Global Market Comments

September 2, 2024

Fiat Lux

Featured Trade:

( AUGUST 28 BIWEEKLY STRATEGY WEBINAR Q&A),

(SMCI), (QQQ), (CRWD), (NVDA), (TSLA), (GOLD), (BRK/B), (BAC), (AAPL)

Global Market Comments

September 2, 2024

Fiat Lux

Featured Trade:

( AUGUST 28 BIWEEKLY STRATEGY WEBINAR Q&A),

(SMCI), (QQQ), (CRWD), (NVDA), (TSLA), (GOLD), (BRK/B), (BAC), (AAPL)

Below please find subscribers’ Q&A for the August 28 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Santa Barbara, CA.

Q: What is your opinion on Supermicro (SMCI)?

A: I can tell you that all fund managers have the same reaction as I do when they hear the words “accounting irregularities” ….run. So, if you haven’t, I would get out. If you’re looking to get in, there’s probably a great opportunity somewhere, but not here. Their product isn’t that high-tech, cooling racks for artificial intelligence servers. But it did have the letters “AI” attached, so it went up 50-fold. But Hindenburg is occasionally right on their research reports, although they’re wildly exaggerated to enhance their short positions. I would stay out of the way on that one for now.

Q: Are there any startup companies worth investing in on the public market right now?

A: No, because new listings are always overhyped. They come in usually double their true value. This happened with Tesla (TSLA)—I think Tesla came out at $32, I waited for the 50% selloff and all the marketing hype to wear off and I bought it at $16, and of course, that's probably about 60 cents now on a split-adjusted basis. So, I don't play the IPO game. If an IPO really is hot, chances are your broker won’t give it to you anyway; he'll give it to his largest clients. That's probably not you. So, I don't get involved in that game, I look at the aftermath. And in hot markets, there is no aftermath, you just watch them go up. The answer to that is a firm no.

Q: Home prices just hit new all-time highs, according to the S&P Case-Shiller. How do the prices keep rising with high interest rates?

A: Because people expect interest rates to fall, and they are doing so dramatically. If you look at all the interest-sensitive sectors which I've been recommending for the last four months, they've all been on fire. So if the cost of your mortgage is about to drop by half, housing prices should double, and we are starting to see that double now.

Q: Should we buy a put on the (QQQ) based on Nvidia (NVDA) earnings?

A: Nobody knows what the Nvidia earnings are going to be, so if you're willing to make a bet on a coin toss, go ahead and do it. I don't make bets on coin tosses. I make bets when there's a 90% chance that I'm going win, and there are no 90% chance trades out there anywhere in any asset class right now. It's better to watch and wait for the next opportunity. If Nvidia sells off 10% on a weak guidance, then I would be in there with both hands buying, because Nvidia is still cheap relative to the rest of the sector and the rest and of the market. And if Nvidia goes up 20%, I might even sell it short. I have shorted Nvidia this year a couple of times this year, and made money both times, so that is the trade. But right here we're in the middle of the next likely range, so no trade there at all.

Q: Will CrowdStrike (CRWD) have a financial liability for the problem it created by crashing the world's travel computers?

A: Yes, and that will no doubt be the subject of litigation for the next 10 years, which I would rather not get involved in.

Q: The tech industry keeps cutting white-collar jobs, and they have been for some time. At which point does this subside, and won’t this crush employment in Silicon Valley?

A: Well, it’s already crushed employment by about 300,000 in Silicon Valley, but artificial intelligence is now starting to soak up those employees, and they certainly are soaking up the office space, which is why the smart money that is now pouring into San Francisco buying up office buildings for pennies on the dollar. They see an employment recovery. In the meantime, buy the Magnificent Seven stocks, because they’re creating profits by cutting the excess staff which they always used to keep.

Q: When you talk about Tesla (TSLA) losing ground in the EV market, do you see the company broadening out its technologies, and growing the company down other avenues?

A: Absolutely, yes. They have a very fast-growing solar panel business, an industrial-scale battery business, and of course, they're basically running the charging network for the entire United States and the entire world. They also have new batteries under development that have the potential to increase car ranges 20 times at zero cost. Elon always has at least a dozen or so other projects underway, many of which he keeps secret. What you have to keep track of is how many of these accrue to Tesla, and how many accrue earnings to his other companies, like SpaceX, Neuralink, and xAI. SpaceX is going gangbusters right now because guess what? They're planning an IPO in the near future and should get a big multiple. xAI just raised $6 billion in a VC round.

Q: How can Nvidia (NVDA) go higher tonight if it disappoints?

A: It won't. It will drop about 10%. I'm just saying you can go higher into next year on 50% earnings growth, but we may have to give back 10%, 20%, or in the case of August 5th, 40% before we can go forward.

Q: Whatever happened to the commercial real estate problem? How is that taken care of so tightly by private capital?

A: It's a play on falling interest rates. A lot of buildings were going for 10 cents on the dollar in Manhattan and in San Francisco, so these guys know bargains, and they're long-term players, and that's how they always make money in that business. I've been watching it for 50 years, and their market timing is excellent.

Q: What will the effects of de-dollarization mean to the long-term health of the stock market?

