Virtually all of the research you receive are about stocks you should buy. This report is about stocks you should sell….with both hands as fast as you can.

It is perhaps the most important data release of the last several years that no one noticed. As a result, one of the best shorting opportunities in years is rearing its ugly head.

US coal production hit a 41-year low in 2020. Coal as a percentage of US power output has plunged from 28% to 10% over the last decade to only 437 million short tons. Total coal production has plunged by 64% during this time.

The end result will be a massive shift of wealth out of the major coal-producing regions of the US in the east.

If energy has a proverbial buggy whip maker, it is king coal. And while US coal production has been in free fall, alternatives have been rising sharply, especially solar, now accounting for 20% of US energy consumption.

The implications for the US economy are enormous. I used to be kept awake at night by the wailing whistles of Union Pacific (UNP) engines delivering Wyoming coal to California ports for shipment on to China. They have all disappeared.

Those trains are now moving oil south from Canada and North Dakota to the oil distribution hub in Cushing, Oklahoma, or even all the way to Gulf ports, except that this time they are using a North/South rail line like Norfolk Southern (NSC) rather than the East/West running Union Pacific. Clearly, there are consequences.

In recent the last year, the few listed coal names left have enjoyed a nice rally. This is because of the generalized global “RISK ON” move that has unfolded since the pandemic peaked. The Van Eck Vectors Coal ETF was shut down in 2020 for lack of interest.

It also helps that the incoming Biden administration is unlikely to hammer away at China on trade front as did the previous one. China is far and away the world’s largest buyer of coal.

I believe that in the coming years, the entire US coal industry will go bankrupt and get purchased by the Chinese for pennies on the dollar, or for their outstanding debt alone at a big discount. Needless to say, this makes the entire sector a great candidate for a core short.

Coal is hopelessly uncompetitive with natural gas. Burning gas produces a fraction of the carbon dioxide of coal, and alternatives like wind and solar produce none whatsoever. Coal faces onerous environmental regulation, which will almost certainly get worse under a future administration. US utilities are therefore closing coal-fired power plants as fast as they can.

The outgoing administration was the most pro-coal one in American history. Yet, not a single new coal-fired was built during their reign.

However, coal-dependent communities are not about to turn into ghost towns. They have the great advantage of offering some of the lowest operating costs anywhere in the country. Free rent is becoming common. You'd be nuts to start a new business in the San Francisco Bay Area these days, which has become a haven of the wealthy.

Throw in some decent broadband and they can handily join the global economic community. Yes, you can turn coal miners into programmers, at least the young ones. They all grew up playing video games just like the rest of us.

I Don’t See Any Future in This, Do You?

https://www.madhedgefundtrader.com/wp-content/uploads/2019/02/miners.png441358Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-09-28 11:02:522021-09-28 12:31:46The Death of King Coal

What would happen if I recommended a stock that had no profits, was losing $3 trillion a year and had a net worth of negative $44 trillion?

Chances are, you would cancel your subscription to the Mad Hedge Fund Trader, demand a refund, unfriend me from your Facebook account, and delete me from your Twitter network.

Yet, that is precisely what my former colleague at Morgan Stanley did a few years ago, technology guru Mary Meeker.

Now a partner at venture capital giant Kleiner Perkins, Mary has brought her formidable analytical talents to bear on analyzing the United States of America as a stand-alone corporation.

The bottom line: the challenges are so great they would daunt the best turnaround expert. The good news is that our problems are not hopeless or unsolvable.

The US government was a miniscule affair until the Great Depression and WWII when it exploded in size. Since 1965 when Lyndon Johnson’s “Great Society” began, GDP rose 2.7 times, while entitlement spending leaped 11.1 times.

If current trends continue, the Congressional Budget Office says that entitlements and interest payments will exceed all federal revenues by 2025.

Of course, the biggest problem is with healthcare spending, which will see no solution until healthcare costs are somehow capped. Despite spending more than any other nation, we get one of the worst results, with lagging quality of life, life spans, and infant mortality.

Some 28% of Medicare spending is devoted to a recipient’s final four months of life. Somewhere, there are emergency room cardiologists making a fortune off of this. A night in an American hospital costs 500% more than in any other country.

Social Security is an easier fix. Since it started in 1935, life expectancy has risen by 26% to 78, while the retirement age is up only 3% to 66. Any reforms have to involve raising the retirement age to at least 70 and means testing recipients. If you make $1 billion a year, you don’t need a monthly social security check.

The solutions to our other problems are simple but require political suicide for those making the case.

For example, you could eliminate all tax deductions, including those for home mortgage deductions, charitable contributions, IRA contributions, dependents, and medical expenses, and raise $1 trillion a year. That would only make a dent in our current $3 trillion a year budget deficit.

Mary reminds us that government spending on technology laid the foundations of our modern economy. If the old DARPANET had not been funded during the sixties, Google, Yahoo, eBay, Facebook, Cisco, and Oracle would be missing today. Tech generates about 50% of all the profits in the US today.

Global Positioning Systems (GPS) were also invented by and is still run by the government and has been another great wellspring of profits. (I got to use it during the 1980s while flying across Greenland when it was still top secret. The Air Force base that ran it was called “Sob Story”).

There are a few gaping holes in Mary’s “thought experiment”. I doubt she knows that the Treasury Department carries the value of America’s gold reserves, the world’s largest at 8,965 tons worth $832 billion, at only $34 an ounce, versus an actual current market price of $1,861. By the way, the stash has only been seen once in 50 years.

Nor is she aware that our ten aircraft carriers are valued at $1 each, against an actual cost of $10 billion each in today’s dollars. And what is Yosemite worth on the open market, or Yellowstone, or the Grand Canyon? These all render her net worth calculations meaningless.

No, the USA is not a short. In fact, it is a long term scream long. The arguments as to why show up in the Diary of a Mad Hedge Fund Trader every day of the year. During the publishing run of this letter, I have seen the Dow Average soar from 600 to 30,000.

How could I think otherwise?

Mary expounds at length on her analysis, which you can buy in a book entitled USA Inc. at Amazon by clicking here.

Worth More Than a Dollar?

https://www.madhedgefundtrader.com/wp-content/uploads/2020/11/worth-more-than-a-dollar.png372496Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-09-15 11:04:152021-09-15 11:31:37Is USA Inc. a Short?

Sorry for the late letter this morning. I received a call from Cal Fires yesterday asking for a spotter pilot near the Lake Tahoe region.

So, the early AM found me flying a wide circle around the Sierra foothills with a pair of binoculars and a GPS calling in new smoke plumes to Central Command in Sacramento.

When you get near the big fires, the turbulence is incredible and you wonder if the plane can hold together. These are things better observed from a distance.

Thank you, Clyde Cessna for building such great aircraft!

Thankfully, the kids are old enough to drive themselves to school. I gave them $20 for dinner in case I didn’t come back.

Don’t worry about me. I evacuated out of Lake Tahoe weeks ago, as even back then, the smoke was so thick that the air was unbreathable. All of Lake Tahoe has now been evacuated, except for Incline Village at the northern tip.

There are now 70 bulldozers building a giant fire break at South Lake Tahoe. The 25,000 residents have been moved to emergency evacuation centers throughout northern Nevada.

The casinos are all closed but the hotels are open to house firefighting and support teams. Some teams have been lost to Covid. The water bombers are knocking the daylights out of the West Shore.

Welcome to the nightmare scenario. This is a disaster on a biblical scale.

At home, we are watching the TV, amazed at videos of 600-pound bears on fire running out of the mountains.

In the meantime, I have received dozens of emails, phone calls, and text messages from subscribers asking about my safety.

Don’t worry, all is well here out in San Francisco. But thanks for asking!

The View from Incline Village, Nevada

https://www.madhedgefundtrader.com/wp-content/uploads/2021/09/nevada-fires.png368490Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-09-02 09:04:482021-09-02 13:45:47Many Thanks for Your Concerns

I am sitting here holed up in my office in San Francisco.

Lake Tahoe is being evacuated as the Caldor fire is only ten miles away and the winds are blowing towards it. The visibility there is no more than 500 yards. The ski resorts are pointing their snow cannons towards their buildings to ward off flames.

Conditions are not much better here in Fog City. We are under a “stay at home” order due to intense smoke and heat. Even here, the fire engines are patrolling by once an hour.

The Boy Scout trip got cancelled this weekend, so the girls are having a cooking competition, chocolate chip waffles versus a German chocolate cake.

To make matters worse, I have been typing with only one finger all week, thanks to the elbow surgery I had on Tuesday. Next time, I’ll think twice before taking down a 300-pound steer. When I told the doctor how I incurred this injury, he laughed. “At your age?”

