Regular readers of this letter are probably weary of me harping away about the financials as a great place to put your money for the rest of 2014.

Never mind that these names have all jumped 10% in the past month. But this is not an ?I told you so? story. This is more of a ?But wait, there?s more,? story.

The basis for my call is quite simple. I believe that bond prices are peaking, and yields bottoming. As mining the yield curve is a major source of bank profits, borrowing short term and lending long term, a rise in interest rates falls straight to the bottom line. Thus, buying banks is an indirect way of selling short the bond market.

However, there are many more reasons to overweight this long neglected sector. In a market that has gone virtually straight up for the past three years, many large institutions are going to be forced to roll money out of leaders, like my favored technology, energy and health care, into laggards, such as the financials.

Expect this trend to accelerate as we head into yearend institutional book closing, which start as early as October 30.

Look at other important drivers of bank profits, and you?ll find them at multi decade lows.

Trading and investment banking volumes are off 30%-40% from mean historic levels. We options traders already know this all too well, as turnover has cratered and spreads widened due to investor lack of interest.

This is especially true of put options, which are now being given away virtually for free. Volatility that seems to permanently live at the $12 handle is another such indicator of this disinterest.

This will not last. If my ?Golden Age? scenario plays out in the 2020?s (click here for ?Get Ready for the Coming Golden Age?), trading and investment banking volumes will not only double to return to the norms, they will skyrocket tenfold from today?s tedious, moribund levels.

Indeed, I have recently discovered an entire subculture of financial oriented private equity firms currently amassing portfolios that are betting on precisely such an outcome. Think of big, smart, long-term money. The big bets on the coming decade are being made now.

There is another ripple in the case for banks. After passage of the Financial Stability Act of 2010, otherwise known as ?Dodd Frank?, banks became target numero uno of the federal government. The public?s demand for accountability for the 2008-09 crash knew no bounds.

As a result, the fines and settlements with the big banks, most of which were rescued from bankruptcy by the government, now well exceed $100 billion. Four years into the enforcement onslaught, the Feds are running out of scandals to prosecute. There is nothing left for the banks to plead guilty to.

This means that a major portion of the banks? costs are about to disappear, not only new massive fines, but hundreds of millions of dollars in legal fees and diverted management time as well. More money drops to the bottom line.

Dramatically rising income? Substantially falling costs? Sounds like ?Ka-ching? to me, and a ?BUY? for the bank stocks.

The bottom line is that bank stock could double from here in coming years. It is not hard to pick names. Bank of America (BAC) took the big hit on fines and settlements, and therefore should enjoy the largest bounce.

So should Citigroup (C), which came the closest to vaporizing. And for good measure, I?ll throw in American Express (AXP) as a play on the burgeoning credit card spending by the growing class of well to do.

Barney Frank Had a Few Things to Say

https://www.madhedgefundtrader.com/wp-content/uploads/2013/05/John-Thomas-and-Barney-Frank.jpg357577Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-09-03 09:29:542014-09-03 09:29:54The Case for Buying Financials

In recent weeks, I couldn?t help but notice the green and white vans of Solar City (SCTY) visiting my neighbors. My trader?s radar went up, so I thought there might be an opportunity here.

With my second Tesla (TSLA) about to be delivered, the Model X SUV, it was time for me to review my electricity bill.

My first Tesla, an S-1, boosted my monthly power consumption from 600 kWh to 1,800 kWh per month, about what a small industrial facility might use. Yet, my bill from PG&E increased from only $350 to $450 a month. This is because they effectively give away power for free from 12:00 AM to 7:00 AM to qualified EV users, charging me only 4.7 cents per kWh.

On my suggestion, Tesla then upgraded their software so vehicles could be programmed to recharge only at these hours. That means it is costing me $4.00 for a full 80 kWh charge that can take me 255 miles, or 1.6 cents a mile. That doesn?t include the enormous savings on maintenance (there is none).

Well then! The IRS currently allows a mileage deduction of 56 cents per mile for business purposes, so that?s an opportunity to exploit right there.

Given that the average US car now gets 25 miles per gallon of gasoline (and that is being generous), that means my equivalent cost for running my S-1 works out to paying a scant 40 cents a gallon.

This compares to the $3.60 at the local service station ($3.45 at Costco), which is at a one year low, or a savings of 89%. That is a little more than I paid for gas when I first started driving a beat up VW Bug at the Santa Anita Race Track parking lot back in 1967.

That sounds like a deal to me.

However, the second Tesla is likely to boost my monthly power consumption from 1,800 kWh to 3,000. When PG&E sees bills that big, they assume someone is operating an illegal marijuana grow house and send the DEA to kick your door down at 5:00 AM on a Monday morning.

So I was on the phone to Solar City the next morning. What I heard was nothing less than amazing.

For a start, they called up a Google Earth mapping program that focused on a picture of my roof from a low earth orbit satellite (Google has invested $280 million in Solar City). Then a second program autofit their existing solar panels to my roof and spit out a mass of numbers.

This complete stranger told me things about my roof that I never knew, like it was 4,000 square feet of flat concrete tiles on 14 planes. Welcome to the 21st century.

I nervously looked down and made sure my fly was fully zipped up.

He went on to tell me that he could fit a 15 kW DC system on my roof that would generate 106% of my power needs, generating 19,365 kWh a year. That would make me completely self sufficient in electricity, even though I will be charging two hulking Tesla 1,000 pound lithium ion batteries every day.

They will install a ?net? two-way electric meter on my house. When the sun shines, it will run backwards as I can sell power to PG&E (PCG) at high prices.