A: Nothing, because de-dollarization isn't going to happen. It's more or less an internet conspiracy theory. There's no serious move whatsoever to replace the US Dollar, and Bitcoin or crypto in general never got to more than 1% of the total value of US dollars out there, and plus it's had its problems. So I don't think de-dollarization is going to happen in my lifetime.

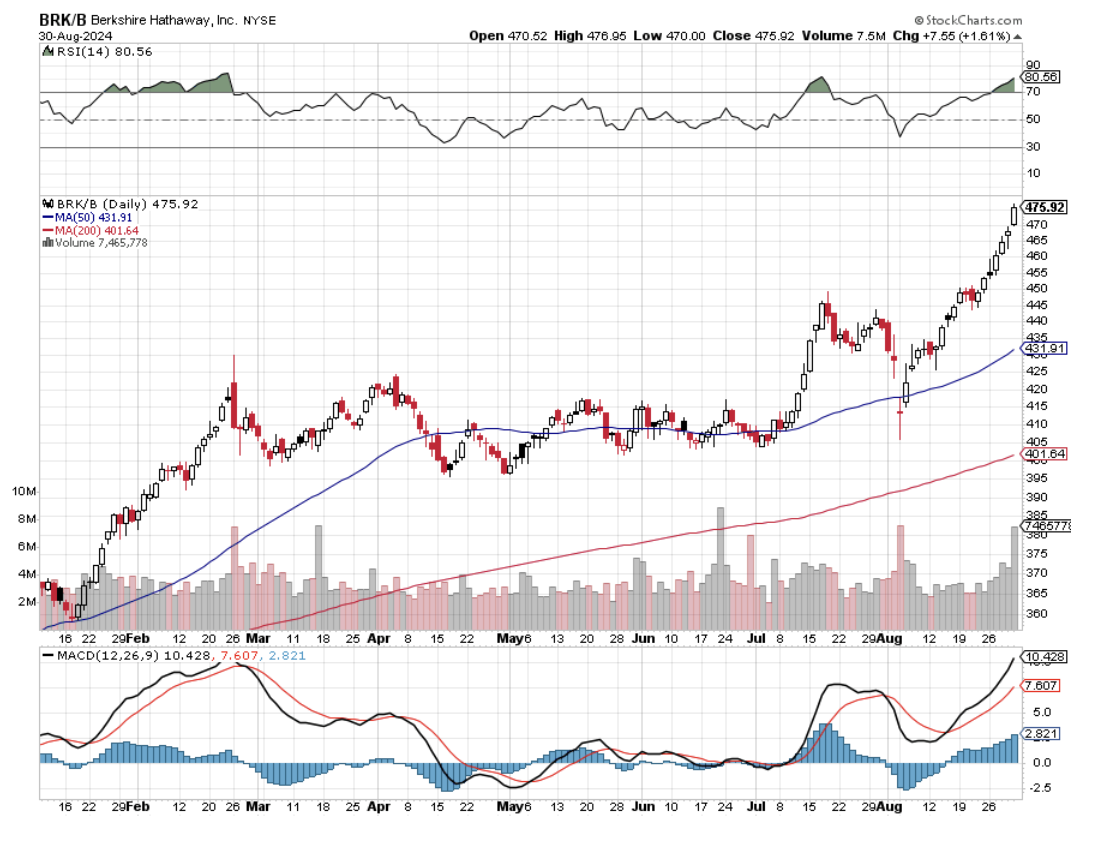

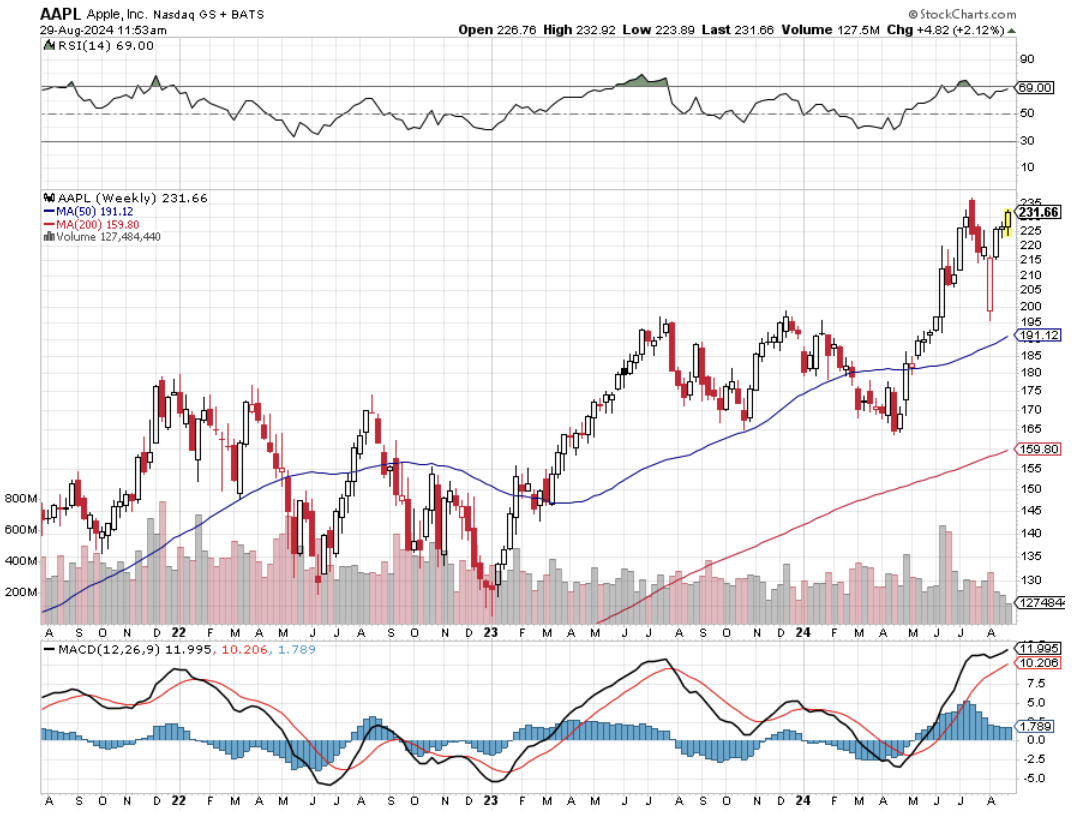

Q: Why is Warren Buffett (BRK/B) unloading shares in Apple (APPL) and Bank of America (BAC)?

A: He thinks the whole market is expensive, and I would agree with him. He likes having a lot of cash during recessions or during major market crashes, so he can swoop in and buy whole companies. So that is the answer. He's thought the market has been expensive for years now, but that doesn't seem to stop them from making money.

Q: Should we take profit on the LEAPS in Barrick Gold (GOLD) expiring in January?

A: Yes, you should take the profit here. You make maybe 20% or 30% and then wait for the next sell-off, and then go back into (GOLD), but add an extra year to the expiration date. Do a 2026 instead of a 2025, because we're getting kind of short on time on all the January 2025 expirations. So that would be the smart thing to do, is to take profits on all your January 25 LEAPS, raise cash, and go back in into an 18-month LEAP on the next sell-off, and I will be reminding you to do exactly that when it happens.

Q: Should we wait until after the election to invest?

A: No. The market will start running before the election, especially if the election outcome becomes more and more certain. So that kind of sets up an October bottom for the market, and maybe even a September one—who knows? We will just have to see how the polls go, even though they are usually wrong. So that's what I would do on that.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, select your subscription (GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or Jacquie's Post), then click on WEBINARS, and all the webinars from the last 12 years are there in all their glory

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

August 29, 2024

Fiat Lux

Featured Trade:

(SEVEN TECH STOCKS TO BUY AT THE ENXT MARKET BOTTOM),

(AMZN), (AAPL), (NFLX), (AMD), (INTC), (TSLA), (GOOG), (META)

Last weekend, I had dinner with one of the oldest and best-performing technology managers in Silicon Valley. We met at a small out-of-the-way restaurant in Oakland near Jack London Square so no one would recognize us. It was blessed with a very wide sidewalk out front and plenty of patio tables.

The service was poor and the food indifferent, as are most dining experiences these days. I ordered via a QR code menu and paid with a touchless Square swipe.

