SPAC Business Pulls Back

Never waste a crisis.

The SEC sure isn’t.

They are using this stock market meltdown to broaden out the risk to who is liable for special purpose acquisition companies (SPACs).

The new regulation has meant that investment bankers who do the deal then advise the companies post-IPO are bailing on this business in droves.

There have been whispers about this potential regulation for quite a while as many investment advisers were putting through low-quality companies that would never turn a profit in a million years.

Investors would be held with the bag as these SPACs were prone to severely underperforming in the stock market.

Powerful Wall Street banks like Goldman Sachs (GS) are pulling out of working with most SPACs it took public, the second-biggest underwriter of special purpose acquisition companies last year, has been telling sponsors of the vehicles it will be ending its involvement.

A SPAC works with its adviser even after going public to finish its merger with a participating firm, known as the de-SPAC transaction.

If it fails to complete that deal, it’s forced to return capital to investors. In cases where the public company is very close to completing the de-SPAC process, Goldman will fulfill its role.

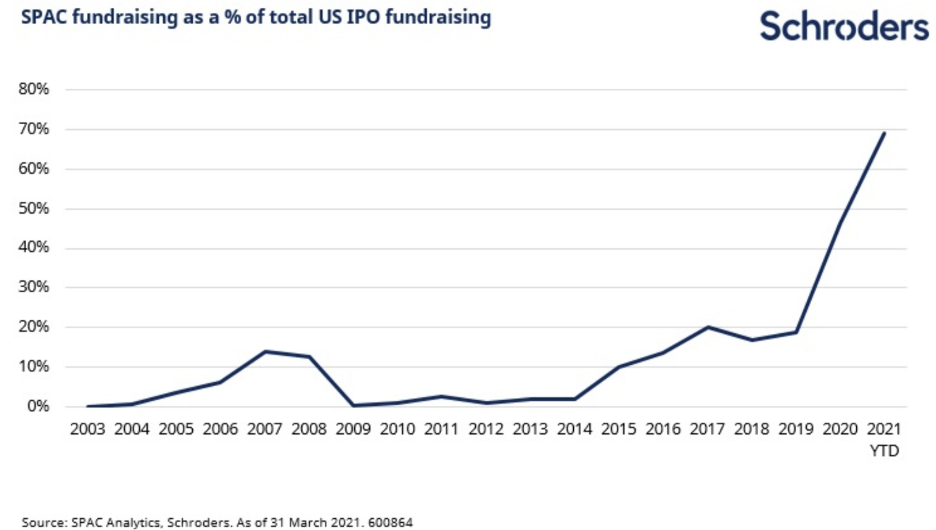

SPACs were popular on Wall Street over the past couple of years, luring financiers, politicians, and celebrities who were able to profit from investors piling into the investment vehicles.

The SEC is tightening oversight of SPACs including exposing underwriters to greater liability risk.

Lawyer advocates have argued the listings were bypassing rules imposed on traditional initial public offerings and exposing retail shareholders to extra risks.

The SEC’s proposal would require SPACs to disclose more information about potential conflicts of interest and make it easier for investors to sue over false projections.

There is no visibility on what company might be acquired (this is a regulatory requirement). A SPAC’s prospectus often includes some wording about the type of company or industry it intends to focus on, but there’s nothing to stop it from going in a totally different direction.

In many cases, those same sponsors were courted by large banks to put their names behind their SPACs, with the structure allowing them to turn an initial investment of a few million dollars into many multiples of that. And their Wall Street underwriters could make more than 5% in fees for taking a SPAC public, helping the sponsor find a takeover target and complete the de-SPAC.

The SEC's concerns might be warranted just based on how awful SPAC stocks are performing.

Take for example, SPAC ETF Morgan Creek - Exos SPAC Originated ETF (SPXZ) whose shares have gone from $21 in the past year to $11 today.

There have been a few SPACs that are worth investing in partially because once the SPAC goes public, the company can turn its business 180 degrees and do something completely different.

They are not beholden to anything, unlike traditional IPOs which are strict in defining what they do and how they do it.

Naturally, a lot of fraud-type companies can go public quickly with the help of a famous celebrity marketing their SPAC and that’s exactly what has happened.

New York doesn’t need more IPOs, but it needs more high-quality IPOs and this will prevent many investors from losing all their money.

One of the big unintended consequences of this bear market is that regulation is finally focusing on the fringe elements in tech and that should mean a healthier tech sector moving forward.