Poke your hand into a hornet's nest and you can count on an extreme reaction, a quite painful one.

As California is the growth engine for the entire US economy, accounting for 20% of US GDP, it is no surprise that it has become the primary target of Chinese retaliation in the new trade war.

The Golden State exported $28.5 billion worth of products to China in 2017, primarily electronic goods, with a host of agricultural products a close second.

In the most devious way possible, the Middle Kingdom targeted Trump supporters in the most liberal state in the country with laser-like focus. California exports 46% of its pistachios to China, followed by 35% of its exported plums, 20% of exported oranges, and 12% of its almonds.

By comparison, California imported a gargantuan $160.5 billion worth of goods from China last year, mostly electronics, clothing, toys, and other low-end consumer goods.

Some $16 billion of this was recycled back into the state via investment in real estate and technology companies.

Anecdotal evidence shows that figure could be dwarfed by the purchase of California homes by Chinese individuals looking for a safe place to hide their savings. Local brokers report that up to one-third of recent purchases have been by Chinese nationals paying all cash.

The Chinese tried to spend more. Their money is thought to be behind Broadcom's (AVGO) $105 billion bid for QUALCOMM (QCOM), which was turned down for national security reasons.

The next big chapter in the trade war will be over the theft of intellectual property, and that one will be ALL about the Golden State.

Also at risk is virtually Apple's (AAPL) entire manufacturing base in China, where more than 1 million workers at Foxconn assemble iPhones, Macs, iPads, and iPods.

The Cupertino, CA, giant could get squeezed from both sides. The Chinese could interfere with its production facilities, or its phones could get slapped with an American import duty.

So far, the trade war has been more bluff than bite. The US duties announced come to only $3 billion on $50 billion worth of trade. China responded with incredible moderation, only restricting $3 billion worth of imports.

By comparison, in 2017 the US imported a total of $505.6 billion in goods from China and exported $130.4 billion. Against this imbalance, the US runs a largest surplus in services.

The next Chinese escalation will involve a 25% tariff on American pork and recycled aluminum. Who is the largest pork producer in the US? Iowa, with $4.2 billion worth, and the location of an early presidential election primary.

Beyond that, Beijing has darkly hinted that is will continue to boycott new US Treasury bond auctions, as it has done for the past six months, or unload some if its massive $1.6 trillion in bond holdings.

Given the price action in the bond market today, with the United States Treasury Bond Fund (TLT) at a two-month high, I would say that the market doesn't believe that for two seconds. The Chinese won't cut off its nose to spite its face.

In the end, I think not much will come of this trade war. That's what the stock market told us yesterday with a monster 700-point rally, the biggest in three years.

The administration is discovering to its great surprise that its base is overwhelmingly against a trade war. And as business slows down, it will become evident in the numbers as well.

The US was the big beneficiary from the global trading system. Why change the rules of a game we are winning?

Still, national pride dies hard.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/03/California-chart-1-1-e1522182790519.jpg217580MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-03-28 01:07:062018-03-28 01:07:06From the Front Line of the Trade War

Flabbergasted consumers reacted last holiday season when Apple dared offer a $1,000 smartphone.

How confident this company has become!

Well, this is just the beginning.

Apple (AAPL) will be the first smartphone maker to offer a $2,000 phone, and I will tell you why!

The tech industry is going through a cumbersome wave of repricing after several high-profile debacles that have cast the light on the true value of data.

The upward revision of data has seen more players pour into the game attempting to carve out a slice of the pie for themselves.

The reason why tech companies will start offering their products at higher price points is because the inputs are rising at a rapid clip.

Apple's Development and Operations (DevOps) costs to design and maintain this outstanding product is going through the roof.

Apple's DevOps employees earn around $145,000 per year and compensation is rising. Granted, the technology is developing and batteries smaller, but salaries are rising at a quicker relative pace because of the dire shortage of DevOps talent in Silicon Valley.

It's possible that living in a shoebox at $4,200 per month in Mountain View, Calif., is off-putting for potential staff.

The most expensive part of an iPhone X is the OLED screen.

Apple estimated costs of $120 per screen manufacturing the Apple iPhone X. The cost doubled from LCD panels from $60 per screen.

Samsung (SSNLF) has been best of breed for screens for a while, and it is currently working on the next generation of Micro LED tech, which is the next gap up from the OLED displays of today.

Samsung has an inherent conflict of interest with Apple, creating tension between these tech stalwarts. Apple made the contentious decision to procure in-house screens at a secret manufacturing facility in Santa Clara, Calif., to avoid the constant friction.

It's common knowledge that the average price of technology shrinks over time, but the American smartphone industry has defied gravity with expected prices to shoot up 6% to $324 in 2018.

The Apple iPhone X raw costs were around $400 per phone. There is zero chance that a next gen, enhanced Apple smartphone will cost this low ever again.

Confirming this trend are Chinese smartphones retail prices rising at 15% last year.

The cost of memory, DRAM and NAND chips, rose dramatically this past year. As more memory is designed into these devices, the costs keep trending higher.

Lithium-ion batteries only add up to 1% to 2% of OEM (Original Equipment Manufacturers) cost and probably only bumps up the cost of iPhones incrementally.

The more skittish situation is the EV (Electric Vehicles) snafu.

Volkswagen (VLKAY) announced it will transform its entire fleet of 300 models into electrified versions by 2025.

In order to achieve this lofty objective, Volkswagen has earmarked $25 billion for batteries from Samsung, LG, and Contemporary Amperex. Volkswagen hopes to have 16 up and running (EV) factories by 2022, up from three today.

The goal is unattainable because of a lack of in-house battery production.

CEO Matthias Muller said the reason for not manufacturing in-house batteries was, "Others can do it better than we can."

Muller will rue the decision down the line as a myriad of companies migrate toward in-house solutions, giving firms more control over the process and overhead.

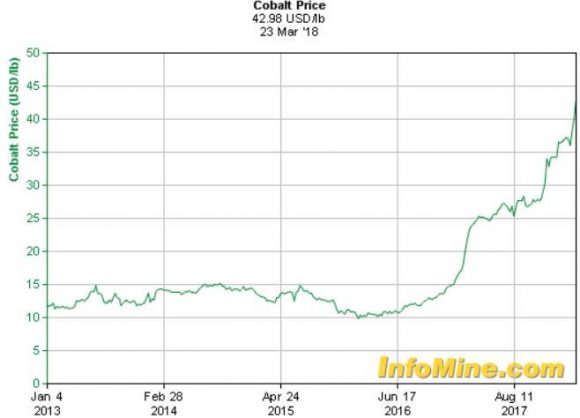

More importantly, Muller will have to rely on the ebb and flow of rising cobalt prices.