I wanted to glean from my friend the names of the best tech stocks to own for the long term right now, the kind you can pick up and forget about for a decade or more, a “lose behind the radiator” portfolio.

To get this information I had to promise the utmost in confidentiality. If I mentioned his name you would say “Oh my gosh!”

Amazon (AMZN) is now his largest holding, the current leader in cloud computing. Only 5% of the world’s workload is on the cloud presently so we are still in the early innings of a hyper-growth phase there.

By the time you price in all the transportation, labor, and warehousing costs, Amazon breaks even with its online retail business at best. The mistake people make is only focusing on these lowest-of-margin businesses.

It’s everything else that’s so interesting. While its profitability is quite low compared to the other FANG stocks, Amazon has the best growth outlook. For a start, third-party products hosted on the Amazon site, most of what Amazon sells, offer hefty 30% margins.

Amazon Web Services (AWS) has grown from a money loser to a huge earner in just four years. It’s a productivity improvement machine for the world’s cloud infrastructure where they pass all cost increases on to the customer, who once in, buys more services.

Apple (AAPL) is his second holding, the next AI stock. The company is in transition now justifying a massive increase in earnings multiples, from 9X to 25X over the last several years. The iPhone has become an indispensable device for people around the world, and it is the services sold through the phone that are key.

The iPhone is really not a communications device but a selling device, be it for apps, storage, music, or third-party services. The cream on top is that Apple is at the very beginning of an enormous replacement cycle for its installed base of over one billion phones. Moving from up-front sales to a lifetime subscription model will also give it a boost.

Half of these are more than four years old and positively geriatric in the tech world. More than half of these are outside the US. 5G will add a turbocharger.

Netflix (NFLX) is another favorite. The world is moving to “over-the-top” content delivery and Netflix is already spending twice as much on content as any other company in this area. This is why the company won an amazing 21 Emmys this year. This will become a much more profitable company as it grows its subscriber base and amortizes its content costs. Their cash flow is growing by leaps and bounds, which they can use to buy back stock or pay a dividend.

Generally speaking, there is no doubt that the pandemic has pulled forward some future technology demand with the stay-at-home trend. But these companies have delivered normal growth in a hard world. Tech growth will accelerate in 2021 and 2022.

