Mad Hedge Technology Letter

July 24, 2019

Fiat Lux

Featured Trade:

(CIAO SILICON VALLEY),

(AAPL), (CRM), (MSFT), (FB), (AMZN), (GOOGL)

Mad Hedge Technology Letter

July 24, 2019

Fiat Lux

Featured Trade:

(CIAO SILICON VALLEY),

(AAPL), (CRM), (MSFT), (FB), (AMZN), (GOOGL)

Bridgewater Associates Founder Ray Dalio carefully articulates an economic landscape in which the unrelenting chase for short-term tech profits finally catches up meaningfully with the gyrations of tech shares.

All of this could come home to roost and the early manifestations can be found in the housing migratory trends.

The robust housing demand, lack of housing supply, mixed with the avalanche of inquisitive tech money will propel these housing markets to new heights and this phenomenon is happening as we speak.

Salesforce Founder and CEO Marc Benioff has lamented that San Francisco, where ironically he is from, is a diabolical “train wreck” and urged fellow tech CEOs to “walk down the street” and see it with their own eyes to observe the numerous homeless encampments dotted around the city limits.

The leader of Salesforce doesn’t mince his words when he talks and beelines to the heart of the issues.

After relinquishing some of his CEO duties to newly anointed Co-CEO Keith Block, Benioff will have the operational time and a wealth of resources to get on top of the pulse of not only tech issues but bigger picture stuff and he now has a mouthpiece for it with Time Magazine which he and his wife recently bought.

In condemning large swaths of the beneficiaries of the Silicon Valley ethos, he has signaled that it won’t be smooth sailing forever.

In tech wonderland, and he urged companies to transform their business model if they are irresponsible with user data.

The tech lash could get messier this year because companies that go rogue with personal data will face a cringeworthy reckoning as the techlash fury seeps into government policy and the social stigma worsens.

I have walked around the streets of San Francisco myself.

Places around Powell Bart station close to the Tenderloin district are eyesores littered with used syringes that lay in the gutter.

South of Market Street isn’t a place I would want to barbecue on a terrace either.

Summing it up, the unlimited tech talent reservoir that Silicon Valley gorged on isn’t flowing anymore because people don’t want to live there now.

This tech talent, equipped with heart-tugging stories from siblings and anecdotes from classmates getting shafted by the San Francisco dream, has recently put the Bay Area in the rear-view mirror for many who would have stayed if it were 20 years ago.

