Mad Hedge Biotech and Healthcare Letter

March 16, 2023

Fiat Lux

Featured Trade:

(WHO’S REALLY THE BOSS?)

(ILMN), (AAPL), (TWX), (MDLZ), (CVX)

Mad Hedge Biotech and Healthcare Letter

March 16, 2023

Fiat Lux

Featured Trade:

(WHO’S REALLY THE BOSS?)

(ILMN), (AAPL), (TWX), (MDLZ), (CVX)

Carl Icahn—the legendary investor known for toppling corporate behemoths and taking charge of their destinies—has swooped in to save Illumina (ILMN) from its own misguided move.

To salvage what’s left of the promising biotechnology company, he has emerged with a plan for shareholders: halt their recent deal with Grail—a cancer-screening firm that Icahn and his faithful followers want nothing more than to see dropped. Part of his plan is to nominate three people to sit on the board of Illumina. The move sent shares of ILMN soaring – no doubt leaving Icahn feeling pretty victorious himself.

For additional background, Icahn isn’t an ordinary businessman and investor. He is the founder, chairman, and majority shareholder of Icahn Enterprises, a diversified conglomerate holding company based in New York City, formerly American Real Estate Partners. He is one of the world's most successful and influential investors, having made billions through his investments in companies such as Apple (AAPL), Time Warner Inc. (TWX), RJR Nabisco (now Mondelez (MDLZ)), and Texaco (CVX). His extensive corporate takeover activities have resulted in him being dubbed "The King of Corporate Raiders."

As an activist investor, he is an individual or a member of a group of investors who uses their financial resources to directly influence the actions and decisions of organizations, often by purchasing shares in the business.

They often demand changes to corporate structure and strategy changes, board composition, and executive compensation practices. Needless to say, activist investors have a significant impact on a company, as they typically target companies that are undervalued and push for changes that can increase their value.

This is an extremely timely announcement for Illumina since the company’s value plummeted from $70 billion in 2021 to $31 billion in 2023. However, the biotech isn’t going down without a fight.

The acquisition of Grail by Illumina was first announced in September 2020, and it has been a subject of discussion and scrutiny since then. The proposed deal involves Illumina buying out the remaining stake in Grail that it does not already own, for a total of $8 billion in cash and stock.

Illumina believes that its plan to acquire Grail is a significant development in the field of genomics and cancer diagnostics. At the moment, Illumina is a leading provider of genomics technology, while Grail is a biotechnology company focused on developing a blood test for early cancer detection.

The acquisition is expected to create significant synergies between the two companies. Illumina's expertise in genomic sequencing technology combined with Grail's cutting-edge liquid biopsy technology could potentially lead to the development of a powerful and efficient cancer detection tool.

The acquisition has, however, faced some challenges, including regulatory hurdles. The Federal Trade Commission (FTC) expressed concerns that the acquisition could lead to Illumina having a monopoly in the market for sequencing machines, which are used in Grail's liquid biopsy tests. As a result, the FTC filed a lawsuit to block the acquisition.

Despite the challenges, Illumina and Grail remain committed to the deal, and in December 2021, they announced that they had reached a settlement with the FTC. The settlement requires Illumina to sell its existing liquid biopsy technology to a third party and abide by certain conditions to prevent any potential anti-competitive effects of the acquisition.

All things considered, it is undeniable that the acquisition of Grail by Illumina has the potential to revolutionize cancer diagnostics and improve patient outcomes. However, the regulatory hurdles demonstrate the importance of ensuring mergers and acquisitions do not harm competition and ultimately negatively impact consumers.

Overall, Illumina is a promising biotech with much room to grow. It pioneered the development of next-generation sequencing (NGS) technology, which revolutionized the field of genomics. NGS allows researchers to sequence large amounts of DNA quickly and at a lower cost than traditional Sanger sequencing methods.

NGS works by breaking the DNA into small fragments and sequencing them simultaneously. These short reads of DNA are then assembled to create a whole genome. Illumina's NGS technology is based on a proprietary sequencing-by-synthesis method, which uses flourescently labeled nucleotides to detect and record the sequence of DNA bases as they are incorporated into a growing DNA chain.

NGS has many applications in genomics research, including identifying genetic mutations, studying gene expression patterns, and characterizing the microbiome. The technology has also played a critical role in advancing precision medicine and personalized healthcare.

Illumina's pioneering work in NGS has allowed the company to establish a dominant market position in the genomics industry and has driven significant innovation in the field of genomics.

Thanks to this biotech’s products, the cost of a complete human genome analysis dropped from the hundreds of millions range in 2001 to less than $1000 today. More notably, the company projects the price to go lower and be below $200 when it releases its new services.

Being hailed as a market leader is a well-deserved description for the company. After all, Illumina quadrupled its revenues in the past 10 years and continues to deliver decent results.

Icahn’s move to take on Illumina offers a fresh and seemingly more promising perspective regarding the company’s direction. He believes Illumina can unlock value by spinning off non-core businesses, returning cash to shareholders, reducing costs, and improving operational efficiency. However, Illumina's management resisted Icahn's calls for a sale and instead focused on investing in research and development to drive growth.

Still, Icahn's targeting of Illumina is likely driven by his belief that the company is undervalued and not maximizing shareholder value. While it will take time before anything gets resolved, what’s apparent is that Illumina doesn’t hold complete freedom when it comes to decision-making, which would inevitably hurt its future success.