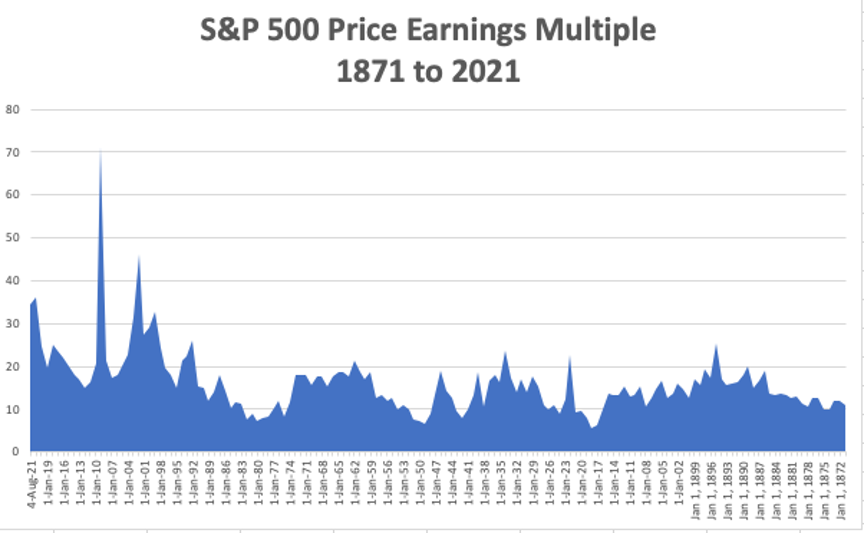

Which leaves me to contemplate this squirrelly stock market of ours. I have always been a numbers guy. But the higher the indexes rise, the cheaper stocks get. That’s not supposed to happen, but that is the fact.

We started out 2021 with an S&P 500 price earnings multiple of 25X. Now, we are down to a lowly 21X and the (SPY) is 20% higher, rising from $360 to $450.25.

The analyst community, ever the lagging indicator that they are, had S&P forward earnings for 2022 all the way down to $175. They have been steadily climbing ever since and are now touching $200 a share.

This is what 20/20 hindsight gets you. That and $5 will get you a cup of coffee at Starbucks. It takes a madman like me to go out on a limb with high numbers and then be right.

So what follows an ever-cheaper market? A more expensive one. That means stocks will continue to my set-in-stone target of $475 for the (SPY) for yearend, and (SPY) earnings of over $200 per share.

It gets better.

(SPY) earnings should hit $300 a share by 2025 and $1,400 a share by 2030. That makes possible my (SPY) target of $1,800 and my Dow Average target of 240,000 in a decade.

What are markets getting right that analysts and bears are getting wrong?

The future has arrived.

The pandemic brought forward business models and profitability by a decade. Technology is hyper-accelerating on all fronts.

Cycles are temporary but adoption is permanent. We are never going back to the old pre-pandemic economy. As a result, stocks are now worth a lot more than they were only two years ago.

So what do we buy now? There is a second reopening trade at hand, the post-delta kind. That means buying banks (JPM), (BAC), (C), brokers (GS), (MS), money managers (BLK), commodities (FCX), (X), hotels (WYNN), (MGM), airlines (ALK), (LUV), and energy (HAL), (SLB).

And what do we avoid like the plague? Bonds (TLT), which offer only confiscatory yields in the face of rising inflation with gigantic negative interest rates.

As for technology stocks, they will go sideways to up small in the aftermath of their ballistic moves of the past three months.

You all know that I am a history buff and there are particular periods of history that are starting to disturb me.

In August, we saw ten new intraday highs for the S&P 500 (SPY). That has not happened since 1987. Remember what happened in 1987?

We have not seen 11 new highs in August since 1929. The only negative three months seen since 1929 are August, September, and October. Remember what happened in 1929?

If that doesn’t scare the living daylights out of you, then nothing will. So, it seems we are in for some kind of correction, even if it’s just the 5% kind.

As for me, I’m looking forward to 2030.

The “Everything” Rally is on, according to my friend, Strategas founder Tom Lee. You can see it in the recent strength of epicenter stocks like energy, hotels, airlines, and casinos. It could run into 2022.

The Taper is this year and interest rate rises are later, said Jay Powell at Jackson Hole last week. Markets will be jumpy, especially bonds. Fed governor Jay Powell’s every word was parsed for meaning. Dove all the way. The larger focus will be on the August Nonfarm Payroll report out this week. Pfizer Covid vaccination gets full FDA approval, requiring millions more to get shots and bringing forward the end of the pandemic. All 5 million government employees will now get vaccinated, including the entire military. It’s the fastest drug approval in history. Some 37,000 new cases in one day. The stock market likes it. Take profits on (PFE) Bitcoin tops $50,000 after breaking several key technical levels to the upside. Next stop is a double top at $66,000. It helps that Coinbase is buying $500 million worth of crypto for its own portfolio. Buy (COIN) on dips. The US Dollar will crash in coming years, says Jeffry Gundlach and I think he is right. Emerging markets will become the next big play but not quite yet. Gold (GLD) will be a great hideout once it comes out of hibernation. China will soon return to outperforming the US. The dollars reserve currency status is at risk. The lumber crash is saving $40,000 per home, says Toll Brothers (TOL) CEO, Doug Yearly. Last year, lumber prices surged from $300 per board foot to an insane $1,700, thanks to a Trump trade war with Canada and soaring demand. It all flows straight through the bottom line of the homebuilders which should rally from here. Buy (TOL) on dips. China’s crackdown creates investment opportunities, says emerging investing legend Mark Mobius. He sees corporate governance improving over the long term. The gems are to be found among smaller companies not affected by Beijing’s hard-line. Mobius loves India too. My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

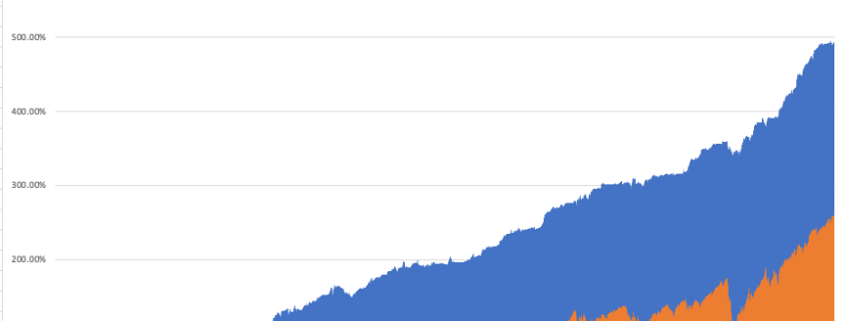

My Mad Hedge Global Trading Dispatch saw a healthy +7.62% gain in August. My 2021 year-to-date performance appreciated to 76.83%. The Dow Average was up 15.87% so far in 2021.

That leaves me 80% in cash at 20% in short (TLT) and long (SPY). I’m keeping positions small as long as we are at extreme overbought conditions.

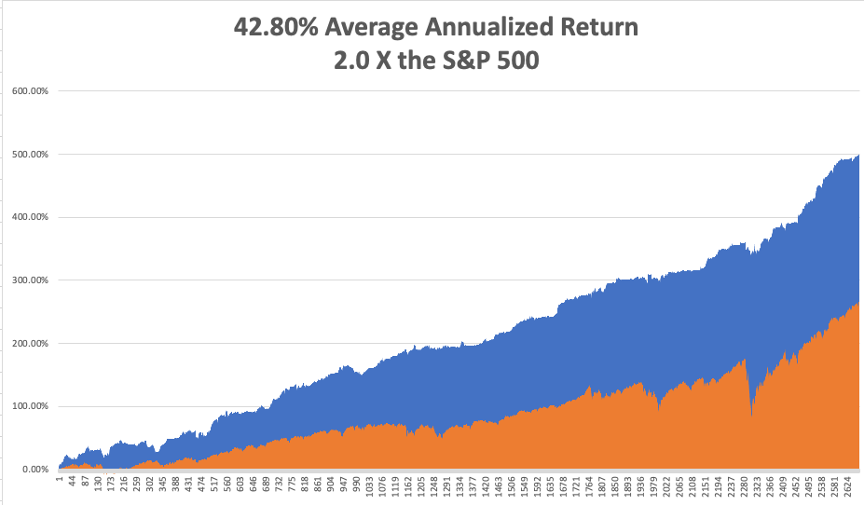

That brings my 12-year total return to 499.38%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return now stands at an unbelievable 42.80%, easily the highest in the industry.

My trailing one-year return popped back to positively eye-popping 116.67%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 39 million and rising quickly and deaths topping 638,000, which you can find here.

The coming week will bring our monthly blockbuster jobs reports on the data front.

On Monday, August 30 at 11:00 AM, Pending Home Sales are published. Zoom (ZM) reports.

On Tuesday, August 31, at 10:00 AM, S&P Case Shiller National Home Price Index for June is released. CrowdStrike (CRWD) reports.

On Wednesday, September 1 at 10:45 AM, the ADP Private Employment report is disclosed.

On Thursday, September 2 at 8:30 AM, Weekly Jobless Claims are announced. DocuSign (DOCU) reports.

On Friday, September 3 at 8:30 AM, the all-important August Nonfarm Payroll report is printed. At 2:00 PM, the Baker Hughes Oil Rig Count is disclosed.