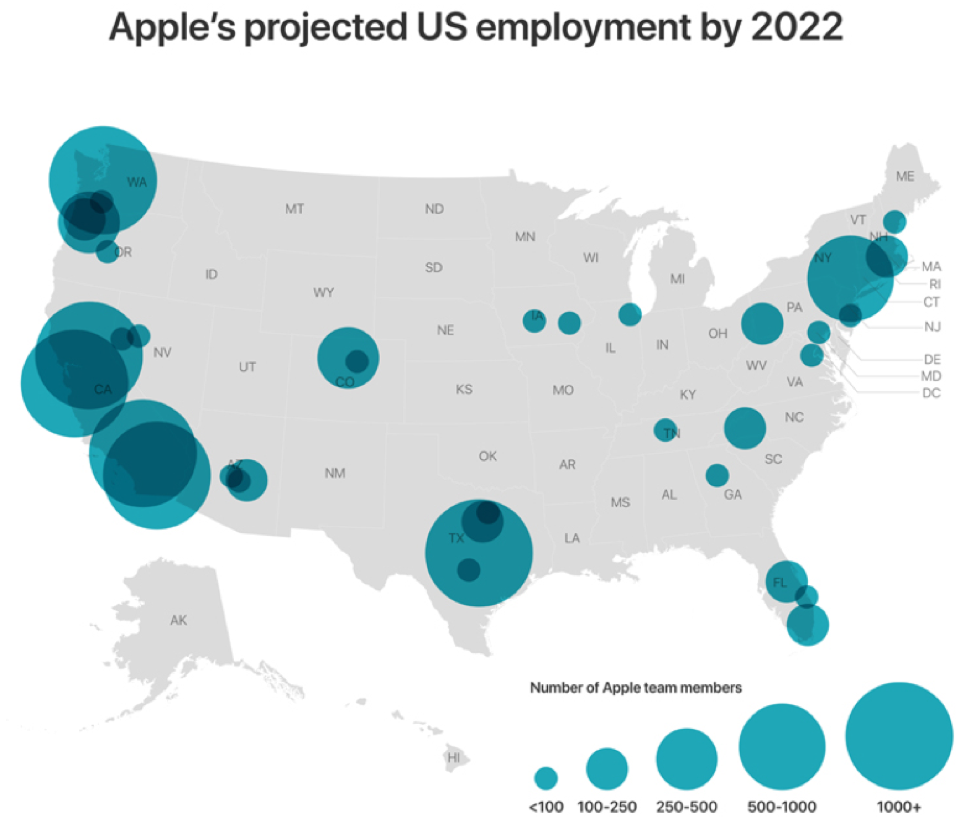

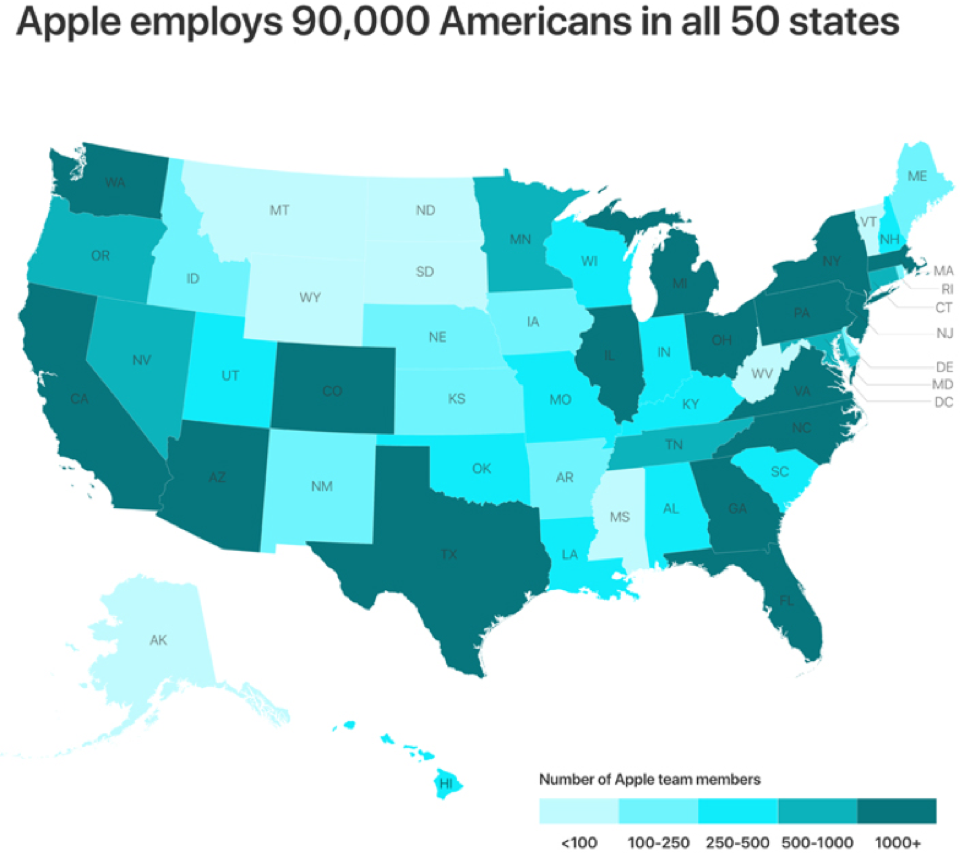

This is exactly what Apple’s $1 billion investment into a new tech campus in Austin, Texas and Amazon adding 500 employees in Nashville, Tennessee are all about.

