Should I Buy Coinbase Today?

For all the cryptocurrency haters in the world, it’s getting harder to take that stand.

I’ll tell you why.

Coinbase (COIN) was the first major crypto business to go public in the U.S. when it began trading at $381 Wednesday morning on the Nasdaq and its IPO symbolizes the acceptance of an alternative digital asset class in technology.

Prior to this watershed moment, the only way to play crypto was through second derivatives plays like PayPal (PYPL) and Square (SQ) who have been handsomely rewarded through higher share prices.

Now, we get the biggest U.S. cryptocurrency exchange trading publicly that will allow exposure to mainstream stock-market investors.

The event has also been tabbed as a catalyst that might drive the adoption of incremental digital assets.

At the very least, this lays down a marker for further crypto-related companies eyeing the Nasdaq after Coinbase’s blowout success.

This also shows that the cryptocurrency infrastructure is developing rapidly and its budding credibility is something that needs to be acknowledged.

The Coinbase IPO was also the catalyst in sending bitcoin prices to almost $65,000.

No doubt that the appreciating asset has been the most attractive use case for the incremental investor and cryptocurrency buyer.

Many early investors who got into bitcoin at 20 cents are now billionaires many times over.

After such stunning success, it’s hard to believe that any fintech or cryptocurrency start-up would ever consider doing their IPO anywhere else but New York.

New York has the liquidity, the US dollar, and the capacity to receive such type of growth companies in bulk.

This is not only an emphatic victory for digital assets, but also for the US tech sector and a stamp of validation for the Nasdaq market.

Ironically enough, even during this trade war, Chinese tech companies are clamoring to go public in New York and not mainland China for the above reasons.

Here are a few other highly positive data points to digest that were talking points in their S-1 filing.

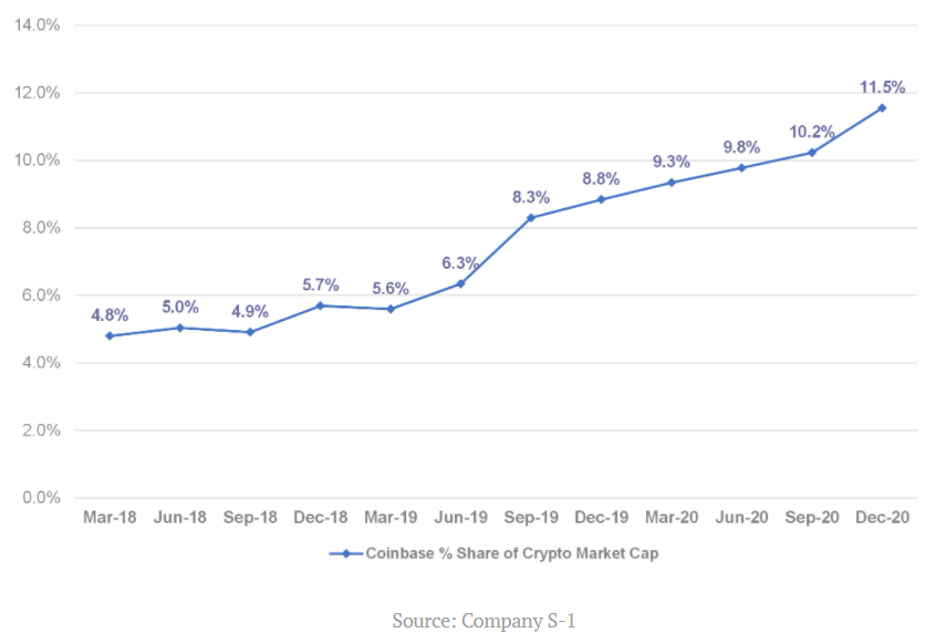

The overall market capitalization of crypto assets grew from less than $500 million to $782 billion between December 31, 2012, and December 31, 2020, representing a CAGR (compound annual growth rate) of over 150%.

Over the same period, Coinbase retail users grew from less than 13,000 to 43 million, a 175% CAGR.

I believe the total market cap of crypto is now around $2 trillion in April 2021.

And more recently, Coinbase has experienced significant growth in the number of institutions on their platform, increasing from over 1,000 as of December 31, 2017, to 7,000 as of December 31, 2020.