Oh and the German chocolate cake won, but please don’t tell anyone.

As for me, given the losses in Afghanistan this week, I am reminded of my several attempts to get into this troubled country.

During the 1970s, Afghanistan was the place to go for hippies, adventurers, and world travelers, so of course, I made a beeline for straight for it.

It was the poorest country in the world, their only exports being heroin and the blue semiprecious stone lapis lazuli, and illegal export of lapis carried a death penalty.

Towns like Herat and Kandahar had colonies of westerners who spent their days high on hash and living life in the 14th century. The one cultural goal was to visit the giant 6th century stone Buddhas of Bamiyan 80 miles northwest of Kabul.

I made it as far as New Delhi in 1976 and was booked on the bus for Islamabad and Kabul ($25 one-way). Before I could leave, I was hit with amoebic dysentery.

Instead of Afghanistan, I flew to Sydney, Australia where I had friends and knew Medicare would take care of me for free. I spent two months in the Royal North Shore Hospital where I dropped 50 pounds, ending up at 125 pounds.

I tried to go to Afghanistan again in 2010 when I had a large number of followers of the Mad Hedge Fund Trader stationed there, thanks to the generous military high-speed broadband. The CIA waved me off, saying I wouldn’t last a day as I was such an obvious target.

So, alas, given the recent regime change, it looks like I’ll never make it to Afghanistan. I won’t live long enough to make it to the next regime change. It’s just one more concession I’ll have to make to my age. I’ll just have to content myself reading A One Thousand and One Nights at home instead. The Taliban blew up the stone Buddhas of Bamiyan in 2001.

In the meantime, I am on call for grief counseling for the Marine Corps for widows and survivors. Business has been thankfully slow for the last several years. But I’ll be staying close to the phone this weekend just in case.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

India in 1976

https://www.madhedgefundtrader.com/wp-content/uploads/2021/08/john-thomas-india.png576864Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-08-30 09:02:562021-08-30 10:27:35The Market Outlook for the Week Ahead, or The Higher We Go the Cheaper We Get

Below please find subscribers’ Q&A for the August 25 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from The Atlantis Casino Hotel in Reno, NV.

Q: How does a 2X ProShares Ultra Technology ETF (ROM) February 2022 vertical bull call spread on the ROM look? Would you do $110-$115 or $115-$120?

A: I would do nothing here at $112.50 because we’ve just gone up 10 points in a week. I’d wait for some kind of pullback, even just $5 or $10 points, and then I would do the $110-$115. I’m leaning towards more conservative LEAPS these days—bets that the market goes sideways to up small rather than going ballistic, which it has done for the last 18 months. Think at-the-money strikes, not deep out-of-the-money on your LEAPS from here on for the rest of this economic cycle. The potential profits are still enormous. The only problem with (ROM) is that the longest maturities on the options are only six months.

Q: How do you recommend entering your long-term portfolio?

A: I would use the one-third rule: you put on ⅓ now, ⅓ higher or lower later on, and ⅓ higher or lower again. That way you get a good average price. Long term, everything goes up until we hit the next recession, which is probably several years off.

Q: I keep reading that the Delta variant is a market risk, but I don’t think that investors will look through this. Is Delta already priced into the shares?

A: Yes, what is not priced into the shares is the end of Delta, the end of the pandemic—and that will lead to my “everything” rally that I’ve been talking about for a month now. And we have already seen the beginning of that, especially with the price action this week. So yes, Delta in: dead market; Delta out: roaring market.

Q: Do you think there will eventually be a rotation into emerging markets (EEM), or has the virus battered these markets too much to even consider it?

A: Sometime in our future—not yet—the emerging markets will be our core holding. And the trigger for that will be the collapse of the dollar, which is hitting an interim high right now. When the greenback rolls over and dies, you can expect emerging markets, especially China, to take off like a rocket. That’s going to be our next big trade. I don't know if it will be this year or next year but it’s coming, so start doing your emerging market research now, and keep reading my newsletter.

Q: Is the coming tax hike a problem for the stock market?

A: No, I don’t think so. First off, I don’t think they’re going to do a tax bill this year; they don’t want anything to interfere with the 2022 election, so it may be next year’s business. Also, any new taxes are going to be overwhelmingly focused on billionaires, carried interest, offshoring, and large corporations. The middle class, people who make less than $400,000 a year, will not see any tax hike at all, possibly even getting some tax cuts via restored SALT deductions. So, I don't really see it affecting the stock market at all.

Q: What do you think about Chinese stocks (FXI)?

A: Long-term they’re okay, short term possibly more downside. Interestingly, the bigger risk may not be China itself and how the government is beating up its own tech companies, but the SEC. It has indicated they don’t really like these offshore vehicles that have been listed on the New York Stock Exchange, and they may move to ban them. I’m not rushing into China right now, only because there are just so many better opportunities in the US stock market for the time being. I may go back in the future—it’s a case where I’d rather buy them on the way up than trying to catch a falling knife on China right now.

Q: Do you expect any market impact from the Jackson Hole meeting?

A: Yes, whatever J Powell says, even if he says nothing, will have a market impact. And it will have a bigger impact on the bond market than it will on the stock market, which is down a full point this morning. So yes, but not yet. I imagine we’ll hear something very soon.

Q: September and October tend to be volatile; do you see us having a 5% or 10% pullback in those months?

A: I don’t see any more than 5%, with the hyper liquidity that we have in the system now. There just aren’t any events out there that could trigger a pullback of 10%—no geopolitical events, and the economy will be getting stronger, not worse. So yes, an “everything rally” doesn’t give you many long side entry points, so I just don’t see 10% happening.

Q: What about a Walt Disney (DIS) January 2022 $180-$220 LEAPS?

A: I would do the $180-$200. I think you can afford to be tighter on your spread there, take some more risk because I think it’s just going to go nuts to the upside once we get a drop in COVID cases. By the way, Disney parks are only operating at 70% capacity, so if you go back up to 100% that's a near 50% increase in profits for the company. And it’s not just Disney, but Netflix (NFLX), Amazon (AMZN), and everybody else that’s about to have the greatest number of blockbuster movies released of all time. They’re holding back their big-ticket movies for the end of the pandemic when people can go back into theaters. We’ll start seeing those movies come out in the last quarter of this year, and I’m particularly looking forward to the next James Bond movie, a man after my own heart.

Q: Are EV car charging companies like ChargePoint Holdings (CHPT) going to do as well as the car companies?

A: No. They’re low margin business, so it’s not a business model for me. I like high-profit margins, huge barriers to entry, and very wide moats, which pretty much characterizes everything I own. The big profits in EVs are going to be in the cars themselves. Charging the cars is a very capital-intensive, highly regulated, and low-margin business.

Q: Would a Fed taper cause a 10% pullback?

A: Absolutely not; in fact, I think a taper would make the market go up because Jay Powell has been talking it into the market all year. And that’s his goal, is to minimize the impact of a taper so when they finally do it, they say ho-hum and “okay you can take that risk out of the market.” That’s the way these things work.

Q: What is your yearend target for United States Treasury Bond Fund (TLT)?

A: $132. Call it bold, but I'm all about bold. I think the first stop will be at $144, then $138, then bombs away!

Q: What will it take for (TLT) to dip below $130?

A: Another year of hot economic growth, which Congress seems hell-bent on delivering us.

Q: What are your ProShares Ultra Short 20+ Year Treasury ETF (TBT) targets?

A: When we were at 1.76% on the 10-year bond, the (TBT) made it all the way back to 22 ½. Next year we go higher, probably to $25, maybe even $30.

Q: What’s your 10-year view on the (TBT)?

A: $200. That’s when you get interest rates back to 10% in 10 years on the 10-year bond. So yes, that’s a great long-term play.

Q: How long can we hold (TBT)?

A: As long as you want. Ten years would be a good time frame if you want to catch that $17 to $200 move. The (TBT) is an ETF, not an option, therefore it doesn’t expire.

Q: Are you working on an electrification stock list?

A: I am not, because it’s such a fragmented sector. It’s tough to really nail down specific stocks. I think it’s safe to say that the electric power grid is going to change beyond all recognition, but they won’t necessarily be in high margin companies, and I tend to prefer high-profit-margin, large-moat companies which nobody else can get into, like Apple (AAPL) or Google (GOOG).

Q: What about gas pipelines with high yields?

A: They have a high yield for a reason; because they’re very high risk. If you're going to a carbon-free economy, you don’t necessarily want to own pipelines whose main job is moving carbon; it’s another buggy whip-type industry I would avoid. I’ve seen people get wiped out by these things more times than I could count. If you remember Master Limited Partnerships, quite a few of them went bankrupt last year with the oil crash, so I would avoid that area. These tend to be very highly leveraged and poorly managed instruments.

Q: Best play on silver (SLV)?

A: Wheaton Precious Metals (WPM) is the highest leveraged silver play out there, and a great LEAPS candidate. Go out 2 years and triple your money.

