Global Market Comments

September 9, 2019

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or SAVED BY A HURRICANE)

(FXB), (M), (XOM), (BAC), (FB), (AAPL),

(AMZN), (ROKU), (VIX), (GS), (MS),

Global Market Comments

September 9, 2019

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or SAVED BY A HURRICANE)

(FXB), (M), (XOM), (BAC), (FB), (AAPL),

(AMZN), (ROKU), (VIX), (GS), (MS),

This was the week when the stock market was saved by Hurricane Dorian.

Why a hurricane?

Because it gave President Trump something else to Tweet about beside China and Jay Powell. The White House went totally silent, at least on matters concerning the stock market. There, the focus instead turned on whether Trump predicted Dorian was going to hit Alabama (it didn’t).

Thank goodness for small favors.

Instead, investors got to hear about progress was purported to be made on the China trade talks with a possible October meeting.

It all reminds me of the 1968 Paris peace talks, which I visited, where I remember Ambassador Avril Harriman storming out of the Majestic Hotel with a very stern expression on his face. They had just spent a year arguing with the North Vietnamese over the shape of the table (they finally settled on an oval).

Brexit finally started lurching towards its inevitable demise. Hard Brexit failed in Parliament, a disaster for Prime Minister Boris Johnson, whose own party and even his own brother voted against him.

Elections will follow which will finally plunge a dagger through the heart of Britain’s attempt to leave the European Community. If this happens, it will be a huge positive for risk markets globally. This is the beginning of the end. Get ready to buy the pound (FXB).

The bad news? Don’t count on this happening again this week, unless we get another hurricane. When a stock market rally is led by sectors with the worst fundamentals, like retail (M), energy (XOM), and banks (BAC), you want to run a mile. It means the rally was driven by short-covering, we are now at a market high, and the short players have a ton of cash.

I have been pounded with questions all week if the bottom is in and if it’s time to load the boat with tech stocks yet again. I have to answer with a firm “Not yet!” We still have three weeks to go in September with plenty of time for more volatility.

If the Fed cuts interest rates by 25 basis points, the Dow average could crater by 1,000 points. If they don’t cut, which I give a 50/50 chance, it will be down by 2,000 points.

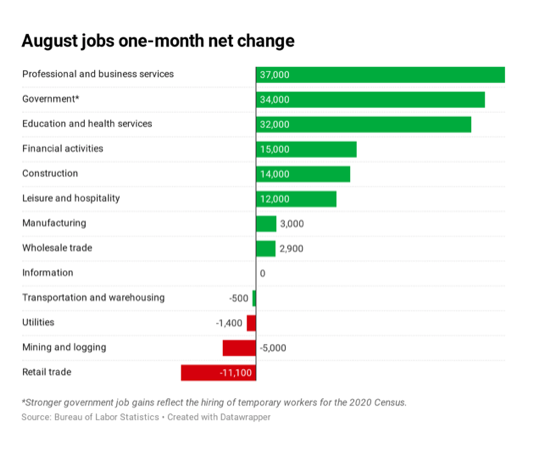

They will be encouraged to cut by an August Nonfarm Payroll Report that came in at a tepid 130,000. The headline Unemployment Rate remained unchanged at 3.7%, a 50-year low. Average Hourly Earnings were an inflationary 0.4%, or 3.2% YOY. June and July were revised down.

The 2020 census was a big factor in August, where the US government hired 25,000 workers to prepare for next year. Without this, August would have come in at a weak 105,000 jobs.

Manufacturing hiring amounted to only 3,000, while Retail lost 11,000 jobs for the seventh consecutive monthly decline. The broader U-6 “discouraged worker” unemployment rate rose from 7.0% to 7.2%.

