40%. What was expensive became cheap. It was a setup that was begging to happen.

This is great news because technology stocks are the core to all non-indexed retirement funds.

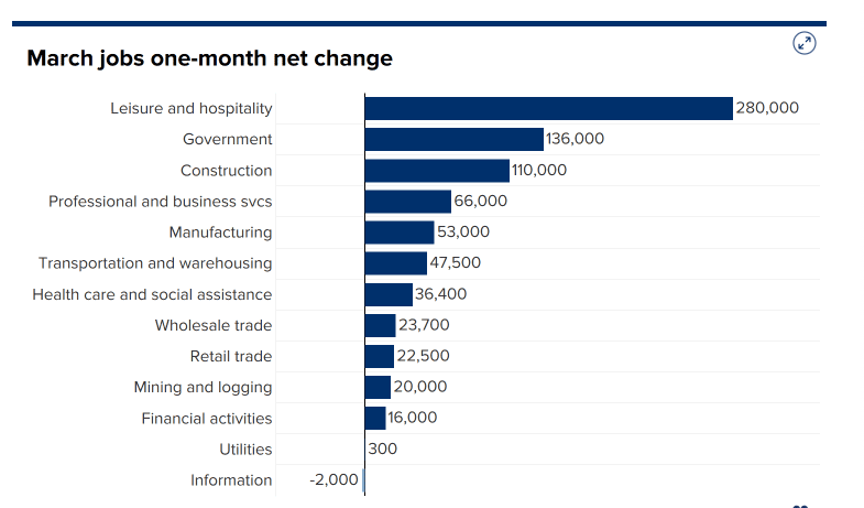

The S&P 500 (SPX) blasted through 4,000, a new all-time high, off the back of one of the largest infrastructure spends in history. Job creation over the next eight years is estimated at 5 million. Corporate earnings will go through the roof. Tech is back from the dead. Leaders were semiconductor equipment makers like my old favorites, Applied Materials (AMAT) and Lam Research (LRCX). The Volatility Index (VIX) sees the $17 handle, hinting at much higher to come. The next leg up for the Roaring Twenties has begun! Biden Infrastructure Bill Tops $2.3 Trillion. Of course, some of it isn’t infrastructure but other laudable programs that starved under the Trump administration, like spending on seniors (I’m all for that!). Still, spending is spending, and this will turbocharge the economy all the way out to say….2024. The impact on interest rates will be minimal as long as the Fed keeps overnight rates near zero, as they have promised to do for nearly three years. Making the power grid carbon-free by 2035 is a goal and would require a 50% increase in solar national installations. Infrastructure spending is always a win-win because the new tax revenues it generates always pay for it in the end. March Nonfarm Payroll Report exploded to the upside, adding a near record 917,000 jobs, and taking the headline Unemployment Rate down to 6.0%. Employers are front running Biden’s infrastructure plans, hiring essential workers while they are still available. Look for labor shortages by summer, especially in high paying tech. Leisure & Hospitality was the overwhelming leader at a staggering 280,000, followed by Government at 136,000 and Construction at 110,000.

Goldilocks lives on, with a 1.0% drop in Consumer Spending in February, keeping inflation close to zero. The Midwest big freeze is to blame. You can’t buy anything when there’s no gas for the car and no electricity once you get there, as what happened in Texas. The $1,400 stimulus checks have yet to hit much of the country, although I got mine. It couldn’t be a better environment for owning stocks. Keep buying everything on dips.

Consumer Confidence soared, up 19.3 points to 109 in February, according to the Conference Board. It’s the second-biggest move on record. A doubling of the value of your home AND your stock portfolio in a year is making people feel positively ebullient. Oh, and free money from the government is in the mail. The Suez Canal reopened, allowing 10% of international trade to resume. A massive salvage effort that freed the 200,000 ton Ever Given. The ship will be grounded for weeks pending multiple inspections. Somebody’s insurance rates are about to rachet up. It all shows how fragile is the international trading system. Deliveries to Europe will still be disrupted for months. It puts a new spotlight on the Arctic route from Asia to Europe, which is 4,000 nm shorter.

Boeing (BA) won a massive order, some 100 planes from Southwest Air (LUV), practically the only airline to use the pandemic to expand. Boeing can fill the order almost immediately from 2020 cancelled orders for the $50 million 737 MAX. Keep buying both (BA), (LUV), and (AKL) on dips.

Tesla blows away Q1 deliveries, with a 184,400 print, or 47.5% high than the 2021 rate. That is without any of the new Biden EV subsidies yet to kick in. Lower priced Model 3 sedans and Model Y SUVs accounted for virtually all of the report. The Shanghai factory is kicking in as a major supplier to high Chinese demand. The one million target for 2021 is within easy reach. Traders saw this coming (including me) and ramped the stock up $100. Buy (TSLA) on dips. My long-term target is $10,000.

United Airlines hires 300 pilots to front-run expected exposure summer travel. CEO Scott Kirby says domestic vacation travel has almost completely recovered. Keep buying (LUV), (AKL), and (DAL) on dips. When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Mad Hedge Global Trading Dispatch profit reached 0.38% gain during the first two days of April on the heels of a spectacular 20.60% profit in March.

I used the Monday low to double up my long in Tesla. After that, it was off to the races for all of tech. I caught a $100 move on the week.

My new large Tesla (TSLA) long expires in 9 trading days.

That leaves me with 50% cash and a barrel full of dry powder.

My 2021 year-to-date performance soared to 44.47%. The Dow Average is up 9.40% so far in 2021.

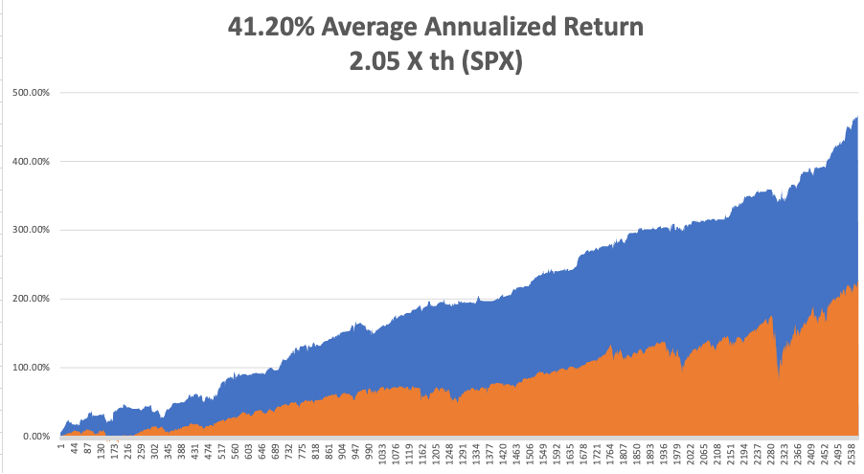

That brings my 11-year total return to 467.02%, some 2.08 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 41.20%, the highest in the industry.