Apple also added numbers in San Diego, Atlanta, Culver City, and Boulder just to name a few.

Apple currently employs 90,000 people in 50 states and is in the works to create 20,000 more jobs in the US by 2023.

Most of these new jobs won’t be in Silicon Valley.

Since the tech talent isn’t giddy-upping into Silicon Valley anymore, tech firms must get off their saddle and go find them.

The tables have turned but that is what happens when the heart of western tech becomes unlivable to the average tech worker earning $150,000 per year.

Driving out young people who envision a long-term future elsewhere than the San Francisco Bay Area forces Silicon Valley to adapt to the new patterns revealing themselves.

Sacramento has experienced a dizzying rise of newcomers from the Bay Area itself.

Some are even commuting, making that 60-mile jaunt past Davis, but that will give way to entire tech operations moving to the state capitol.

Millennials are reaching that age of family formation and they are fleeing to places that are affordable and possible to become a new home buyer.

These are some of the practical issues that tech has failed to embrace and to maintain the furious pace of growth that investors' capricious expectations harbor.

Silicon Valley will have to become more practical adding a dash of empathy as well instead of just going by the raw and heartless data.

We aren’t robots yet, and much of the world still augurs to emotional decisions and disregards the empirical data.

But, instead of physical offices being planted in the Bay Area, the tech industry will heed way to the “spirit” of Silicon Valley with offices in far-flung places.

And remember that all of these new tech talent strongholds will need housing, and housing that an IT worker making $150,000 per year desires.

No wonder why San Jose real estate has dropped in the past year, people and their paychecks are on the way out.

Global Market Comments

July 19, 2019

Fiat Lux

Featured Trade:

(DON’T MISS THE JULY 24 GLOBAL STRATEGY WEBINAR)

(WHAT’S HAPPENED TO APPLE?), (AAPL)

(STORAGE WARS)

(MSFT), (IBM), (CSCO), (SWCH)

One of the great mysteries of the tech world has at last been answered.

Apple’s brand new spaceship-designed headquarter, one of the world’s most valuable buildings, has finally had a value put on it.

New figures released this week show the tech giant’s circular headquarters in Cupertino, CA was assessed at a breathtaking $3.6 billion by Santa Clara County for property tax purposes. The valuation doesn’t perfectly coincide with its market value — how much it would sell for — but is based off a detailed appraisal of the building, which opened in 2017.

If you include computers, furniture, and even farm equipment to take care of the property’s abundant peach trees, the figure rises to $4.17 billion for the fiscal year that ended in June, the assessor’s office said.

Beyond its giant 2.8 million-square-foot size, Apple Park’s high-end materials, abundant glass, and intricate design make it a standout in Silicon Valley. The building is so big it even has its own weather.