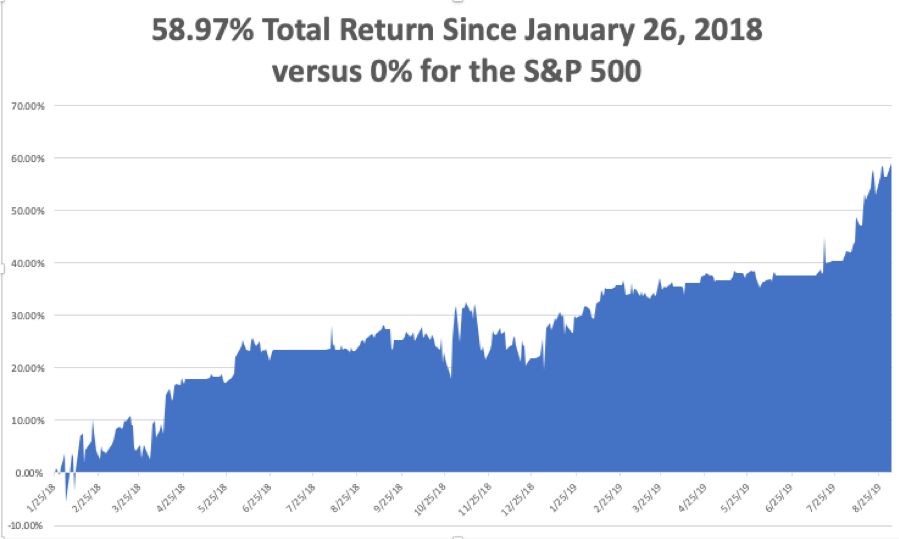

To demonstrate how much value you are gaining with this service, I generated the chart below. Since January 26, 2018 when the S&P 500 peaked, the total return has been zero, with a lot of heart-stopping volatility, including one 20% drawdown.

That has been the cost to the stock market of the trade war, which started only a few days later. The profit created by the Mad Hedge Fund Trader during the same period has been 58.97%.

You couldn’t even beat the Mad Hedge Fund Trader by pouring all your money into big technology stocks. Over the same time, Facebook (FB) fell 4.1%, Apple (AAPL) rose 21.7%, and Amazon (AMZN) by 22.2%.

The only way you could have topped my performance was to pour your life savings into Roku (ROKU), right when Amazon was about to put it out of business. Jeff Bezos partnered with Roku instead of delivering a 225% pop in the shares.

You might think such a performance is blown out of proportion, exaggerated, and fake. However, it is perfectly consistent with the numbers generated for the in-house trading books by senior traders at Goldman Sachs (GS) and Morgan Stanley (MS) where I come from.

In fact, during my day, if a trader earned less than 30% a year on his capital, he got fired or transferred over to covering retail accounts because the firm had so many better places to invest. They are also consistent with the performance of the top-end hedge managers, of which I used to be one.

Chinese Manufacturing Activity fell for four consecutive months taking the Purchasing Managers Index below a recessionary 50. If you wreck the economy of the world’s largest customer, the rest of the world goes into recession.

US Manufacturing hit a three-year low, the ISM Manufacturing PMI diving from an average 56.5 to 49.1 in August. Anything below 50 is a recession indicator. Hoping that China will bleed worse than us in a trade war is not a winning strategy. Stocks dove 300 points and the Volatility Index (VIX) shot up to $21 on the news. Avoid risk, as this is going to be a terrible month.

The prospect of a China meeting popped stocks 400 points, with an agreement to meet in October, citing progress on a phone call. Boy, I’m getting tired of this. When can we go back to looking at earnings, dividends, and book value?

The European Central Bank will almost certainly ease this week. It hasn’t worked for ten years so let’s try it again. They’re obviously not printing enough Euros. Overnight rates will fall from -0.4% to -0.6%. Some 30 billion euros a month will hit the economy in a new QE.

The Atlanta Fed downgraded the economy, cutting its Q3 GDP growth forecast from 2.0% to 1.5%. Expect a string of poor data points in the coming months as the delayed effect of an escalated trade war. However, the non-manufacturing service economy remains strong. That’s me, and probably you too.

The Mad Hedge Trader Alert Service has posted its best month in two years. Some 22 or the last 23 round trips, or 95.6%, have been profitable, generating one of the biggest performance jumps in our 12-year history.

My Global Trading Dispatch has hit a new all-time high of 334.48% and my year-to-date shot up to +34.35%. My ten-year average annualized profit bobbed up to +34.30%.

Better yet, since July 31, we generated a 20% profit for the trade alert service while the gain in the Dow Average was absolutely zero!

I raked in an envious 16.01% in August. All of you people who just subscribed in June and July are looking like geniuses. My staff and I have been working to the point of exhaustion, but it’s worth it if I can print these kinds of numbers.

As long as the Volatility Index (VIX) stays above $20, deep in-the-money options spreads are offering free money. I am now 40% long big tech. It rarely gets this easy.

The coming week will be a snore, as it always is after the jobs data.

On Monday, September 9 at 11:00 AM, August Consumer Inflation Expectations are out.

On Tuesday, September 10 at 12:00 PM, the NFIB Business Optimism Index for August is released.