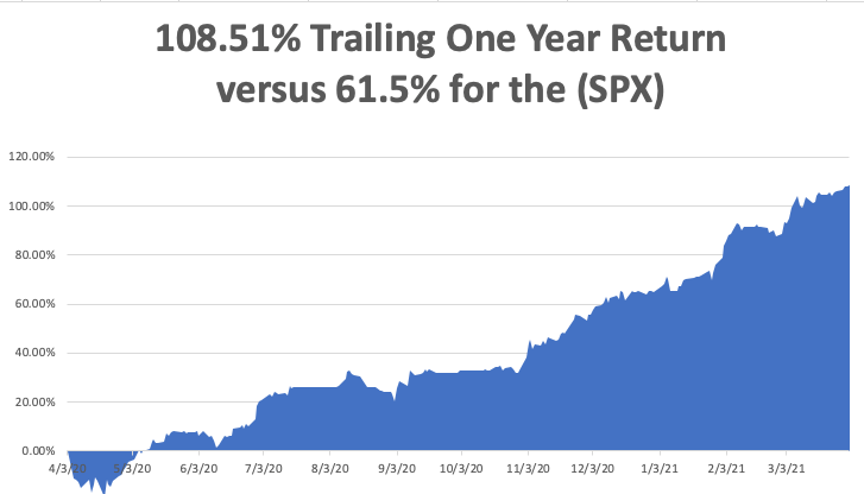

My trailing one-year return exploded to positively eye-popping 108.51%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 30.6million and deaths topping 555,000, which you can find here.

The coming week will be dull on the data front.

On Monday, April 5, at 10:00 AM, the ISM Non-Manufacturing Index for March is released.

On Tuesday, April 6, at 10:00 AM, US Consumer Inflation Expectations for March are published.

On Wednesday, April 7 at 2:00 PM, the minutes of the last Federal Open Market Committee Meeting are published.

On Thursday, April 8 at 8:30 AM, the Weekly Jobless Claims are printed.

On Friday, April 9 at 8:30 AM we get the Producer Price Index for March. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, I recently turned 69, so I used a nice day to climb up to the Lake Tahoe High Sierra rim at 9,000 feet, found a nice granite boulder sit on to keep dry, and tried to figure out what it was all about.

I’ve been very lucky.

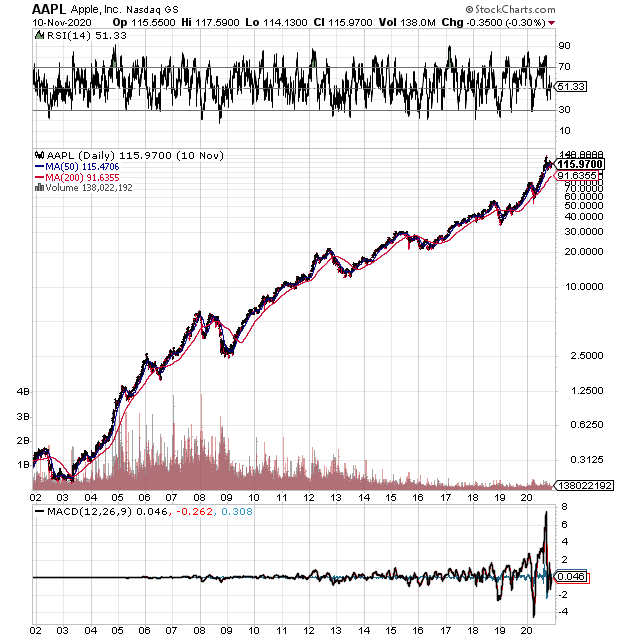

I had a hell of a life that I wouldn’t trade for anything. I wouldn’t change a bit (well, maybe I would have bought more Apple shares at a split-adjusted 30 cents in 1998. I knew Steve was going to make it).

Since I’ve always loved what I did, journalist, trader, combat pilot, hedge fund manager, writer, I don’t think I have “worked” a day in my life.

I fought for things I believed in passionately and won, and kept on winning. It’s good to be on the right side of history.

I have loved and lost and loved again and lost again, and in the end outlived everyone, even my younger brother, who died of Covid-19 a year ago. The rule here is that it is always the other guy who dies. My legacy is five of the smartest kids you ever ran into. They’re great traders as well.

So I’ll call it a win.

I visited my orthopedic surgeon the other day to get a stem cell top-up for my knees and she asked how long I planned to keep coming back. I told her 30 years, and I meant it.

There’s nothing left for me to do but to make you all savvy in the markets and rich, something I leap out of bed every morning at 5:00 AM to accomplish.

Enjoy your weekend.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2019/04/john-thomas-pilot.png531597Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-05 09:02:332021-04-05 12:22:42The Market Outlook for the Week Ahead, or A Supercharged Economy is Supercharging the Stock Market

Once considered one the safest stock market sectors in which to hide out during bear markets and more recently pandemics, Consumer Staples no longer offer the hideout they once did.

Who needs a hideout anyway now that the Roaring Twenties are on and may make another decade to run.

Take a look at the Consumer Staples Select Sector SPDR ETF (XLP). It’s top five holdings include Proctor & Gamble (PG) (11.13%), Coca-Cola (KO) (10.07%), PepsiCo, Inc. (PEP) (8.7%), Philip Morris (7.80%) (PM), and Walmart (WMT).

Its only remaining attraction is that it has a 30-day SEC yield of 2.67%.

The (XLP) has recently been one of the best performing ETFs. However, costs are rising dramatically, and the bloom is coming off the rose.

In short, the industry is caught in a vice.

In the meantime, ferocious online competition from the likes of Amazon (AMZN) makes it impossible for consumer staples to pass costs on to consumers as they did in past economic cycles.

In fact, the prices for many consumer staples are falling thanks to the world’s most efficient distribution network. And if you are an Amazon Prime member, they will deliver it to your door for free. I just bought a pair of Head Kore 93 skis in Vermont, and they were delivered in two days.

It gets worse. The largest sector of the consumer staples market, the poor and working middle class are seeing the smallest wage gains, the worst layoffs, and the slowest pandemic recovery. Almost all pay increases are now taking place at the top of the wage ladder.

