Mad Hedge Technology Letter

December 1, 2021

Fiat Lux

Featured Trade:

(TAKE A REST FROM FINTECH)

(PYPL), (SQ), (BNPL), (AMZN), (TWTR), (AAPL)

Mad Hedge Technology Letter

December 1, 2021

Fiat Lux

Featured Trade:

(TAKE A REST FROM FINTECH)

(PYPL), (SQ), (BNPL), (AMZN), (TWTR), (AAPL)

The fintech trade is tiring — that is what the underperformance of stocks like PayPal (PYPL) and Square (SQ) is telling us.

Jack Dorsey’s Square has retraced around 25% from its peak and is bang on even from where it was 365 days ago.

Not what you want to hear if you’re a fintech trader.

The pullback from PYPL is even more precipitous declining around 40% from its peak.

Certainly, it would be cliché for me to say that the low-hanging fruit is gone from the fintech trade, but that’s exactly what is happening here.

Not only that, but I would also like to point out that most companies without a home-field advantage ecosystem are getting penalized for exactly that — not having an ecosystem.

Wasn’t it weird how the whole tech sector literally gave us a rip-your-face-off selloff the other day yet, Apple was one of the only tech stocks that reacted positively?

As we move into the late stages of the economic cycle, the goalposts are certainly narrowing for the tech companies, and that’s bad news for SQ and PYPL.

Another way to get penalized is to let that moat narrow which is effectively what has happened to PYPL and SQ.

And that’s the thing with PYPL, it’s just a way to pay, and not an ecosystem.

It plays second fiddle to that of wall gardens and the user trapped in it who is spending and can’t find a way out.

Another point I would like to make is that Twitter (TWTR) at these levels is an ideal buy-the-dip candidate precisely because it’s a great walled garden whose potential has yet to be untapped.

And readers shouldn’t let the mismanagement of the company by former CEO Jack Dorsey turn you off from a great long-term investment.

PYPL would kill for a platform like Twitter and instead needs to grovel to other strategic platforms to allow them to use PYPL’s technology.

PYPL is finally exposed, and I guess more accurate would be to say they are getting undercut by stickier technology that is more convenient to the consumer.

And what does that get you in late 2021?

Downgrades and slews of them which cut blocks the stock at its knees.

We just got one from Bernstein the other day and then it almost becomes a self-fulfilling prophecy with other analyst outlets doing the same thing in a copycat league.

Instead of catching a falling knife in SQ and PYPL, traders need to let these stocks breathe and find support where we know buyers will come in to breed confidence in an upward trajectory.

Easier said than done.

What has been all the rage so far denting PYPL and SQ’s model?

Enter Buy Now Pay Later (BNPL).

Naturally, the differentiated mechanism around which this technology revolves around is the delay in paying, which is never a good concept for a fintech player who rather gets paid ASAP.

Delayed payment is one headache, but then the downward force on fees is another monumental concern, if not downright scary.

This will no doubt trounce margin expansion moving forward and evidence of slowed growth in the latest quarter does not portend well for the company, especially as pandemic tailwinds continue to fade.

Another talking point is BNPL’s lack of credit checks meaning the quality of purchasers will naturally decline, may I even say attract fraudsters as well, and the companies will need to build up loss reserves to compensate for a riskier purchaser profile.

Klarna is another major BNPL company, and they were part of this new industry that took in around 20% of all sales on Cyber Monday.

That rather high number bodes poorly for PYPL in the short term.

Reinforcing the strategic hole of a lack of walled garden is that PYPL is desperate to cultivate partnerships like PYPL’s Venmo joining forces with Amazon (AMZN) — Starting next year, you'll be able to use the money anybody Venmo’s you to buy products directly from Amazon — so long as you live in the US.

But again, Amazon is infamous for replacing outside technology with its own in-house solution over time.

PYPL’s counter solution for BNPL is to enter the BNPL lovefest as well which will effectively trigger a race to zero.