Global Market Comments

March 10, 2023

Fiat Lux

Featured Trade:

(THE MAD HEDGE TRADERS & INVESTORS SUMMIT IS ON MARCH 14-16)

(MARCH 8 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (TLT), (UUP), (FXY), (FXB), (FXE), (FXA), (UNG), (BOIL), (AAPL), (TSLA), (WW), (BHP), (NVDA), (RIVN), (FCX)

CLICK HERE to download today's position sheet.

Below please find subscribers’ Q&A for the March 8 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Incline Village, CA.

Q: Do you think the US dollar will drop this year?

A: Absolutely it will drop; in fact, the drop started in October last year. We’re actually six months into a bear market for the US dollar (UUP), and bull market for the yen (FXY), the British pound (FXB), the euro (FXE), and the Australian dollar (FXA). However, the rate-cutting scenario is on vacation, and when it comes back from that vacation, then we will see very sharply dropping interest rates, soaring bond prices, and a weak dollar. That scenario is certain to happen by year-end, probably by 10 or 20% —quite a lot. If you just want to buy the basket for foreign currencies, you can sell short the Invesco DB US Dollar Index Bullish Fund (UUP).

Q: Can stocks (SPY) and bonds (TLT) go up at the same time?

A: Well, they shouldn’t, and usually they don’t. But this time it’s different now because we’re all beholden to the interest rate decisions of the Fed. All asset classes are moving together like synchronized swimmers, which means that on days when the market believes that Powell is finished raising rates, you get big bull moves in stocks, bonds, commodities, precious metals, and beanie baby collectibles. And on the bad days like yesterday, where Powell really reiterates how tough his stance is on inflation is unchanged, everything falls in unison. It’s really become a liquidity/confidence/inflation on-off type market. We have been playing that like a maestro for the last six months and have made a ton of money. I hope it continues that way. “If it’s working, don’t fix it” is my philosophy on trading, which is constantly changing.

Q: Do small caps underperform or overperform in a rising rates era?

A: They always do poorly because small caps have fewer cash reserves, more leverage, and more exposure to interest rates, as opposed to large caps which, in the tech area, don’t borrow at all. They’re actually net creditors to the system so they make more money when interest rates go up. I imagine the interest income at Apple this year has to be absolutely gigantic. That said, small caps always lead recoveries because of their excess leverage, so that's why people are piling into small caps on dips right now. Going from terrible to just bad often generates the best stock returns.

Q: How long will “steering wheel falling off” news tank Tesla?

A: Well, it was worth a $6 dollar drop today in an otherwise weak market. First of all, if there are any actual problems with Tesla, they fix them immediately for free, and most of the fixes can be done with a software upgrade which they do at midnight the day of the recall. Second, a lot of these stories about Tesla problems are false, planted there by the oil industry, trying to head off their own demise. Third, when you go from making several thousand to several million cars a year, scaling up to mass production always uncovers some sort of manufacturing flaws. Tesla can fix them faster than anyone else. I remember when the first Model S came out 13 years ago, we had a hot day and all the sealants on the windows melted. They said they didn’t know because it doesn’t get that hot in Fremont California where they build the cars. They sent out a truck the next day and installed all new sealants on our windows. So that is part of living with Tesla, which seems bent on taking over the world. And I’m working on a major update on Tesla report. I listened to the whole 3.5-hour investors day, and I'll get that out when I get all the snow shoveled. Full disclosure: Elon Musk personally gave me a free $12,800 Tesla Powerwall three years ago. It’s the red one.

Q: I just bought the United States Natural Gas Fund (UNG) 14/15 2025 LEAP for $0.20 with UNG down 3%.

A: I’m going to share that LEAPS with all the Global Trading Dispatch members tomorrow. So far, only the Mad Hedge Concierge members have seen it. We’ll go into great detail in tomorrow’s letter about why you want to buy natural gas here and how you want to play it.

Q: It seems the Fed won’t be happy unless there’s a recession; am I reading this wrong?

A: I think Powell is striving for perfection—killing off inflation and lowering interest rates without a recession. I actually am hoping for a recession myself, even if it’s just for one quarter because that greatly increases market volatility and makes my bond long look like a stroke of genius. And let’s see if he can pull it off. He’s coming facing so many unprecedented challenges to the economy, like the pandemic, the end of liquidity, and the extreme worker shortage. It’ll be really interesting to see what happens. Multiple PhD theses in economics begging to be addressed in there.

Q: Will artificial intelligence cause another bubble?

A: Absolutely, yes. And if you’ve been in the market long enough, you become a bubble collector like me. Just off the top of my head, 3D printing, cold fusion, bitcoin, portfolio insurance, Nifty 50, eyeballs,—if I spent more time, I could come up with an endless list. And this is how Wall Street makes their money—they create bubbles by manufacturing compelling, irresistible stories that can be sold to the masses. Some of these like cold fusion, I know immediately won’t work for 20 years because of my physics background, and definitely not now. Some of these other ones are just flashes in the pan and never work. You just get used to an endless series of bubbles. AI is new only if you haven’t been watching. The share prices of Google, Amazon, Apple, have already had gigantic moves in the last 20 years, largely because of their use of artificial intelligence. So those are your plays—those and (NVDA), which provides the essential chips for artificial intelligence, and we’re active in all of these, both on the long and short side.

Q: Is climate change a hoax or a bubble?

A: If you think it’s a hoax, will you please come over to Incline Village and get the 12 feet of snow off my damn roof before the house collapses. I already can’t close any doors in the house because the weight of the snow is buckling the house and bending the door frames. If you finish the roof, then you can get to work on my deck which also has about 8 ft of snow and is at risk of collapsing, like many in town already have. This has never happened before. The climate has changed.

Q: How come there’s never mention of demographic shift in other parts of the world when there is in the US?