AI specialists and online marketing experts, yes, Safeway checkout clerks and fast food workers, no.

This also will get a lot worse as some 50% of all jobs will disappear over the next 20 years, mostly at the low end.

Blame technology. There is even a robot now that can assemble Ikea furniture. And there goes my side gig!

So, if your friend at the country club locker room tells you it’s time to load up on Consumer Staples because they are cheap, safe, and high-yielding, ignore him, delete his phone number from your contact list, and unfriend him on Facebook.

If anything, the sector is a great “sell short on rallies” candidate.

As I never tire of telling followers, never confuse “gone down a lot” with “cheap.”

Eventually, the sector will fall enough to where it offers value. But that point is not now. There has to be a bottom somewhere.

After all, everyone needs toilet paper, right? Or will a robot soon take over that function as well? They already have in Japan.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/04/Charmin-story-2-image-5.jpg237336MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2021-04-02 09:04:302021-04-05 10:50:20Why Consumer Staples Are Peaking

Below please find subscribers’ Q&A for the March 31 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from frozen Incline Village, NV.

Q: Would you buy Facebook (FB) or Zoom (ZM) right here?

A: Well, Zoom was kind of a one-hit wonder; it went up 12 times on the pandemic as we moved to a Zoom economy, and while Zoom will permanently remain a part of our life, you’re not going to get that kind of growth in stock prices in the future. Facebook on the other hand is going to new highs, they just announced they’re laying a new fiber optic cable to Asia to handle a 70% increase in traffic there. So, for the longer term and buying here, I think you get a new high on Facebook soon; there's maybe another 20-30% move in Facebook this year.

Q: I can’t really chase these trades here, right?

A: Correct; if you wait any more than a day or 2 on executing a trade alert, you’re missing out on all of the market timing value we bring to the game. So that's why I include an entry price and the “don’t pay more than” price. And we never like to chase, except last year, when we did it almost all the time. But last year was a chase market, this year not so much.

Q: How are LEAP purchase notifications transmitted?

A: Those go out in the daily newsletter Global Trading Dispatch when I see a rare entry point for a LEAP, then we’ll send out a piece and notify everybody. But it’s very unusual to get those. Of course, a year ago we were sending out lists of LEAPS ten at a time when the Dow Average ($INDU) is at 18,000. But that is not now, you only wait for those once or twice a year. On huge selloffs to get into two-year-long options trades, and that is definitely not now. The only other place I've been looking out for LEAPS right now are really bombed out technology stocks begging for a rotation. Concierge members get more input on LEAPS and that is a $10,000 a year upgrade.

Q: What are your thoughts on silver (SLV) and long-term gold (GLD)?

A: I see silver going to $50 and eventually $100 in this economic cycle, but it's out of favor right now because of rising interest rates. So, once we hit 2.00% in the ten years, it’s not only off to the races for tech but also gold and silver. Watch that carefully because your entry point may be on the horizon. That makes Wheaton Precious Metals (WPM) a very attractive “BUY” right now.

Q: Are you going to trade the (TLT)?

A: Absolutely yes, but I’m kind of getting picky now that I’m up 42% on the year; and I only like to sell 5-point rallies, which we got for about 15 minutes last week. And I also only like to buy 5- or 10-point dips. Keep your trading discipline and you’ll make a ton of money in this market. Last year we made about 30% trading bonds on about 30 round trips.

Q: How much further upside is there for US Steel (X) and Nucor Corp. (NUE)?

A: More. There's no way you do infrastructure without using millions of tons of steel. And I kind of missed the bottom on US Steel because it had been a short for so long that it kind of dropped off the radar for me. I think we have gone from $4 to 27 since last year, but I think it goes higher. It turns out the US has been shutting down steel production for decades because it couldn't compete with China or Japan, and now all of a sudden, we need steel, and we don’t even make the right kind of steel to build bridges or subways anymore—that has to be imported. So, most of the steel industry here now is working for the car industry, which produces cold-rolled steel for the car body panels. Even that disappears fairly soon as that gets taken over by carbon fiber. So enough about steel, buy the dips on (X) and (NUE).

Q: What stocks should I consider for the infrastructure project?

A: Well, US Steel (X) and Nucor Corp (NUE) would be good choices; but really you can buy anything because the infrastructure package, the way it’s been designed, is to benefit the entire economy, not just the bridge and freeway part of it. Some of it is for charging stations and electric car subsidies. Other parts are for rural broadband, which is great for chip stocks. There is even money to cap abandoned oil wells to rope in Texas supporters. All of this is going to require a massive upgrade of the power grid, which will generate lots of blue-collar jobs. Really everybody benefits, which is how they get it through Congress. No Congressperson will want to vote against a new bridge or freeway for their district. That’s always the case in Washington, which is why it will take several months to get this through congress because so many thousands of deals need to be cut. I’ve been in Washington when they’ve done these things, and the amount of horse-trading that goes on is incredible.

Q: Is it a good thing that I’ve had the United States Treasury Bond Fund (TLT) LEAPS $125 puts for a long time.

A: Yes. Good for you, you read my research. Remember, the (TLT) low in this economic cycle is probably around $80, so you probably want to keep rolling forward your position….and double up on any ten-point rally.

Q: Do you think we get a pop back up?

A: We do but from a lower level. I think any rallies in the bond market are going to be extremely limited until we hit the 2.00%, and then you’re going to get an absolute rip-your-face-off rally to clean out all the short term shorts. If you're running put LEAPS on the (TLT) I would hang on, it’s going to pay off big time eventually.

Q: If we see 3.00% on the 10-year this year, do you see the stock market crashing?

A: I don’t think we’ll hit 3.00% until well into next year, but when we do, that will be time for a good 10% stock market correction. Then everyone will look around again and say, “wow nothing happened,” and that will take the market to new highs again; that's usually the way it plays out. Remember, then year yields topped all the way up at 5.00% when the Dotcom Bubble topped in April 2020.

Q: Has the airline hospitality industry already priced in the reopening of travel?

A: No, I think they priced in the hope of a reopening, but that hasn’t actually happened yet, and on these giant recovery plays there are two legs: the “hope for it” leg, which has already happened, and then the actual “happening” leg which is still ahead of us. There you can get another double in these stocks. When they actually reopen international travel to Europe and Asia, which may not happen this year, the only reopening we’re going to see in the airline business is in North America. That means there is more to go in the stock price. Also coming back from the brink of death on their financial reports will be an additional positive.