Stopgap solutions will inevitably cannibalize its own business model.

Then let’s point to another walled garden — Tim Cook’s Apple with its Apple wallet.

It’s getting better and with the Apple Card, do they ever really need to spend one second considering a partnership with PYPL or SQ.

There is an inquisition going on in the fintech industry and big body blows will need to be landed for some clear-cut solutions that will ultimately lead to consolidation.

In this precarious environment, don’t get too fancy while fintech is getting elbowed out the way, head to higher ground where balance sheets can absorb just about anything.

Global Market Comments

November 30, 2021

Fiat Lux

Featured Trade:

(NEW VIDEO UPDATE ON EXECUTING A VERTICAL BULL CALL DEBIT SPREAD),

(AAPL), (GS)

Mad Hedge Technology Letter

November 22, 2021

Fiat Lux

Featured Trade:

(RENOMINATION BOOSTS BIG TECH)

(FB), (GOOGL), (AMZN), (MSFT), (AAPL)

U.S. President Joe Biden is doing all he can do to make sure that the US Central Bank stays accommodative to big tech investors.

He let the doves back in the driving seat which is highly positive for corporate America and terrible for penny-pinching savers.

Biden’s decision to re-elect incumbent Fed Chair Jerome Powell was cheered by the market locking in his ultra-low interest rate policies for yet another term.

Even more brazen was the appointment of Vice Chair, an even more pronounced dove Dr. Lael Brainard.

The second in command often helps signal Fed policy and gives it a dovish twist and clears the way for all systems go in 2022.

Any inclination that interest rates would rise faster than expected is now a non-starter, and the Fed will push its "lower for longer" mantra in the face of surging inflation for as long as they can make excuses for it.

Ostensibly, the path of easiest conjecture leads me to say that the five biggest stocks in the S&P 500 – Facebook, Apple, Amazon, Microsoft, and Google, which are around 30% of the market and growing, will do well in 2022.

Long-term, they have comprised an average of about 14% of the entire stock market, and 2022 should be the year they knock on the 35% threshold.

This essentially means that the stock market is techs to win or lose and everyone else is just a footnote.

And yeah I know…it’s been like that for quite a while now; but it’s more prevalent than ever.

We are rolling into a year where big tech will weaponize their cash horde to issue low-interest corporate bonds of their own company debt and then spin those cash harvests into higher rate corporate bonds that cheapen their cost of doing business because they pocket the higher interest payments as profits.

Industry leaders are able to borrow more cheaply and in greater quantities, and the size of their balance sheets also offers incredible optionality.

This also means they can buy back more shares and also leverage up their balance sheets.

Preferential access to cheap money also cheapens the process of expansion, or in buying rivals, more easily. In effect, lower rates give leading companies an unfair set of tools to accelerate their dominance and which no regulator dares to prevent.

What does this mean in practice for investors? If falling rates have spiced up valuations of the biggest tech stocks on the way up, it implies they may struggle if rates rise, particularly as this would mean investors place less of a premium on future earnings.

But since the expectations are lower for longer, the market will be comfortable with the nominal rate even in the face of surging inflation, meaning it’s a net positive for tech stocks in 2022.

Powell and Baird will move as slow as needed and anything faster than that will shock the tech market and we will get a 5% drop which will be a golden buying opportunity.

I have read many experts’ take on tech preaching that regulation is here and coming fast to take down big tech.

However, I am in the camp that Congress will do hardly anything, and any investigation will end with a slap on the wrist which is fine.

I don’t subscribe to this ridiculous idea that superstars eventually tend to fall to earth.

I believe the current climate has set up big tech to gain an even bigger market share, crush the little guy faster, and trigger EPS to grow uncontrollably.

That’s what I am seeing on the ground with my own eyes, as opposed to baseless claims that big tech will revert back to the mean.

This sets the stage for big tech to benefit from such elevated rates of profitability next year, they will be happy to overpay for smaller companies to whom they will give an ultimatum to either sell up or get killed by them.