5G will enable better Internet coverage for everyone and will increase the competitiveness of telecom companies. Factory automation will be another big area for 5G, as it is reliable and secure, and can be integrated with artificial intelligence.

Transportation will benefit greatly. Connected self-driving cars will be a big deal, improving safety and the quality of life.

My friend is not as worried about government-threatened breakups as regulation. There will be more restraints on what these companies can do going forward. Europe, which has no big tech companies of its own, views big American tech companies simply as a source of revenue through fines. Driving companies out of business through cutthroat competition is simply not something Europeans believe in.

Google (GOOG) is probably more subject to antitrust proceedings both in Europe and the US. The founders have both retired to pursue philanthropic activities, so you no longer have the old passion (“don’t be evil”).

Both Google and Meta (META) control 70% of the advertising market, which is inherently a slow-growing market, expanding at 5% a year at best. (META)’s growth has slowed dramatically, while it has reversed at (GOOG).

He is a big fan of (AMD), one of his biggest positions, which is undervalued relative to the other chip companies. They out-executed Intel (INTC) over the last five years and should pass it over the next five years.

He has raised the value of tech stocks from 15% to 30% of his portfolio. Apple used to be one of these. Semiconductor companies today also fall into this category. Samsung with 40% margins in its memory business is a good example. Selling for 10X earnings it is ridiculously cheap. It is just a matter of time before semiconductors get rerated too.

He was an early owner of Tesla (TSLA) back in the nail-biting days when it was constantly running out of cash. Now they have the opposite problem, using their easy access to cash through new share issues as a weapon to fight off the other EV startups. Tesla is doing to Detroit what Apple did to the cell phone companies, redefining the car.

Its stock is overvalued now but will become much more profitable than people realize. They also are starting to extract service revenues from their cars, like Apple has. Tesla will grow revenues by 30%-50% a year for the next two or three years. They should sell several million of the new small SUV Model Y. Most other companies bringing EVs will fall on their faces.

EVs are a big factor in climate change, even in China, the world’s biggest polluter. In Europe, they are legislating gasoline cars out of existence. If you can make money building cars in Fremont, CA, you can make a fortune building them in China.

Tech valuations are high, there is no doubt about it. However, interest rates are much lower. The Fed is forcing people to buy stocks, enabling these companies to evolve even faster.

When rates rise in a year or so tech stocks may have to come down. They have a lot more things going for them than against them. The customers keep coming back for more.

Needless to say, the above stocks should make up your shortlist for LEAPS to buy at the coming market bottom.

Global Market Comments

August 22, 2024

Fiat Lux

Featured Trade:

(THE TOP SEVEN CHINESE RETAILIATION TARGETS),

(AAPL), (GM), (WMT), (TGT), (BA), (SBUX), (CAT),

(AND MY PREDICTION IS….)

It’s looking like the trade war between the US and China is going to heat up some more, no matter who wins the presidential election. It is no longer a question of “if”, but “how much” and “when.”

Please forgive me, but I am new at this. I have only been covering China for 50 years now since the Cultural Revolution was sweeping an impoverished, starving third-world communist country.

With a massive US trade deficit with China in 2023, the Middle Kingdom has become a top administration target.

A real trade war would cause thousands of businesses in the US to go bankrupt and leave millions unemployed. Transpacific transportation would ground to a halt, filling up harbors with hundreds of redundant ships.

Trillions of dollars of direct investment in the two countries would be held hostage.

In other words, a trade war would be like cutting off our noses to spite our faces.

Just as America has its Tea Party and right-wing conspiracy theorists, so does China.

Their entire worldview revolves around the merciless exploitation of China by the Western powers that took place during the 19th century.

British trading companies, like Jardine Matheson, imported cheap opium from India and sold it to the Chinese at the point of a gun, triggering three wars. With only primitive weapons at hand, the Chinese were powerless to resist.

By the time of the fall of the Qing Dynasty in 1912, the entire country had been carved up into spheres of influence dominated by the West and Japan.

Then the Japanese invaded in 1937, and 29 million Chinese died. As recently as 1938, my Marine Corps uncle, Colonel Mitchell Paige, was charged with protecting American gunboats cruising the Yangtze River.

To us, this is all ancient history inhabiting dusty textbooks in libraries never visited. Patriotic Chinese feel like this happened yesterday.

You could dismiss all this as academic musings.

But national pride and sovereignty are really big deals in China today.

During China’s last trade war with Japan only five years ago, several Japanese facilities were burned down by angry, uncontrollable mobs, and visiting businessmen were assaulted on the street. Trade ground to a halt.

So it behooves us to analyze which companies will suffer the most from any deterioration in the US-Chinese relationship before markets figure this out. The Chinese are not interested in any “America First” policy in any way, shape, or form.

Here is my hit list:

1) Apple (AAPL) – Yes, Cupertino, CA-based Apple has a big fat bull’s-eye on its back. The company is a vast, finely tuned machine that needs everything to work perfectly to deliver hundreds of millions of iPhones around the world.

The number of things that can go wrong here can’t be counted. What if the one million workers at its Foxconn subcontractor fail to show up for work someday? What if they are not allowed to go to work? What if they burn THAT factory down?

Another problem is that Chinese growth is a key part of Apple’s long-term sales strategy. A Chinese boycott would put a huge dent in those plans.