At night, when I recharge my cars, I would then buy cheap power from Solar City. No storage devices are required. The PG&E grid is effectively the storage system. That would turn me into a day trader of electricity, selling high by day and buying low by night. I love it!

How did their satellite know I was a hedge fund trader? What else does it know?

Now comes the best part. The cost of the installation and panels was $66,000. Solar City would do it for free. Yes, free, as in gratis, with no money down. They would lease me the panels for 20 years, with an annual price increase of 6.2%. That would cut my monthly electricity bill from $450 to $200. It does this by eliminating the tier 3, 4 and 5 prices I am currently paying PG&E.

If I sell my house, I can either buy out my contract at the discounted, fully depreciated value, or pass it on to the new owners. It is well known that solar panels significantly increase the value of existing homes.

Installation can be done in a day. But it can only take place on unbreakable concrete tile roofs. Those made of clay tiles, metal, tar and gravel, wood shakes, or slate don?t work for various reasons. You need a FICO score of 680 or better to qualify. There is a 60-day waiting list to get this done.

It didn?t take me long to figure out the game here. By purchasing the panels and leasing them to me, they keep the 30% government subsidy for capital investments in alternative energy, which works out to $19,890 for my house alone. Solar city also gets to depreciate these panels on an accelerated schedule, mostly in the first five years.

This explains why Solar City has grown larger than the next 15 competitors combined. Solar City?s largest customer is the US Army, which has already installed panels on 1 million structures.

There is one cautionary note to add here. The government subsidies that help float the company expire in 2018, making the entire proposition financially less attractive. That is, unless they get renewed. Think President Hillary.

The only things that would save them are dramatically higher conventional energy costs. However, right now energy costs are heading the opposite direction, thanks to fracking.

As with everything else Elon Musk touches, an investment in Solar City has been wildly successful. Since the company went public at the end of 2012, the shares have risen by an awesome 670%. Needless to say, with no earnings, and no dividend, the $6.5 billion market cap company may appear hopelessly expensive.

Like with Elon?s other company, Tesla, your aren?t betting on the value of the business today, but where it will be in five years, when it has a far larger share of the market.

Given Musk?s track record so far, that is a bet that I am willing to take.

My Home from Outer Space

It?s Been a Long and Winding Road Driving from This?

To This

https://www.madhedgefundtrader.com/wp-content/uploads/2014/08/John-Thomas-Tesla.jpg330317Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-08-28 09:35:342014-08-28 09:35:34Taking a Look at Solar City

Those who followed my advice to buy Apple a year ago are now drowning in riches (click here for ?Buy Apple on the Dip?). Since the July, 2013 bottom, the shares have risen by a meteoric 92%. It is the largest company in the world once again.

As a result, I have heard of my readers shopping for second homes on Lake Tahoe, sponsoring NASCAR teams, or buying new Rolex watches for significant others.

I recommended China Mobile (CHL) then as well, the big beneficiary of a new deal with Apple, whose shares have also gone ballistic.

The question of the day is: ?Now what do we do?

You are right to ask the question. The company?s stock is notorious for running up massively into every major product launch, and then giving back a big chunk afterwards.

So while the expected announcement of the iPhone 6 on September 9 is welcomed as producing a major new source of revenue, it could also signal the end of the current run.

Take a look at the long-term charts, and the hair on the back of your neck should stand up. The fanfare for the iPhone 6 will almost exactly come at a potential double top in the stock price. Could we be setting up for the greatest ?buy the rumor, sell the news? of all time?

The last time we visited this territory, which we visited on the launch of the iPhone 5, Apple?s shares plunged a gut churning 45%, prompting some shareholders to dump their iPhones in the trash.

Certainly the problems that caused the rally to fail last time are kicking in once again. The law of large numbers applies once more. Apple?s market capitalization is at $607 billion today. There may not be enough equity investors in the world to push the shares up appreciably from here.

Oh, and because of the recent rapid appreciation, most institutions are now overweight Apple, as they were in September, 2012. The only difference is that Apple accounts for only 3% of the S&P 500, compared to a hefty 5% two years ago.

The shares are now at a 15.5 earnings multiple, up from under 10 at the recent bottom, and 7 if you took out all of the cash. That is still a discount to the main market, as well as most other technology stocks.

The truth is that this is not your father?s Apple.

CEO Tim Cook has shown a much greater respect for investors compared to founder, Steve Jobs, who despised Wall Street with a passion. I know, because I escorted Steve to meet with institutional investors looking at a secondary share issue during the early 1980?s. It was not a happy time for me.

There is a $50 billion stock buyback program in place, which soaked up a ton of shares at the bottom.

We also now have a 2% dividend yield, a mere 37 basis points through ten year Treasury bond today, another idea Jobs poo pooed.

The company is also strategically in a much stronger position than it was in 2012. Apple has a far broader, more attractive, and more advanced product range than it did only 24 months ago. The China Mobile deal has kicked in big time.

There is immense demand for the new larger screen, faster iPhone 6, which will offer consumer untold bells and whistles. Some 50% of the iPhones in existence are 4s?s or older, so upgrades from the installed base will the largest in history.

This will enable it to retake market share from hated rival, Samsung, which moved to a big screen in 2013. This will open the way for an expansion of Apple?s profit margins, possibly by 25% or more.

Samsung?s smart phone strategy all along has been to copy Apple?s patents and milk them for whatever they are worth, before they inevitably lose the next infringement case in court. As I never tire of telling listeners at my speaking engagements and luncheons, you can?t steal your way to the top in technology.

I would expect, at the very least, that the market has to put the double top theory to the test at least once. That alone will prompt a 10% correction, back down to $92.