Q: Geopolitical oil (USO) risks?

A: No, nobody cares about oil anymore—that’s why we’re giving up on Afghanistan. China is buying 80% of the Persian Gulf oil right now. We don’t really need it at all, so why have our military over there to protect China’s oil supply?

Q: What about Freeport McMoRan (FCX)?

A: I absolutely love it. Any big economic recovery can’t happen without copper, and you have a huge tailwind there from electric cars which need 200 pounds of copper each, as opposed to 20 pounds in conventional cars.

Q: I see AMC Entertainment Holdings (AMC) is up 20% today; should everyone be chasing this stock?

A: No, absolutely not. (AMC) and all the meme stocks aren’t investments, they’re gambling, and there are better ways to gamble.

Q: Should I buy the lumber dip?

A: Yes. I think the slowdown on housing is temporary because it will take 10 years for supply and demand in the housing market to come back into balance because of all the millennials entering the housing market for the first time. So, that would be a yes on lumber and all the other commodities out there that go into housing like copper, steel, and aluminum.

Q: Should I put money into Canadian Junior Gold Miners (GDX)?

A: No, I would rather go out and take a long nap first. These are just so high risk, and they often go bankrupt. The liquidity is terrible, and the dealing spreads are wide. I would stick with the bigger precious metal plays like Newmont Mining (NEM), Barrick Gold (GOLD), and Wheaton Precious Metals (WPM).

Q: Is Boeing (BA) a buy here?

A: Yes, we’re back at the bottom end of the trading range for the stock. It’s just a matter of time before they get things right, and the 737 Max orders are rolling in like crazy now that there’s an airplane shortage.

Q: What do you think about Robinhood (HOOD)?

A: I like it quite a lot; I got flushed out of my long position on Friday with a 10% down move. Of course, 90% of my stop losses end up expiring at their maximum profit points, but I have to do it to keep the volatility of the portfolio down. So yes, I’ll try to buy it again on the next dip. The trouble is it’s kind of a quasi-meme stock in its own right, hence the volatility; so I would say on the next 10% down day, you go into Robinhood, and I probably will too.

Q: How are the wildfires around Tahoe?

A: They’re terrible and there are three of them. I did a hike two days ago there, and out of a parking lot with 100 spaces, I was the only one there. It’s the only time I’d ever seen Tahoe deserted in August. With visibility of 500 yards, it's just terrible. Fortunately, I was able to hike without coughing my guts out—it’s not so thick that you can’t breathe.

Q: What do you think of US Steel (X)?

A: I like it, I think the whole industrial commodity complex rallies like crazy going into the end of the year.

Q: As a new member, where is the best place to start? It’s just kind of like drinking from a fire hose.

A: Wait for the trade alerts; they only happen at sweet spots and you may have to wait a few days or weeks to get one since we only like to enter them at good points. That’s the best place to enter new positions for the first time. In the meantime, keep reading all the research, because when these trade alerts do come out, they’re not surprises because I’m pumping out research on them every day, across multiple fronts. Be patient— we are running a 93% success rate, but only because we take our time on entering good trades. The services that guarantee a trade alert every day lose money hand over fist.

Q: If they do delist Chinese stocks, will US investors be left holding the bag?

A: Yes, and that will be the only reason they don’t delist them, that they don’t want to wipe out all current US investors.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH or TECHNOLOGY LETTER (whichever applies to you), then select WEBINARS and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2021/08/john-thomas-wine-1.png812562Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-08-27 10:02:412021-08-27 11:03:48August 25 Biweekly Strategy Webinar Q&A

Gophers have lately been eating my rose bushes. So I bought some special humane catch and release traps imported from France. Using peanut butter and almonds as bait, what did I catch the first night?

A skunk.

Guess who has skunk removal duty in this family? That would be me.

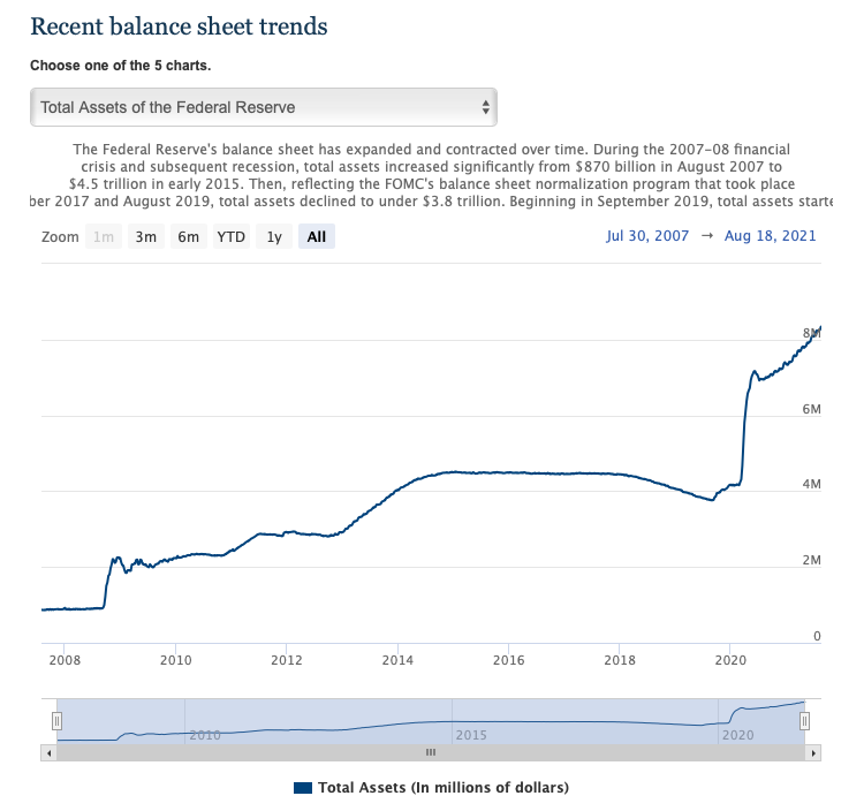

The Federal Reserve has some skunk duty of its own in the near future. For the time to take the punch bowl away is rapidly approaching.

A majority of Fed presidents now believe that continuing $40 billion a month worth of mortgage bond purchases while there are nationwide bidding wars going on in the housing market is nuts. So a taper is coming most likely in September if we get another hot jobs report.

The last time the Fed tapered, way back in 2013, the stock market dropped 5%. Remember the “taper tantrum”? It then realized the error of its ways and resumed stimulus. So, the worst we can expect is a 5% correction in the fall. And by the way, the market technicals have been screaming for a correction.

It will just be another buying opportunity. The wall of money is still getting higher, even with a Fed pullback. US corporate profits are likely to soar from $1.9 trillion in 2020 to over $10 trillion in 2021. More than $1 trillion of this is being poured straight back into share buybacks by the healthiest companies.

So the first round of taper, some $480 billion annualized, pales by comparison to the enormous profits and wealth being created right now.

And the Fed isn’t about to end QE, just tone it down. There isn’t a hint of actually withdrawing liquidity from the system, just slowing the rate of increase. It’s why there is active discussion of reappointing Jay Powell for a second term as Fed governor, the greatest QE king of all time. That alone would be worth a thousand-point rally in the Dow.

It is truly amazing how much liquidity has entered the system since the Great Recession. Since 2008, the Fed balance sheet has exploded from $400 billion to $8.9 trillion. It has created this staggering amount of money while keeping interest rates near zero.

During this time, the Dow has risen 59X from 600 to 35,500. All of the new money created is still in the system. The only thing it can buy is stocks, homes, and commodities.

And the best is yet to come!

It’s looking like the delta variant will cost the US about 3% in GDP growth this year. But that growth isn’t lost, just deferred into 2022. That keeps the party rolling on, with or without a punch bowl.

Fed Minutes show a Taper is in the Works, almost certainly cutting monthly bond purchases before yearend, but the delta variant is stretching it out. The (TLT) was rallied on the news and interest rates dropped. Short term rates to remain glued to zero. Asset inflation continues.

Equity Mutual Funds see third week of inflows, some $2.67 billion. Blockbuster Q2 earnings were a major driver where 73% of firms beat forecasts. Q3 looks just as good. Financial sector funds saw the greatest gain, one of the few places where investors can still find value.

Bitcoin market recovers $2 trillion value, with the weekend rally to $48,142, a three-month high. The break above the 200-day moving average is proving big.

Delta continues to take its toll, with new cases topping 130,000, half the January 20 peak, and deaths at 1,500. When it peaks in a few weeks, it will present one of the best buying opportunities of the year for stocks. The “end of delta” rally is coming. The US should top the 625,000 fatalities we saw during the 1919 Spanish Flu in the coming week.

Share Buy Back companies are beating the market. Shrinking the float has always been a big winner for the share prices and the senior management who are paid in stock options. This year, they have the money to do so with massive earnings increases. Goldman Sachs (GS) has put together a portfolio of the biggest buy-back companies and it is handily outperforming the index. What is the number one holding by a large market? Apple (AAPL), which has $250 billion in cash.