Numerous signs point to a devastatingly profitable and comically successful 2022 for the most recognizable and biggest tech firms who will refine their tech and harness their balance sheets in a systematically lethal way.

Unprofitable startups have a mountain climb as it relates to competing in their industries and they can thank President Joe Biden for that; they will be unduly penalized as a group that will result in lower share prices that force them to crawl on their knees to venture capitalists for capital injections.

Global Market Comments

November 1, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or LET THE GAMES BEGIN!)

(MS), (GS), (BLK), (JPM), (BAC), (TLT), (TSLA), (AAPL), (MSFT), (GOOGL), (AMZN), (ROM)

Welcome to the first day of November, when the seasonals swing from negative to positive. The hard six months are over. The next six should be like shooting fish in a barrel.

At least that’s what happened in the past. The period from November 1 to May 31 has delivered the highest stock returns for the past 75 years.

So how do we play a hand that we have already been dealt full of aces and kings?

Load the boat with financials, like (MS), (GS), (BLK), (JPM), and (BAC). Notice that when we had the sharpest rise in interest rates in a year, financials barely moved when they should have crashed? That means they will soon start going up again.

You might have also observed that technology stock has been flat-lining when rising rates should have floored them. That means their torrid 20% earnings growth will keep floating their boats.

It gets better. We just learned that the GDP growth rate plunged in Q3 from a rip-roaring 6% rate to only 2%. What happens next? That 4% wasn’t lost, just deferred into 2022. The rip-roaring 6% growth rate returns. That’s why stocks are pushing up to new all-time highs right now.

So, buy the dips. We may have seen our last 5% correction of 2021. The only unknown is how markets will react to a Fed taper, which could come as early as Wednesday. But on the heels of that, we will get a $1.75 billion rescue package, the biggest in 50 years. One will cancel out the other, and then some.

Take a look at the ProShares Ultra Technology Fund (ROM), the 2X long ETF. I just analyzed its 30 largest holdings. Half are tech stocks that have been trash and are down 30% or more. The other half are at all-times highs, like Microsoft (MSFT) and Alphabet (GOOGL).

What happens next when the seasonals are a tailwind? The tech stocks that are down will rally because they are cheap, while the high stocks keep going because they are best of breed. I think (ROM) has $150 written all over it by March.

You’ve got to love Elon Musk, whose net worth is approaching $300 billion. When the pandemic broke, every automaker cancelled their chip orders for the rest of the year while Tesla took them all. Today, Detroit has millions of cars built but in storage because they are all missing chips. In the meantime, Tesla is snagging orders for 100,000 cars at a time.

Like I say, you gotta love Musk. Hey, Elon, call me! Why don’t you just buy the entire US coal industry and shut it down. It would only cost $5 billion, as market caps are so low. That would have more impact on the environment than another million Teslas. Worst affected would be China, where 70% of US coal now goes.

A continued major driver of the bull case for stocks is profit margins of historic proportions.

Q1 saw a 13% margin, Q2 13.5% and Q3 12.3%, and Q3 had to carry the dead weight of a delta impaired GDP growth rate of only 2.0%. Imagine what companies can do in Q4 when the growth rate is returning to a torrid 6% rate.

This has been one of my basic assumptions for the entire year and it seems it was I was alone in having it. This is where the 90% year-to-date performance comes from.

Inflation is Here to Stay, says top investing heavyweights, at least 4% through 2022. That means high inflation, higher financial shares, and higher Bitcoin prices. It’s going to take two years to unwind the mess at the ports that is driving prices.

Covid is Getting Knocked Out by a One-Two Punch, via a new round of booster shots and imminent childhood vaccinations. It could take new cases to zero in a year and give us a booming economy.

S&P Case Shiller is Still Rocketing, the National Home Price Index up 19.8% YOY in August. Phoenix (33.3%), San Diego (26.2%), and Tampa (25.9%) were the hot cities. This will continue for a decade but as a slower rate.