Remember, Apple is getting it from both sides, with Trump promising a 35% import duty on all Apple products. That would certainly hurt sales.

I’m sure Apple management is on tenterhooks as to how all this will play out in the coming months.

There is no backup plan here. Apple is just too big and too sophisticated to change any part of its incredibly complex supply chain in less than a decade.

2) General Motors (GM) – Is one of the most globalized US companies of all. (GM) can’t build a car in Detroit without 40% of its parts coming from Japan, Mexico, South Korea, or dozens of other countries.

General Motors is also hugely dependent on Chinese sales. It sells more Buicks in China than it does in the US. That is one-third of GM’s total worldwide sales.

Next, the company plans to sell Chinese-made Buicks in America.

While we weren’t looking, General Motors has become a Chinese company, and many others are falling suit.

3) Wal-Mart (WMT) – Imagine walking into your local Walmart one day and finding out that all of the prices have been marked up by 35%.

This is the reason why the company is called the “Chinese Embassy.” I dare you to find anything there that is NOT made in China, except for the food and the flowers (a dozen long stem red roses are only $10!).

Like Apple, the company is so big that any change in its supply chain would take years. You can add Target (TGT) to this hit list for the same reasons.

On top of that, Wal-Mart has 432 stores operating in China. Imagine the effect that a boycott would have there.

4) Boeing (BA) - The local flight school that maintains my plane has been totally taken over by Chinese students. That is because China needs to buy $1 trillion worth of aircraft over the next 20 years, some 6,800 jetliners in all.

Boeing expects to provide the lion’s share of these. The company has already entered the planning phases for the construction of a giant new aircraft assembly plant in China.

It would be really easy for China to switch a major part of these orders over to Europe’s Airbus Industries, which has been aggressively competing to accomplish exactly that.

Boeing didn’t get the business because of the advanced technology seen in the 787 Dreamliner. Chinese were simply attempting to even out the trade balance.

5) Starbucks (STBX) – Starbucks founder Howard Schultz made no secret of his dislike for Donald Trump before the election. With 2,500 stores in China, and plans to double that figure, he had little other choice.

With relations between the US and China turning colder than the firm’s overpriced ice espresso, sales, growth plans, and share prices could take a big hit. Chinese may have to postpone their caffeine addiction until the next Democratic administration.

6) Caterpillar (CAT) – You can’t have an infrastructure boom anywhere in the world without Caterpillar, whose heavy machinery is the gold standard for large public works projects. I have been covering the company for 40 years.

7) Tesla (TSLA) – Tesla’s factory in China is the company’s biggest seller. If the Chinese expropriate or impede in any way such as through strikes, Tesla’s share price would drop by half instantly. I know the Chinese promised to play nice when Tesla made this groundbreaking, technology-transferring investment. But guess what Elon? The Chinese can change their minds.

As a result of the upcoming US round of massive deficit spending, (CAT)’s share has been one of the best performers since the presidential election.

Unfortunately, this time the company is so heavily invested in China that it has also built a large assembly plant there. China accounts for 20% of the firm’s worldwide sales.

Time for a short?

The net effect on the impairment of business at all of these companies will be lower profits, high volatility of profits, and continued uncertainty. The shares will be forced to trade at a discount.

When you are running a mammoth global business, the last thing in the world you want is unpredictability.

It will also bring a rapid rise in inflation, as prices are raised to offset higher costs and a strong dollar.

Who will be the biggest victims?

Working-class Trump voters in Rust Belt states, least able to afford price hikes, especially those who already have jobs in Midwest manufacturing.

Global Market Comments

August 19, 2024

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD or LESSONS LEARNED) plus (GLIDING INTO LITHUANIA),

(SPY), (GLD), (DHI), (TSLA), (JPM), (AAPL), (DHI), (LRCX)

After the worst week of the year, we get the best. If you are confused by all of this, so am I.

On the one hand, the downside was firmly rejected by the $8 trillion sitting under the market that has been trying unsuccessfully to get into the market all year. The upside was rejected as well and who knows why? Did it run too far, too fast? Did valuations get overblown? Or was it simply time to take a summer vacation?

Who knows? All three were true.

I don’t really care. I am up 2.67% in August and am 100% in cash. I’m waiting for the market to tell me what to do next. If we get another crash, I’ll buy. I’m selling the next melt-up as well. The only thing I’m really confident in is my 6,000 target for the S&P 500 by year-end which appears right on schedule.

London certainly has become the most internationally diverse city in the world. Last week my tablemates in pubs included two women from Japan who nearly fell out of their chairs when they heard me speak Japanese. A business consultant from Milan was visiting London for the first time. The head of international marketing for Industrial Light & Magic from Mill Valley, CA, filled me in on the latest developments in the digital arts.

Two Arabic-speaking ladies from Oxford University were working for a charity getting food into Gaza. One bartender was headed for Sandhurst, England’s West Point. The other was from China, and I had to explain to him what Bushmills was (it’s an Irish whiskey). Oh, and my barber was from Syria and my cleaning lady was from Barbados.

All seven of my languages were given a thorough workout. There are 56 countries in the British Commonwealth, and it seems like all of them are here at once.