Homebuilder Sentiment dives, down 5 points to 75, as high prices cure high prices. Anything above 50 is still positive, but this is the lowest reading since last year. Materials and labor shortages are still a big problem. Nobody can get windows.

July Retail Sales disappoints, down 1.1%, delivering a 300-point hit for stocks. Tech is leading the downturn and Bitcoin took a hit. Clearly, delta is inciting a new “stay at home” movement, at least for the short term.

Housing Starts hit three -month low, down 7% in July to 1.53 million units. Materials and labor shortages are the issue.

Robinhood reports a Q2 loss of $2.16 a share, or $502 million. Revenues came in at $565 million, up over 131%, making it the fastest-growing broker on Wall Street. Shares were down small on the news. Some 60% of account owners are trading in crypto. Buy (HOOD) on dips. My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

My Mad Hedge Global Trading Dispatch saw a modest +6.05% in August. My 2021 year-to-date performance appreciated to 75.26%. The Dow Average was up 14.77% so far in 2021.

This was an options expiration week, running five positions in (TLT), (JPM), (GS), and (V) into max profit. I stopped out of a long in (HOOD) close to cost.

That leaves me 80% in cash at 20% in short (TLT) and long (SPY). I’m keeping positions small as long as we are at extreme overbought conditions.

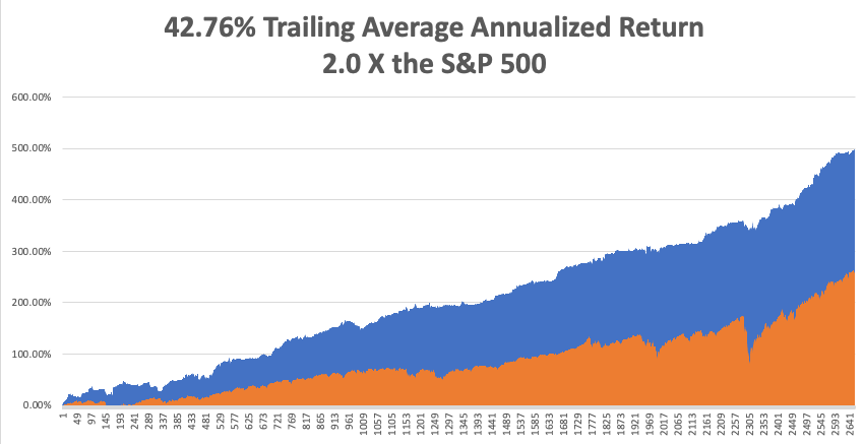

That brings my 12-year total return to 497.81%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return now stands at an unbelievable 42.76%, easily the highest in the industry.

My trailing one-year return popped back to positively eye-popping 113.21%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 37 million and rising quickly and deaths topping 628,000, which you can find

The coming week will bring our monthly blockbuster jobs reports on the data front.

On Monday, August 23 at 11:00 AM, the Existing Home Sales for July are out. Palo Alto Networks (PANW) reports.

On Tuesday, August 24, at 11:00 AM, New Home Sales for July are published. Toll Brothers (TOL) reports. On Wednesday, August 25 at 8:30 AM, the July Durable Goods get printed. Snowflake (SNOW) reports.

On Thursday, August 26 at 8:30 AM, Weekly Jobless Claims are announced. We also get the second estimate of US Q2 GDP. Dell Computers (DELL) reports.

On Friday, August 27 at 8:30 AM US Personal Income & Spending are disclosed. At 2:00 PM, the Baker Hughes Oil Rig Count are disclosed.

And how did I deal with my captive skunk? I gingerly approached the cage with a large garbage bag and threw it over. Then I wrapped the entire cage up and threw it in the back of the car (not the Tesla). I then drove down the mountain, pulled over to the side of the road, opened the gate to the trap, and ran like hell. One angry skunk took off up the hill.

As for me, while in New York a few years ago waiting to board Cunard’s Queen Mary II to sail for Southampton, England, I decided to check out the Bay Ridge address near the Verrazano Bridge where my father grew up.

At the outbreak of WWI, my Italian-born grandfather volunteered for the army as a ploy to gain US citizenship. He was mustard gassed and was completely blinded for two years, living in a veteran’s hospital, a relic from the Civil War.

In 1923, 5% of his vision came back in one eye, so US citizenship in hand, he used his veteran’s benefits to buy a home on 76th street in Bay Ridge, then a middle-class Italian neighborhood.

I took a limo over to Brooklyn and knocked on the front door. I told the driver to keep the engine running.

The owner was expecting a plumber, so he let me right in, despite the fact that I was wearing my pre-boarding attire of a Brioni double-breasted blue blazer and Gucci shoes. I told him about my family history with the property, but I could see from the expression on his face that he didn’t believe a single word.

Then I told him about the relatives moving into the basement during the Great Depression. Grandpa never bought a stock in his life and thought the stock market was a Ponzi scheme. After the 1929 crash, several relatives lost their homes and moved into grandpa’s basement as a last resort.

He immediately offered me a tour of the house. He told me that he had just purchased the home and had extensively remodeled it. When they tore out the basement balls, he discovered that the insulation was composed of crumpled-up Brooklyn newspapers from the 1930s, so he knew I was telling the truth.

When the Japanese attacked Pearl Harbor on December 7, 1941, dad went straight down to Times Square and volunteered for the US Marine Corps. He was given a few days to settle his affairs and then the family didn’t see him for four years.

Before he left, dad wrapped up the engine parts of a 1928 Ford Model A with old newspapers which he had bought from a junkyard and was rebuilding. There they sat in cardboard boxes until 1945.

At the end of my tour, I was shown the brick garage where those cardboard boxes sat. Grandpa received a telegram indicating the day dad would return from San Francisco by train. He warned everyone not to cry. The second dad stepped into the house, some 40 pounds lighter, it was grandpa himself who started bawling.

I told the owner that grandpa would be glad that the house was still in Italian hands. Could I inquire what he had paid for the house that sold in 1923 for $3,000? He said he bought it as a broken-down fixer-upper for a mere $1.5 million and had put another $300,000 in it.

As I passed under the Verrazano Bridge on the Queen Mary II later that day in the two-floor Owner’s Suite, I contemplated how much smarter grandpa became the older I got.

I hope the same is true with my kids.

Grandpa in 1966

76th Street in 1930

1928 Ford Model A

Queen Mary II Sailing Under the Verrazano Bridge Past Bay Ridge

https://www.madhedgefundtrader.com/wp-content/uploads/2021/08/1928-ford.png576864Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-08-23 09:02:132021-08-23 14:22:26The Market Outlook for the Week Ahead, or Doing Skunk Duty

I am really happy with the performance of the Mad Hedge Long Term Portfolio since the last update on February 2, 2021. In fact, not only did we nail the best sectors to go heavily overweight, we also completely dodged the bullets in the worst-performing ones.

For new subscribers, the Mad Hedge Long Term Portfolio is a “buy and forget” portfolio of stocks and ETFs. If trading is not your thing and you don’t want to remain glued to a screen all day, these are the investments you can make. Then don’t touch them until you start drawing down your retirement funds at age 72.

For some of you, that is not for another 50 years. For others, it was yesterday.

There is only one thing you need to do now and that is to rebalance. Buy or sell what you need to reweight every position to its appropriate 5% or 10% weighting. Rebalancing is one of the only free lunches out there and always adds performance over time. You should follow the rules assiduously.

Despite the seismic changes that have taken place in the global economy over the past nine months, I only need to make minor changes to the portfolio, which I have highlighted in red on the spreadsheet.

To download the entire new portfolio in an excel spreadsheet, please go to www.madhedgefundtrader.com, log in, go “My Account”, then “Global Trading Dispatch”, the click on the “Long Term Portfolio” button, then “Download.”

Changes

Biotech

Pfizer (PFE) has nearly doubled in six months, while Crisper Therapeutics (CRSP) has almost halved. Since the pandemic, which Pfizer made fortunes on, is peaking and we are still at the dawn of the CRISPR gene editing revolution, the natural switch here is to take profits in (PFE) and double up on (CRSP).

Technology

I am maintaining my 20% in technology which are all close to all-time highs. I believe that Apple (AAPL), (Amazon (AMZN), Google (GOOGL), and Square (SQ) have a double or more over the next three years, so I am keeping all of them.

Banks

I am also keeping my weighting in banks at 20%. Interest rates are imminently going to rise, with a Fed taper just over the horizon, setting up a perfect storm in favor of bank earnings. Loan default rates are falling. Banks are overcapitalized, thanks to Dodd-Frank. And because of the trillions in government stimulus loans they are disbursing, they are now the most subsidized sector of the economy. So, keep Morgan Stanley (MS), Goldman Sachs (GS), JP Morgan (JPM), and Bank of America, which will profit enormously from a continuing bull market in stocks. They are also a key part of my” barbell” portfolio.

