The Cloud Movement is Intact

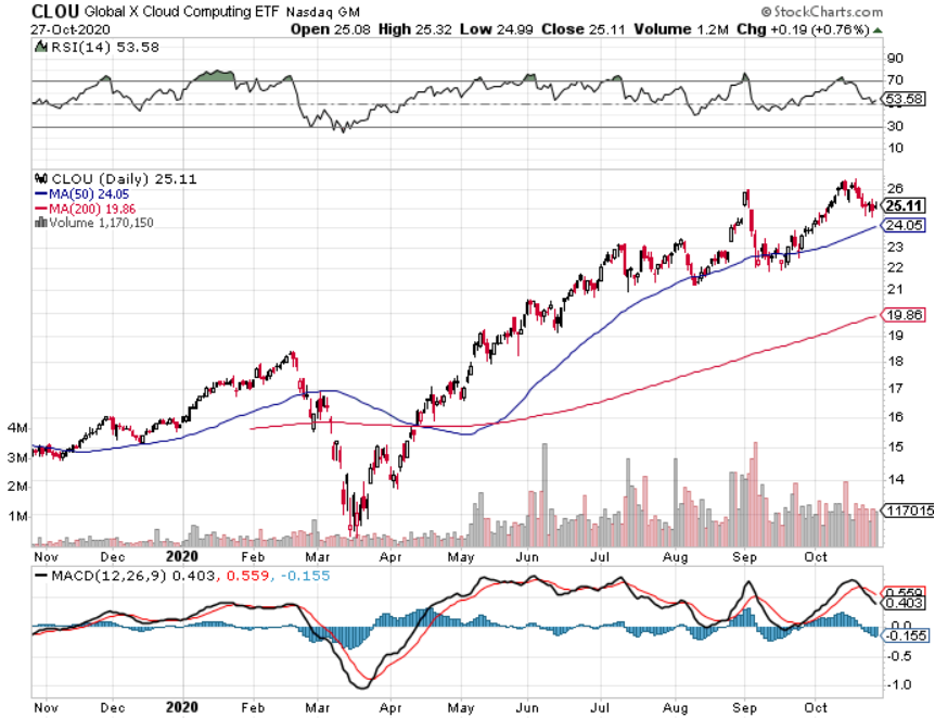

We got another solid sign that the software-as-a-service (SaaS) phenomenon is sticky as ever. You can simply play this with cloud ETF — Global X Cloud Computing ETF Global X Cloud Computing ETF (CLOU)

One of the leading cloud barons of our time, Salesforce.com (CRM) Chief Executive Officer Marc Benioff criticized German rival SAPs business performance in explicit words, rejecting the idea that the German software giant’s challenges are a sign of things to come for his company.

Benioff said that at “SAP, you can see they’re having very significant troubles with the CEO transition they’re going through…they, as you know, moved from one CEO to two, they fired one of those two CEOs. The CEO transition is just not going well and their customers are saying that. Now you can see that their revenues are also reflecting this trouble.”

Protecting his industry makes sense as SAP have decided to blame the cloud industry on their woes and not their management.

Fair enough but Benioff is clearing the debris off the runway and offering a more accurate and rosier snapshot of the current cloud industry.

It’s certainly investor’s every right to worry over SAP’s decision to cut its full-year forecast that helped drag down other software makers, including Salesforce.

Benioff also chimed in and said, “SAP’s troubles, I think, are unique to them.”

Salesforce hasn’t felt the same weakness in guidance, and it was only just this past August, Salesforce reported quarterly sales increased 29% and jacked up its revenue forecast for the year.

The addressable market is growing, and Salesforce is making headway in that market.

Even weaker cloud companies are still showing a healthy heartbeat like Seattle-based F5 Networks (FFIV) saw shares rise after its fiscal fourth quarter earnings report beat expectations.

The company posted revenue of $615 million, up 4%, and non-GAAP earnings per share of $2.59. Wall Street expected revenue of $606 million and EPS of $2.37.

F5 Networks continues to benefit from its move into software and services, expanding beyond its traditional networking hardware business. Software revenue was up 36% from the year-ago quarter and their hardware business drags the overall growth number down to single digits.

The SaaS success is why President and CEO of F5 François Locoh-Donou has indicated that F5 is jumping headfirst into SaaS and nothing will stop this strategy apart from an apocalypse.

Locoh-Donou laid out the company’s strategy to enable “adaptive applications” that can adapt based on the environment.

F5 plans to leverage its traditional application delivery technologies along with its $1 billion acquisition of Shape Security and $670 million acquisition of web server NGINX to position itself as a key player amid a larger trend of automation and artificial intelligence driving advances in software applications and computer networks.

Cloud companies are held up so well that Locoh-Donou told employees that F5 won’t make layoffs during its fiscal year 2020.

I believe that this upcoming earnings season will offer more olive branches into why software stocks continue to be solid, but it's is not to say they aren’t expensive in the short-term.

The software-as-a-service (SaaS) business model continues to be a buckle-your-seatbelt-up growth leader, but other cloud-based services are poised to eclipse it as it matures.

SaaS applications are expected to deliver a highest-ever $105 billion in revenue this year, even as global technology spend dropped 8%, or about $300 billion.

The largest x-factor to SaaS was the broad-based pivot to cloud applications to accommodate remote working.

Even after workers return to the office, SaaS will continue growing because of the computing power and agility it could offer that otherwise couldn't afford it if they had to buy an on-premises or enterprise solution.

SaaS revenue is poised to surpass $121 billion next year and $141 billion in 2022.

For the five-year period between 2018 and 2022, SaaS will grow at a 12% annual rate.

We are now entering the consolidation phase for SaaS where companies are slowly replacing the last on-premises stalwarts in their portfolio, but the low-hanging fruit has mostly been harvested.

The applications with the strongest business case for SaaS have mostly been implemented.

SaaS companies are also facing increased competition and the numbers validate this as SaaS companies typically competed against three other companies in 2012, but by 2017, a SaaS startup could expect to face nine competitors in the same market segment.

Take for instance the digital market industry, the number of SaaS products increased from about 500 to 8,500 during that 5-year period.

The SaaS model has proven to be robust and critical to business continuity.

It will continue to be the preferred deployment mechanism for most applications and until this overarching strategy shifts, the money will be poured into SaaS software.

The first-mover advantage will take hold as the more marginal SaaS applications appear; the more customers will migrate into “brand” names.

For companies like Salesforce and F5 Networks, this means tailwinds, but it will virtually be impossible to become a new SaaS start-up in 2020 as this industry starts to mature.