Q: Do you think a corporate tax increase will drive companies out of the US again and raise the unemployment rate?

A: Absolutely not. First of all, more than half of the S&P 500 don’t even pay taxes, so they’re not going anywhere. Second, I think they will make these offshoring moves to tax-free domiciles like Ireland illegal and bring a lot of tax revenues back to the US. And third, all Biden is doing is returning the tax rate to where it was in 2017; and while the corporate tax rate was 35%, the stock market went up 400% during the Obama administration, if you recall. So stocks aren't really that sensitive to their tax rates, at least not in the last 50 years that I’ve been watching. I'm not worried at all. And Biden was up on the polls a year ago talking about a 28% tax rate; and since then, the stock market has nearly doubled. The word has been out for a year and priced in for a year, and I don't think anybody cares.

Q: What about quantum computers?

A: I’m following this very closely, it’s the next major generation for technology. Quantum computers will allow a trillion-fold improvement in computing power at zero cost. And when there's a stock play, I will do it; but unfortunately, it’s not (IBM), because we’re not at the money-making stage on these yet. We are still at the deep research stage. The big beneficiaries now are Alphabet (GOOGL), Microsoft (MSFT), and Amazon (AMZN).

Q: Is it time to buy Chinese stocks?

A: I would say yes. I would start dipping in here, especially on the quality names like Tencent (TME), Baidu (BIDU), and Alibaba (BABA), because they’ve just been trashed. A lot of the selloff was hedge fund-driven which has now gone bust, and I think relations with China improve under Biden.

Q: Your timing on Tesla (TSLA) has been impeccable; what do you look for in times of pivots?

A: Tesla trades like no other stock, I have actually lost money on a couple of Tesla trades. You have to wait for things to go to extremes, and then wait two more days. That seems to be the magic formula. On the first big selloff go take a long nap and when you wake up, the temptation to buy it will have gone away. It always goes up higher than you expect, and down lower than you expect. But because the implied volatilities go anywhere from 70% to 100%, you can go like 200 points out of the money on a 3-week view and still make good money every month. And that’s exactly what we’re going to do for the rest of the year, as long as the trading’s down here in the $500-$600 range.

Q: Is Editas Medicine (EDIT), a DNA editing stock, still good?

A: Buy both (EDIT) and Crisper (CRSP); they both look great down here with an easy double ahead. This is a great long-term investment play with gene editing about to dominate the medical field. If you want to learn more about (EDIT) and (CRSP) and many others like them, subscribe to the Mad Hedge Fund Biotech & HealthcareLetter because we cover this stuff multiple times a week (click here).

Q: Is the XME Metals ETF a buy?

A: I would say yes, but I'd wait for a bigger dip. It’s already gone up like 10X in a year, but the outlook for the economy looks fantastic. (XME) has to double from here just to get to the old 2008 high and we have A LOT more stimulus this time around.

Q: What about hydrogen?

A: Sorry, I am just not a believer in hydrogen. You have to find someone else to be bullish on hydrogen because it’s not me. I've been following the technology for 50 years and all I can say is: go do an image Google for the name “Hindenburg” and tell me if you want to buy hydrogen. Electricity is exponentially scalable, but Hydrogen is analog and has to be moved around in trucks that can tip over and blow up at any time. Hydrogen batteries are nowhere near economic. We are now on the eve of solid-state lithium-ion batteries which improve battery densities 20X, dropping Tesla battery weights from 1,200 points to 60 pounds. So “NO” on hydrogen. Am I clear?

Q: Why do you do deep-in-the-money call and put spreads?

A: We do these because they make money whether the stock goes up down or sideways, we can do them on a monthly basis, we can do them on volatility spikes, and make double the money you normally do. The day-to-day volatility on these positions is very low, so people following a newsletter don’t get these huge selloffs and sell at bottoms, which is the number one source of retail investor losses. After 13 years of trade alerts, I have delivered a 40.30% average annualized return with a quarter of the market volatility. Most people will take that.

Q: Is ProShares Ultra Short 20 Year Plus Treasury ETF(TBT) still a play for the intermediate term?

A: I would say yes. If ten-year US Treasury bonds Yields soar from 1.75% to 5.00% the (TBT) should rise from $21 to $100 because it is a 2X short on bonds. That sounds like a win for me, as long as you can take short term pain.

Q: What is the timing to buy TLT LEAPS?

A: The answer was in January when we were in the $155-162 range for the (TLT). Down here I would be reluctant to do LEAPS on the TLT because we’ve already had a $25 point drop this year, and a drop of $48 from $180 high in a year. So LEAP territory was a year ago but now I wouldn’t be going for giant leveraged trades. That train has left the station. That ship has sailed. And I can’t think of a third Metaphone for being too late.

Q: Would you buy Kinder Morgan (KMI) here?

A: That’s an oil exploration infrastructure company. No, all the oil plays were a year ago, and even six months ago you could have bought them. But remember, in oil you’re assuming you can get in and out before it crashes again, it’s just a matter of time before it does. I can do that but most of you probably can’t, unless you sit in front of your screens all day. You’re betting against the long-term trend. It works if you’re a hedge fund trader, not so much if you are a long-term investor. Never bet against the long-term trend and you always have a tailwind behind you. All surprises work to your benefit.

Q: If you get a head and shoulders top on bitcoin, how far does it fall?

A: How about zero? 80% is the traditional selloff amount for Bitcoin. So, the thing is: if bitcoin falls you have to worry about all other investments that have attracted speculative interest, which is essentially everything these days. You also have to worry about Square (SQ), PayPal (PYPL), and Tesla (TSLA), which have started processing Bitcoin transactions. Bitcoin risk is spread all over the economy right now. Those who rode the bandwagon up will ride it back down.

Q: Is Boeing (BA) a long-term buy?

A: Yes, especially because the 737 Max is back up in the air and China is back in the market as a huge buyer of U.S. products after a four-year vacation. Airlines are on the verge of seeing a huge plane shortage.

Q: What about Ags?

A: We quit covering years ago because they’re in permanent long-term downtrends and very hard to play. US farmers are just too good at their jobs. Efficiencies have double or tripled in 60 years. Ag prices are in a secular 150-year bear market thanks to technology.

Q: Is this recorded to watch later?

A: Yes, it goes on our website in about two hours. For directions on where to find it, log in to your www.madhedgefundrader.com account, go to “My Account,” and it will be listed under there, as are all the recorded webinars of the last 12 years.