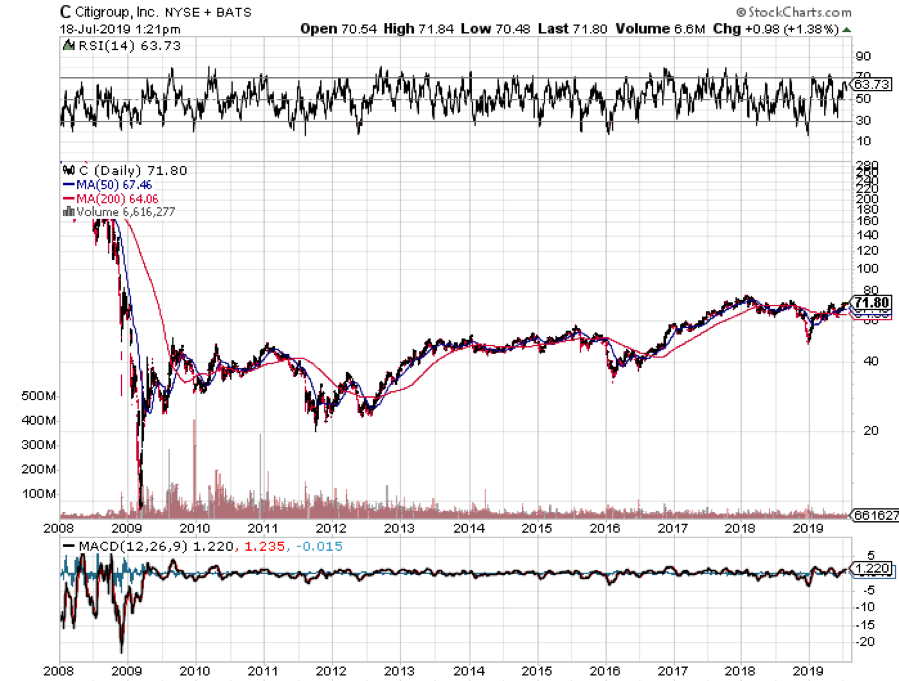

Unfortunately, the share prices of companies that spend billions on flashy new designer headquarters do not have a great history. Ride around Manhattan in an Uber cab and you’ll quickly understand that time has not been kind to the extravagant: the Chrysler Building, the Pan Am Building, and the AT&T building to name just a few.

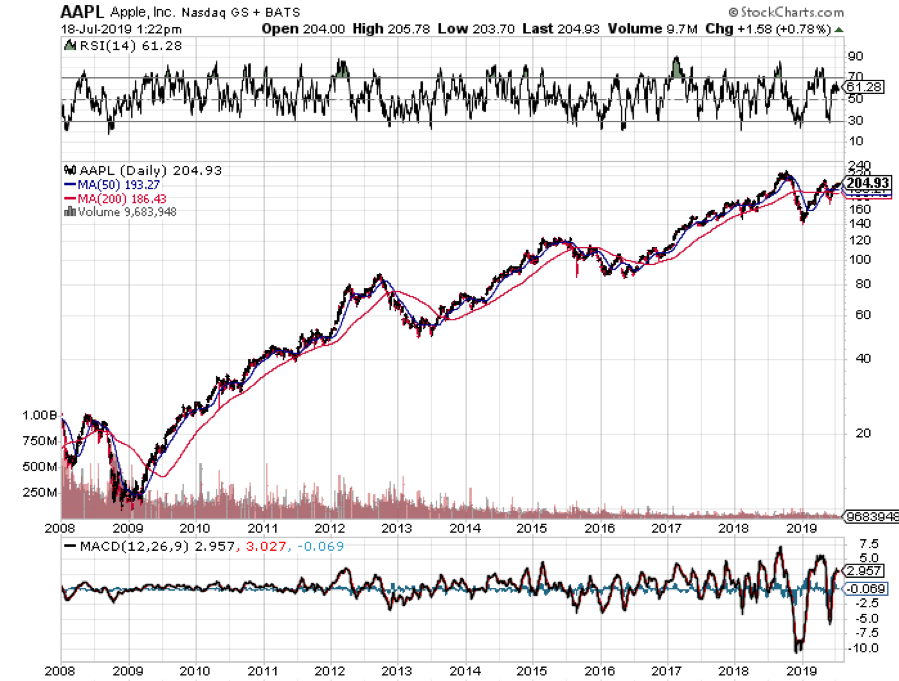

Citicorp’s HQ, with its horizon-defining slant-edged roof, is still in business, but the stock is still down 75% from its pre-crash high. Is Apple headed in the same direction?

Looking at the share price performance of the past year, which has been zero, you might be forgiven for thinking so. Other tech stocks have risen by 50% or more during the same period.

Apple Park is among the world’s dozen most expensive buildings despite its relatively modest four-storey height.

America’s tallest spire, the 1,776-foot One World Trade Center in New York, cost $3.9 billion to build according to the Port Authority of New York and New Jersey which owns the building and has 3.5 million square feet. Singapore’s Marina Bay Sands resort reportedly topped $5 billion in costs, while Finland’s Olkiluoto 3 nuclear reactor exceeded $6 billion.