Then, if we really are still in a bull trend, it will bounce off that number and head to new highs. If it doesn?t, then it?s game over until the run up to the next big product launch. The iPhone 7?

So the clever thing to do here has to be to do a buy write and sell short Apple September, 2014 $105 calls against you existing stock position.

At this moment, you can get 96 cents for them, with September 19 expiration. If you are braver still, you can go out another month and take in $2.01 for the October 17, 2014 calls. Don?t go farther out than that, or you might miss the yearend rally.

That way, if the stock keeps rising, you will sell your shares out at the higher price of $105. If it falls, your average cost declines by 96 cents, or $2.01. Either way, it is a win-win.

Isn?t that what you pay me for?

Meet Your New iPhone

https://www.madhedgefundtrader.com/wp-content/uploads/2014/08/iPhones.jpg250484Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-08-27 01:04:002014-08-27 01:04:00What to Do About Apple?

We have snatched 92% of the potential profit in the Currency Shares Euro Trust (FXE) September, 2014 $133-$135 in-the-money bear put spread, riding the Euro (FXE) down on the short side, from $1.33 down to $1.30.

The risk/reward of continuing with such a large position is no longer justified.

So I am going to reduce my overweight position down from 20% back to a more normal 10%. If you are similarly overweight the ProShares Ultra Short Euro ETF (EUO), I would also be lightening up, retuning to a normal weighting there as well.

I have not suddenly fallen in love with the beleaguered continental currency. I think we are headed towards $1.27, $1.20, and eventually $1.00. This is just a short-term tactical move.

That way, if by some miracle, we get a two-cent rally in the Euro, I will have plenty of dry powder to reload with and add more shorts.

The big event of the weekend was European Central Bank President, Mario Draghi, ramping up his war on his own currency.

On Friday evening, after the markets closed and traders were long gone for the Hamptons, Bal Harbor, or Napa Valley (oops), Draghi ramped up his rhetoric, warning that he would use ?all available tools? to spur Europe?s economy. This is central banker talk for throwing down the gauntlet at the feet of the monetary hawks (read Germans).

He then threw the fat on the fire, opining that the recent decline an inflation expectations were a concern, and this was a topic for the coming September 4 ECB meeting. Translation: this is a central banker?s equivalent to giving the hawks the middle finger salute, and then putting the pedal to the metal on the easing front.

The bottom line for all of this is that the ECB is almost certain to cut Euro interest rates next week. As interest rates differentials are the primary driver of foreign exchange markets, this is great news for the greenback and terrible news for the Euro.

After that, we may get a small rally in the Euro, as short sellers, like me, take profits. This has been the pattern with other Euro interest rates reductions in the past. That is the rally I want to resell into.

You can expect this pattern to continue until Europe solves its structural monetary problems, which will take years. The current flawed system dramatically undervalues Germany?s currency, while overvaluing the currencies of Italy, Spain, Portugal, and Greece.

This is why the German economy is healthy, while everyone else?s economies suck. Without the Euro, the old deutschmark would be double or triple what it was, demolishing the country?s massive export business. In the meantime, the other countries would be devaluing their own currencies like crazy.

We caught the entire reaction to Draghi?s verbiage at this morning?s opening, with the Euro gapping down a full half-cent against the dollar. The stop loss selling was severe.

I wish all my trades were this easy. Since I doubled up on the short side, the Euro has been in a complete free fall. European dithering has been one of the lowest risk bets of 2014.

That said, I think I?ll get back to cleaning up my earthquake damage.

https://www.madhedgefundtrader.com/wp-content/uploads/2014/08/Falling-100-Bills-Euros.jpg249430Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-08-26 01:04:512014-08-26 01:04:51Why I?m Covering Some Euro Shorts

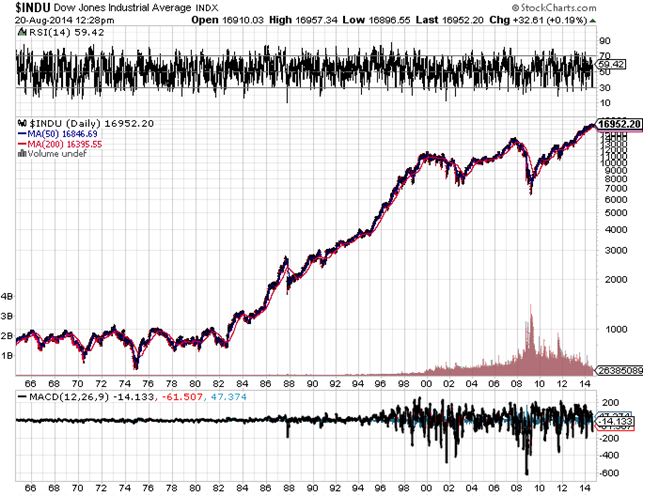

If anyone had any doubts about the future direction of stocks this year, you better take a look at the chart below for the S&P 500.

It shows a very convincing trend upward at almost a perfect 45-degree angle going back for the past year. The range is 100 points wide. It?s almost as if an architect drew it with drafting tools.

To take maximum advantage of this trend, you have to buy every 80 dip, as the floor is constantly rising. It?s as simple as that. Think of Trading 101 for Dummies.

We have had a host of challenges that threatened to knock us out of this channel for the past year.

A second Cold War with Russia? Wake me up when it?s over.

The ongoing collapse of Iraq? Snore?

The suspension of oil exports from Libya barely elicited a blip on your screen, as did the horrific civil war in Syria, a replay of the Middle Ages.

China slowdown? Pshaw! ?Sell in May and Go Away?? Cancelled!

Subpar American economic growth? No problemo.