Q: Would you buy Canadian Pacific (CP) here, the railroad?

A: No, that news is in the price. Go buy the other ones—Union Pacific (UNP) especially.

Q: What are your thoughts on Bitcoin?

A: We don’t cover Bitcoin because I think the whole thing is a Ponzi scheme, but who am I to say. There is almost ten times more research and newsletters out there on Bitcoin as there is on stock trading right now. They seem to be growing like mushrooms after a spring storm. There are always a lot of exports out there at market tops, as we saw with gold in 2010 and tech stock in 2000.

Q: What do you think about Juniper Networks (JNP)?

A: It’s a Screaming “BUY” right here with a double ahead of it in two years. I’m just waiting for the tech rotation to get going. This is a long-term accumulate on dips and selloffs.

Q: Did the Archagos Investments hedge fund blow threaten systemic risk?

A: No, it seems to be limited just to this one hedge fund and just to the people who lent to it. You can bet banks are paring back lending to the hedge fund industry like crazy right now to protect their earnings. I don’t think it gets to the systemic point, but this is the Long Term Capital Management for our generation. I was involved in the unwind of the last LTCM capital, which was 23 years ago. I was one of the handful of people who understood what these people were even doing. So, they had to bring me in on the unwind and huge fortunes were made on that blowup by a lot of different parties, one of which was Goldman Sachs (GS). I can tell you now that the statute of limitations has run out and now that it's unlikely I'll ever get a job there, but Goldman made a killing on long-term capital, for sure.

Q: Will Tesla benefit from the Biden infrastructure plan?

A: I would say Tesla is at the top of the list of companies the Biden administration wants to encourage. That means more charging stations and more roads, which you need to drive cars on, and bridges, and more tax subsidies for purchases of new electric cars. It’s good not just Tesla but everybody’s, now that GM (GM) and Ford (F) are finally starting to gear up big numbers of EVs of their own. By the way, I don't see any of the new startups ever posing a threat to Tesla. The only possible threats would be General Motors, Ford, and Volkswagen, which are all ten years behind.

Q: Would you put 10% of your retirement fund into cryptocurrencies?

A: Better to flush it down the toilet because there’s no commission on doing that.

Q: Is growing debt a threat to the economy? How much more can the government borrow?

A: It appears a lot more, because Biden has already indicated he’s going to spend ten trillion dollars this year, and the bond market is at a 1.70%—it’s incredibly low. I think as long as the Fed keeps overnight rates at near-zero and inflation doesn't go over 3%, that the amount the government can borrow is essentially unlimited, so why stop at $10 or $20 trillion? They will keep borrowing and keep stimulating until they see actual inflation, and I don’t think we will see that for years because inflation is being wiped out by technology improvements, as it has done for the last 40 years. The market is certainly saying we can borrow a lot more with no serious impact on the economy. But how much more nobody knows because we are in uncharted territory, or terra incognita.

To watch a replay of this webinar just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2020/12/john-thomas-lakeshore-e1608229033313.png338450Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-01 11:02:522021-04-01 14:14:23March 31 Biweekly Strategy Webinar Q&A

We are now seven months into the tech correction, and it may come to an end in a month or two. That turn will be dictated by the topping in the ten-year US Treasury bond somewhere around the 10% yield.

So, generational opportunities are starting to open up in some of the best long-term market sectors. It’s time to start building your list of names for when the sun, moon, and stars line up.

Suppose there was an exchange-traded fund that focused on the single most important technology trend in the world today.

You might think that I was smoking California’s largest export (it’s not grapes). But such a fund DOES exist.

The Global X Robotics & Artificial Intelligence ETF (BOTZ) drops a golden opportunity into investors’ laps as a way to capture part of the growing movement behind automation.

The fund currently has an impressive $2.6 billion in assets under management.

The universal trend of preferring automation over human labor is spreading with each passing day. Suffice to say there is the unfortunate emotional element of sacking a human and the negative knock-on effect to the local community like in Detroit, Michigan.

But simply put, robots do a better job, don’t complain, don’t fall ill, don’t join unions, or don’t ask for pay rises. It’s all very much a capitalist’s dream come true.

Instead of dallying around in single stock symbols, now is the time to seize the moment and take advantage of the single seminal trend of our lifetime.

No, it’s not online dating, gambling, or bitcoin, it’s Artificial Intelligence.

Selecting individual stocks that are purely exposed to A.I. is challenging endeavor. Companies need a way to generate returns to shareholders first and foremost, hence, most pure A.I. plays do not exist right now.

However, the Mad Hedge Fund Trader has found the most unadulterated A.I. play out there. A real diamond in the rough.

The best way to expose yourself to this A.I. trend is through Global X Robotics & Artificial Intelligence ETF (BOTZ).

This ETF tracks the price and yield performance of ten crucial companies that sit on the forefront of the A.I. and robotic development curve. It invests at least 80% of its total assets in the securities of the underlying index. The expense ratio is only 0.68%.

Another caveat is that the underlying companies are only derived from developed countries. Out of the 10 disclosed largest holdings, seven are from Japan, two are from Silicon Valley, and one, ABB Group, is a Swedish-Swiss multinational headquartered in Zurich, Switzerland.

Robotics and A.I. walk hand in hand, and robotics are entirely dependent on the germination prospects of A.I. Without A.I., robots are just a clunk of heavy metal.

Robots require a high level of A.I. to meld seamlessly into our workforce. The stronger the A.I. functions, the stronger the robot’s ability, filtering down to the bottom line.

A.I. embedded robots are especially prevalent in military, car manufacturing, and heavy machinery. The industrial robot industry projects to reach $80 billion per year in sales by 2024 as more of the workforce gradually becomes automated.

The robotic industry has become so prominent in the automotive industry that they constitute greater than 50% of robot investments in America.

Let’s get the ball rolling and familiarize readers of the Mad Hedge Technology Letter with the top 5 weightings in the underlying ETF (BOTZ).

Nvidia (NVDA)

Nvidia Corporation is a company I often write about as their main business is producing GPU chips for the video game industry.

This Santa Clara, California-based company is spearheading the next wave of A.I. advancement by focusing on autonomous vehicle technology and A.I. integrated cloud data centers as their next cash cow.

All these new groundbreaking technologies require ample amounts of GPU chips. Consumers will eventually cohabitate with state-of-the-art IOT products (internet of things), fueled by GPU chips, coming to mass market like the Apple Homepod.

The company is led by genius Jensen Huang, a Taiwanese American, who cut his teeth as a microprocessor designer at competitor Advanced Micro Devices (AMD).