A: The US is the only country in the world where you can earn enough money to retire early. If you live on the coasts, you can sell your house for cash, move inland and never work again, no matter your age. There is no other country where you can do that. Maybe there will be in the future, but definitely not right now. People who complain about how awful the economy is here forget that this is the best economy in the world and has been so for a very long time. I go with the Warren Buffet outlook on this, which is “Never bet against America.”

Q: How about an Entry point for Freeport McMoRan (FCX)?

A: It’s lower. You don’t want to touch it while the entire commodity sector is selling off in fears of higher interest rates in a recession. Once that’s over it goes to $100.

Q: What is the best way to play Natural Gas?

A: I’ll send an extended report tomorrow, but the short answer is United States Natural Gas Fund (UNG) and ProShares Ultra Bloomberg Natural Gas (BOIL), which is a 2x long day trading NatGas ETF.

Q: Are we entering LEAPS territory for Rivian (RIVN)?

A: Yes, just wait for the current selloff to end and then go to the longest possible expiration. This thing will have a multiple move 2x, 3x, or a 10x out the other side of any recession. The CEO is brilliant and people love the cars.

Q: What happens to housing prices when interest rates on mortgages are at 7%?

A: Well, they should go down 10-20%. What they’re actually doing is going sideways, and they’re still going up in the cheaper neighborhoods because of the structural shortage of 10 million houses in the US. The all-cash buyers are still out there buying. There is tremendous inventory shortage in the housing market now; every broker I know got cleaned out of all their inventory in January when we had a brief 100 basis point dip in rates back then, which has since gone away. I think we go sideways in housing until the end of the year, and then big interest rate cuts will be obvious by then, and the market takes off and we have another 10-year bubble. If you think housing is expensive now, go visit Sydney Australia or Shanghai, China and you’ll see how expensive housing can really get.

Q: How how high would Fed funds have to get to cause a real recession?

A: My guess is 6%. We might actually get there in the second quarter. That might trigger enough of a recession to start unemployment rising just enough to let them cut interest rates. My attitude is: rip the Band-Aid off, raise by 75 basis points on March, and get it over with. But Jay Powell is a very gradualist type of guy, even though he’s brought the sharpest interest rate rise in history.

Q: Should I chase Apple (AAPL) here at $150 a share?

A: In this kind of market, you never chase anything. Only buy Apple at $150 if you think happy days are here again and you think we’re going up forever. To me on the chart it looks like we’re double topping and may actually get a lower low, which you then buy. You may even want to do a LEAPS on Apple if we get down into the $130s or $120s again.

Q: Isn’t it hard for the economy to really tank when seniors and savers are now generating income again for their retirement, giving them more income to spend?

A: Well not only that but workers have had 10-20% pay increases also, and they have more money to spend. It’s really hard to see a severe recession in any kind of scenario, barring another pandemic, and that’s why we’re saying buy the dips—we are in fact in a new bull market that started in October. When you get these market reversals, you often don’t get confirmation on the charts for up to a year, and we’re in one of those periods now. That's why there are still a lot of non-believers in the bull scenario and no confidence.

Q: Would you buy Tesla LEAPS?

A: Yes, under $150 on Tesla shares. And, given its record of volatility, we may actually get there, because this is a $1,000 stock easily in 5 years. I'll send you a report giving you all the details of why. Detroit is basically screwed, someday it’ll just be reduced to building Teslas under license from Tesla and painting them different colors and giving them different names or something like that.

Q: What’s a buy-on-dip?

A: Sorry, but no easy answer here. It’s unique to every stock depending on the historic volatility and ranges of the stock. It’s going to be 1% for a stock, it can be 10% for an option, it could be 20% for a stock like Tesla. It’s vague but it really is unique to every single stock. A good rule of thumb is that after you execute a trade and then throw up on your shoes you’ve just done a great trade.

Q: I see from your pictures that you lost weight? How do you do it?

A: I got COVID last May. I lost 20 pounds in two weeks because I couldn’t eat while I was sleeping 20 hours a day. I just woke up long enough to send out trade alerts. All of a sudden, a 40-year collection of expensive designer pants fit. My kids now call me Captain Fancy Pants. When I go through airport security now and take my belt off they fall down so I’m always careful to wear my best underwear, the ones with the dollar sing all over them.

Q: What’s the best way to play obesity drugs?

A: Unfortunately, There is no pure play on obesity drugs. It will be a $150 billion market that will grow very quickly. I will talk about it at length next week in the summit at the Biotech & Health Care webinar, which you’ll get registration links for tomorrow. Weight loss drugs are small pieces of very large drug companies, so the effect gets diluted by everything else they’re doing. The purest play may be Weight Watchers (WW). If you just need to go to Weight Watchers just to get a shot, that could be really good for them. The stock just doubled in one day on this.

Q: Commodity-based foreign stocks are the best bet on inflation protection; should I get involved?

A: Yes, use the current selloff to get into the whole commodity space (except for maybe food) because not only are they a commodity play, they’re a weak dollar play and that way you get a combined double leverage effect on prices, which I've seen happen many times in my life. So yes, look at foreign-type commodity stocks, and of course, the biggest one out there is Broken Hill Proprietary (BHP), which I always watch very closely. It’s the largest stock in Australia owned by virtually everybody in Australia who has any money, with great volatility, and which has recently just had a selloff.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, or TECHNOLOGY LETTER, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

2015 in Ouarzazate Morocco

Global Market Comments

February 27, 2023

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or MAKING A SILK PURSE FROM A SOW’S EAR)

(META), (GOOGL), (MSFT), (AAPL), (AMZN), (NFLX), (TSLA), (SPY), (TLT), (ENPH), (UUP), (GLD), (SLV), (EEM)

CLICK HERE to download today's position sheet.