All of these problems the market has weathered nicely, much like a wet dog shakes off water.

In fact, it has been three years since we endured the distress of a 10% correction, the self-inflicted wound triggered by the government?s hand wringing debt ceiling crisis.

In the end, it amounted to nothing, and was the last decent buying opportunity traders have seen. It has all be one giant ?chase? for performance and reach for yield since then.

The lesson of all of this is that what counts is the good old USA. That is what really is driving markets. All of those foreign distractions are just so much noise. At the end of the day, only the health of the American economy is what matters.

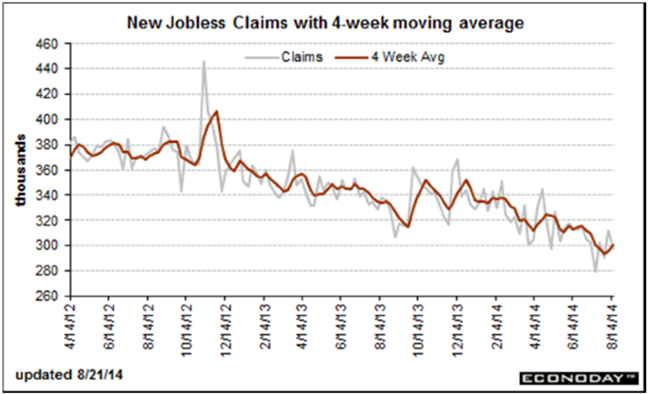

That?s all great news, because our economy is looking pretty darn muscular. Just last week, we saw the Markit August Purchasing Managers Index rocket from 55.8 to 58.0. Weekly jobless claims, the most accurate predictor of true business activity in this cycle, is plumbing seven-year lows. Housing data has just engineered a dramatic turnaround.

It gets better. The upshot of last week?s gathering of Federal Reserve officials at Jackson Hole, Wyoming is that ?normalization? is the new word du jour. What does this mean to us plebeians?

That the economy is so healthy that the government is actually thinking of raising interest rates sometime in the far future, possibly at the end of 2015, and then only by a little bit. That would bring to an end eight years of zero interest rate policy.

Until then, you have a government issued license to print free money. Buy the dips and sell the rallies, and work the 100-point range. If we continue ascending as we have done, the (SPX) should reach 2,100 by December, which happens to be my long held yearend target.

My bet is this could run all the way until April, when the next round of seasonal weakness kicks in again. If there is a risk of anything, it is that the buyers start to panic over missing the move and the (SPY) melts up, possibly as high as 2,200 by January, and 2,300 by March.

Of course, it?s always useful to engage in what my role model, Albert Einstein, called ?thought experiments? and consider what might cause the wheels to fall off of the bull market. To consider that in depth, please read ?What Could Derail the Coming Golden Age? by clicking here.

So what individual sectors should you focus on now? I hate to sound redundant and repetitive. As you may have noticed, ?boring? is not in my DNA (sending Trade Alerts on my iPhone while hanging by ropes from a cliff in the Swiss Alps during a ferocious storm?).

However, I?ll hark back to my favorite three legs for the economy, technology, energy, and health care. Biotechnology continues to sizzle, as do the car companies. And if bonds are peaking, as I believe, the entire financial sector is a screaming buy here.

One unknown is how the markets will take the Alibaba IPO in September, with an expected $150-$200 billion valuation, the largest in history. If institutions have to unload their existing holdings to make room for the new issues, it could trigger our next 4% correction. If that happens, buy the dip with both hands.

By the way, now that the summer is ending, subscription renewals are coming, so don?t forget to ?re-up? if you want to continue with your 41% average annualized returns.

Hey, the house is starting to shake. I think it?s an earthquake, a big one. Better get this out before the broadband goes down?

Uncle Sam is Looking Pretty Muscular These Days

00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-08-25 09:39:332014-08-25 09:39:33My End 2014 Stock Market Forecast

Many commentators are warning of a top, a bubble and Armageddon to come in the stock market. There has not been a 10% correction in the indexes since the debt ceiling crisis three years ago.

But I think that we are just getting started.

Share prices have the rocket fuel for the Dow average to make it to 18,000 by the end of 2014, and possibly 100,000 by 2025. To understand why, you have to focus on major long-term structural changes occurring in the global economy which at this point only a handful for strategists can see, and then, only faintly.

The evidence couldn?t be more undeniable. The major stock indexes have repeatedly broken out to new all time highs in 2014. The more volatile and economically sensitive Russell 2000 small cap index has left it in the big caps dust.

Inflows to equity mutual funds have been the most prolific since 2008. It all paints a picture of a run up (SPX) to and of 2,100 by year-end, which by the way, has been my own forecast all year. Perma bears be damned!

Betting on the Federal Reserve?s fears of a replay of 1937, when premature tightening tipped the US economy into the second leg of the Great Depression, has been a huge winner for me for years now. It means that it is willing to err on the side of over stimulation, by a lot.

With wages growth stagnant for decades, and many commodity prices and precious metals down 30% or more year to date, the Fed certainly has a free pass on the inflation front to do so. Corporate earnings are also helping, consistently surprising to the upside.

However, I think the market is trying to tell us infinitely more than what appeared in yesterday?s headlines, or what flew by in the last tweet or text. There is something deeper going on here beyond the noise of the daily data releases. Asset prices are acting like there is a major structural change underway in the world economy, which so far has remained invisible to all except the market.

Yes, there are a few professionals out there who can see imminent momentous change within their own narrow industries. But no one has yet aggregated all these changes together, so I?ll take a whack at it.

Here are ten theories for you to contemplate.