New Home Sales Pop, to 800,000. Annual median prices jump at an annual 18.7% to $408,000. The share of homes selling over $1 million increased from 5% to 9% in a year. It cost $500,000 to get a starter home in an Oakland slum these days. Homebuilders Sentiment Soars to 80. Buy (KBH), (PUL), and (LEN) on dips.

Bonds Melt Up, creating one of the best trade entry points of the year. A successful 30-year auction this week that took yields from 1.71% down to 1.52% in a heartbeat. It makes no sense. Buying bonds here is like buying oil in the full knowledge that someday it will go to zero. I am doubling my short position here. Look at the (TLT) December 2022 $150-$155 vertical bear put spread LEAPS which is offering a 14-month return of 54%. This is the month when the Fed has promised to begin the first of six interest rate hikes. Just buy it and forget about it.

Proof that the Roaring Twenties is Here. It’s demand that is spiking, the greatest ever seen, not supplies that are drying up in the supply chain issue. It should continue for a decade and the bull market in stocks that follows it. You heard it here first. Dow 240,000 here we come.

Apple Blows it in Q3, with millions of its phones lost at sea and no idea when unloads are possible, costing it $6 billion in sales. Revenues were up a ballistic 29% YOY. Buy (AAPL) on dips. I see $200 a year next year.

Amazon Craters, with both shrinking revenues and profits. Supply chain problems about with several billion of inventory trapped at sea off the coast of Long Beach. It plans to hire 275,000 to handle the Christmas rush. The stock hit a one year low. There is a time to buy (AMZN) on the dip, but not quite yet.

My Ten Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

My Mad Hedge Global Trading Dispatch saw a massive +8.95% gain in =October. My 2021 year-to-date performance maintained 88.55%. The Dow Average is up 17.06% so far in 2021.

After the recent ballistic move in the market, I am continuing to run my longs in Those include (MS), (GS), (BAC), and a short in the (TLT). All are approaching their maximum profit point and we have nothing left but time decay to capture. So, I am going to run these into the November 19 expiration in 14 trading days. It’s like have a rich uncle write you a check one a day.