Call this the Dr. Jekyll and Mr. Hyde market.

On the up days, we see the kindly ministrations of Dr. Jekyll.

On the down days, we suffer from the evil hand of Mr. Hyde.

To say that traders are confused would be an understatement. Many seasoned pros have told me that this is one of the most difficult markets they have ever seen.

Fridays have been particularly treacherous when weekly options expire. Some 56% of all options trading now takes place with expirations of five days or less. Trading before 4:00 PM sees billions of dollars of hot money trying to force closing prices just in or out of the money for key at-the-money strike prices.

What is especially disturbing is that some 80% of the gain in the S&P 500 (SPY) this year has been in just seven names, Meta, (META), Alphabet (GOOGL), Microsoft (MSFT), Apple (AAPL), Amazon (AMZN), Netflix (NFLX) and Tesla (TSLA). Most other stocks went nowhere….or down. That much concentration means that any rallies lack confidence and will fail….for now.

Remember these names because when we finally do get a real upside breakout, they will be the leaders. You can take that to the bank.

Thanks to turmoil in the House of Representatives intent on a national default, bonds have given up 70 of the 120-basis point drop in yields since October. That deprives us of one of our biggest money makers of 2022, our long bond trades.

That means were are also seeing the automatic flip side of the bond trade, a strong US Dollar (UUP), and weak precious metals, (GLD) and (SLV), and emerging markets (EEM).

This too shall end.

If it was excess liquidity that caused stocks to rocket for 13 years, then maybe we should be focusing on what little liquidity is left. That would be the font of government money pouring into infrastructure and alternative energy plays.

Some $370 billion I know available for investment in ESG, would most of it going into the battery industry for the burgeoning electric vehicle industry. Even foreign firms like Finland’s Neste is moving to the US to cash in on federal munificence, converting an old US oil refinery to produce diesel fuel out of animal and vegetable fat (click here for the link).

Probably the best bet here is in California-based Enphase Energy (ENPH), which makes a 40% gross profit margins on microinverters for solar panels and has just seen a 42% dive in its share price. That makes (ENPH) a BUY. Hint: solar stocks always follow the price of oil to which it is tied, which has lately been down.

Some nimble and aggressive trading managed to push me back in the green for February, taking me up +0.93% on the month. That’s a dramatic improvement of +5.48% from a week ago.

You might even call it making a silk purse from a sow’s ear.

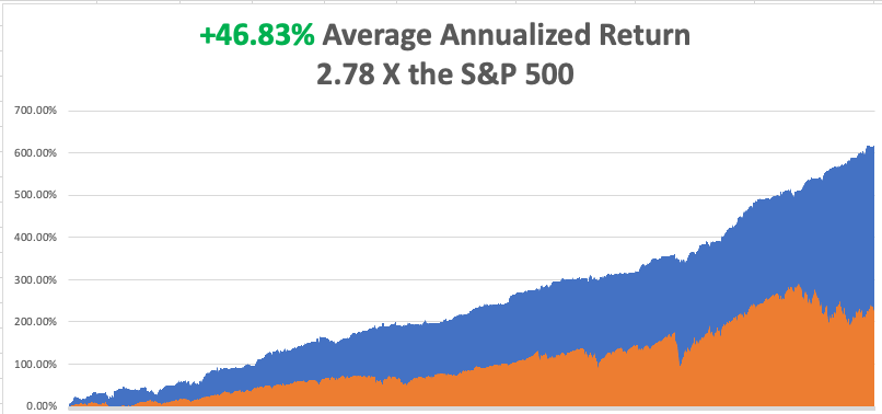

My 2023 year-to-date performance is still at the top at +23.28%. The S&P 500 (SPY) is up +4.32% so far in 2023. My trailing one-year return maintains a sky-high +86.58% versus -12.97% for the S&P 500.

That brings my 15-year total return to +620.47%, some 2.78 times the S&P 500 (SPX) over the same period. My average annualized return has recovered to +46.83%, still the highest in the industry.

Last week, I piled on a Tesla (TSLA) March $155-$260 short strangle betting that the stock can stay within a $95 range for 19 trading days. I also added a deep in-the-money long in the bond market for the first time in six weeks. Both positions turned immediately profitable.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

Q4 GDP Dips, from 3.9% to 2.7% in the October-December quarter. Consumption took a dive, which is amazing over the holidays. This is nowhere near a recession.

Fed Minutes Show More Hikes to Come, with the emphasis on the plural. That could take the overnight borrowing rate to a 5.40% high. It certainly pees on the parade for the falling interest rates crowd.

The Tail is Wagging the Dog, with short, dated options, often same-day expiration dominating trading every Friday. Billions of dollars are battling around key strike prices attempting to force expirations in or out of the money. No place for the little guy. Better to take Fridays off.

Netflix Slashes Prices in 30 countries, taking the stock down a modest 3%. (NFLX) is still the leader in the sector with 231 million subscribers, followed by Amazon (200 million), Disney Plus (162 million, HBO Max (95 million, Peacock (18 million), and Hulu 47 million). Buy (NFLX) and (AMZN) on dips.

Individual 401k’s Lost 23% in 2022, according to a study from Fidelity. High inflation is shrinking the remaining purchasing power even faster. A rising number of workers are also borrowing against their 401k’s to make ends meet. Such loans can go up to 50% of the principal. Better start making up the losses or you’ll be spending your golden years working at Taco Bell.