On Wednesday, September 11, at 8:30 AM, the US Producer Price Index is announced.

On Thursday, September 12 at 8:30 AM, the Weekly Jobless Claims are printed. At the same time, the US Inflation Rate is published.

On Friday, September 13 at 8:30 AM, the US Retails Sales are printed. The Baker Hughes Rig Count follows at 2:00 PM.

As for me, I’ll be driving up to Lake Tahoe to make final preparations for the October 25-26 Mad Hedge Lake Tahoe Conference. A record number of black bears have been breaking into homes this summer and I just want to make sure my lakefront estate is OK.

It seems that Airbnb tenants have been leaving trails of cookies to their front doors and painting their refrigerators with peanut butter so they can get better selfies with their ursine neighbors.

Not a good idea.

I’ll be avoiding Interstate 80. A truck carrying 1,000 live chickens crashed there yesterday and the California Highway Patrol was last seen chasing them down the freeway.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

August 27, 2019

Fiat Lux

Featured Trade:

(FIVE STOCKS TO BUY AT THE BOTTOM),

(AAPL), (AMZN), (SQ), (ROKU), (MSFT),

(HOW TO EXECUTE A VERTICAL BULL CALL SPREAD)

(AAPL)

Global Market Comments

August 22, 2019

Fiat Lux

Featured Trade:

(WHAT THE NEXT RECESSION WILL LOOK LIKE),

(FB), (AAPL), (NFLX), (GOOGL), (KSS), (VIX), (MS), (GS),

(TESTIMONIAL)

Global Market Comments

August 21, 2019

Fiat Lux

Featured Trade:

(WHY YOU MIISED THE TECHNOLOGY BOOM AND WHAT TO DO ABOUT IT NOW),

(AAPL), (AMZN), (MSFT), (NVDA), (TSLA), (WFC), (FB)

Global Market Comments

August 8, 2019

Fiat Lux

Featured Trade:

(HOW TO KNOW IF THE BULL MARKET IS WELL AND TRULY OVER),

(THE TALE OF TWO ECONOMIES),

(FB), (AAPL), (AMZN)

I’m looking at my screens this morning and virtually every stock sold short by the Dairy of a Mad Hedge Fund Trader cratered to new six-month lows.

Call it lucky, call it fortuitous. All I know is that the harder I work the luckier I get.

If you are in the right economy, that of the future, you are having another spectacular year. If you aren’t, you are probably posting horrific losses for 2019. Call it the “Tale of two Economies.”

I suspected that this was setting up over the last couple of weeks. No matter how much bad news and uncertainty dumped on these companies, the shares absolutely refused to go down. Instead, they flat lined just below their 2019 highs. It was a market begging for a selloff.

When the Facebook (FB) hacking scandal hit, investors were ringing their hands about the potential demise of Mark Zuckerberg’s vaunted business model and the shares plunged to $123.

However, while analysts were making these dire productions, I knew that Facebook itself was signing a long-term lease for a brand new 46-story skyscraper in downtown San Francisco just to house its Instagram operations.

Months later, and the company that misused Facebook’s data, Steve Bannon’s Cambridge Analytica, is bankrupt, and (FB) is trading at $185, a new high. Facebook was right, and the Cassandras were wrong.

Amazon was given up for dead during the February melt down as the shares withered from a daily onslaught of presidential attacks threatening antitrust action. Today, the shares are up a mind-blowing 38% above those lows.

And when Apple announced its earnings, the shares tickled $222, putting it squarely back into the ranks of the $1 trillion club ($949 billion at today’s close).

It turns out that technology companies are immune from most of the negative developments that have caused the rest of the stock market to drag. I’ll go through these one at a time.

Falling Interest Rates

Tech companies are sitting gigantic cash mountains, some $245 billion in Apple’s case, which means that as net lenders to the credit markets, they are beneficiaries of the credit markets. This makes tech companies immune from the credit problems that will demolish old economy industries during the next rate spike.

Rising Oil Prices

While tech companies are prodigious consumers of electricity, many power these with massive solar arrays and they sell periodic excess power to local utilities. So as net energy producers, they profit from rising energy prices.

Rising Inflation

Since the output of technology companies is entirely digital, they can handily increase productivity faster than the inflation rate, whatever it is. Traditional old economy companies, like industrials and retailers can’t do this.

Remember that while analogue production grows linearly, digital production grows exponentially, enabling tech companies to handily beat the inflation demon, leaving others behind in the dust.