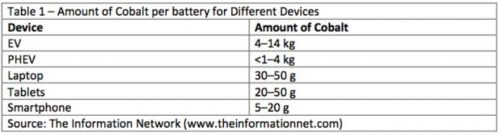

A battery for an (EV) ranges between $8,000- to 20,000, comprising the largest input for the (EV) makers such as Tesla (TSLA) and Ford (F).

Making matters worse, companies cut from all cloth are hoarding cobalt reserves based on anticipating the potential demand.

This phenomenon will cause all big tech players to replenish any reserves of base materials immediately.

Apple has had chip shortage problems in the past. This year is even worse than 2017, with NAND and DRAM chip supply trailing the demand by 30%. Tech companies have been hastily locking down contracts in advance to ensure the necessary materials to produce their flashy gadgets.

Lithium battery demand is expected to rise 45% between 2017 and 2020, and there has been no meaningful large-scale investment into this industry.

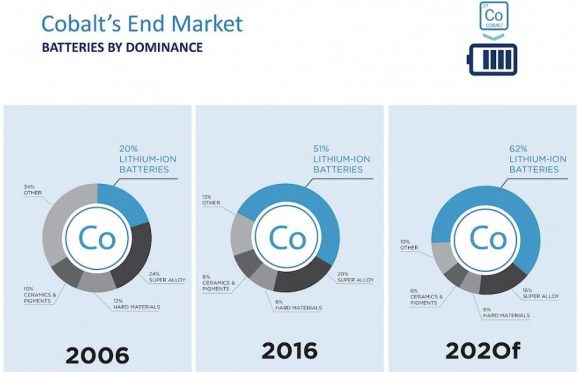

Battery production made up 51% of cobalt demand in 2016 and will hit around 62% by 2022.

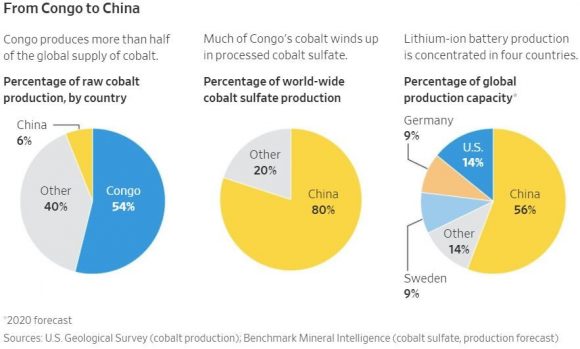

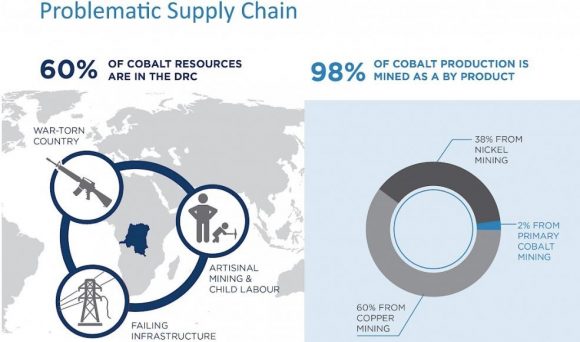

Compounding the complexity is 60% of global cobalt production is found in one country - the Democratic Republic of the Congo (DRC).

DRC is a hotspot for geopolitical fallout and its history is littered with civil war, internal conflict, and poor infrastructure.

The 21st century will be dependent on a chosen group of valuable materials. Cobalt is shaping up to be the leader of this pack and is needed in a plethora of business applications such as EV, lithium-ion batteries, and PCs.

Cobalt is vital in metallurgical applications that include aerospace rotating parts, military and defense, thermal sprays, prosthetics, and much more.

The DRC recently proposed a revised mining law increasing taxes on cobalt and other precious metals. The legislation has yet to be written into stone and would certainly jack up the price of cobalt.

Glencore's (GLNCY) management has noted this mining tax is "challenging" at a time it is just completing its Katanga expansion.

Katanga has the potential to become the largest global copper and cobalt producer.

Copper is equally important to cobalt since cobalt production is a by-product of copper and nickel mining. Only 2% of cobalt results directly from cobalt mining, and 60% via copper mining, and 38% via nickel mining.

Last year, Freeport-McMoRan (FCX) was dangling its cobalt project to outside investors in the DRC but was unable to fetch a premium price.

In a blink of an eye, China Molybdenum Co. (CMCLF) swooped in and (FCX) accepted an offer of $2.65 billion. (FXC) used the sale to pay down debt while the price of cobalt has taken off to the moon.

It gets worse, China owns 80% of refined global cobalt production and 90% of its operations are in the DRC.

China is attempting to corner the cobalt market in the DRC, gaining a stranglehold on future technological devices, (EV)s, and big data.

The keys to future technological hegemony lie in the jungles of the DRC, and China has the first mover advantage and backing of the communist party as (CMCLF) strives to be a global leader in cobalt production.

China has smartly wriggled its way down to the bottom of the supply chain capturing cobalt resources, and if a trade war ensues, China can simply cut off cobalt supply lines to whomever.

There is nothing CFIUS or Donald Trump can do.

America's 14% of global cobalt production will be insufficient to produce the new (EV)s, iPhone 11s, gizmos and gadgets that American consumers demand for daily life.

Analysts expected Apple to acquire some supplementary companies that will aid in expansion following the overseas repatriation.

A thriving software outfit or a company of cloud developers would have sufficed. However, reports streaming in that Apple has entered into negotiations to buy a five-year supply of cobalt directly from miners for the first-time underscore where Apple's priorities lie.

Cobalt demand expects to increase by 30% from 2016 to 2020.

Apple is scared it will be locked out of the cobalt market or forced to pay ludicrous prices for its cobalt needs.

Considering the price of cobalt has quadrupled since June 2016, and smartphones are 25% of the cobalt market, it's a strategically prudent move by Apple's CEO Tim Cook in light of BMW (BMWYY) announcing the need of 10X more cobalt by 2025.

Going forward anything comprised of cobalt-based technology will garner a higher premium resulting in higher prices for consumers including that $2,000 iPhone.