Apple to Add Glucose Monitor on its Watches, to aid diabetic clients. Some 38 million Americans have diabetes and given the obesity epidemic that figure is certain to rise. It highlights Big Tech’s move into the low-hanging fruit in health care.

Existing Home Sales Dive 0.7% in January, to a 4 million annualized rate, the weakest since October 2010. That makes 12 consecutive months of falling sales. The Median Home Price sold rose to $359,000. An imminent national debt crisis and spiking interest rates is not a great environment in which to sell your home.

Biden Ukraine Visit Tanks Gas and Oil Prices, cutting Russia’s chances of a win and eventually leading to a flood of oil on the market. Biden’s visit is sending the message to Putin that there’s no chance of a win here. Energy is hitting two-year lows across the board. Only energy stocks are staying high. Energy is getting so cheap it might be worth a trade.

Germany Accelerates Move Towards Alternatives, permanently cutting all ties with Russia energy. Europe’s biggest economy, and the fourth largest in the world, hopes to get 80% of its electricity from solar and wind by 2030. Hydrogen is also entering the picture. Other countries will follow.

On Monday, February 27 at 8:30 AM EST, US Durable Goods are out.

On Tuesday, February 28 at 9:00 AM, the S&P Case Shiller National Home Price Index for December is released.

On Wednesday, March 1 at 10:00 AM, the ISM Manufacturing PMI is printed.

On Thursday, March 2 at 8:30 AM, the Weekly Jobless Claims are announced.

On Friday, March 3 at 8:30 AM, the ISM Non-Manufacturing PMI. At 2:00 the Baker Hughes Oil Rig Count is out.

As for me, I usually get a request to fund some charity about once a day. I ignore them because they usually enrich the fundraisers more than the potential beneficiaries. But one request seemed to hit all my soft spots at once.

Would I be interested in financing the refit of the USS Potomac (AG-25), Franklin Delano Roosevelt’s presidential yacht?

I had just sold my oil and gas business for an outrageous profit and had some free time on my hands so I said, “Hell Yes,” but only if I get to drive. The trick was to raise the necessary $5 million without it costing me any money.

To say that the Potomac had fallen on hard times was an understatement.

When Roosevelt entered the White House in 1932, he inherited the presidential yacht of Herbert Hoover, the USS Sequoia. But the Sequoia was entirely made of wood, which Roosevelt had a lifelong fear of. When he was a young child, he nearly perished when a wooden ship caught fire and sank, he was passed to a lifeboat by a devoted nanny.

Roosevelt settled on the 165-foot USS Electra, launched from the Manitowoc Shipyard in Wisconsin, whose lines he greatly admired. The government had ordered 34 of these cutters to fight rum runners across the Great Lakes during Prohibition. Deliveries began just as the ban on alcohol ended.

Some $60,000 was poured into the ship to bring it up to presidential standards and it was made wheelchair accessible with an elevator, which FDR operated himself with ropes. The ship became the “floating White House,” and numerous political deals were hammered out on its decks. Some noted guests included King George VI of England, Queen Elisabeth, and Winston Churchill.

During WWII Roosevelt hosted his weekly “fireside chats” on the ship’s short-wave radio. The concern was that the Germans would attempt to block transmissions if broadcast came from the White House.

After Roosevelt’s death, the Potamac was decommissioned and sold off by Harry Truman, who favored the much more substantial 243-foot USS Williamsburg. The Potamac became a Dept of Fisheries enforcement boat until 1960 and then was used as a ferry to Puerto Rico until 1962.

An attempt was made to sail it through the Panama Canal to the 1962 World’s Fair in Seattle, but it broke down on the way in Long Beach, CA. In 1964 Elvis Presley bought the Potomac so it could be auctioned off to raise money for St. Jude Children’s Research Hospital. It sold for $65,000. It then disappeared from maritime registration in 1970. At one point there was an attempt to turn it into a floating disco.

In 1980 a US Coast Guard cutter spotted a suspicious radar return 20 miles off the coast of San Francisco. It turned out to be the Potomac loaded to the gunnels with bales of illicit marijuana from Mexico. The Coast Guard seized the ship and towed it to the Treasure Island naval base under the Bay Bridge. By now the 50-year-old ship was leaking badly. The marijuana bales soaked up the seawater and the ship became so heavy it sank at its moorings.

Then a long rescue effort began. Not wanting to get blamed for the sinking of a presidential yacht on its watch the Navy raised the Potomac at its own expense, about $10 million, putting its heavy lift crane to use. It was then sold to the City of Oakland, Ca for a paltry $15,000.

The troubled ship was placed on a barge and floated upriver to Stockton, CA, which had a large but underutilized unionized maritime repair business. The government subsidies started raining down from the skies and a down-to-the-rivets restoration began. Two rebuilt WWII tugboat engines replaced the old, exhausted ones. A nationwide search was launched to recover artifacts from FDR’s time on the ship. The Potomac returned to the seas in 1993.

I came on the scene in 2007 when the ship was due for a second refit. The foundation that now owned the ship needed $5 million. So, I did a deal with National Public Radio for free advertising in exchange for a few hundred dinner cruise tickets. NPR then held a contest to auction off tickets and kept the cash (what was the name of FDR’s dog? Fala!).

I also negotiated landing rights at the Pier One San Francisco Ferry Terminal, which involved negotiating with a half dozen unions, unheard of in San Francisco maritime circles. Every cruise sold out over two years, selling 2,500 tickets. To keep everyone well-lubricated I became the largest Bay Area buyer of wine for those years. I still have a free T-shirt from every winery in Napa Valley.