International

China has been a disaster this year, with Alibaba (BABA) dropping by half, while emerging markets (EEM) have gone nowhere. I am keeping my positions because it makes no sense to sell down here. There is a limit to how much the Middle Kingdom will destroy its technology crown jewels. Emerging markets are a call option on a global synchronized recovery which will take place next year.

Bonds

Along the same vein, I am keeping 10% of my portfolio in a short position in the United States Treasury Bond Fund (TLT) as I think bonds are about to go to hell in a handbasket. I rant on this sector on an almost daily basis so go read Global Trading Dispatch. Eventually, massive over-issuance of bonds by the US government will destroy this entire sector.

Foreign Exchange

I am also keeping my foreign currency exposure unchanged, maintaining a double long in the Australian dollar (FXA). Eventually, the US dollar will become toast and could be your next decade-long trade. The Aussie will be the best performing currency against the US dollar.

Australia will be a leveraged beneficiary of the synchronized global economic recovery through strong commodity prices which have already started to rise, and the post-pandemic return of Chinese tourism and investment. I argue that the Aussie will eventually make it to parity with the US dollar, or 1:1.

Precious Metals

As for precious metals, I’m keeping my 0% holding in gold (GLD). From here, it is having trouble keeping up with other alternative assets, like Bitcoin, and there are better fish to fry.

I am keeping a 5% weighting in the higher beta and more volatile iShares Silver Trust (SLV), which has far wider industrial uses in solar panels and electric vehicles. The arithmetic is simple. EV production will rocket from 700,000 in 2020 to 25 million in 2030 and each one needs two ounces of silver.

Energy

As for energy, I will keep my weighting at zero. Never confuse “gone down a lot” with “cheap”. I think the bankruptcies have only just started and will stretch on for a decade. Thanks to hyper-accelerating technology, the adoption of electric cars, and less movement overall in the new economy, energy is about to become free. You are looking at the next buggy whip industry.

The Economy

My ten-year assumption for the US and the global economy remains the same. I’m looking at 3%-5% a year growth for the next decade after this year’s superheated 7% performance.

When we come out the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 700% or more from 35,000 to 240,000 in the coming decade. The American coming out the other side of the pandemic will be far more efficient, productive, and profitable than the old.

You won’t believe what’s coming your way!

I hope you find this useful and I’ll be sending out another update in six months so you can rebalance once again. If I forget, please remind me.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-08-19 10:02:182021-08-19 12:09:09My Newly Updated Long-Term Portfolio

With the Volatility Index (VIX) going through the roof today, I think it is timely to remind everyone what it is.

At my advanced age, I have very few friends. Most of them are either puttering around some county golf course, or are dead.

By there is one who has stuck with me for my entire 50-year trading career, through thick and thin.

That would be Leonardo Fibonacci.

It always seemed like he could read my mind, as well as everyone else’s.

When a stock looks like it fell into a bottomless pit, it would bounce hard off of the precise price that he selected.

Similarly, he always knew high prices would rise before they topped out.

As a result, I think of Fibonacci as more of a magician than a mathematician.

I remember the 12th century like it was yesterday.

In those days, the leading intellectuals used to get together and drink wine by the gallon, which then was really little more than rotten grape juice.

The problem was that we all used to pass out before anybody came up with a great idea.

Then someone started importing coffee from the Middle East, and thinkers stayed awake long enough to produce great thoughts.

Enter the Renaissance.

One of the guys I used to hang out with then was named Leonardo Fibonacci.

Good old Leo was a man after my own heart, a world-class nerd and geek, with a penchant for mathematics.

His dad was a diplomat from the Court at Pisa to the Algiers sultanate who had a nice little import/export business on the side.

It is safe to say that there was probably as little action in Algiers than as there is today. I know, because I’ve been there.

Instead of camping out in his dad’s basement and staying depressed like a lot of young men these days, Leo killed time trolling the local bazaars for interesting used books he could buy on the cheap.

Remember, this was before texting.

That was not hard to do since most people couldn’t read. He took the trouble to learn Arabic and translated them back into Latin. Ancient math books were his specialty.

It didn’t take Leo long to figure out that the Arabs had developed a numbering system vastly superior to the Roman numerals then in use in Europe.

Most importantly, they mastered the concept of zero and the placement of digits in addition and subtraction. The Arabs themselves, in fact, lifted these concepts from archaic Indian mathematicians as far back as the 6thcentury.

If you don’t believe me about the significance of this discovery, try multiplying CCVII by XXXIV. (The answer is VIIXXXVIII, or 7,038).

Good luck designing a house, a bridge, or a computer software program with such a cumbersome numbering system.

Leo didn’t just stop there.

He also discovered a series of numbers, which seemed to have magical predictive powers. The formula is extremely simple. Start with zero, add the next number, and you have the next number in the series.

Continue the progression and you get 0,1,1,2,3,5,8,13,21,34,55…. and so on. It’s no surprise that the sequence became known as the “Fibonacci Sequence”.

The great thing about this series is that if you divide any number in it by the next one, you get a product that has become known as the “Golden Ratio”. This number is 1:1.618, or 0.618 to one.

Fibonacci’s original application for this number was to predict the growth rate of a population of breeding rabbits.

Then some other mathematicians started poking around with it. It turns out the Great Pyramid in Egypt was built to the specification of a Fibonacci ratio.

So is the rate of change of the curvature in a seashell, or a human ear. So is the ratio of the length of your arms to your legs.

Upon closer inspection, the Fibonacci formula turned out to be absolutely everywhere, from the structure of the tiniest cell to the swirl of the largest galaxies in the universe.

Fibonacci introduced his findings in a book entitled “Liber Abaci”, or “Free Abacus” in English, which he published in 1202.

In it, he proposed the 0-9 numbering system, place values, lattice multiplication, fractions, bookkeeping, commercial weights and measures, and the calculation of interest.

It included everything we would recognize as modern mathematics.

The book launched the scientific revolution in Europe that led us to where we are today and was a major bestseller. In fact, you can still buy it on Amazon, making it the longest continuously published book in history.

Enter the stock market.

By the end of the 19thcentury, some observers noticed that share prices tended to move in predictable patterns on charts.

In particular, they always seemed to advance and pull back around the numbers forecast by my friend, Fibonacci, seven hundred years earlier.

These people came to be known as “technical analysts,” as opposed to fundamental analysts, who look at the underlying business behind each company.

By the 1930s, Fibonacci numbers had worked their way into mainstream technical analytical theories, such as Elliot Wave.

Today, most market tracking software and data systems, like Bloomberg, will automatically throw up Fibonacci support and resistance numbers on every stock chart.

Why am I talking about this?

Because I am frequently asked how I pick the precise strike prices for options in my own Trade Alert Service.

I use a combination of moving averages, moving average convergence-divergence (MACD) indicators, Bollinger bands, Fibonacci numbers, and a mumbling chant taught to me by an old Yaqui Indian shaman.

And I do all of this only after going over the underlying fundamentals of the stock or index with a fine-tooth comb. I can’t be any clearer than that.

Enter the high-frequency traders. Knowing that the bulk of us rely on Fibonacci numbers for our short-term trading calls, they have developed algorithms that seek to exploit that preference.

They enter a large number of stop-loss orders to sell just below a “Fibo” support level, then put up fake, but extremely large offers just above it which are usually cancelled.

Only 1% of these orders ever get executed.

When conventional traders see these huge offers to sell, they panic, dump their stocks, and trigger the stop losses. The HFTs then jump in and cover their own shorts for a quick profit, sometimes only for a fraction of a penny.

The net effect of these shenanigans is to make Fibo numbers less effective. Fibo support is just not as rock solid as it used to be, nor is resistance.

This is why the performance of several leading technical analysts has seriously deteriorated in recent years.

Although their importance is now somewhat diluted, I still enjoy Fibonacci numbers as I see them in nature all around me. They occasionally have other uses such as in cryptography.

When I watched The Da Vinci Code sequel, “Angels & Demons,” and listened to the clues, I recognized the handiwork of my old friend Leo.

The rest of the audience sat there clueless, except for the group in the next row wearing “UC BERKELEY” hoodies.

For the fellow geeks and nerds among you, here are the precise Fibonacci numbers indicating support and resistance, which you will find on a stock chart.

Fibonacci Ratios

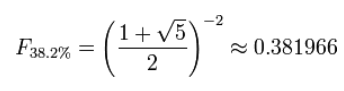

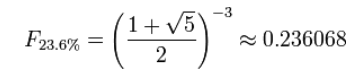

Fibonacci ratios are mathematical relationships, expressed as ratios, derived from the Fibonacci sequence. The key Fibonacci ratios are 0%, 23.6%, 38.2%, and 100%.

The key Fibonacci ratio of 0.618 is derived by dividing any number in the sequence by the number that immediately follows it. For example: 8/13 is approximately 0.6154, and 55/89 is approximately 0.6180.

The 0.382 ratio is found by dividing any number in the sequence by the number that is found two places to the right. For example: 34/89 is approximately 0.3820.