Yasakawa Electric is the world's largest manufacturer of AC Inverter Drives, Servo and Motion Control, and Robotics Automation Systems, headquartered in Kitakyushu, Japan.

It is a company I know well, having covered this former zaibatsu company as a budding young analyst in Japan 45 years ago.

Yaskawa has fully committed to improve global productivity through Automation. It comprises the 2nd largest portion of BOTZ at 8.35%.

Fanuc was another one of the hot robotics companies I used to trade in during the 1970s, and I have visited their main factory many times.

The 3rd largest portion in the (BOTZ) ETF at 7.78% is Fanuc Corp. This company provides automation products and computer numerical control systems, headquartered in Oshino, Yamanashi.

They were once a subsidiary of Fujitsu, which focused on the field of numerical control. The bulk of their business is done with American and Japanese automakers and electronics manufacturers.

They have snapped up 65% of the worldwide market in the computerized numerical device market (CNC). Fanuc has branch offices in 46 different countries.

To visit their company website, please click here.

Intuitive Surgical (ISRG)

Intuitive Surgical Inc (ISRG) trades on Nasdaq and is located in sun-drenched Sunnyvale, California.

This local firm designs, manufactures, and markets surgical systems and is completely industriously focused on the medical industry.

The company's da Vinci Surgical System converts surgeon's hand movements into corresponding micro-movements of instruments positioned inside the patient.

The products include surgeon's consoles, patient-side carts, 3-D vision systems, da Vinci skills simulators, da Vinci Xi integrated table motions.

This company comprises 7.60% of BOTZ. To visit their website, please click here.

Keyence Corp (Japan)

Keyence Corp is the leading supplier of automation sensors, vision systems, barcode readers, laser markers, measuring instruments, and digital microscopes.

They offer a full array of service support and closely work with customers to guarantee full functionality and operation of the equipment. Their technical staff and sales teams add value to the company by cooperating with its buyers.

They have been consistently ranked as the top 10 best companies in Japan and boast an eye-opening 50% operating margin.

They are headquartered in Osaka, Japan and make up 7.54% of the BOTZ ETF.

(BOTZ) does have some pros and cons. The best AI plays are either still private at the venture capital level or have already been taken over by giant firms like NVIDIA.

You also need to have a pretty broad definition of AI to bring together enough companies to make up a decent ETF.

However, it does get you a cheap entry into many for the illiquid foreign names in this fund.

Automation is one of the reasons why this is turning into the deflationary century and I recommend all readers who don’t own their own robotic-led business, pick up some Global X Robotics & Artificial Intelligence ETF (BOTZ).

And by the way, the entry point right here on the charts is almost perfect.

To learn more about (BOTZ), please visit their website by clicking here.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-03-31 10:02:412021-03-31 11:07:08Here an Easy Way to Play Artificial Intelligence

Of course, WWII historians know well the man who never was, the popular name for Operation Mincemeat.

In 1943, British intelligence found a homeless man who died on the streets of London, dressed him up as a Royal Marine Major William Martin, and released his body from a submarine off the coast of Spain, a German ally.

Handcuffed to his wrist was a briefcase with highly detailed plans for the allied invasion of Greece and the Balkans. The Germans shifted ten divisions to defend the region.

When the allies invaded Sicily instead, it came completely out of the blue. The invading American and British forces found the island almost undefended and inadequately manned and supplied by Italian troops. The allies planned for three months to capture Sicily. Instead, they did it in a mere 38 days. Allied losses came in at a tenth of those expected, thanks to Royal Marine Major William Martin.

The analogy here is that last week, we witnessed the market that never was. Stocks went down, then up. Bonds went up, then down. Even Tesla was virtually unchanged. It all ended up as a big fat zero for traders.

What all of this means for us investors is a subject of heated discussion among strategists. Of course, the Cassandras are always out there arguing that this is all proof that markets are peaking and that the mother of all stock market crashes is just ahead of us.

I take a different tack.

I think we are well into a long-overdue “time” correction whereby stocks go sideways for weeks or months before resuming their heroic assault on new highs. The timing will be dictated by the frantic reversal of the bond market at a ten-year Treasury yield of 2.00%.

Investors will rotate from the newly expensive recovery plays like banks into the newly cheap, such as technology stocks. Notice the sudden recent interest in legacy companies like Oracle (ORCL), Intel (INTC), and Cisco Systems (CSCO), which completely missed the great 2020 tech rally.

All of this sets up perfectly for the barbell portfolio which I have been advocating all year.

If there is a selloff, it will be by things that normal people don’t own. Those include SPACS, anything the Reddit crowd chases, stay-at-home stocks, and very high-priced tech stocks with no earnings.

Much focus has been placed on the Taiwanese-owned Ever Given stuck in the Suez Canal. As a Middle Eastern war correspondent for many years, I spent endless hours debating with my compatriots over what closure of the canal would mean.

What hasn’t been mentioned was that the accident was not caused by a Chinese captain, but Egyptian pilot ships are required to take on to raise revenues, and bribes, for the impoverished country. This all happened in the middle of a sandstorm where visibility is near zero.

I can tell you right now that they won’t get the Ever Given off there until they start to unload containers and lift off some weight so the 200,000-ton ship can rise of its own accord. Good luck with that in the middle of the Sinai Desert. Why not just sell all the contents on Amazon and have them deliver it for free as part of their prime membership?

This is a debacle that will last weeks, if not months, and will cost $9 billion a day in international trade until it’s over. In the meantime, commercial shippers have asked for protection from pirates from the US Navy as they navigate the unfamiliar water around the tip of Africa.

The Mad Hedge Summit Videos are Up, from the March 9,10, and 11 confab. Listen to 27 speakers opine on the best strategies, tactics, and instruments to use in these volatile markets. The product discounts offered last week are still valid. Start, stop, and pause the videos at your leisure. Best of all, access to the videos is FREE. Access them all by clicking here, click on CURRENT SUMMIT REPLAYS in the upper right-hand corner, and then choose the speaker of your choice.

Weekly Jobless Claims dive by 100,000, to 684,000, a one-year low. The decline was led by Illinois and Ohio. Labor shortages are popping up around the country in skilled areas, but bars and restaurants are still lagging severely.

Huge Office Cuts are coming, with execs planning a permanent 20% cut. Better to give the money to shareholders. Downtowns across the country will change beyond all recognition. How do you turn an office into an apartment?