This summer’s crash down, then up offered many lessons and I want to make sure you catch them all. Let every loss be a learning experience, lest you be doomed to repeat it. Of the 20 great single-day losses in the S&P 500 (SPX) since 1923, I have traded through nine. The other 11 took place in the aftermath of the 1929 crash where the market eventually dropped by 90%. But I had many friends who traded all of those. Click here for details.

For a start, it helps a lot if you see a crash coming. This market had been begging for a crash during May and June and I positioned accordingly. I went into the meltdown with nine short positions in July-August, which covered most of my losses. And I only ran positions into very short August 16 option expiration, thus greatly limiting damage incurred by the losers.

I limited losses by stopping out of out-of-the-money losers quickly in (CAT), (BRK/B), and (AMZN), right at the August 5 opening in most cases. I then became super aggressive when the Volatility Index ($VIX) hit $65, a 2-year high. I also went hyper-conservative by adding four technology positions very deep 20% in-the-money in (NVDA), (META), (TSLA), and (MSFT), which instantly became money makers.

I used the first 1,000-point rally to add a short position for a very long, thus neutralizing the portfolio at the middle of the recent range and taking in a lot of extra income.

I did ALL of this while traveling in England, Switzerland, Lithuania, Poland, Austria, and Slovakia, from assorted airport business lounges, hotels, and Airbnb’s. The travel actually helped because the New York market doesn’t open until 3:30 PM each day, giving me plenty of time to plan the day’s strategy.

Now all we have to do is figure out what the Volatility Crash ($VIX) from $65 to $14 in 9 days means, the fastest in history by a huge margin. It usually takes 170 days to make this kind of move. Could it mean that our lives are about to become boring beyond tears once again?

I doubt it.

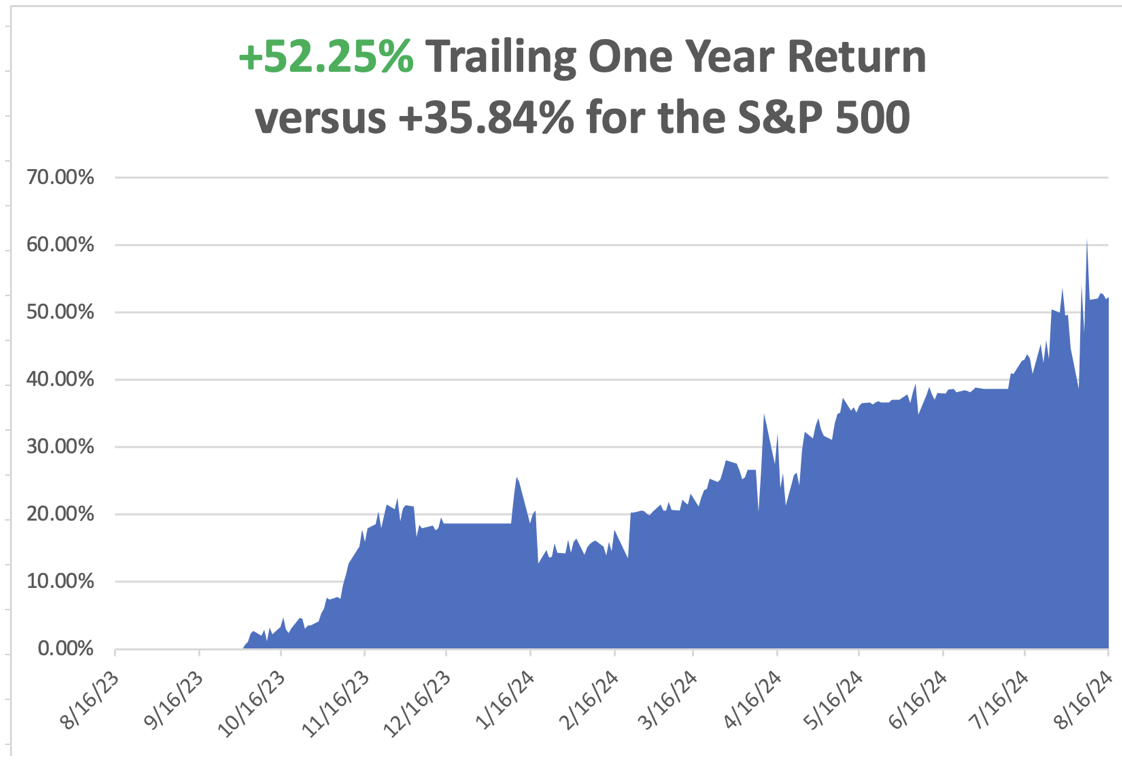

In July we ended up a stratospheric +10.92%. So far in August, we are up by +2.67%. My 2024 year-to-date performance is at +33.61%. The S&P 500 (SPY) is up +16.14% so far in 2024. My trailing one-year return reached +52.25.