Saudi Arabia’s holy city of Mecca is home to two of the most valuable buildings in the world: the $15 billion Abraj Al Bait Towers and the $100 billion Great Mosque of Mecca.

Apple Park was assessed at more than twice the amount of Salesforce Tower, San Francisco’s tallest building, which was valued at $1.7 billion by San Francisco. Salesforce Tower has about half as much office space as Apple Park despite being 57 stories taller.

With property taxes in Santa Clara County running around 1.25%, Apple would owe around $50 million annually.

The building is a manageable expense for Apple’s profit machine. In its most recent quarter, Apple reported a mind-numbing $58 billion in revenue and $11.5 billion in net income.

Apple was Santa Clara County’s largest property taxpayer for the 2017-18 fiscal year, with $56 million in taxes paid.

Investors have been frustrated with Apple’s recent performance, although it did make back most of the 40% hickey it suffered last fall.

Its business plan seems well on track, shifting from a hardware company to one that focuses on software and services. If anything, the shift has been taking place faster than expected, with the cloud, iTunes, Apple Wallet, Apple Care, the App Store, and other services accounting for a growing share of earnings.

All will become clear when the company announces their Q3 earnings on Tuesday, July 30 after the stock market close.

No, I think the problem with Apple is that it is suffering from the China Disease. Employing a million people who produce 225 million iPhones a year, Apple is the preeminent hostage in the US-China trade dispute. That, undoubtedly, has been a dead weight on the shares.

However, after covering this field for half a century, I can tell that trade wars start, trade wars play out, and trade wars end. Unlike other trade wars, this one has a specific end date. That would be on Wednesday, January 20, 2021, or in 18 months, the date of the next presidential inauguration.

As for me, I am waiting to upgrade my current iPhone X until it includes 5G wireless technology early next year. I bet 225 million others are as well. Dump the trade war and Apple shares could rocket up towards my old long-term target of $250 a share in a heartbeat.

By the way, there is one other headquarter that may be about to join the dustbin of history. That would be 725 Fifth Avenue, NY, NY 10022, which has been appraised at a mere $371 million and carries a hefty $100 million in debt. In is now partly owned by the US Justice Department, which will soon sell its stake.

Locals know it as Trump Tower.

Global Market Comments

July 12, 2019

Fiat Lux

Featured Trade:

(THE QUANTUM COMPUTER IN YOUR FUTURE),

(AMZN), (GOOG),

(THE WORST TRADE IN HISTORY), (AAPL)

Mad Hedge Technology Letter

July 5, 2019

Fiat Lux

Featured Trade:

(THE BALL IS IN NETFLIX’S COURT)

(NFLX), (DIS), (AAPL), (IQ), (KHC)

Being as volatile as it is, investors are afforded ample opportunity to get into one of the premium tech stocks in the land Netflix (NFLX).

Chasing this one higher is a dangerous thought, as habitual 30% dips is part and parcel of being attached to this supreme online streaming stock.

December of 2018 gave you that sinking feeling when Netflix dropped off a cliff dipping to $260 but spiking after the turn of the year as the Fed swiveled on a dime to save the equity market from implosion.

Let’s make no bones about it, the long-term narrative for Netflix is intact as it’s ever been.

The company simply makes a great product, period, and systematically taps endless demand.

What many cable companies don’t understand is that you cannot make a high-quality film product that wedges in annoying commercials and equally as obnoxious, dictate the window of time in which they should watch the content.

Optionality is value and Netflix has this spot on.

I know many Millennial consumers that would rather jump off a building than subject themselves to commercials.

These factors erode the quality of the product just as if an employer would dictate to one of his or her employees that wanted to take a vacation to Africa.

But the vacation to Africa would have some strings attached.

He or she would only be able to visit at the height of summer in 120-degree Fahrenheit weather while every activity he or she chose to do, would be pre-empted by numerous advertisements that he or she must be shown.

Consumers don’t need these sideshows anymore; the world has developed away from these models and corporates have lost this control.