1) There is more Peace Dividend to Pay - Is it possible that the markets have not yet fully discounted America?s victory in the Cold War? That the payout was interrupted by the dotcom and housing crashes, and that it is now resuming?

Yes, we priced in a chunk with the run up in the Dow average from 2,500 to 11,000 during the 1990?s. But could there be more to go? After all, 22 years since the fall of the Soviet Union and the US still faces no industrial strength enemy, and there are none on the horizon either.

At the very least, this reality should be enough to chop our current defense spending by half, and eliminate most of our budget deficit. Much of the defense establishment agrees with me. They?d rather be spending money on inexpensive, high value, targeted programs, like cyber warfare and drones, rather than the costly, politically inspired, heavy metal weapons systems of old.

2) Obama Care Works ? With the House of Representatives voting to repeal the President?s health care plan for the 50th time, and closing down the government for 16 days in protest, conservative antipathy towards Obamacare couldn?t be more clear. But what if, instead of doubling health care costs as the right has claimed, it drops them by half? What if the plan does add 0.5% to annual GDP and creates 2 million jobs?

This, after all, was the original plan. Health care is expensive in the US because of the lack of competition, and Obamacare delivers that in spades for the first time. Of course there were going to be teething problems. After all, the government is trying to create 50 Amazons overnight at once. It took 20 years for my former Morgan Stanley colleague, Jeff Bezos, to create just one.

The early evidence shows that the competitive health insurance exchanges the plan sets up are delivering price reductions of 30% to 50% in New York and California. I walked into Costco the other day and was offered a plan for $235 a month with an $8,000 deductable, just so I could avoid the penalties for the uninsured. The best offer I previously received from Blue Cross of California was $3,500 a month, typical for an elderly white male like myself.

If this, in turn, solves the health care and Social Security crisis, it will do a lot to wipe out that ?uncertainty? you hear so much about. The predictions of the eventual insolvency of the United States, a perennial Internet conspiracy favorite, also go down the drain.

3) Another Technology Revolution ? Are we on the verge of another great technology breakthrough like the one we saw during the dotcom boom, when PC?s, the Internet, and the World Wide Web simultaneously came together to supercharge corporate earnings for a decade? What if the cost of treating cancer drops from $100,000 to $200, as my friend, Dr. Michio Kaku, believes. What if new Apples and Googles (GOOG) continue to appear out of nowhere?

If you lived in San Francisco and were barraged by venture capital pitches on a daily basis, as I am, you would think this new Golden Age is going to start any minute. There are a thousand innovations percolating out there.

The only question is whether the lead industry will be communications, health care, energy, or all three. Ride your bike south of Market Street someday and see how much research capacity is being built now, the size of a small city. It is awe-inspiring.

4) The Real Cost of Energy Collapses ? We all know about the new 100-year supply of natural gas discovered under our feet that will turn us into Saudi America. But there are 100 additional ways that energy supply is improving and demand is falling.

Conservation will be huge, as will grid and utility modernization. What if Tesla?s (TSLA) Elon Musk is able to deliver a $40,000 electric car with a 300-mile range in three years, as he has promised? This will be a game changer. His track record so far is pretty good.

This is the man so brimming with confidence that he just bought James Bond?s submarine car for $1 million (see the cool modified Lotus in The Spy Who Loved Me). Falling energy costs mean that the profitability of virtually every listed company goes through the roof.

It is likely that if Iran ever does make good on its threat to close the Straights of Hormuz, no one will care. Some 80% of that oil, and soon to be 100%, goes to China, and that will be their problem, not ours.

5) Productivity Accelerates ? By relentlessly introducing new technologies and cutting costs, corporate profitability has soared for the past 30 years. Pessimists now say things can?t get any better. But what if they do?

As I tell guests at my strategy luncheons, this is not a mean reverting data series. Having invested in the machine that took your labor force from 1,000 to 100, what if the next one brings it to 10? Guess which country is about to lose millions of jobs from offshoring and new technology? China. Just talk to any European CEO about their new ?American Strategy.?

6) Interest Rates Stay Low for Another Decade ? If wages stay in check, oil prices fall, and commodity places stay low, then the Fed has absolutely no reason to substantially raise interest rates for another ten years, no matter what the economy does. The next demographic push that creates a worker shortage and higher wages doesn?t start until the early 2020?s.

Sure, the Fed will probably normalize overnight rates back to 2% by next year, as the safety net for the economy is no longer needed. But rates could remain historically very low for quite a long time. This savings immediately drops to the bottom line of any borrower, be they individual, corporate, or government.

In fact, looking at the main causes of the recessions for the last 50 years?a spike in interest rates or a sudden cut off in oil supplies, and absolutely none are visible on the horizon, for now.

7) Shinzo Abe Saves Japan ? The conventional wisdom is that the new government in Japan is resorting to a last desperate act to save their economy that will fail, and that a complete collapse of their over leveraged financial system will result.

But what if Abe gets his necessary reforms through and the country regains its powerhouse status. If Japan?s $6 trillion economy, the world?s third largest, bounces back from a 1% to a 4% GDP growth rate, there will be positive implications for all of us.

8) Europe Gets Its Act Together ? It seems that all we ever hear about from the continent is debt crisis and stagnation and a political system so fragmented that no one can do anything about it. But what if new leadership emerges and takes the initiative to coalesce and solidify Europe?

That would involve creating a single Ministry of Finance, issuing pan Euro bonds, and a European Central Bank with teeth and courage. Their economic problems would disappear and growth would double. As part of my consulting arrangements with governments there, I have been recommending these measures for years, and everyone agrees. All that is missing is the political will to carry them out.