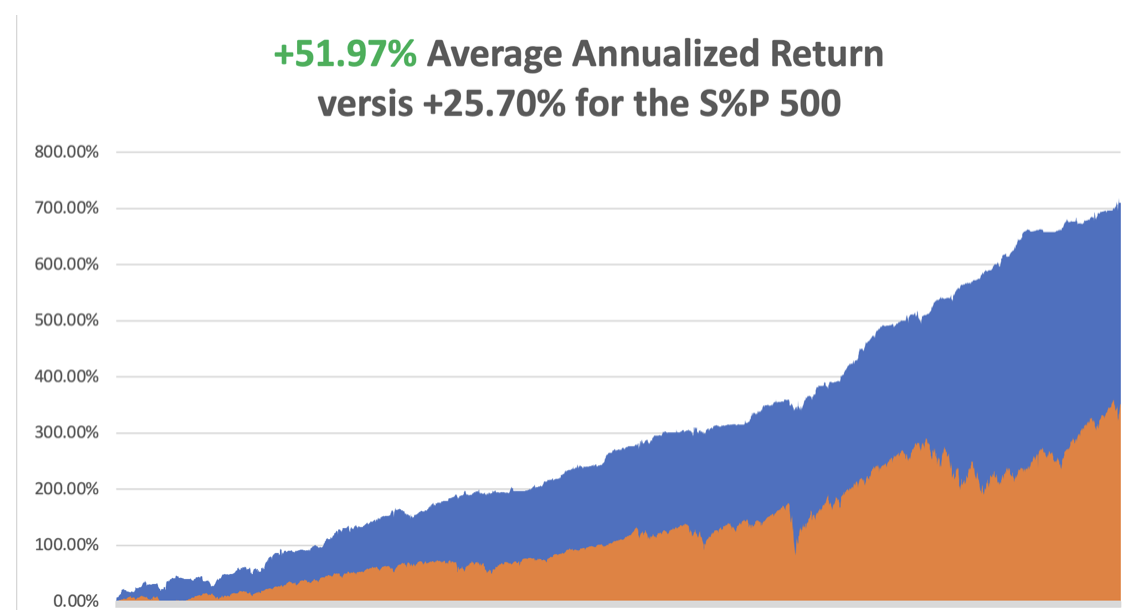

That brings my 16-year total return to +710.24. My average annualized return has recovered to +51.97%.

I spent the entire week taking profits. I cashed in on my longs in (GLD) and (DHI) and covered shorts in (TSLA), (JPM), (AAPL), and (DHI). I am now 100% in cash and boy does it feel good.

Some 63 of my 70 round trips, or 90%, were profitable in 2023. Some 49 of 66 trades have been profitable so far in 2024, and several of those losses were really break-even. That is a success rate of 74.24%.

Try beating that anywhere.

The “Soft Landing” is Back, or so says Goldman Sachs after the meteoric rise in share prices of the last ten days. The extreme concerns about the U.S. economy that have re-emerged over the past month appear overblown and investors shouldn’t get too defensive. The recent spike of market volatility had more to do with positioning than a real scare about economic growth and that investors should “keep the faith” that the U.S. avoids a recession, while also avoiding a revival in inflation.

Now it’s Volatility That’s Crashing, down a record 49 points from $65 to $16 in 9 trading days, suggesting that investors may be returning to strategies that bank on low stock volatility despite a near-meltdown in equities early this month. The ($VIX) long-term median level is $17.6. Similar reversions in the so-called fear gauge have, on average, taken 170 sessions to play out.

Consumer Price Index is a Snore, at 0.2% MOM and 2.9% YOY, below the long-term average. Ebbing inflation aligns with anecdotes from businesses that consumers are pushing back against high prices, through bargain hunting, cutting back on purchases, and trading down to lower-priced substitutes. Stock was a snore as well.

Consumer Sentiment Drops, to an eight-month low according to the University of Michigan. It was revised higher to 66.4 in July 2024 from a preliminary reading of 66.

The Yen Carry Trade is Back, with hedge funds piling back into positions they baled on only two weeks ago. It’s just a matter of math, now that the Bank of Japan has given up on raising interest rates anytime soon. What this means is more leverage, risk, and volatility for global financial markets. I love it!

New Home Construction Dives, in July to the lowest level since the aftermath of the pandemic as builders respond to weak demand that’s keeping inventory levels high. Total housing starts decreased 6.8% to a 1.2 million annualized rate last month, dragged down the biggest decline in single-family units since April 2020

Global EV Sales Jump 21% YOY, in July thanks to a large rise in China. In the European Union MG Motor, owned by China's SAIC Motor Corp, expects to be hit hardest by provisional imposed on EVs imported from China. Europe is not going to give away its core industry, especially Germany’s. EVs - whether fully electric (BEV) or plug-in hybrids (PHEV) - sold worldwide were at 1.35 million in July, of which 0.88 million were in China, where they were up 31% year-on-year.

Refi’s Rocket 35% in a Week, the result of falling inflation and a monster rally in the bond market. The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($766,550 or less) fell slightly to 6.54% from 6.55%. The refinance share of mortgage activity increased to 48.6% of total applications from 41.7% in the previous week

US Producer Price Index Fades, coming in at a weak 0.1%, and giving the interest rate cut crown a high five. Stocks took off like a scalded chimp. Treasury yields fell on Tuesday as wholesale inflation measures came in softer than expected. The yield on the ten-year US Treasury was lower by about 4 basis points at 3.867%.

Foreign Investors Pull Record Amount from China, $15 billion in Q2. Chinese firms invest a record $71 billion overseas at the same time. It’s why the Chinese yuan has been so weak. The glory days are never coming back. Avoid (FXI).