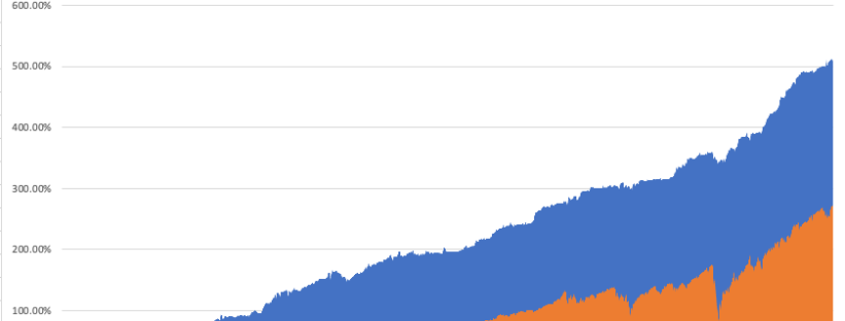

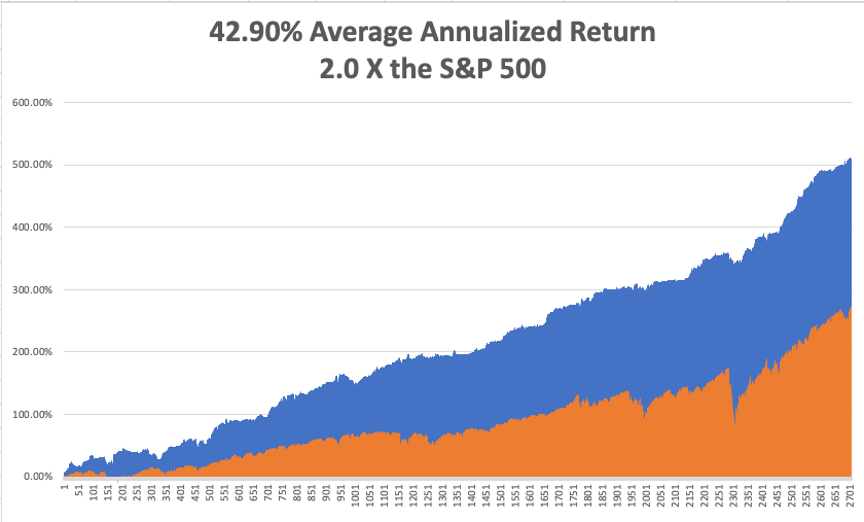

That brings my 12-year total return to 511.10%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return now stands at an unbelievable 42.90%, easily the highest in the industry.

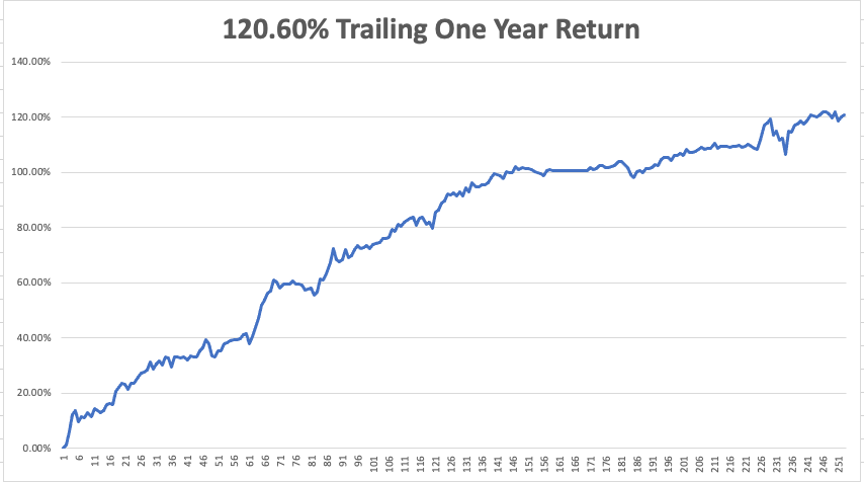

My trailing one-year return popped back to positively eye-popping 120.60%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 46 million and rising quickly and deaths topping 746,000, which you can find here.

The coming week will be slow on the data front.

On Monday, November 1 at 7:00 AM, the ISM Manufacturing PMI for October is out. Avis (CAR) Reports.

On Tuesday, November 2 at 1:30 PM, the API Crude Oil Stocks are released. Pfizer (PFE) reports.

On Wednesday, November 3 at 7:30 AM, the Private Sector Payroll Report is published. Etsy (ETSY) reports. At 11:00 AM, the Federal Reserve interest rate decision is announced, followed by a press conference.

On Thursday, November 4 at 8:30 AM, Weekly Jobless Claims are announced. Airbnb reports (ABNB).

On Friday, November 5 at 8:30 AM, The October Nonfarm Payroll Report is released. DraftKings (DKNG) reports. At 2:00 PM, the Baker Hughes Oil Rig Count are disclosed.

As for me, I have been known to occasionally overreach myself, and a trip to the bottom of the Grand Canyon a few years ago was a classic example.

I have done this trip many times before. Hike down the Kaibab Trail, follow the Colorado River for two miles, and then climb 5,000 feet back up the Bright Angle Trail for a total day trip of 27 miles.

I started early, carrying 36 pounds of water for myself and a companion. Near the bottom, there was a National Park sign stating that “Being Tired is Not a Reason to Call 911.” But I wasn’t worried.

The scenery was magnificent, the colors were brilliant, and each 1,000 foot descent revealed a new geologic age. I began the long slog back to the south rim.

As the sun set, it was clear that we weren’t going to make to the top. I was passed by a couple who RAN the entire route who told me “better hurry up.” I realized that I had erred in calculating the sunset, it'staking place an hour earlier in Arizona than in California.