Share Buybacks

While technology companies account for only 26% of the S&P 500 stock market capitalization, they generate 50% of the profits. Thanks to the massive tax breaks and low tax repatriation of foreign profits enabled by the 2017 tax bill, share buybacks are expected to rocket from $500 billion to $1 trillion this year. Companies repurchasing their own shares have become the sole net buyers of equities in 2019.

And companies with the biggest profits buy back the most stock. This has created a virtuous cycle whereby higher share prices generate more buybacks to create yet higher share prices. Old economy companies with lesser profits are buying back little, if any, of their own shares.

Of course, tech companies are not without their own challenges. For a start, they have each other to worry about. FANGs will simultaneously cooperate with each other in a dozen areas, while fight tooth and nail and sue on a dozen others. It’s like watching Silicon Valley’s own version of HBO’s Game of Thrones.

Also, occasionally, the tech story becomes so obvious to the unwashed masses that it creates severe overbought conditions and temporary peaks, like we saw in January.

Mad Hedge Technology Letter

August 5, 2019

Fiat Lux

Featured Trade:

(THE CHINA TARIFF BOMBSHELL AND TECHNOLOGY),

(AAPL), (NVDA), (INTC), (MU), (WDC), (BBY)

With one little tweet, the state of technology and the companies that rely on the public markets that serve them went haywire.

U.S. President Donald Trump levied another 10% on the $300 billion that had not been tariffed up yet compounding the misery for anyone who has any vested interest in trade with mainland China.

The tariffs will take effect on September 1st.

How does this shake out for American technology?

Any brand tech name that has substantial supply chain operations can kiss their stay in the Middle Kingdom goodbye.

If management didn’t understand that before, then it's clear as night that they need to shift their supply chain out of the reaches of the Chinese communist party.

The U.S. Administration tripling down on China being our archnemesis means that any sort of cross-border economic trade or cultural exchange will be viewed through the prism of warped geopolitics.

The U.S. President Donald Trump has in fact taken a page out of the Chinese playbook turning everything he sees and touches into a transactional tool for what he is pursuing at the time or in the future.

Specific companies facing the wrath of the tariffs are companies as conspicuous as Apple filtering down to the SMEs that make local business local.

Semiconductor chips are a huge loser in this new development as the price of electronic goods will rise with the tariffs.

If you want a name that lies in the heart of electronic consumer goods, then BestBuy (BBY) would encapsulate this thesis and unsurprisingly they were taken out to the back of the woodshed and taught a lesson dropping 10% on the news.

Any technology outfit that imports goods from China will be hit as well and this means semiconductor chips along the lines of Nvidia (NVDA), Intel (INTC), Western Digital (WDC) and Micron (MU) among others.

Chips are the meat and bones that go into end products like iPads and a slew of smart devices.

Demand will be hit because of the cost of producing these types of consumer products will rise.

The softness is showing up in the numbers with Apple’s iPhone revenue down 12% year-over-year.

Samsung of Korea also showed that this isn’t just an American problem with their semiconductor division’s operating profits down 71% year-over-year.

The Korean conglomerate is in a spat with the Japanese government over war crimes from the second world war causing the Japanese government to bottleneck the supply of chemicals needed to produce high-level semiconductor chips.

The export restriction will drag down SK Hynix display business who is one of the largest producers of DRAM chips and also a Korean company.

Consumers are also using their phones longer with Apple iPhone customers holding their device up to 4 years delaying the refresh cycle.

The company that Steve Jobs built will have to repurpose themselves for a brave new tech landscape that includes heavier regulation, trade tariffs, and device saturation.

When investors talk about the “low hanging fruit,” at this point, Apple isn’t one of them.

And if you think the services business is a cakewalk, ponder about how many apps and behemoths that spit out a whole lineup of apps.

Apple still has its ecosystem and should guard it with its life, this is the same ecosystem that can charge Google around $10 billion per year to slap on Google search as the primary search engine on Apple devices.

Expect tech to telegraph a deceleration in revenue for the last quarter and next year.

The tech environment is brittle at this point and uncertainty wafts in the air like a hot stack of pancakes.

Global Market Comments

July 25, 2019

Fiat Lux

Featured Trade:

(HOW TO HEDGE YOUR CURRENCY RISK)

(FXA), (FXC), (UUP)

(HOW TO EXECUTE A VERTICAL BULL CALL SPREAD)

(AAPL)