(FCX) is a must buy for those who believe precious metals are the foundation to all future technology. Other intriguing names include Brazilian company Vale S.A. (VALE), and Glencore, the largest Swiss company by revenue.

Or if you have the cash, plunk it down on a cobalt mine in the DRC. But only if you're insane.

"Heavier-than-air flying machines are impossible." - Lord Kelvin, President of the Royal Society, in 1895

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-03-28 01:05:332018-03-28 01:05:33How the Cobalt Shortage Will Lead to the $2,000 iPhone

With the stock market falling for the next few weeks, or even months, it's time to rehash how to profit from falling markets one more time.

There is nothing worse than closing the barn door after the horses have bolted.

No doubt, you will receive a wealth of short selling and hedging ideas from your other research sources and the media at the next market bottom. That is always how it seems to play out.

So I am going to get you out ahead of the curve, putting you through a refresher course on how to best trade falling markets now.

Market's could be down 10% by the time this is all over.

THAT IS MY LINE IN THE SAND!

There is nothing worse than fumbling around in the dark looking for the matches after a storm has knocked the power out.

I'm not saying that you should sell short the market right here. But there will come a time when you will need to do so. Watch my Trade Alerts for the best market timing. So here are the best ways to profit from declining stock prices, broken down by security type:

Bear ETFs

Of course the granddaddy of them all is the ProShares Short S&P 500 Fund (SH), a non leveraged bear ETF that is supposed to match the fall in the S&P 500 point for point on the downside. Hence, a 10% decline in the (SPY) is supposed to generate a 10% gain the in the (SH).

In actual practice, it doesn't work out like that. The ETF has to pay management operating fees and expenses, which can be substantial. After all, nobody works for free.

There is also the "cost of carry," whereby owners have to pay the price for borrowing and selling short shares. They are also liable for paying the quarterly dividends for the shares they have borrowed, around 2% a year. And then you have to pay the commissions and spread for buying the ETF.

Still individuals can protect themselves from downside exposure in their core portfolios through buying the (SH) against it (click here for the prospectus). Short selling is not cheap. But it's better than watching your gains of the last seven years go up in smoke.

Virtually all equity indexes now have bear ETF's. Some of the favorites include the (PSQ), a short Play on the NASDAQ (click here for the prospectus), and the (DOG), which profits from a plunging Dow Average (click here for the prospectus).

My favorite is the (RWM) a short play on the Russell 2000, which falls 1.5X faster than the big cap indexes in bear markets (click here for the prospectus).

Leveraged Bear ETFs

My favorite is the ProShares Ultra Short S&P 500 (SDS), a 2X leveraged ETF (click here for the prospectus). A 10% decline in the (SPY) generates a 20% profit, maybe.

Keep in mind that by shorting double the market, you are liable for double the cost of shorting, which can total 5% a year or more. This shows up over time in the tracking error against the underlying index. Therefore, you should date, not marry, this ETF or you might be disappointed.

3X Leveraged Bear ETFs

The 3X bear ETFs, like the UltraPro Short S&P 500 (SPXU), are to be avoided like the plague (click here for the prospectus).

First, you have to be pretty good to cover the 8% cost of carry embedded in this fund. They also reset the amount of index they are short at the end of each day, creating an enormous tracking error.

Eventually, they all go to zero, and have to be periodically redenominated to keep from doing so. Dealing spreads can be very wide, further added to costs.

Yes, I know the charts can be tempting. Leave these for the professional hedge fund intra day traders they are meant for.

Buying Put Options

For a small amount of capital, you can buy a ton of downside protection. For example, the April (SPY) $182 puts I bought for $4,872 allowed me to sell short $145,600 worth of large cap stocks at $182 (8 X 100 X $6.09).

Go for distant maturities out several months to minimize time decay and damp down daily price volatility. Your market timing better be good with these, because when the market goes against you, put options can go poof, and disappear pretty quickly.

That's why you read this newsletter.

Selling Call Options

One of the lowest risk ways to coin it in a market heading south is to engage in "buy writes." This involves selling short call options against stock you already own, but may not want to sell for tax or other reasons.

If the market goes sideways, or falls, and the options expire worthless, then the average cost of your shares is effectively lowered. If the shares rise substantially they get called away, but at a higher price, so you make more money. Then you just buy them back on the next dip. It is a win-win-win.

I'll give you a concrete example. Let's say you own 100 shares of Apple (AAPL), which closed on Friday at $95.13, worth $9,513. If you sell short 1 July, 2016 $100 call at $1.30 against them, you take in $130 in premium income ($1.30 X 100 because one call option contract is exercisable into 100 shares).

If Apple closes below $100 on the July 15, 2016 expiration date, the options expire worthless and you keep your stock and the premium. You are then free to repeat the strategy for the following month. If (AAPL) closes anywhere above $100 and your shares get called away, you still make money on the trade.

Selling Futures

This is what the pros do, as futures contracts trade on countless exchanges around the world for every conceivable stock index or commodity. It is easy to hedge out all of the risk for an entire portfolio of shares by simply selling short futures contracts for a stock index.

For example, let's say you have a portfolio of predominantly large cap stocks worth $100,000. If you sell short 1 June, 2016 contract for the S&P 500 against it, you will eliminate most of the potential losses for your portfolio in a falling market.

The margin requirement for one contract is only $5,000. However if you are short the futures and the market rises, then you have a big problem, and the losses can prove ruinous.

But most individuals are not set up to trade futures. The educational, financial, and disclosure requirements are beyond mom and pop investing for their retirement fund.

Most 401ks and IRAs don't permit the inclusion of futures contracts. Only 25% of the readers of this letter trade the futures market. Regulators do whatever they can to keep the uninitiated and untrained away from this instrument.

That said, get the futures markets right, and it is the quickest way to make a fortune, if your market direction is correct.

Buying Volatility

Volatility (VIX) is a mathematical construct derived from how much the S&P 500 moves over the next 30 days. You can gain exposure to it through buying the iPath S&P 500 VIX Short Term Futures ETN (VXX), or buying call and put options on the (VIX) itself.

If markets fall, volatility rises, and if markets rise, then volatility falls. You can therefore protect a stock portfolio from losses through buying the (VIX).

I have written endlessly about the (VIX) and its implications over the years. For my latest in-depth piece with all the bells and whistles, please read Buy Flood Insurance With the (VXX)by clicking here.

Selling Short IPO's

Another way to make money in a down market is to sell short recent initial public offerings. These tend to go down much faster than the main market. That's because many are held by hot hands, known as "flippers", and don't have a broad institutional shareholder base.