It turned out to be the most successful fundraiser in the history of NPR and the Potomac. We easily got the $5 million and then some. The ship received a new coat of white paint, new rigging, modern navigation gear, and more period artifacts. I obtained my captain’s license and learned how to command a former coast guard cutter.

It was a win-win-win.

I was trained by a retired US Navy nuclear submarine commander, who was a real expert at navigating a now thin-hulled 73-year-old ship in San Francisco’s crowded bay waters. We were only licensed to cruise up to the Golden Gate bridge and not beyond, as the ship was so old.

The inaugural cruise was the social event of the year in San Francisco with everyone wearing period Depression-era dress. It was attended by FDR’s grandson, James Roosevelt III, a Bay area attorney who was a dead ringer for his grandfather. I mercilessly grilled him for unpublished historical anecdotes. A handful of still-living Roosevelt cabinet members also came, as well as many WWII veterans.

As we approached the Golden Gate Bridge, some poor soul jumped off and the Coast Guard asked us to perform search and rescue until they could get a ship on station. No body was ever found. It certainly made for an eventful first cruise.

Of the original 34 cutters constructed only four remain. The other three make up the Circle Line tour boats that sail around Manhattan several times a day.

Last summer I boarded the Potomac for the first time in 14 years for a pleasant afternoon cruise with some guests from Australia. Some of the older crew recognized me and saluted. In the cabin, I noticed a brass urn oddly out of place. It contained the ashes of the sub-commander who had trained me all those years ago.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Captain Thomas at the Helm

Global Market Comments

February 24, 2023

Fiat Lux

Featured Trade:

(FEBRUARY 22 BIWEEKLY STRATEGY WEBINAR Q&A)

(SPY), (BA), (CCI), (HD), (TLT), (TSLA), (PPLT), (PALL),

(JPM), (NVDA), (AAPL), (GOOGL), (META), (AMZN)

CLICK HERE to download today's position sheet.

Below please find the subscribers’ Q&A for the February 22 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley in California.

Q: Will Russia use nuclear weapons on Ukraine?

A: No, they won’t. If you’re trying to take over a country, you don’t exactly want to drop atomic bombs on it first and render it useless. If they do, Ukraine will retaliate in kind with the nukes they have. Most of the nuclear weapons the old Soviet Union had were assembled in Ukraine and the machinery is still there. We know Ukraine has four nuclear power plants and hundreds of tons of fuel so they have uranium. You only need to increase the purity from 80% to 93% and then convert it to plutonium to get weapons-grade and you only need 20 pounds to make a small bomb. At the very least, they could build a dirty truck bomb and make Moscow uninhabitable for 100 years. If the Russians did explode a nuke, the fallout cloud would blow back on them the next day, China in three days, the US in 10 days, and back on Russia again in two weeks. If Ukraine doesn’t remember how to make nuclear weapons, they can just ask me. I do have “Nuclear Test Site” on my resume.

Q: What would be the impact on the markets of a government debt default?

A: Bonds would collapse, causing interest rates to spike, and taking down stocks big time. Higher interest rates would crash the real estate market. You also can’t do real estate closings during a shutdown because Fannie Mae and Freddie Mac aren’t there to buy the debt. Commodities would fall sharply on recession fears. Even gold and silver do poorly on a massive liquidity squeeze. Government payments would cease, including Social Security, Medicare, and military salaries. Air traffic control would stop unless they are happy to work for free. The only place to hide is cash under your mattress since US Treasury bills and commercial banks will also be at risk. This is what the House Republicans are risking. It really depends on how long the shutdown lasts. Every time Georgia representative Marjorie Taylor Greene shouted “liar” at the State of the Union address you could see bond prices ticking down. She is one of the people who has to agree to a rise in the debt ceiling and she didn’t inspire a lot of confidence in bondholders. All that said, a $10 dip is a good place to buy the (TLT).

Q: Would you buy Boeing up here?

A: I loved Boeing at $100 and we did a could trades down there. At $220 not so much. It’s more than doubled off the October low and all the best-case scenarios have happened. The 737 MAX, which crashed twice due to an AI issue, got back in the air. The 787 Dreamliner is selling well. The company now has a two-year order backlog. And Air India followed up with the biggest aircraft order in history, some 450 planes over ten years. If Boeing dips $50 that would be another story because I think it hits a new all-time high at $450 in a couple of years. By the way, I took a 737 MAX on my flight back from Hawaii last weekend and the crew loved it. There are no screens on the seats. Instead, they broadcast the 800 greatest movies of all time on free WIFI.

Q: How do we know if your trade alert is for the stock, the ETF, or another underlying position?

A: Look at the ticker symbol—it always tells you exactly which security we are working in.

Q: With Bullard signaling a 50 basis-point rate hike, will the S&P (SPY) go down in the near term and how much?

A: Well Bullard is only one guy out of nine, so he doesn’t have the final say. It really depends on what Jay Powell wants. And if the data continues hot and inflation keeps rising, we will get a 50 basis point rise, and that should take the index down 10% from the recent high, or give up half of its recent year-to-date gains, so that’s a good rule of thumb. As long as we’re waiting for bad news, (which we won’t get until March 22) the markets will do nothing until then.

Q: What do you think about Crown Castle International (CCI), the cell tower company, taking a big hit with the bond market?

A: It pretty much moves in sync with the bond market, which has just dropped 10 points, so you probably want to be buying or doubling up on (CCI) right here, because it will be the first thing to recover once we see a negotiated increase in the debt ceiling which has to happen before the summer. The 5G buildout continues unabated.

Q: Would you recommend buying Tesla (TSLA) shares again?