CP Rail buys Kansas City Southern, for $25 billion, further concentrating the north American rail industry. It’s a steal because an economy entering a decade-long boom moves lots of stuff. It’s also a great North/South international trade play, which is recovering strongly with the exit of our last president. I used to ride box cars on the old Canadian Pacific back in the sixties (you can’t hitch hike where there are no cars), and occasionally the engineers would let me drive. It suddenly makes Norfolk South (NSC) and Union Pacific (UNP) look very tempting.

Another Tesla $3,000 Target was issued by Ark’s Cathie Wood, an early investor. Cathie’s Ark Innovation Fund ETF was up 180% last year largely on the strength of a massive Tesla (TSLA) holding. Her bear case is a low of $1,500 by 2025, nearly triple the current price. She has only one more triple to go to get to my own $10,000 forecast.

Biden has $3 Trillion More to Spend on top of the just passed $1.9 trillion rescue package. It's all rocket fuel for the stock market, not so much for bonds. The money will be spent on a mix of old-line freeway and bridge repair along with new spending on decarbonizing the power grid and social measures. It will be financed by tax hikes on those earning over $400,000. Remember, Roosevelt hiked the maximum tax rate to 90% on the wealthy, where it stayed for 30 years, and Biden is old enough to remember. Daily Air Travelers top 1.5 Million, for the first time in a year. The pandemic low was 200,000 a day. It’s an indication of how anxious Americans have become to travel, and how strong the imminent economic boom will be.

Intel to build two chip fabs for $20 billion in Arizona to address the current severe shortage. US construction is a positive as it helps reduce reliance on foreign supplies. Too bad it will still leave them five years behind (AMD), but it’s a major move in the right direction. It deals with everything investors wanted to hear and moves them solidly into the 10nm architecture market. Buy (INTC) on dips.

New Home Sales Dive, off 18.2% in February, now that the free money train has left the station. Weather was blamed as a factor, with giant snowstorms slamming much of the country. Shortage of supply is another big issue. Some big builders are basically out of inventory and are reduced to selling floor plans with extended completion dates.

US Dollar (UUP) hits a four-month high, with a major assist from rising US bond interest rates. Expect the rally to continue until ten-year yields hit 2.00%, then sell the daylights out of it. With the US money supply growing at a near exponential 30% annual rate, there’s no way the dollar strength can continue. When you increase the supply, you decrease the value, simple supply and demand. My first pick is to buy the Aussie (FXA) a call option on a global synchronized economic recovery. When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000, here we come!

It’s amazing how well patience can help your performance. My Mad Hedge Global Trading Dispatch profit reached a super-hot 18.61% so far in March on the heels of a spectacular 13.28% profit in February.

It was a go-nowhere week in the market, so I limited myself to a single trade all week, a double short in the bond market (TLT) on top of a welcome $5 rally. The position turned immediately profitable.

I still have a deep in-the-money call spread Tesla (TSLA) that is profitable and expires in 14 trading days. That leaves me with 70% cash and a barrel full of dry powder.

This is my fifth double-digit month in a row. My 2021 year-to-date performance soared to 42.10%. The Dow Average is up 9.9% so far in 2021.

That brings my 11-year total return to 464.65%, some 2.08 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 41.30%.

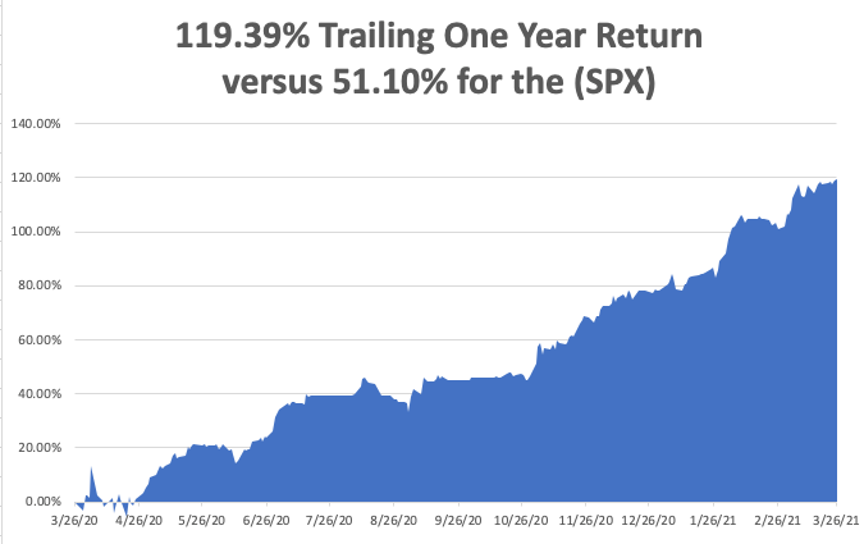

My trailing one-year return exploded to positively eye-popping 119.39%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Corona virus cases at 30.2million and deaths topping 550,000, which you can find here.

Thankfully, death rates have slowed dramatically, but Obituaries are still the largest sector in the newspaper. At this point, some 47% of the US population has achieved immunity through vaccination or catching the disease. Herd immunity is near.

The coming week is a big one for jobs data.

On Monday, March 29, at 9:00 AM, the Dallas Fed Manufacturing Index for March is released.

On Tuesday, March 30, at 9:00 AM, the S&P Case Shiller National Home Price Index for January is published.

On Wednesday, March 31 at 8:15 AM, the ADP Challenger Private Employment Report for March is out. Pending Home Sales for February are indicated at 9:00 AM.

On Thursday, April 1 at 8:30 AM, the Weekly Jobless Claims are published.

On Friday, April 2 at 8:30 AM we get the Nonfarm Payroll Report for March. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, tax time is coming up and let me tell you, I have absolutely the best IRS story of all time.

It comes from my late, dear friend, Al Pinder, who I sat next to for ten years at the Foreign Correspondents of Japan in Tokyo, pounding away on antiquated Royal typewriters until our shoulders were as stiff as boards. Al then was the shipping correspondent for the New York Journal of Commerce newspaper.

Al was a colorful character, to say the least.

In the run up to WWII, Al took an extended vacation in Japan where he toured and photographed the country’s beaches, looking for the best landing sites for the US military in case war broke out.

To sneak the top-secret pictures out of the country, he bought a large steamer trunk and placed them a false bottom. Then he went to Tokyo’s red-light district in Yoshiwara, bought a dubious sex toy, an inflatable life-sized Japanese doll, and placed it on top.

When the trunk was searched, the customs officials found the doll, had a good laugh and passed him on. Al’s photos were the basis of Operation Olympic, the 1945 US invasion of Japan, made unnecessary by the dropping of the atomic bomb.