Many of the recent ones don't make money and are based on an, as yet, unproven business model. These are the ones that take the biggest hits.

Individual IPO stocks can be tough to follow to sell short. But one ETF has done the heavy lifting for you. This is the Renaissance IPO ETF (click here for the prospectus).

Buying Momentum

This is another mathematical creation based on the number of rising days over falling days. Rising markets bring increasing momentum, while falling markets produce falling momentum.

So selling short momentum produces additional protection during the early stages of a bear market. Blackrock has issued a tailor made ETF to capture just this kind of move through its iShares MSCI Momentum Factor ETF (MTUM). To learn more, please read the prospectus by clicking here.

Buying Beta

Beta, or the magnitude of share price movements, also declines in down markets. So selling short beta provides yet another form of indirect insurance. The PowerShares S&P 500 High Beta Portfolio ETF (SPHB) is another niche product that captures this relationship.

The Index is compiled, maintained and calculated by Standard & Poor's and consists of the 100 stocks from the (SPX) with the highest sensitivity to market movements, or beta, over the past 12 months.

The Fund and the Index are rebalanced and reconstituted quarterly in February, May, August and November. To learn more, read the prospectus by clicking here.

Buying Bearish Hedge Funds

Another subsector that does well in plunging markets are publicly listed bearish hedge funds. There are a couple of these that are publicly listed and have already started to move.

One is the Advisor Shares Active Bear ETF (HDGE) (click here for the prospectus). Keep in mind that this is an actively managed fund, not an index or mathematical relationship, so the volatility could be large.

Oops, Forgot to Hedge

00DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2018-02-09 01:06:362018-02-09 01:06:36Short Selling School 101

This is the most important research piece you will ever read, bar none. But you have to finish it to understand why. So, I will get on with the show.

I have been hammering away at my followers at investment conferences, webinars, and strategy luncheons this year about one recurring theme. Things are good, and about to get better, a whole lot better.

The driver will be the exploding rate of technological innovation in electronics, biotechnology, and energy. The 2020s are shaping up to be another roaring twenties, and asset prices are going to go through the roof.

To flesh out some hard numbers about growth rates that are realistically possible and which industries will be the leaders, I hooked up with my old friend, Ray Kurzweil, one of the most brilliant minds in computer science.

Ray is currently a director of Engineering at Alphabet (GOOG), heading up a team that is developing stronger artificial intelligence. He is an MIT grad, with a double major in computer science and creative writing. He was the principal inventor of the CCD flatbed scanner, first text-to-speech synthesizer, and the commercially marketed large-vocabulary speech recognition.

When he was still a teenager, Ray was personally awarded a science prize by President Lyndon Johnson. He has received 20 honorary doctorates and has authored 7 books. It was upon Ray?s shoulders that many of today?s technological miracles were built.

His most profound book to date, The Singularity Is Near: When Humans Transcend Biology, was a New York Times best seller. In it he makes hundreds of predictions about the next 100 years that will make you fall out of your chair.

I met Ray at one of my favorite San Francisco restaurants, Morton?s on Sutter Street. I ordered a dozen oysters, a filet mignon wrapped in bacon, and washed it all down with a fine bottle of Duckhorn Merlot. Ray had a wedge salad with no dressing, a giant handful of nutritional supplements, and a bottle of water. That?s Ray, one cheap date.

The Future of Man

A singularity is defined as a single event that has monumental consequences. Astrophysicists refer to the big bang and black holes in this way. Ray?s singularity has humans and machines merging to become single entities, partially by 2040 and completely by 2100.

All of our thought processes will include built in links to the cloud, making humans super smart. Skin that absorbs energy from the sun will eliminate the need to eat. Nanobots will replace blood cells, which are far more efficient at moving oxygen. A revolution in biotechnology will enable us to eliminate all medical causes of death.

Most organs can now be partially or completely replaced. Eventually they all will become renewable by taking one of your existing cells and cloning it into a completely new organ. We will become much more like machines, and machines will become more like us.

The first industrial revolution extended the reach of our bodies, and the second is extending the reach of our minds.

And, oh yes, prostitution will be legalized and move completely online. Sound like a turn off? How about virtually doing it with you favorite movie star? Your favorite investment advisor? Yikes!

Ironically, one of the great accelerants towards this singularity has been the war in Iraq. More than 50,000 young men and women came home missing arms and legs (in Vietnam these were all fatalities, thanks to the absence of modern carbon fiber body armor).

Generous government research budgets have delivered huge advances in titanium artificial limbs and the ability to control them with only our thoughts. Quadriplegics can now hit computer keystrokes merely by thinking about them.

Kurzweil argues that exponentially growing information technology is encompassing more and more things that we care about, like health care and medicine. Reprogramming of biology will be the next big thing and is a crucial part of his ?singularity.?

Our bodies are governed by obsolete genetic programs that evolved in a bygone era. For example, over millions of years our bodies developed genes to store fat cells to protect against a poor hunting season the following year. That gave us a great evolutionary advantage 10,000 years ago. But it is not so great now, with obesity becoming the country?s number one health problem.

We would love to turn off these genes through reprogramming, confident that the hunting at the supermarket next year will be good. We can do this in mice now, which in experiments can eat like crazy, but never gain weight.

The happy rodents enjoy the full benefits of no caloric restriction, with no hint of diabetes or heart disease. A product like this would be revolutionary, not just for us, health care providers, and the government, but, ironically, for fast food restaurants as well.

Within the last five years, we have learned how to reprogram stem cells to rebuild the hearts of people who have suffered heart attacks. The stem cells are harvested from skin cells, not human embryos, consequently circumventing the political and religious issues of the past.

If we can turn off genes, why not the ones in cancer cells that enable them to pursue unlimited reproduction, until they kill its host? That development would cure all cancers, and is probably only a decade away.

The Future of Computing

If this all sounds like science fiction, you?d be right. But Ray points out that humans have chronically underestimated the rate of technological innovation.

This is because humans evolved to become linear thinking animals. If a million years ago we saw a gazelle running from left to right, our brains calculated that one second later it would progress ten feet further to the right. That?s where we threw the spear. This gave us a huge advantage over other animals and is why we became the dominant species.

However, much of science, technology, and innovation grows at an exponential rate, and consequently is the reason we make our most egregious forecasting errors. Count to seven, and you get to seven. However, double something seven times and you get to a billion.