A: Yes, but at least $50 lower, which we may get. Or at least $50 off the $217 top. I think Tesla goes to $1,000 sometime in the next couple of years and so does Elon Musk. All of the factors that could drive the stock that high are in progress. I know it’s happening over there, and that’s easily a $1,000 stock once their current breakthroughs go mass-market.

Q: Any interest in Iron Condors?

A: It is the same as Strangles, with more limited risk with four legs, a call spread and a put spread because you stop out your losses at much lower levels. But they are very trading-intensive, commission-intensive trades, and it’s really too much for most beginners to handle. However, if you’re a professional, you might consider doing iron condors on these positions. Iron Condors also max profits when nothing moves, and lately, no move is a pretty rare event. We’re going to get it for the next couple of months, but don’t count on that being a frequent trade.

Q: Any iShares 20 Plus Year Treasury Bond ETF (TLT) LEAPS to buy now?

A: Yes I've been kind of sitting on my hands waiting to see if this bottom here holds at 99 before I put out LEAPS, but we’re so close it really almost makes no difference. And if I were to do a LEAPS here it probably would be the $100-$105 one-year out. That might get you about a 100% profit in a year. That’s a very safe LEAPS, and I’ll get the numbers out when I get a chance.

Q: What’s your opinion on Home Depot (HD)?

A: I like it for the long term. Clearly, their disastrous earnings report shows that the economy for home repair is not as strong as we thought it was, so it may go lower first. I would hold off until we get a real capitulation selloff in those stocks.

Q: Are gold and silver possible candidates for LEAPS?

A: Yes, especially in view of the recent correction in these metals. And we did put these out last October at the market bottom. I probably will be updating that sometime in the next few weeks.

Q: How much longer will the Ukraine/Russia war last?

A: The general consensus among the military now is that this goes on for several more years, and both sides will just keep pouring troops into the meat grinder until they get exhausted.

Q: Any way to play Platinum (PPLT) or Palladium (PALL)?

A: Yes, there are ETFs on each of them.

Q: Any thoughts on the crypto industry?

A: I have given up on the crypto industry because it has been shown that so many of these trading platforms were stealing from their customers. Once you lose the confidence of a customer on trust, you never get it back in the financial industry. Also, crypto was interesting a couple of years ago when it was going up and everything else in the world was too expensive, but now you have all the best stocks trading not far from multi-year lows, and that makes quality stocks much more attractive than a crypto where you really don't know what’s going to happen. Crypto could be another Nikkei, which after 32 years still hasn’t reached its old highs. That is unless it gets taken over by big banks like (JPM) and regains respectability that way.

Q: Any thoughts on investing in the AI trend?

A: AI has suddenly become what crypto was 2 years ago, and what 3D printing was 15 years ago. It’s just the theme of the day, and something to promote. There are no pure AI plays. Basically, all companies have been using it for 10 or 15 years, it’s not a new thing. In fact, AI is already in every aspect of your life, you just might not know it yet. NVIDIA (NVDA) is probably the purest AI play out there whose chips everyone needs to execute AI. Beyond that, the biggest AI users are Apple (AAPL), Alphabet (GOOGL), Meta (META), and Amazon (AMZN). When Amazon makes ten more recommendations on books you might like or movies you might watch, that is AI.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH or TECHNOLOGY LETTER, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

With Medal of Honor Winner Colonel Mitchel Paige

Global Market Comments

February 22, 2023

Fiat Lux

Featured Trade:

(TESTIMONIAL),

(TEN MORE TRENDS TO BET THE RANCH ON),

(AAPL), (AMZN), (GOOGL), (TSLA), (CRSP), (EDIT), (NTLA)

CLICK HERE to download today's position sheet.

I believe that the pandemic and hyper-accelerating technology is bringing forward the future at an astonishing rate.

More applications will be created in the next year than over the last 40, some 500,000. The sum total of human knowledge is now doubling every year. The profits spun off and investment opportunities will be incredible, which is why I just doubled my ten-year forecast for the Dow Average (INDU) from 120,000 to 240,000.

Here are ten major trends for the economy and the markets that we can see already. It’s the unseen ones that will be really interesting.

(1) The Insurance Industry Changes Beyond All Recognition, confirming from “Recovery After Risk” to “Prevention of Risk”. Today, fire insurance pays you after your house burns down. Life insurance pays your next of kin after you die. And health insurance (which is really sick insurance) pays only after you get sick. During the next decade, we’ll see a new generation of insurance providers that offer you a service to KEEP you healthy and keep your house safe during a wildfire. Also, full autonomous driving will cut hospital admissions by half, dramatically dropping the cost of insurance. This is driven by machine learning, ubiquitous sensors, low-cost genome sequencing, and robotics to detect risk, prevent disaster, and guarantee safety before any costs are incurred.

(2) Autonomous Vehicles and Flying Cars (eVTOL) will make travel cheaper and easier. Fully autonomous vehicles (TSLA), (GOOGL), car-as-a-service fleets, and aerial ridesharing (flying cars) will be fully operational in most major metropolitan cities in the coming decade. The cost of transportation will plummet 3-4X, transforming real estate, finance, insurance, the materials economy, and urban planning. Where you live and work, and how you spend your time, will all be fundamentally reshaped by this future of human travel. Your kids and elderly parents will never drive. Already, a half dozen eVTOL companies have gone public raising more than $10B to fuel their growth. These vehicles are real and will help define the decade ahead. This is driven by machine learning, sensors, materials science, battery storage improvements, and ubiquitous gigabit connections.