9) The Dollar Stays Strong ? With America?s debt to GDP now over 100% and rising, many analysts believe it is just a matter of time before we see a major crash in the dollar. This is only the continuation of a 220-year-old trend.

What if it goes up instead? Energy independence means we will no longer ship $250 billion a year to the Middle East to pay for oil imports. CEO?s in Europe and Asia are stumbling over each other to find ways to get capital into the US to take advantage of a stronger economy. Higher growth rates mean the feared American deficits start shrinking on their own, with no action from congress whatsoever. This is all long-term dollar positive.

10) Multiples Keep Expanding ? Most strategists believe that the S&P 500 is fairly valued at 1,983 with a price earnings multiple of 15 times, dead in the middle of its historic 9-22 range. But if any of my theories above unfold, then much higher multiples are justified. If they all unfold, then investors wouldn?t hesitate to pay a 25 multiple for American stocks, as their future outlook is so unremittingly positive.

You may say this sounds crazy, and you?d be right. But remember, twice in the last 25 years we have seen market multiples skyrocket to 100. Japanese share valuations reached that nosebleed summit in 1989, and American Dotcom stocks did so in 2000. And they reached those numbers with fundamentals far less substantial than we are facing now. Just take multiples on today?s market up from 15X to 20X, and the Dow should be worth 26,000.

Sure, all of the above represents a pie in the sky best-case scenario. Some, or none, of them may actually play out in the real world. But the ones that do occur will have a super-leveraged effect on each other. The net impact will be US GDP growth easily leaps back from today?s feeble 2% to the virile 4% or more that we grew comfortable with during the fifties, sixties, and eighties.

That growth rate will solve America?s Social Security, Medicare, and deficit problems in fairly short order, without any action by the government.

Needless to say, all of the above is hugely positive for the stock market. It brings forecasts for a Dow 18,000 by the end of 2014, and 100,000 by 2025 out of the realm of fantasy. It kind of makes today?s stock prices look dirt-cheap.

Maybe that?s what the market is trying to tell us, if we only had the patience and the foresight to listen.

This doesn?t mean that you need to rush out and buy more stocks today. Some of these trends will take a decade or more to play out. Better entry points will no doubt present themselves. But the writing is on the wall for higher equity prices, not just in the US, but globally.

I can tell you from the vast expanse of my own 45 years in the prediction business, I have learned one thing. All that is forecast never happens, and all that happens was never forecast.

I?m still waiting for my flying car, although the Tesla S-1 comes close.

My Tesla S-1

https://www.madhedgefundtrader.com/wp-content/uploads/2013/05/JT-with-Tesla-e1427723768460.jpg227400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-08-21 01:03:432014-08-21 01:03:43Why US Stocks Are Dirt Cheap

You usually don?t expect US housing data to cause the collapse of a foreign currency. But that is exactly what happened this morning.

The announcement by the Census Bureau that new home stats for July came in at a breathtaking 1.09 million, up 15.7%, blew away even the optimistic forecasts. Earlier figures for June were revised up substantially.

New building permits for July came in at a robust 1.1 million. Perma bears on the housing market were sent scampering to lick their wounds.

The real shocker was that the Euro promptly dropped 50 basis points, piercing a major support level on the long term charts. The short Euro ETF (EUO), which I have been recommending since the spring for my non-option clients skyrocketed. That clears the way for a run in the (FXE) down to $127.

The (FXE) wasn?t the only asset that saw a kneejerk reaction. The Treasury bond market (TLT) dove by 1 ? points. It is now 2 ? points off the short squeeze high last Friday, when false rumors of a Russian invasion of the Ukraine caused traders to panic. This sent the ProShares Ultra Short 20+ Year Treasury ETF (TBT) soaring, which I am also long.

You can come up with a nice academic theory as to why there is a connection between American housing data and the beleaguered continental currency. Stronger housing means a better economy and higher dollar interest rates, sooner.

As interest rates differentials are the primary driver of foreign exchange markets, this is great news for the greenback and terrible news for the Euro.

The truth is a little more complicated than that. The outlook for the European economy is now so poor, thanks to the sanctions against Russia, that traders and investors have been desperate to add to their short positions. After the prolonged, one-way move down we saw this summer, the Euro managed barely a one-cent short covering rally in the past week.

There is another factor that no one else is talking about. Scotland is about to hold a referendum on whether it should break away from the United Kingdom. Scottish nationalists are hoping for the best.

If successful, it could spur other independence movements across Europe. Catalonia is having a similar vote to break away from Spain in November, with some separatists avid followers of this letter (yes, that?s you, Joan!). The Basque region is not far behind. If this trend ripples across the continent, it would be hugely Euro negative.

The European Central Bank is almost certain to lower Euro interest rates and expand quantitative easing at a September or October meeting. This will weaken the Euro further, paving the way for a move to $127, and eventually $120.

That?s why I am doubling my shorts in the (FXE) today, even though we are at the low for the year. Non-options players should buy more of the ProShares Ultra Short Euro ETF (EUO).

The Euro is Not Looking So Hot

https://www.madhedgefundtrader.com/wp-content/uploads/2014/08/Mario-Draghi.jpg269401Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-08-20 08:50:102014-08-20 08:50:10The Euro Breaks Down

Treasury bonds spike to new one year highs, closing at a 2.40% yield, and trading as low as a 2.30% yield in the overnight market at one point last week. Clearly, serious deflation is continuing for the indefinite future.

Buy more bonds!

US corporate profits are at all time highs, just closing one of the strongest reporting periods in history. What?s more, the outlook they painted for the rest of the year is rosy. With dividend yields for many shares in excess of interest rates paid by government bonds, the bull market is alive and well.