The history of the progress of communications is a good example of an exponential effect. Spoken language took hundreds of thousands of year to develop. Written language emerged in thousands of years, books in a 100 years, the telegraph in a century, and telephones 50 years later.

Some ten years after Steve Jobs brought out his Apple II personal computer, the growth of the Internet went hyperbolic. Within three years of the iPhone launch, social media exploded out of nowhere.

At? the beginning of the 20th century, $1,000 bought 10 X -5th power worth of calculations per second in our primitive adding machines. A hundred years later a grand got you 10 X 8th power calculations, a 10 trillion-fold improvement. The present century will see gains many times this.

The iPhone itself is several thousand times smaller, a million times cheaper, and billions of times more powerful than computers of 40 years ago. That increases price per performance by the trillions. More dramatic improvements will accelerate from here.

Moore?s law is another example of how fast this process works. Intel (INTC) founder Gordon Moore published a paper in 1965 predicting a doubling of the number of transistors on a printed circuit board every two years. Since electrons had shorter distances to travel, speeds would double as well.

Moore thought that theoretical limits imposed by the laws of physics would bring this doubling trend to an end by 2018, when the gates became too small for the electrons to pass through. For decades I have read research reports predicting that this immutable deadline would bring an end to innovation and technological growth, resulting in economic Armageddon.

Ray argues that nothing could be further fr

om the truth. A paradigm shift will simply allow us to leapfrog conventional silicon based semiconductor technologies and move on to bigger and better things. We did this when we jumped from vacuum tubes to transistors in 1949, and again in 1959, when Texas Instruments (TXN) invented the first integrated circuit.

Paradigm shifts occurred every ten years in the past century, every five years in the last decade, and will occur every couple of years in the 2020s. So fasten your seat belts!

Nanotechnology has already allowed manufacturers to extend the 2018 Moore?s Law limit to 2022. On the drawing board are much more advanced computing technologies, including calcium based systems, using the alternating direction of spinning electrons and nanotubes.

Perhaps the most promising is DNA based computing, a high research priority at IBM and several other major firms. I earned my own 15 minutes of fame in the scientific world 40 years ago as a member of the first team ever to sequence a piece of DNA which is why Ray knows who I am.

Deoxyribonucleic Acid (DNA) makes up the genes that contain the programming which makes us who we are. It is a fantastically efficient means of storing and transmitting information. And it is found in every single cell in our bodies, all 10 trillion of them.

The great thing about DNA is that it replicates itself. Just throw it some sugar. That eliminates the cost of building the giant $2 billion silicon based chip fabrication plants of today.

The entire human genome is a sequential binary code containing only 800 MB of information which, after you eliminate redundancies, has a mere 30-100 MB of useful information which is about the size of an off-the-shelf software program, like Word for Windows. Unwind a single DNA molecule, and it is only six feet long.

What this means is that, just when many believe that our computer power is peaking, it is in fact launching on an era of exponential growth. Super computers surpassed human brain computational ability in 2012, computing about 10 to the 16th power (ten quadrillion) calculations per second.

That power will be available on a low-end laptop by 2020. By 2050, this prospective single laptop will have the same computing power as the entire human race which is comprised of about 9 billion individuals. It will also be small enough to implant in our brains.

The Future of the Economy

Ray is not really that interested in financial markets or, for that matter, making money. Where technology will be in a half century and how to get us there are what get his juices flowing. However, I did manage to tease a few mind-boggling thoughts from him.

At the current rate of change, the 21st century will see 200 times the technological progress that we saw in the 20th century. Shouldn?t corporate profits and, therefore, share prices rise by as much?

Technology is rapidly increasing its share of the economy, and increasing its influence on other sectors. That?s why tech has been everyone?s favorite sector for the past 30 years, and will remain so for the foreseeable future. For two centuries, technology has been eliminating jobs at the bottom of the economy and creating new ones at the top.

Stock analysts and investors make a fatal error estimating future earnings based on the linear trends of the past, instead of the exceptional growth that will occur in the future.

In the last century, the Dow appreciated from 100 to 10,000, an increase of 100 times. If we grow at that rate in this century, the Dow should increase by 10,000% to 1 million by 2100. But so far, we are up only 8%, even though we are already 16 years into the new century.

The index is seriously lagging, but will play catch up in a major way during the 2020s, when economic growth jumps from 2% to 4% or more, thanks to the effects of massively accelerating technological change.

Some 100 years ago, one third of jobs were in farming, one third were in manufacturing, and one third in services. If you predicted then that in a century farming and manufacturing would each be 3% of total employment and that something else unknown would come along for the rest of us, people would have been horrified. But that?s exactly what's happened.

Solar energy use is also on an exponential path. It is now 1% of the world?s supply, but is only seven doublings away from becoming 100%. Then we will consume only one 10,000th of the sunlight hitting the earth. Geothermal energy offers the same opportunities.

We are only running out of energy if you limit yourself to 19th century methods. Energy costs will plummet. Eventually, energy will be essentially free when compared to today?s costs, further boosting corporate profits.

Hyper growth in technology means that we will be battling with deflation for the rest of the century, as the cost of production and the price of everything falls off a cliff. That makes our 10-year Treasury bonds a steal at a generous 2.60% yield, a full 460 basis points over the real long term inflation rate of negative 2% a year.

The upshot to all of this, these technologies will rapidly eliminate poverty, not just in the US, but around the world. Each industry will need to continuously reinvent its business model or it will disappear.

The takeaway for investors is that stocks, as well as other asset prices, are currently wildly undervalued given their spectacular future earnings potential. It also makes the Dow target of 1 million by 2100 absurdly low, and off by a factor of 10 or even 100. Will we be donning our ?Dow 100 Million? hats then?

Other Random Thoughts

As we ordered dessert, Ray launched into another stream of random thoughts. I asked for Morton?s exquisite double chocolate mousse. Ray had another handful of supplements. Yep, Mr. Cheap Date.

The number of college students has grown from 50,000 to 12 million since 1870s. A kid in Africa with a cell phone has more access to information than the president of the United States did 15 years ago.

The great superpower, the Soviet Union, was wiped out by a few fax machines distributing information in 1991.

Company offices will become entirely virtual by 2025.

Cows are very inefficient at producing meat. In the near future, cloned muscle tissue will be produced in factories, disease free, and at a fraction of the present cost, without the participation of the animal. PETA will be thrilled.