(3) On-demand Production and On-demand Delivery Will Create an “Instant Economy of Things”. Urban dwellers will learn to expect “instant fulfillment” of their retail orders as drone and robotic last-mile delivery services carry products from local supply depots directly to your doorstep. Further riding the deployment of regional on-demand digital manufacturing (3D printing farms), individualized products can be obtained within hours—anywhere, anytime. I ordered a new high-end 50-pound garage door opener from Amazon Prime (AMZN) last month after my old one went kaput. Incredibly, they delivered it in hours! This is driven by networks, 3D printing, robotics, and AI.

(4) The Ability to Sense and Know Anything, Anytime, Anywhere. We’re rapidly approaching the era where 100 billion sensors (the Internet of Everything) are monitoring and sensing (imaging, listening, measuring) every facet of our environments, all the time. Global imaging satellites, drones, autonomous car LIDARs, and forward-looking augmented reality (AR) headset cameras are all part of a global sensor matrix, together allowing us to know anything, anytime, anywhere. In this future, it’s not “what you know,” but rather “the quality of the questions you ask” that will be most important. That gives us old guys a huge advantage. This is driven by the convergence of terrestrial, atmospheric, and space-based sensors, vast data networks, 5G and 6G communication networks (AAPL), next-gen Wi-Fi, and machine learning.

(5) Advertising Hyper Evolves. As ads become the primary driver of new services for free, AI becomes increasingly embedded in everyday life and your custom personal AI will soon understand what you want better than you do. In turn, we will begin to both trust and rely upon our AIs to make most of our buying decisions, turning over shopping to AI-enabled personal assistants. Your AI might make purchases based on your past desires, current shortages, conversations you’ve allowed your AI to listen to, or by tracking where your pupils focus on a virtual interface (i.e., what catches your attention). As a result, the advertising industry—which normally competes for your attention (whether at the Superbowl or through search engines)—will have a hard time influencing your AI. This is driven by machine learning, sensors, augmented reality, and 5G/networks.

(6) Cellular Agriculture Moves from the Lab to Inner Cities, Providing High-quality Protein that is Cheaper and Healthier. The next decade will witness the birth of the most ethical, nutritious, and environmentally sustainable protein production system devised by humankind. Stem cell-based “cellular agriculture” will allow the production of beef, chicken, and fish anywhere, on-demand, with far higher nutritional content, and a vastly lower environmental footprint than traditional livestock options. Traditional legacy steaks found at Ruth’s Chris and Morton’s will only to available to the wealthy. This is driven by biotechnology, materials science, machine learning, and agtech.

(7) Your Brain Will Integrate with Super-Fast Hardware and Software. My friend, technologist and futurist Ray Kurzweil, has predicted that by the mid-2030s, we will begin connecting the human neocortex to the cloud. This next decade will see tremendous progress in that direction, first serving those with spinal cord injuries, whereby patients will regain both sensory capacity and motor control. Yet beyond assisting those with motor function loss, several BCI pioneers are now attempting to supplement their baseline cognitive abilities, a pursuit with the potential to increase their sensorium, memory, and even intelligence. Recent demonstrations of a macaque monkey playing Pong using a Neuralink implant is proof of incredible progress. This is driven by materials science, AI/machine learning, robotics, and some fantastic imaginations.

(8) High-resolution Virtual Reality Will Transform Both Retail and Real Estate Shopping & the Future of Education. If you were a couch potato, you are about to become one on steroids. High-resolution, lightweight virtual reality headsets will allow individuals at home to shop for everything from clothing to real estate—all from the convenience of their living room. Need a new outfit? Your AI knows your detailed body measurements and can whip up a fashion show featuring your avatar wearing the latest 20 designs on a runway. Want to see how your furniture might look inside a house you’re viewing online? No problem! Your AI can populate the property with your virtualized inventory and give you a guided tour. On the education front, the use of VR and AI-driven avatars with technology such as that demonstrated by Dreamscape promises a future of game-like, immersive, and powerful education and training. This is driven by VR, machine learning, and high-bandwidth networks. Get your Oculus Rift from Facebook (FB) now!

(9) Increased Focus on Sustainability and the Environment will drive companies to invest in sustainability—both from a necessity standpoint and for marketing purposes. Breakthroughs in materials science, enabled by AI, will allow companies to drive tremendous reductions in waste and environmental contamination. One company’s waste will become another company’s profit center. Want to visit my chalet in Switzerland? You can do so by connecting your Oculus Rift headset to Google Maps….today! This is driven by materials science, AI, CRISPR, digital biology, and broadband networks.

(10) CRISPR and Gene Therapies Will Eliminate Disease. Perhaps one of the most powerful, underappreciated technologies in the world is CRISPR. In 2020, two incredible women won the Nobel Prize in medicine for its discovery, and revenues from CRISPR doubled between 2019 and 2020 to over $1.5B. A vast range of infectious diseases, from AIDS to Ebola, are now potentially curable, as are a wide range of genetic ailments like sickle cell anemia, thalassemia, and certain forms of congenital blindness. In addition, gene-editing technologies continue to advance in precision and ease of use, allowing families to treat and ultimately cure hundreds of inheritable genetic diseases. This is driven by various biotechnologies (CRISPR, Gene Therapy), genome sequencing, and AI. Only three companies have a monopoly in this sector right now, (CRSP), (EDIT), and (NTLA).

In the decade ahead, master entrepreneurs will look beyond the immediate effects of a given technology to seize secondary and tertiary, Google-sized business opportunities on the horizon.

As an investor, you should be asking yourself: What challenges or problems can I help solve? How can I leverage the coming waves of tech advancements?

I just thought you’d like to know.

John Thomas