The 0.236 ratio is found by dividing any number in the sequence by the number that is three places to the right. For example: 55/233 is approximately 0.2361.

The 0 ratio is :

Leonardo Fibonacci (Maybe)

https://www.madhedgefundtrader.com/wp-content/uploads/2018/10/Leonardo-Fibonacci.png464343MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2021-08-18 09:02:042022-12-28 10:55:10Hanging With Leonardo

When the pandemic hit in February, I figured Airbnb was toast. Global travel had ground to a halt, and competitors like Wynn Resorts (WYNN) and Hyatt Hotels (H) saw their share prices plunge to near zero.

Instead, the opposite happened.

While the big hotels continue to roast in purgatory, Airbnb catapulted to a new golden age, and how they did it was amazing.

They turned all travel local. Instead of recommending that I visit Cairo, Tokyo, or Rio de Janeiro, they suggested Carmel, Monterey, or Mendocino, all destinations within driving distance. It worked, and the company is now moving from strength to strength.

My neighborhood in Incline Village, NV was almost always deserted outside of holidays. Now it is packed with Airbnbrs awkwardly moving in every Friday only to flee on Sunday.

How would you like to get a 90% discount on all of your luxury hotel accommodations?

During my most recent trip to Dubrovnik in Croatia, I rented an 800-square foot, two-bedroom, two-bath home inside the city walls for $300 a night.

A single, cramped 150 square foot room in the nearest five-star hotel was $600 night.

All that was missing was room service, a hand out for a big tip, and a surly attitude.

Sounds like a massive, game-changing disruption to me.

Thank you, Airbnb!

I was not surprised to hear that the home-sharing app, Airbnb, was given a $31 billion valuation in the latest venture capital funding round.

The big question for you and me is: Will the valuation soar tenfold to $300 billion, and how much of a piece of that will you and I be allowed to get?

To answer that question, I spent six weeks traveling around the world as an Airbnb customer. This enabled me to understand their business model, their strengths and weaknesses, and analyze their long-term potential.

As a customer, the value you receive is nothing less than amazing.

I have been a five-star hotel client for most of my life, with someone else picking up the tab much of the time (thank you, Morgan Stanley!), so I have a pretty good idea on the true value of accommodations.

What you get from Airbnb is nothing less than spectacular. You get three or four times the floor space for one-third the price. That’s a disruption factor of 7:1.

The standards are often five-star and at the top end depending on how much you spend. I found out I could often get an entire three-bedroom house for the price of a single hotel room, with a better location.

Or, I could get an excellent abode in rural settings, where none other was to be had, whatsoever.

That’s a big deal for someone like me who spends so much of the year on the road.

You also get a new best friend in every city you visit.

On most occasions, the host greeted me on the doorsteps with the keys, and then introduced me to the mysteries of European kitchen appliances, heating, and air conditioning.

Pre-stocking the refrigerator with fresh milk, coffee, tea, and jam seems to be a tradition the hosts pick up in their Airbnb orientation course.

One in Waterford, Ireland even left me a bottle of wine, plenty of beer, and a frozen pizza. She read my mind. She then took me on a one-hour tour of their city, divulging secrets about their favorite restaurants, city sights, and nightspots. Everyone proved golden. Thanks, Mary!

After you check out, Airbnb asks you to review the accommodation. These can be incredibly valuable in deciding your next pick.

I had one near miss with what I thought was a great deal in London, until I read, “The entire place reeks of Indian cooking.”

Similarly, the hosts rate you as a guest.

One hostess in Dingle, Ireland shared a story about picking up her clients from town after they got drunk and lost in the middle of the night. Then they threw up in the back of the car on the way home.

Guests forgetting to return keys are another common complaint.

Needless to say, I received top ratings from my hosts, as fixing their WIFI to boost performance became a regular and very popular habit of mine.

After my initial fabulous experience in London, I thought it might be a one-off, limited to only the largest cities. So, I started researching accommodations for my upcoming trips.

I couldn’t have been more wrong.

Just the Kona Coast on the big island of Hawaii had an incredible 50 offerings, including several bargain beachfront properties.

The center of Tokyo had over 300 listings. The historic district in Florence, Italy had a mind blowing 351 properties.

Fancy a retreat on the island of Bali in Indonesia and tune up your surfing? There are over 197 places to stay!

Airbnb has truly gone global.

Airbnb’s business model is almost too simple to be true, involving no more than a couple of popular applications. Call it an artful melding of Google Earth, email, text, and PayPal.

While no one was looking, it became the world’s largest hotel at a tiny fraction of the capital cost.

The company has 4 million hosts in 100,000 cities worldwide, and 150 million users. That supply/demand imbalance shifts burden of the cost to the renters, who usually have to fork out a 12% fee, plus the cost of the cleaning service.

Hosts only pay 3% to process the credit card fees for the payment.

The tidal wave of revenues this has created has enabled Airbnb to become San Francisco’s largest privately owned “unicorn”,

To say that Airbnb has created controversy would be a huge understatement.

For a start, it has emerged as a major challenge to the hotel industry, which is still stuck with a 20th century business model. There’s no way hotels can compete on price.

One Airbnb “super host” in Manhattan at one point managed 200 apartments, essentially, creating out of scratch, a medium sized virtual “hotel” until the city caught on to them.

Taxes are another matter.

Some municipalities require hosts to pay levies of up to 20%, while others demand quarterly tax filings and withholding taxes. That is, if tax collectors can find them.

Airbnb may be the largest new source of tax evasion today.

In cities where housing is in short supply, Airbnb is seen as crowding out local residents. After all, an owner can make far more money subletting their residence nightly than with a long-term lease.

Several owners told me that Airbnb covered their entire mortgage and housing cost for the year, while paying off the mortgage at the same time.

Owners in the primest of areas, like mid-town Manhattan off of Central Park, or the old city center in Dubrovnik, rent their homes out as much as 180 days a year.

It is doing nothing less than changing lives.

That has forced local governments to clamp down.

San Francisco has severe, iron-clad planning and zoning restrictions that only allow 2,000 new residences a year to come on the market.

It is cracking down on Airbnb, as well has other home sharing apps like FlipKey, VRBO, and HomeAway, by forcing hosts to register with the city or face brutal $1,000 a day fine.

So far, only 1,675 out of 9,000 hosts have done so.

Ratting out your neighbor as an off the grid Airbnb member has become a new cottage industry in the City of the Bay.

Airbnb is fighting back with multiple lawsuits, citing the federal Communications Decency Act, the Stored Communications Act, and the First Amendment covering the freedom of speech.

It is a safe bet that a $31 billion company can spend more on legal fees than a city the size of San Francisco.

The company has also become the largest contributor in San Francisco’s local elections. In 2015, it fought a successful campaign against Proposition “F” meant to place severe restrictions on their services.

An Airbnb stay over is not without its problems.

The burden of truth in advertising is on the host, not the company, and inaccurate listings are withdrawn only after complaints.

A twenty-something-year-old guy’s idea of cleanliness may be a little lower than your own.

Long time users learn the unspoken “code”.

“Cozy” can mean tiny, “as is” can be a dump, and “lively” can bring the drunken screaming of four letter words all night long, especially if you are staying upstairs from a pub.

And that spectacular seaside view might come with relentlessly whining Vespa’s on the highway out front. Always bring earplugs and blindfolds as backups.

Researching complaints, it seems that the worst of the abuses occur in shared accommodations. Learning new foreign cultures can be fascinating. But your new roommate may want to get to know you better than you want, especially if you are female.

In one notorious incident, a Madrid guest was raped and had to call customer service in San Francisco to get the local police to rescue here. The best way to guard against such unpleasantries is to rent the entire residence for your use only, as I do.

Another problem arises when properties are rented out for illegal purposes, such as prostitution or drug dealing.

More than once, an unsuspecting resident woke up one morning to discover they were living next door to a new bordello.

Coming out of the pandemic, my conclusion is that the travel industry is entering a hyper growth phase. Blame the emerging middle-class Chinese, who seem to be everywhere.

The real shock came when I left Airbnb and stayed in a regular hotel. Include the fees and the cleaning charges, and the service is no longer competitive for a single night stay. Total costs now regularly run double the posted one night price posted on websites.

In any case, most hosts have two or three night minimums to minimize hassle.

When I checked in at a Basel, Switzerland Five Star hotel, all I got was a set of keys and a blank stare. No great restaurant tips, no local secrets, no new best friend.

I spent that night surfing www.airbnb.com , planning my next adventure.

My New Best Friend

https://www.madhedgefundtrader.com/wp-content/uploads/2016/07/Airbnb-Hostess-e1468963965771.jpg400393Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-08-17 09:02:482021-08-17 11:42:46Is Airbnb Your Next Ten-Bagger?

According to the legendary economist John Maynard Keynes: “Markets can remain irrational longer than you can remain liquid.”

Keynes should know. After making a fortune trading foreign currency, he was almost wiped out by the 1929 crash when markets fell 90%.