Use of nano materials to build ultra light, but ultra strong, cars will cut fuel consumption dramatically. Battery efficiencies will improve by 10 to 100 times. Imagine powering a Tesla Model S1 with a 10-pound battery! Advances in nanotube construction mean the weight of the vehicle will drop from the present 3 tons to just 100 pounds but will be far safer.

Ray is also on a scientific advisory panel for the US Army. Uncertain about my own security clearance, he was reluctant to go into detail. Suffice it to say that the weight of an M1 Abrams main battle tank will shrink from 70 tons to 1 ton, but will be 100 times stronger.

A zero tolerance policy towards biotechnology by the environmental movement exposes their intellectual and moral bankruptcy. Opposing a technology with so many positive benefits for humankind and the environment will inevitably alienate them from the media and the public who will see the insanity of their position.

Artificial intelligence is already far more prevalent than you understand. The advent of strong artificial intelligence will be the most significant development of this century. You can?t buy a book from Amazon, withdraw money from your bank, or book a flight, without relying on AI.

Ray finished up by saying that by 2100, humans will have the choice of living in a biological or, in a totally virtual, online form. In the end, we will all just be files.

Personally, I prefer the former, as the best th

ings in life are biological and free!

I walked over to the valet parking, stunned and disoriented by the mother load of insight I had just obtained, and it wasn?t just the merlot talking either! Imagine what they talk about at Alphabet all day.

To buy The Singularity Is Near at Amazon, please click here. It is worth purchasing the book just to read Ray?s single chapter on the future of the economy.

Did You Say ?BUY? or ?SELL?

The Future is Closer than You Think

https://www.madhedgefundtrader.com/wp-content/uploads/2014/05/Borg.jpg343442Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-12-27 01:06:452016-12-27 01:06:45Peeking into the Future with Ray Kurzweil

There is no doubt that old tech is back with a vengeance.

Look at the trifecta of blockbuster earnings reports from Microsoft (MSFT), Amazon (AMZN), and Alphabet (GOOGL) recently, and you can reach no other conclusion.

The Microsoft turnaround in particular has been amazing.

PCs, and the software to run them were so 1990s.

After the Dotcom bust in 2000, Microsoft was dead money for years.

Founder Bill Gates retired in 2008. CEO Steve Ballmer finally got the message in 2013, and retired to pay through the nose, some $2 billion, for the basketball team, the LA Clippers.

Succeeding operating systems offered little that was new, and they fell woefully behind the technology curve.

Even I gave away my own machines years ago to switch to Apple devices. These virus immune machines are perfect for a small business like mine, as they seamlessly integrate and all talk to each other.

When the company brought out the Windows Phone in 2010, three years after Apple, people in Silicon Valley laughed.

Long given up for dead as a trading and investment vehicle, the shares have been on a tear in 2015.

The stock is hitting a new all time high FOR THE FIRST TIME IN 15 YEARS!

Satya Nadella, who took over management of the company in 2014, clearly had other ideas. The challenge for Nadella from day one was to move boldly into new technologies, while preserving its legacy Windows business lines.

So far, so good.

The key to the company?s new found success was it?s dumping of its old ?Wintel? strategy of yore that focused entirely on the growth of the PC market.

The problem was that the PC market stopped growing, as the world moved onto the Cloud and mobile.

The company is now rivaling Apple with $100 billion in cash, almost all held tax-free overseas.

EPS growth will reach 10% next year, beating other big competitors.

Windows and servers, the (MSFT)?s core products, still account for 80% of the firm?s business.

But its cloud presence is being ramped up at a frenetic pace, where the future for the company lies, nearly doubling YOY. Mobile technologies, where it has lagged until now, are also on fire.

Rave reviews from its latest operating system upgrade, Windows 10, also helped.

On top of all of this, Microsoft is paying a generous 3% dividend. It?s earnings multiple at 15X makes it a bargain compared to other big tech companies and the rest of the market.

As I explained in my recent research piece ?Switching From Growth to Value? (click here?), Microsoft makes a perfect investment for a mature bull market.

It is not only at a multiple discount to the rest of the market, now at 18X, it is cheap when compared to the rest of its own sector as well.

This is when investors and traders bail from their high priced stocks to safer, lower multiple companies.

Obviously, I don?t want to pile into Microsoft, or any other of the big tech stocks on top of a furious 10% spike. But it is now safely in the ?buy on the dip? camp, along with the rest of big tech.

The party has only just stated.

To read my interview with Bill Gates? father, click here for ?An Evening With Bill Gates, Sr.?.

https://www.madhedgefundtrader.com/wp-content/uploads/2015/10/Microsoft-Logo-e1445631099676.jpg92400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-09-23 01:07:492016-09-23 01:07:49Old Tech is Back!

I first spoke to Steve Wozniak via HAM radio when I was 12 and he was the 14-year-old president of the Homestead High School Radio Club in Cupertino, California.

With seven children, my dad was pretty stingy with allowance money. But when it came to electronic parts, I had an unlimited budget, as that is where he saw the future.

So while other kids collected baseball cards, I stocked up on tubes, resistors, capacitors, and rheostats. This was back when you could buy WWII surplus parts from Radio Shack for pennies a pound.

Then the transistor came out, and building projects, like simple computers programmed with basic '1's' and '0's' suddenly became possible.

By junior high school, I had gained my radio license, learning Morse code at the required five words per minute, and a path opened that eventually led me to Woz.

Whenever I had a design problem, Woz always had a solution. He seemed to know everything about electronics.

I planned to attend De Anza College in the San Francisco Bay Area to collaborate with Woz, but then the State of California dropped a big fat scholarship to the University of Southern California in my lap, and we parted ways.

That?s government for you. The state thought I was smarter than Woz. Ha!

The last thing he taught me was this really cool way to make long distance phone calls for free with something called a 'blue box.'

I later heard that Woz went to work for some kind of fruit company designing computers, which sounded stupid to me at the time, but Woz was always a guy who marched to a different drummer.

A decade later, I was an ambitious young vice president at Morgan Stanley, and ran into Woz again while escorting Steve Jobs around to big institutional investors hawking an Apple (AAPL) secondary share offering.

By then he had gained a lot of weight. He fascinated me with stories about how he had gone from scrounging around for a bootleg $12 chip, to making $100 million on the Apple IPO in just three years.

The phrase ?only in America? has to come to mind.

We bought our planes at the same time, me a Cessna 340 twin, and he a Beechcraft Bonanza. When I heard he totaled his in a crash in Santa Cruz a few years later, I sent flowers to his hospital room, even though he was in a coma and wasn't expected to live.