When the war broke out, Pinder parachuted into western China, where he acted as the liaison with Mao Zedong’s guerilla forces in Hunan province. In 1944, Al received a coded message from headquarters ordering him to intercept a top-secret airdrop from a DC3 in the middle of the night.

Knowing he would be mercilessly tortured by the Japanese if caught, he set up three signal fires in a triangle in a remote part of the desert and managed to find the parachute. Dodging enemy patrols all the way, he returned to his hideout in a mountain cave and opened the package.

In it was a letter from the IRS asking why he had not filed a tax return for the past three years.

I told this story at Al’s wake a few years ago and everyone had a good laugh. Al went on to run CIA operations in Japan during the fifties and sixties. When he passed away, there was a frantic search for a safe deposit box by American intelligence officials containing records of all CIA payoffs to Japan’s leading conservative party.

When the box was finally found, there was an enormous sigh of relief at the embassy. I still miss Al.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2021/02/john-thomas-apple-visitor.png460468Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-03-29 09:02:262021-03-29 10:47:39The Market Outlook for the Week Ahead, or The Week that Never Was

I am once again writing this report from a first-class sleeping cabin on Amtrak’s legendary California Zephyr.

By day, I have two comfortable seats facing each other next to a panoramic window. At night, they fold into two bunk beds, a single and a double. There is a shower, but only Houdini could navigate it.

I am anything but Houdini, so I go downstairs to use the larger public hot showers. They are divine.

We are now pulling away from Chicago’s Union Station, leaving its hurried commuters, buskers, panhandlers, and majestic great halls behind. I love this building as a monument to American exceptionalism.

I am headed for Emeryville, California, just across the bay from San Francisco, some 2,121.6 miles away. That gives me only 56 hours to complete this report.

I tip my porter, Raymond, $100 in advance to make sure everything goes well during the long adventure and to keep me up-to-date with the onboard gossip. The rolling and pitching of the car is causing my fingers to dance all over the keyboard. Microsoft’s Spellchecker can catch most of the mistakes, but not all of them.

As both broadband and cell phone coverage are unavailable along most of the route, I have to rely on frenzied Internet searches during stops at major stations along the way to Google obscure data points and download the latest charts.

You know those cool maps in the Verizon stores that show the vast coverage of their cell phone networks? They are complete BS.

Who knew that 95% of America is off the grid? That explains so much about our country today.

I have posted many of my better photos from the trip below, although there is only so much you can do from a moving train and an iPhone 12 Pro.

After making the rounds with strategists, portfolio managers, and hedge fund traders in the run-up to this trip, I can confirm that 2020 was one of the most challenging for careers lasting 30, 40, or 50 years.

This was the year that EVERYTHING crashed, then posted heroic recoveries. Comparisons with 2008, 1999, and 1929 were frequently made. It truly was a year of extremes.

My own 66.64% return for last year is the best in the 13-year history of the Mad Hedge Fund Trader, nearly ten times the Dow Average performance of 7.3%. Yet, even during the darkest days of the March bottom, when the Dow was down 40%, we were never down more than 12%.

That took my eleven-year average annualized return up to an eye-popping 38.18%.

If you think I spend too much time absorbing conspiracy theories from the Internet, let me give you a list of the challenges I see financial markets are facing in the coming year:

The Ten Key Variables for 2020

1) Will the Covid-19 vaccine work, or will new mutations render it useless?

2) When will the pandemic peak, at 500,000 or 1 million deaths?

3) Will there be a double dip recession in Q1, or will the economy keep powering on?

4) Will the Democrats get control of the Senate through the Georgia Senate races, paving the way for more government spending?

5) Will technology stocks continue to dominate, or will domestic recovery stocks take over for good?

6) How long will the commodities boom continue?

7) Is the US dollar dead for good or are we approaching a bottom?

8) How long can the Fed artificially support the bond market, or is a crash imminent?

9) Has international trade been permanently impaired or will it recover?

10) Is oil seeing a dead cat bounce or is this a sustainable recovery?

With the worst economic whipsaw in American history taking place in 2020, one might be hesitant about making forecasts for 2021. However, I shall press onward.

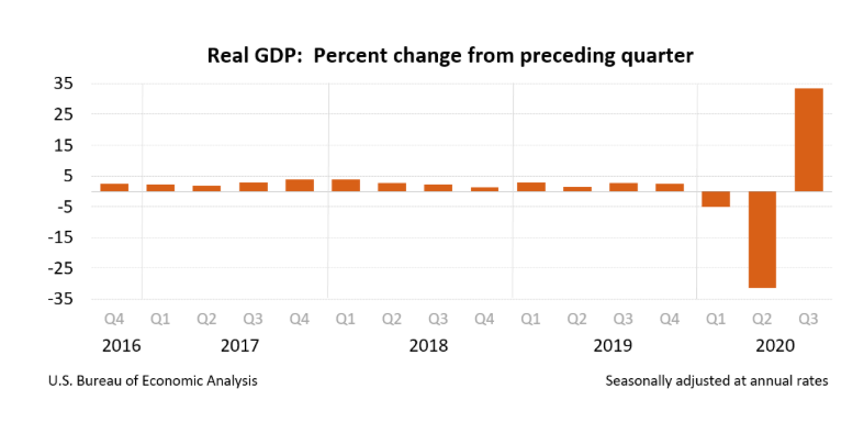

Last year saw a horrific 32.8% drawdown in Q2 GDP followed by an explosive 33.4% growth in Q3. It was the perfect “V” shaped recovery. However, we won’t see 2019 GDP levels until 2022, so there is plenty of growth to come, both nationally and on an individual company basis.

The reopening of the economy will bring us more double-digit growth after a Q1 slowdown mired by a peaking pandemic and delayed stimulus spending.

But it won’t be the same economy.

I figured out early that the pandemic was instantly moving us ten years into the future, placing a turbocharger on all existing trends. The economy is digitized at a rate that it has never seen before at the expense of mass closings of shopping malls and other old-line business models.

This will continue.

The online economy, working at home, and Zoom meetings are here to stay. You can’t get the genie back into the bottle. That has permanently increased the profitability of all the benefiting industries, while many others will never come back. As a result, the investment portfolio you should own in the future will look nothing like the one you had in the past. It’s not your father’s stock market.

It all sets out a base for an economic boom that could extend for another decade. Yes, Virginia, the Roaring Twenties are here. Better learn that Charleston!