I keep that quote taped to my monitor to instill humility, discipline, self-control, and to avoid hubris. It works most of the time. It is the father of my aggressive stop-loss strategy.

However large the wall of money was before; it is getting bigger. People are making more money, their home values have soared, more are working, the Fed’s quantitative easing continues unabated, and Washington deficit spending is breaking all records, and federal benefits continue to pour through the system.

A very large part of this new money has gone into the stock market, and it will continue to do so. August usually presents the best buying opportunity of the year with a frightful, gut-churning selloff. It’s not happening this time, baby.

If we get another hot payroll report for August, then happy days are here again and it’s off to the races for the rest of 2021. A 100% trading profit for the year comes into range for me, as well as you.

It gets better.

The delta variant has taken new Covid cases from 15,000 a day to 100,000, pushing back the reopening and slowing the economy. ALL of that growth gets pushed back into 2022, making it another hot year. We won’t see the current historic 12% growth rate, but 5% could be doable. Stocks will love it.

Could 2022 be another 100% return year? Maybe.

One thing is for sure. The market could care less about Covid, closing at an all-time high on Friday. Covid is now a known quantity. A year ago, it looked like the end of the world.

If you are vaccinated, it’s now just an inconvenience. It’s currently only killing unvaccinated Republicans and sadly, children.

The next big thing to happen will be for new cases to peak out and begin a sharp decline, causing stocks to rocket. That’s how traders are positioning themselves now. July Nonfarm PayrollReport explodes to 943,000, taking the Headline Unemployment Rate down an amazing half-point to 5.4%. Leisure & Hospitality was up a staggering 380,000. Bonds (TLT) were crushed, down two full points and yields up 19 basis points from the low to 1.29%, gold (GLD) was destroyed, and the US dollar (UUP) popped. The hot number could bring forward a Fed tapper and interest rate rise. Certainly, makes this month’s Jackson Hole meeting interesting. New Covid Cases hit 100,000 daily, 86% of which are the delta variant, 1,000 times more powerful than the original strain. That’s still a fraction of the 2.5 million cases a day seen in January. The vaccines seem powerless against the onslaught, although they eliminate the possibility of death. The unvaccinated are the walking dead. Companies like Wells Fargo, Amazon, and JP Morgan have delayed reopening. We’re all helpless until a new booster shot comes out in months. Infrastructure Deal to be signed, at $550 billion worth of road, bridge, water, and power projects. It should generate 2.75 million jobs, if you can find the workers. Expect your local freeways to start getting tied up in a few months when the projects begin in all 50 states. Per capital, Alaska and Hawaii will get the most money.

Copper Unions Vote to strike in Chile, cutting off 33% of the global supply. This is just when the green economy, especially electric cars, is driving demand through the roof. Great news for Freeport McMoRan, which predominantly mines in the US. By (FCX) on dips. US Treasury to sell $126 billion in bonds this week. It also sees rising demand for Treasury Inflation-Protected Securities (TIPS). Am I the only one seeing the contradiction? Fed governor Clarida said the taper could start in November. Don’t buy bonds here on pain of death. ADP disappoints in its monthly read of private job openings, coming in at only 330,000 instead of an expected 690,000. Leisure & Hospitality saw the biggest decline, with only 139,000. Could Friday’s July Nonfarm Payroll report be a bust? Weekly Jobless Claims come in at 385,000, taking another run at post-pandemic lows. This number should really collapse once kids go back to school for the first time in 17 months. Most large companies are now requiring proof of vaccination to return to the office. The same will soon be true for airlines. Think the market is expensive now? After the last pandemic ended in 1919, price earnings multiple for the S&P 500 soared 3.09 times from 5.74X to 17.77X. So, today’s 34.39X looks rich indeed but is only half of the 70.91 peak seen at the bottom of the 2009 Great Recession, back when investors were throwing stocks out the window with both hands. The Index started at a lowly 11.1X back when America was still an emerging market. Could we get the 3X move up seen in the last pandemic? One can only hope.

My Ten Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

My Mad Hedge Global Trading Dispatch saw a healthy gain of +3.36% so far in August. My 2021 year-to-date performance appreciated to 72.57%. The Dow Average is up 15.06% so far in 2021.

I stuck with my four positions, a long in (JPM) and a short in the (TLT) and a short in the (SPY). Since stocks refused to go down, I added longs in Goldman Sachs (GS) and Visa (V). I doubled up my short in the (TLT) after it spiked to a 1.10% yield. The market surge off the back of the July Nonfarm Payroll report also forced me to stop out of my second (SPY) short for a loss.

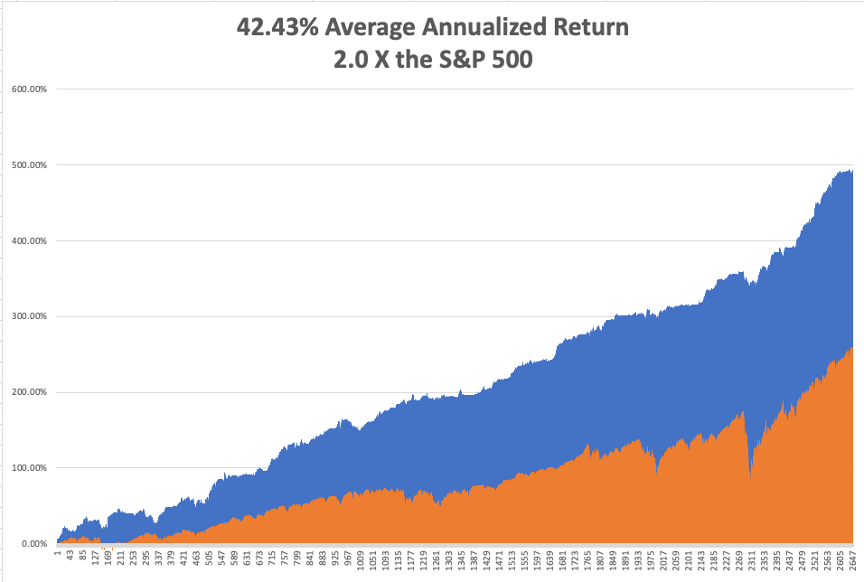

That brings my 11-year total return to 495.12%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return now stands at an unbelievable 42.43%, easily the highest in the industry.

My trailing one-year return retreated to positively eye-popping 110.12%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 35.8 million and rising quickly and deaths topping 617,000, which you can find here.

The coming week will be slow one on the data front.

On Monday, August 9 at 8:00 AM, US Consumer InflationExpectations are out. AMC (AMC) reports.

On Tuesday, August 10 at 7:30 AM, the NFIB Business Optimism Index for July is printed. Coinbase (COIN) and Softbank (SFTBY) report.

On Wednesday, August 11 at 5:30 AM, the US Core Inflation Rate is released. eBay (EBAY) reports.

On Thursday, August 12 at 8:30 AM, Weekly Jobless Claims are announced. Disney (DIS) and Airbnb (ABNB) report.

On Friday, August 13 at 7:00 AM, we get the University of Michigan Consumer Expectations.

As for me, with the 34th anniversary of the 1987 crash coming up, when shares dove 20% in one day, I thought I’d part with a few memories.

I was in Paris visiting Morgan Stanley’s top banking clients, who then were making a major splash in Japanese equity warrants, my particular area of expertise.

When we walked into our last appointment, I casually asked how the market was doing (Paris is six hours ahead of New York). We were told the Dow Average was down a record 300 points. Stunned, I immediately asked for a private conference room so I could call the equity trading desk in New York to buy some stock.

A woman answered the phone, and when I said I wanted to buy, she burst into tears and threw the handset down on the floor. Redialing found all transatlantic lines jammed.

I never bought my stock, nor found out who picked up the phone. I grabbed a taxi to Charles de Gaulle airport and flew my twin Cessna as fast as the turbocharged engines take me back to London, breaking every known air traffic control rule.

By the time I got back, the Dow had closed down 512 points. Then I learned that George Soros asked us to bid on a $250 million blind portfolio of US stocks after the close. He said he had also solicited bids from Goldman Sachs, Merrill Lynch, JP Morgan, and Solomon Brothers, and would call us back if we won.

We bid 10% below the final closing prices for the lot. Ten minutes later, he called us back and told us we won the auction. How much did the others bid? He told us that we were the only ones who bid at all!

Then you heard that great sucking sound. Oops!

What has never been disclosed to the public is that after the close, Morgan Stanley received a margin call from the exchange for $100 million, as volatility had gone through the roof, as did every firm on Wall Street. We ordered JP Morgan to send the money from our account immediately. Then they lost it! After some harsh words at the top, it was found. That’s when I discovered the wonderful world of Fed wire numbers.

The next morning, the Dow continued its plunge but, after an hour, managed a U-turn and launched on a monster rally that lasted for the rest of the year. We made $75 million on that one trade from Soros.

It was the worst investment decision I have seen in the markets in 53 years, executed by its most brilliant player. Go figure. Maybe it was George’s risk control discipline kicking in?