In later years we moved into the same philanthropic circles at the San Francisco Ballet, the Computer Museum, and local art museums. To me, Woz always stood out at the social events as the only one who was not an inveterate social climber.

That was vintage Woz. He just didn't care.

When I finally stumbled across his autobiography, iWoz, I grabbed it and devoured the pages in a couple of days.

The tome filled in the holes about what I knew about the man: the wives, the rock concerts, his universal remote control idea, and the early days at Apple.

You also learn a lot about electronics and basic computer hardware and software design.

While there are a lot of 5th grade science teachers who wish they were billionaires, there is only one billionaire who aspired to teach 5th grade science. That is what Woz did for ten years.

Despite the billions, Steve is still an all right guy. To buy the book of his engaging and entertaining story from Amazon, please click here.

https://www.madhedgefundtrader.com/wp-content/uploads/2013/02/Steve-Wozniak.jpg301382Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-08-02 01:06:322016-08-02 01:06:32Hanging Out With the Woz

Having been in this market for yonks, ages, and even a coon?s age, I have seen trading strategies come and go.

First, there was the nifty fifty during the 1960?s. Junk bonds had their day in the sun. Then portfolio insurance was all the rage.

Oops!

While the dollar was weak, international diversification was the flavor of the day. After foreign stocks turned bitter, the IPO mania and the Dotcom bubble of the nineties followed.

Macro trading dominated the new Millennium until the high frequency traders took over.

What is the cutting edge management strategy today?

According to my friend, Anthony Scaramucci, of Skybridge Capital, activist shareholder trading now has the unfair advantage.

Anthony, known as the ?Mooch? to his friends, is so convinced of the merit of this bold, in-your-face approach that he has devoted nearly 40% of his assets to this aggressive posture.

That is no accident.

Have you ever heard the term ?unintended consequences?? Scaramucci argues that The Financial Stability Act of 2010, otherwise known as Dodd-Frank produced that effect with a turbocharger.

The Act brought in a raft of new shareholder rights intended to help Mom & Pop. But activist investors have, so far, been the prime beneficiaries of the reform, using the new regulations to shake down companies for quick profits.

Historic low interest rates are allowing them to leverage up at minimal cost, increasing their firepower.

These include known sharks (once spurned as ?green mailers?) like my former neighbor, Carl Icahn, and his younger, more agile competitor, Bill Ackman.

They can simply buy a small number of shares in a target company and demand a management change, share buy backs, the spinning off of assets, several seats on the board, and even making allegations of criminal activity, which are often unfounded.

A message from Icahn on the voicemail is not something management is eager to hear.

He even shook down Apple (AAPL) last year, with great success, harvesting a near double on the trade.

This is why names like Herbalife (HLF), Netflix (NFLX), and JC Penny?s (JCP) are constantly bombarding the airwaves.

The net result of this is that savvy activist shareholders have effectively replaced the traditional ?buy and hold? strategy as a way to add alpha, or outperformance.

This has enabled activist oriented hedge funds to beat the pants off of traditional macro hedge funds because many historical cross asset relationships they follow have broken down.

Tell me about it!

Suddenly, the world no longer makes sense to them and has apparently gone mad, at the investors? expense. Long/short equity managers, which comprise 43% of the funds out there, are also underperforming for the sixth consecutive year.

The activist managers themselves justify their often harsh actions by arguing that individual shareholders can ride to riches on their coattails. Shaking up management can result in better-run companies, even if it is at the point of a gun.

Activism accelerates evolution, breaks up clubby boards of insiders, and enhances the bottom line. Corporations can be forced to retool and restructure.

How does the individual investor get involved in the new wave of activist investors? The short answer is that they don?t. There are few, if any, such exchange traded funds (ETFs) in existence.

Doing the quantitative screens to generate short lists of potential activist targets, and then listening to the jungle telegraph regarding who is coming into play, are well beyond the resources of your average Joe.

You can try to give your money to the best activist managers. But they are either closed to new investors, or have very high minimum initial investments, often in the $1-$10 million range.

If you are lucky enough to get your dosh in, you will find the talent very expensive. Activist funds are one of the last redoubts of the old 2%/20% management fee and performance bonus structure. And ?hockey stick? bonus schedules are not unheard of.

When I ran my old hedge fund, we made 40% a year like clockwork. I took the first 10%, the limited partners the remaining 30% and they were thrilled to get it.

And you wonder why the small guys feel the market is rigged.

The activist trend won?t last forever. Interest rates will inevitably rise, making the strategy expensive to finance. If the stock market keeps rising, as I expect, then cheap targets will become as scarce as hen?s teeth.

Eventually, gobs of money will pour into the strategy, compressing returns as the Johnny-come-latelys pile in. In the end, trading around activist shareholders will get tossed into the dustbin of history, along with all the other investment fads.

Checking in With the ?Mooch?

https://www.madhedgefundtrader.com/wp-content/uploads/2014/09/John-Thomas-with-Anthony-Scaramucci.jpg294382Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-07-19 01:07:552016-07-19 01:07:55Why Activist Investors Have the Upper Hand

With the stock market falling for the next few weeks, or even months, it?s time to rehash how to profit from falling markets one more time.

There is nothing worse than closing the barn door after the horses have bolted.

No doubt, you will receive a wealth of short selling and hedging ideas from your other research sources and the media at the next market bottom. That is always how it seems to play out.

So I am going to get you out ahead of the curve, putting you through a refresher course on how to best trade falling markets now, while stock markets are still only 3% short of an all time high, and unchanged on the year.

Market?s could be down 10% by the time this is all over.

THAT IS MY LINE IN THE SAND!

There is nothing worse than fumbling around in the dark looking for the matches after a storm has knocked the power out.

I?m not saying that you should sell short the market right here. But there will come a time when you will need to do so. Watch my Trade Alerts for the best market timing. So here are the best ways to profit from declining stock prices, broken down by security type:

Bear ETFs

Of course the granddaddy of them all is the ProShares Short S&P 500 Fund (SH), a non leveraged bear ETF that is supposed to match the fall in the S&P 500 point for point on the downside. Hence, a 10% decline in the (SPY) is supposed to generate a 10% gain the in the (SH).

In actual practice, it doesn?t work out like that. The ETF has to pay management operating fees and expenses, which can be substantial. After all, nobody works for free.