Weekly Jobless Claims totaled 227,000, a decrease of 7,000 from the previous week and lower than the estimate for 235,000.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 600% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, August 19 the Meeting of Central Bankers at Jackson Hole begins. Traders will peruse the tea leaves looking for clues about future interest rates policy. All the major countries of the world have already started cutting rates except the US.

On Tuesday, August 20 nothing of note is released.

On Wednesday, August 21 at 8:30 PM EST, the Minutes from the last FOMC meeting are released.

On Thursday, August 22 at 8:30 AM, the Weekly Jobless Claims are announced.

On Friday, August 16 at 8:30 AM, Federal Reserve Chairman Jay Powell speaks. Also, New Home Sales are disclosed. At 2:00 PM the Baker Hughes Rig Count is printed.

As for me, when a Concierge member invited me to spend a week in Lithuania, I jumped at the chance. I had never been to this miniscule country of 3 million, formerly a part of the Soviet Union. The last time I spent any appreciable amount of time in Eastern Europe was in 1968, at the height of the Cold War.

My friend grew up in the old USSR. He remembers as a child having to go to school in the snow wearing worn-out shoes repaired with duct tape because there weren’t any in the stores.

I remember the old Soviet Union and it was grim beyond belief. Standards of living were sacrificed for military spending in the extreme. I remember I swapped my Levi’s for a worn-out pair plus $50 because they were unobtainable.

My friend cashed in on the collapse of the Soviet Union and the mass privatizations that followed. As a trader in Gazprom shares, he made millions. Now he lives a life of leisure, taking occasional potshots at the market with my assistance. He has been with me since 2011.

Knowing I was an avid pilot he treated me to a day at the local glider club. Introduced as a Top Gun instructor who had flown everything from RAF Spitfires to F-18s, and whose grandfather had worked for Orville Wright, the club pilots were somewhat in awe. I was asked to sign logbooks, which is a great honor among pilots.

I donned my parachute with ease, and everyone relaxed. A tow plane took us up to 2,500 feet, we pulled the release from the cable and suddenly were floating over the endless green forests of Eastern Europe.

I took the stick and performed some light aerobatics, careful not to scare the daylights out of my co-pilot. The thing that really impresses you about gliders is the complete silence. No earplugs inside your headphones here, just the whooshing of the wind. We headed for the nearest clouds in search of uplifting thermals.

I was informed that birds knew more about thermals than any of us, and sure enough, we found a flock and followed them right in. We immediately picked up a few hundred feet, our electronic altimeter whining all the way.

Flying with the birds on a perfect day, how cool is that?

We could have stayed up for hours but I had a lunch appointment. So we yanked on the speed brakes and plummeted down towards the field. At 50 feet, wind shear hit us from the side and we fell like a ton of bricks, bouncing hard. My left elbow smashed against the side of the cockpit inflicting a big gash.

The glider club rushed the aircraft expecting the worst, but I gave them a thumbs up. Any landing you walk away from is a good landing. I later learned that the previous day another pilot broke both legs executing the same maneuver.

When the Soviet Union broke up in 1991, we thought it would take 100 years to integrate the former republics with the West. Although Lithuania is still one of the cheapest countries in Europe, the improvement in the standard of living has been enormous. Old Towns in Europe are usually prime real estate with the most expensive accommodation. Here it’s so cheap that you see a lot of young families with kids in strollers on the sidewalks and in the parks.

They have adopted our vices too, with elaborate tattoos commonplace and teenagers vaping on every street corner.

In the capital city of Vilnius, I developed a work schedule that was tolerable. I spent my mornings walking the Old Town, visiting palaces, castles, baroque churches, museums, and art galleries. Then when the New York Stock Exchange opened up at 4:30 PM I was at my computer banging out my trade alerts as fast as I could write them. The market closed at 11:00 PM. Thank goodness the bars were still open.

Of course, the language is a challenge. Usually, I can understand half of what is going on in Europe. But Lithuanian is a direct descendant of Sanskrit so I couldn’t understand a single word. Everyone under 40 speaks English so I was thankfully able to do my grocery shopping with some assistance.

Every year, I like to return to all my favorite countries, plus add one or two new ones. Where will next year’s new countries be? I’m already scheduled to visit Nicaragua, Columbia, Panama, Costa Rica, and Curacao before yearend. Estonia, Argentina, Latvia, Brazil, Tahiti, who knows?

Ask me in 2025.

To watch a short video of my Lithuanian glider flight, please click here.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

August 14, 2024

Fiat Lux

Featured Trade:

(A REFRESHER COURSE AT SHORT SELLING SCHOOL),

(SH), (SDS), (PSQ), (DOG), (RWM), (SPXU), (AAPL), (TSLA),

(VIX), (VXX), (IPO), (MTUM), (SPHB), (HDGE)

Global Market Comments

August 12, 2024

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD or THE ROUND TRIP TO NOWHERE), plus (A VISIT TO TRINITY),

(ROM), (TQQQ), ($VIX), (TLT), (SLRN), (CAT), (AMZN), and (BRK/B). (NVDA), (TSLA), (AAPL), and (META), ($INDU), (TSLA), (DHI), (DE), (AAPL), (JPM), (DE), (GLD), (DHI)