Buy more stocks!

Stocks! Bonds! Stocks! Bonds! Which group of talking heads is right? The stock bulls or the bond bulls?

Yikes! What is a poor money manager to do?

Here is the certain answer to your plaintive question: They are both right.

So how does one deal with this dilemma? It?s easy. You buy everything, both stocks and bonds. That has been the judgment of the markets, which have sent both bonds and stocks flying in tandem for most of 2014.

How is this possible? Doesn?t this violate Economics 101? Should I take my copies of Paul Samuelson and Graham & Dodd and sell them on Ebay?

Not really.

Here is the explanation for it all. The world is now facing a cash glut unprecedented in history. There is so much money chasing everything these days, it is truly unbelievable for those of us rather long in the tooth. Prices can only go northward, whatever they are for.

Take a look at the U.S. government?s accounts, and you get a partial explanation. Over the past four years, the budget deficit has nearly vaporized, from a stratospheric $1.6 trillion to only $600 billion. Next year, $300 billion is in the cards.

This has caused the Treasury to massively cut back on new issuance. In fact, some recent government bond auctions have faced an outright shortage of bonds, prompting bid prices to spike.

The incredible thing is that this has been happening in the face of the Federal Reserve?s winding down of quantitative easing. By October, it will have removed $80 billion a month in bond buying to zero. Imagine how low rates would be by now if my friend, Fed governor Janet Yellen, had kept it going.

This is why virtually everyone in the world got the bond market wrong this year, calling for a swan dive, except for bond maven and hedge fund guru, Jeffrey Gundlach. I include myself in this category of errant prognosticators.

However, I still have a chance to be right. I expect bonds to give up all of their gains going into yearend, ending dead unchanged on the year with 10 year Treasuries showing a 3.0% yield. Improving US growth prospects is the reason.

In my New Year forecast (click here for my ?2014 Annual Asset Review?) I expected bonds to be weak, but not fall below a 3.50% yield. I was in a small minority of strategists who called for such a small decline in Treasuries. If I am right, and yields retrace to 3.0%, I will only be 50 basis points off my target, which is better than most.

But that is not to say that 10-year yields won?t first spike to 2.25% first, which happens to be Gundlach?s personal target.

I am a guy who puts his money where his mouth is, who eats his own cooking, and wears his opinions on his sleeve. So, I have been shorting bonds for all of this year.

But my trading approach is so forgiving, using price spikes to buy out of the money-put-spreads, that my followers have had more than adequate room to get profitably in and out.

Every single trade was either a winner, or broke even, except for one, adding an eye popping 10.61% to my 28% profit for 2014. It has been my most profitable trade this year.

While I have been dead wrong with the trend, I have been erring so slowly that we were able to coin it almost every month. Such is the forgiveness of the options spread strategy.

Physicists like ?unified theories? that explain everything, be they the movement of single electrons around nuclei, or galaxies in the universe. Here is a nice unified theory of everything for your investments: technology is curing all.

Hyper accelerating technology means that the price of things is falling faster than anyone believes. That means inflation stays at bay forever, which is great for bonds.

Technology is also reducing the cost, and even the need for labor by business. That is also disinflationary, and helps generate ever rising corporate profits, which is wonderful for stocks.

It all sounds like a ?buy stocks and bonds? explanation to me.

It reinforces the ?Golden Age? scenario for the 2020?s that I have been harping about all year, when the last impediment for growth, demographics, shifts from a headwind to a tailwind. That is when risk assets really go ballistic.

Maybe Google?s Ray Kurzweil is right? (click here for ?Peeking into the Future with Ray Kurzweil).

https://www.madhedgefundtrader.com/wp-content/uploads/2014/08/Wrong-Right-Sign.jpg351355Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-08-15 08:48:432014-08-15 08:48:43Bonds or Stocks: Who?s Right?

I can tell you exactly how the crisis in the Ukraine is going to play out. This has major implications for the global economy, financial markets and your personal portfolio, so listen up!

The key to deciphering this puzzle is oil, far and away Russia?s largest export. At 10 million barrels a day, the country is taking in $360 billion a year in revenues from oil shipments.

You can analyze Russia all day long, and come up with bullish arguments for the country, like the emerging middle class, its huge hoard of basic commodities, and substantial wheat exports. But Texas tea (Russian tea?) overwhelms everything else in its impact on the national accounts.

The bottom line is that Russia is basically a call option on oil. This is why I never buy the Market Vectors ETF Trust (RSX). Look at the charts below for oil, and it is clear that it almost trades tick for tick with the (RSX).

If I?m bullish on oil, I go straight to the end commodity, and not the intermediary, where price earnings multiples are permanently low, corruption is rampant and the rule of law is absent.

And therein lies the problem for Vladimir Putin.

Any chink in the global growth picture flows straight into the price of oil. Slower growth brings lower oil prices and therefore smaller incomes for the Russians. And guess who the principal threat to global growth is? Vladimir Putin and his attempt to take over the Ukraine by force.

So far, crude has dropped by 10% from the May peak of $107.60. That may not sound like a lot. But this is not your father?s Russian oil industry.

Back in the old days, when my friend, Occidental Petroleum?s (OXY) Dr. Armand Hammer and Fred Koch were the only Americans running around the Caucasus, oil there was incredibly cheap. There, technology was 50 years old and labor was virtually free. Slave labor is great for profit margins. If you don?t believe me, just ask Wal-Mart (WMT) and Apple (AAPL).

The fall of the Berlin Wall and the end of the Soviet Union brought many far-reaching, unintended consequences. A big one is that Russia?s dependence on international trade grew tremendously. The country was also able to modernize its oil industry with extensive American assistance.