There is also the ?cost of carry,? whereby owners have to pay the price for borrowing and selling short shares. They are also liable for paying the quarterly dividends for the shares they have borrowed, around 2% a year. And then you have to pay the commissions and spread for buying the ETF.

Still individuals can protect themselves from downside exposure in their core portfolios through buying the (SH) against it (click here for the prospectus: http://www.proshares.com/funds/sh.html). Short selling is not cheap. But it?s better than watching your gains of the last seven years go up in smoke.

My favorite is the (RWM) a short play on the Russell 2000, which falls 1.5X faster than the big cap indexes in bear markets (click here for the prospectus: http://www.proshares.com/funds/rwm.html).

Leveraged Bear ETFs

My favorite is the ProShares Ultra Short S&P 500 (SDS), a 2X leveraged ETF (click here for the? prospectus: http://www.proshares.com/funds/sds.html). A 10% decline in the (SPY) generates a 20% profit, maybe.

Keep in mind that by shorting double the market, you are liable for double the cost of shorting, which can total 5% a year or more. This shows up over time in the tracking error against the underlying index. Therefore, you should date, not marry, this ETF or you might be disappointed.

3X Leveraged Bear ETFs

The 3X bear ETFs, like the UltraPro Short S&P 500 (SPXU), are to be avoided like the plague (click here for the prospectus: http://www.proshares.com/funds/spxu.html).

First, you have to be pretty good to cover the 8% cost of carry embedded in this fund. They also reset the amount of index they are short at the end of each day, creating an enormous tracking error.

Eventually, they all go to zero, and have to be periodically redenominated to keep from doing so. Dealing spreads can be very wide, further added to costs.

Yes, I know the charts can be tempting. Leave these for the professional hedge fund intra day traders they are meant for.

Buying Put Options

For a small amount of capital, you can buy a ton of downside protection. For example, the April (SPY) $182 puts I bought for $4,872 allowed me to sell short $145,600 worth of large cap stocks at $182 (8 X 100 X $6.09).

Go for distant maturities out several months to minimize time decay and damp down daily price volatility. Your market timing better be good with these, because when the market goes against you, put options can go poof, and disappear pretty quickly.

That?s why you read this newsletter.

Selling Call Options

One of the lowest risk ways to coin it in a market heading south is to engage in ?buy writes?. This involves selling short call options against stock you already own, but may not want to sell for tax or other reasons.

If the market goes sideways, or falls, and the options expire worthless, then the average cost of your shares is effectively lowered. If the shares rise substantially they get called away, but at a higher price, so you make more money. Then you just buy them back on the next dip. It is a win-win-win.

I?ll give you a concrete example. Let?s say you own 100 shares of Apple (AAPL), which closed on Friday at $95.13, worth $9,513. If you sell short 1 July, 2016 $100 call at $1.30 against them, you take in $130 in premium income ($1.30 X 100 because one call option contract is exercisable into 100 shares).

If Apple close2 below $100 on the July 15, 2016 expiration date, the options expire worthless and you keep your stock and the premium. You are then free to repeat the strategy for the following month. If (AAPL) closes anywhere above $100 and your shares get called away, you still make money on the trade.

Selling Futures

This is what the pros do, as futures contracts trade on countless exchanges around the world for every conceivable stock index or commodity. It is easy to hedge out all of the risk for an entire portfolio of shares by simply selling short futures contracts for a stock index.

For example, let?s say you have a portfolio of predominantly large cap stocks worth $100,000. If you sell short 1 June, 2016 contract for the S&P 500 against it, you will eliminate most of the potential losses for your portfolio in a falling market.

The margin requirement for one contract is only $5,000. However if you are short the futures and the market rises, then you have a big problem, and the losses can prove ruinous.

But most individuals are not set up to trade futures. The educational, financial, and disclosure requirements are beyond mom and pop investing for their retirement fund.

Most 401ks and IRAs don?t permit the inclusion of futures contracts. Only 25% of the readers of this letter trade the futures market. Regulators do whatever they can to keep the uninitiated and untrained away from this instrument.

That said, get the futures markets right, and it is the quickest way to make a fortune, if your market direc

tion is correct.

Buying Volatility

Volatility (VIX) is a mathematical construct derived from how much the S&P 500 moves over the next 30 days. You can gain exposure to it through buying the iPath S&P 500 VIX Short Term Futures ETN (VXX), or buying call and put options on the (VIX) itself.

If markets fall, volatility rises, and if markets rise, then volatility falls. You can therefore protect a stock portfolio from losses through buying the (VIX).

I have written endlessly about the (VIX) and its implications over the years. For my latest in-depth piece with all the bells and whistles, please read ?Buy Flood Insurance With the (VXX)? by clicking here.

Selling Short IPO?s

Another way to make money in a down market is to sell short recent initial public offerings. These tend to go down much faster than the main market. That?s because many are held by hot hands, known as ?flippers,? and don?t have a broad institutional shareholder base.

Many of the recent ones don?t make money and are based on an, as yet, unproven business model. These are the ones that take the biggest hits.

This is another mathematical creation based on the number of rising days over falling days. Rising markets bring increasing momentum, while falling markets produce falling momentum.

So selling short momentum produces additional protection during the early stages of a bear market. Blackrock has issued a tailor made ETF to capture just this kind of move through its iShares MSCI Momentum Factor ETF (MTUM). To learn more, please read the prospectus by clicking here: https://www.ishares.com/us/products/251614/MTUM.

Buying Beta

Beta, or the magnitude of share price movements, also declines in down markets. So selling short beta provides yet another form of indirect insurance. The PowerShares S&P 500 High Beta Portfolio ETF (SPHB) is another niche product that captures this relationship.

The Index is compiled, maintained and calculated by Standard & Poor's and consists of the 100 stocks from the (SPX) with the highest sensitivity to market movements, or beta, over the past 12 months.

Another subsector that does well in plunging markets are publicly listed bearish hedge funds. There are a couple of these that are publicly listed and have already started to move.

One is the Advisor Shares Active Bear ETF (HDGE) (click here for the prospectus: http://www.advisorshares.com/fund/hdge). Keep in mind that this is an actively managed fund, not an index or mathematical relationship, so the volatility could be large.

Oops, Forgot to Hedge

https://www.madhedgefundtrader.com/wp-content/uploads/2014/04/Wile-E.-Coyote-TNT.jpg365496Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-05-23 01:06:362016-05-23 01:06:36Short Selling School 101

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.

3X Leveraged Bear ETFs

3X Leveraged Bear ETFs