By 8:00 PM it was pitch dark, the trail had completely iced up, and it was 500 feet straight down over the side. I only had 500 feet to go but the batteries on my flashlight died. I resigned myself to spending the night on the cliff face in freezing temperatures.

Then I saw three flashlights in the distance. Some 30 minutes later, I was approached by three Austrian Boy Scouts in full dress uniform. I mentioned I was a Scoutmaster and they offered to help us up.

I grabbed the belt of the last one, my companion grabbed my belt, and they hauled us up in the darkness. We made it to the top and I said, “thank you”, giving them the international scout secret handshake.

It turned out that I wasn’t in great shape as I thought I was. In fact, I hadn’t done the hike since I was a scout myself 30 years earlier. I couldn’t walk for three days.

Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Happy Halloween!

Mad Hedge Technology Letter

October 29, 2021

Fiat Lux

Featured Trade:

(APPLE HIT BY LOGISTIC CHAOS)

(AAPL)

The numbers tell the story for Apple (AAPL) — 745 million paid subs.

It’s not at Facebook levels yet, but Apple’s 745 million almost entirely can claim to buying multiple Apple devices.

Then step back and admire the increase of 160 million paid subs versus just 12 months ago and understand this minor dip in today’s shares is just another buying opportunity.

Being able to add 160 million paying subs in 12 months stems from the ability to continue to launch new services and new offerings within the services that they already have, new features that are game-changers.

In short, that’s how you grow a large business that does $68 billion in the last 12 months with levers that are diversified as any.

At a granular level, The Apple App Store notched a September quarter record.

This highlights the trend that consumers are paying on the platform and are happy to do it, which is why the services keep growing to double digits.

I applaud Apple for taking a stand against ad technology and giving privacy back to the user.

It’s a luxury they can afford, but I believe it will turn into a tailwind.

The feedback from customers is overwhelmingly positive.

Customers appreciate having the option of whether they want to be tracked or not.

It’s just another feature that goes into making Apple one of the best tech firms in the world.

Some more accomplishments this past quarter was setting an all-time record for Mac sales and quarterly records for iPhone, iPad, wearables, home, and accessories, representing 30 percent year-over-year growth in products.

This level of sales performance, combined with the unmatched loyalty of Apple’s customers and the ecosystem strength drove services to an all-time revenue record of $18.3 billion, up 26 on services.

Some people in the industry and some people outside the industry thought that the pandemic would reduce demand, they pulled their orders down, things reset. And what really happened was demand went up and went up even more than a straight trend would predict. And so, the industry is working through that now.

When everything is working, it’s hard to pick the bad out. However there was one black eye, and I would say nothing structural, but a consequence of the external variables Apple can’t always control, i.e. supply.

“Constraints” reared its ugly head to the tune of a $6 billion revenue dollar impact, driven primarily by industrywide silicon shortages and COVID-related manufacturing disruptions.

Supply constraints cost Apple $6 billion and it affected the iPhone the iPad and the Mac.

Chips are becoming harder to secure, especially the legacy variation.

Next, was the pandemic-related manufacturing disruptions in Southeast Asia which produce many of Apple’s products.

However, the situation has eased in Southeast Asia, and fewer disruptions in October bode well for next quarter’s earnings.

But from a demand point of view — demand is very robust.

Apple supply simply can’t meet the global demand for its own products, which has grown over the pandemic.

Long term, I look at this as a good problem, because the supply chain will get sorted, and bottlenecks will fix themselves.

CEO Tim Cook likes to say that Apple’s operational team is “world-class” and him being an operational guy himself originally, I can give him the benefit of the doubt.

There is nothing to worry about with Apple.

They remain incredibly profitable and efficient, and any short-term weakness is an appetizing buying opportunity for investors.

Mad Hedge Technology Letter

October 25, 2021

Fiat Lux

Featured Trade:

(HOW TO PLAY THE TECH EARNINGS SEASON)

(MSFT), (FB), (GOOGL), (AAPL), (SNAP)