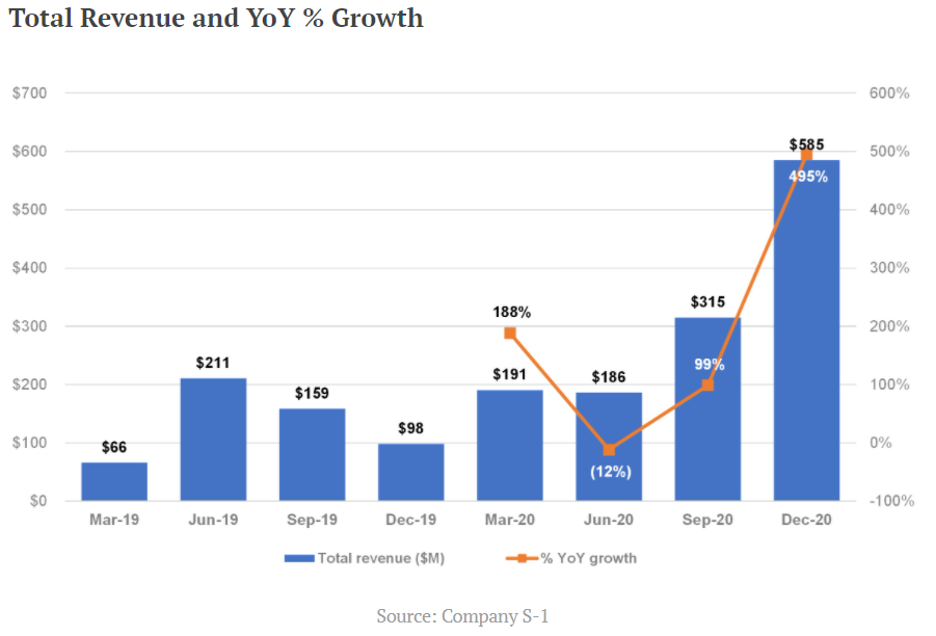

Bitcoin reported a nine-fold increase in Q1 revenue, to $1.8B, up from $190.6M the previous year.

Just like Google and Facebook benefit from a duopoly, Coinbase will benefit from being the only pure cryptocurrency option on the Nasdaq and that will put a floor under shares in the short-term.

The growth metrics of the company are also robust via a helping hand by the increasingly expensive price of bitcoin.

No doubt that this company’s prospects are tied to the hip with the prices of cryptocurrencies.

If the price of bitcoin retraces to $30,000, which it could because of the high volatility of it, expect Coinbase shares to dive with it.

This for all intents and purposes is a bet on the health and price trajectory of bitcoin for better or worse until other crypto-based choices are introduced which would give more layers and complexity to this sub-sector.

Bitcoin calls out Binance which they state as a competitor and Kraken is another exchange that is large and vying for the same capital.

I believe these two companies have a chance to go public and that is when you will really see the institutions jump on this crypto bandwagon.

More options and a foundational investment base will also promote stability in this new technology sub-sector.

Should you buy Coinbase today?

No.

I understand Coinbase’s growth metrics are off the charts with revenue growing 900%, but it’s not worth $100 billion market cap on just $1.8 billion of quarterly sales.

Investors would need solid tailwinds such as bitcoin passing $100,000 in 2021 for this company to be worth $100 billion and I just don’t see it.

Then also understand the cybersecurity and possible regulations are two risks that could blow up the business model at any moment which would take down the premium in the stock.

Yes, the meteoric rise of crypto at the start of 2021 has turned heads, but as the economy reopens, I do believe money will rotate from crypto back into traditional technology that is underpinned by cash cow businesses.

Highly profitable companies that aren’t FANGs are also set to deliver share appreciation to shareholders such as Salesforce (CRM) or a company like Adobe (ADBE) who earn profits of $5.27 billion on $13 billion of annual revenue.

I acknowledge that Coinbase’s IPO was the perfect time to go public.

They are taking advantage of easy money and low rates while the acceptance of this alternative asset class has never been higher.

However, I don’t see any more incremental growth in the short term and the stock is more than fully priced today.

The risk-reward is not favorable to pile into this stock now unless you have a bullish 50-year view on crypto and can’t wait.

This stock will go through volatility because of the inherent dynamics they are tied to and I would seriously look at buying Coinbase only on a massive sell-off.

Don’t go chasing unicorns.

At the end of the day, this is a real company with real revenue growth of 900% year-over-year. Slice it up anyway, and these numbers are numbers that attract investors, but the stock is too expensive right here.