Russian oil production exploded, as did the cost of production. In my lifetime, expenses have soared from $5 to $70 a barrel. So when oil dips by 10% on the international markets, Russian incomes plunge by 25%. The Russian oil industry has become a highly leveraged affair.

This is why such relatively minor price declines brought apparently desperate actions by the Russian authorities to prop up the economy. They have imposed a 3% emergency VAT, or sales tax. While I was in Europe, four Russian tour companies were driven into bankruptcy by the banking sanctions, stranding some 10,000 tourists on Mediterranean beaches.

Now there is a ban on food imports from Europe, stranding thousands of trucks at the Russian borders. Russia doesn?t grow much food, thanks to their horrendous winters and short growing seasons. Essentially, it?s just wheat and potatoes.

Everything else has to be imported. Some of the lost food can be made up with new imports from emerging, non sanctioning economies, but not much. In the meantime, some 350 McDonald?s franchises in Russia are trying to figure out how to make Big Macs purely from domestic supplies. Good luck to that!

The thing that really struck me speaking to Russians in Europe this summer was Putin?s unbelievably high 85% approval rating (our congress is at 14%!). They trotted out the most incredible conspiracy theories which painted them as the injured party. (The Ukraine was trying to assassinate Putin when it shot down Malaysian Air 17, and then blamed it on Russia).

It almost reminded me of home. The Russians are calling their opponents ?fascists.? This is a people who act like WWII ended last week.

Which leads me to believe that Putin?s popularity is peaking. The sanctions coupled with falling oil revenues are starting to have a severe impact on Russian standards of living. It is a matter of time before this feeds into poor election results for Putin. Nationalism is great, but who wants to live on canned food left over from the Soviet Union (yuck!).

Putin knows this. So to head off the riot, he is going to declare victory in the Ukraine fairly soon, and then take his troops home. This will enable the Ukraine to snuff out the separatists and return to an uneasy peace. We might even luck out and get a written treaty.

If that is a case, you can expect global financial markets to rocket. There would me a massive shift of capital out the risk spectrum, out of bonds and into stocks. This would give the green light for my scenario where S&P 500 adds 10% from last week?s low to end of 2014.

Maybe this is what stocks are trying to tell us by refusing to go down more that 5% this summer and the face of a host of geopolitical disasters.

As for the exact timing for all of this, just watch the price of oil. The lower it goes, the sooner we will get a favorable resolution. The charts are hinting that another $5-$10 break to the downside is imminent.

The last Cold War drove the Soviet Union broke and Putin definitely has no interest in repeating the exercise.

Not Until the Sanctions Are Over

https://www.madhedgefundtrader.com/wp-content/uploads/2014/08/McDonalds-Russia.jpg321337Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-08-14 09:32:162014-08-14 09:32:16How the Ukraine Crisis Will Play Out

War threatens in the Ukraine. Iraq is blowing up. Rebels are turning our own, highly advanced weapons against us. Israel invades Gaza. Ebola virus has hit the US. Oh, and two hurricanes are hitting Hawaii for the first time in 22 years.

Should I panic and sell everything I own? Is it time to stockpile canned food, water and ammo? Is the world about to end?

I think not.

In fact the opposite is coming true. The best entry point for risk assets in a year is setting up. If you missed 2014 so far, here is a chance to do it all over again.

It is an old trading nostrum that you should buy when there is blood in the streets. I had a friend who reliably bought every coup d? etat in Thailand during the seventies and eighties, and he made a fortune, retiring to one of the country?s idyllic islands off the coast of Phuket. In fact, I think he bought the whole island.

Now we have blood in multiple streets in multiple places, thankfully, this time, it is not ours.

I had Mad Day Trader, Jim Parker, do some technical work for me. He tracked the S&P 500/30 year Treasury spread for the past 30 years and produced the charts below. This is an indicator of overboughtness of one market compared to another that reliably peaks every decade.

And guess what? It is peaking. This tells you that any mean reversion is about to unleash an onslaught of bond selling and stock buying.

There is a whole raft of other positive things going on. Several good stocks have double bottomed off of ?stupid cheap? levels, like IBM (IBM), Ebay (EBAY), General Motors (GM), Tupperware (TUP), and Yum Brands (YUM). Both the Russian ruble and stock market are bouncing hard today.

There is another fascinating thing happening in the oil markets. This is the first time in history where a new Middle Eastern war caused oil price to collapse instead of skyrocket. This is all a testament to the new American independence in energy.

Hint: this is great news for US stocks.

If you asked me a month ago what would be my dream scenario for the rest of the year, I would have said an 8% correction in August to load the boat for a big yearend rally. Heavens to Betsy and wholly moley, but that appears to be what we are getting.

It puts followers of my Trade Alert service in a particularly strong position. As of today, they are up 24% during 2014 in a market that is down -0.3%. Replay the year again, and that gets followers up 50% or more by the end of December.

Here is my own shopping list of what to buy when we hit the final bottom, which is probably only a few percent away:

Longs

JP Morgan (JPM) Apple (AAPL) Google (GOOG) General Motors (GM) Freeport McMoRan (FCX) Corn (CORN) Russell 2000 (IWM) S&P 500 (SPY)

Shorts

Euro (FXE), (EUO) Yen (FXE), (YCS)

No, Not This Time

https://www.madhedgefundtrader.com/wp-content/uploads/2014/08/Gun-Ammunition-War-Room.jpg280438Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-08-11 01:05:382014-08-11 01:05:38Is the Turnaround at Hand, and Ten Stocks to Buy at the Bottom?

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.