The loss of corporate control of the consumers is because the internet gives consumers millions of different options at the tip of their fingers.

Tapping into the optionality and the habits that revolve around it is paramount to corporate America.

This is the same reason why big box food companies like Kraft Heinz (KHC) is getting smacked around, consumers have better options and are more aware of them because of technology.

Another example of corporate miscalculation comes in the form of supply chains being redirected from China to South East Asia.

It was clear as day that during my time in China that companies were making a terrible mistake going into China in the first place.

This shows how many corporates are dragged down by a lack of vision and do an awful job of anticipating paradigm shifts that are becoming more common because of the accelerating rate of change of the corporate climate, weather, technology, rule of law, and human migration.

Netflix is effectively blocked from China and China has its own Netflix called iQIYI (IQ), they had no chance from the beginning like Google, Amazon, Facebook, and the many other American tech firms.

Netflix’s business model now has scale working for them and growth numbers will be the main recipients going forward if they focus on high quality content.

That means expect high pay packages to the best media talent in the world.

They can afford to pay a tier 1 actor $50 million per movie because the data buttresses this strategy.

At the same time, Netflix is crushing competition by hoarding the talent with extraordinary pay packages while allowing these highly paid specialists 100% creative control over what they do.

Who would want to work for a company that paid more than double and whose management gave them free reign on creative decisions?

Sounds like an artist’s dream and it’s exactly that for actors like Will Smith who have signed onto Netflix’s project.

I would even suggest that Netflix needs to overpay actors just for the reason of taking them off the market for competitors.

This truly is the lucrative golden age for actors, producers, and directors who are the top 1% of their craft, but for everyone else, it’s a hard slog.

This usually means becoming a tier 1 actor before the migration to online streaming happened.

The picture I am painting is that Netflix’s success and future prospects aren’t about Disney or other competitors, but entirely about them.

He who has the most chips at the table with the best cards is in best position to win and the same goes for Netflix.

The rest of the bunch like Apple (AAPL) and Disney who are late to the party will be feeding off the rest of what Netflix cannot exploit and that’s the best-case scenario.

Disney should be able to have moderate success with its array of great movie, television, and sports content.

I’d be surprised if Disney failed because they possess the ingredients to concoct a delicious cocktail.

Apple has a harder proposition because of the lack of entertainment value in their content. They are still tied to the hardware sales and much of the service sales come from their app store and servicing the hardware.

But Apple does have money, and a lot of it to throw at the problem, but I don’t believe CEO of Apple Tim Cook is the right man to navigate through the travails of the online content world. He’s an operations guy and has never proved anything more than that.

Netflix still has substantial opportunity to grow its brand and the runway is long.

The demand for watching great original movies and television programs without commercials whenever consumers want is still in the first innings.

Even though Disney will remove some non-original content from Netflix’s platform, the content spend on a massive pipeline of new projects will more than fill the void left by Disney’s content.

In fact, Netflix should thank Disney for all those years that Disney allowed them to build their brand through 3rd party premium content like the television program Friends.

I believe Netflix does not need 3rd party content anymore, that is how much Netflix has bolted ahead in the past few years.

The company has introduced price hikes with its 4K premium package going from $14 to $16 per month.

But Netflix is still underpricing itself to the consumer to grab market share, and there is still pricing headway in the future if the company wants it.

In the coming months, Netflix plans to offer more detailed reporting on its metrics and the transparency will give investors even more insight into why this company is brilliant.

I believe the numbers will show that Netflix is absolutely killing it.

As for the trading, Netflix has settled in a range of $320 to $380 and any dips to the $340 range should be quite appetizing.

Add incrementally and use any large dip to drop your cost basis.

Stand aside if you cannot handle heightened volatility.

Mad Hedge Technology Letter

July 3, 2019

Fiat Lux

Featured Trade:

(CHIPS ARE BACK FROM THE DEAD)

(XLNX), (HUAWEI), (AAPL), (AMD), (TXN), (QCOM), (ADI), (NVDA), (INTC)

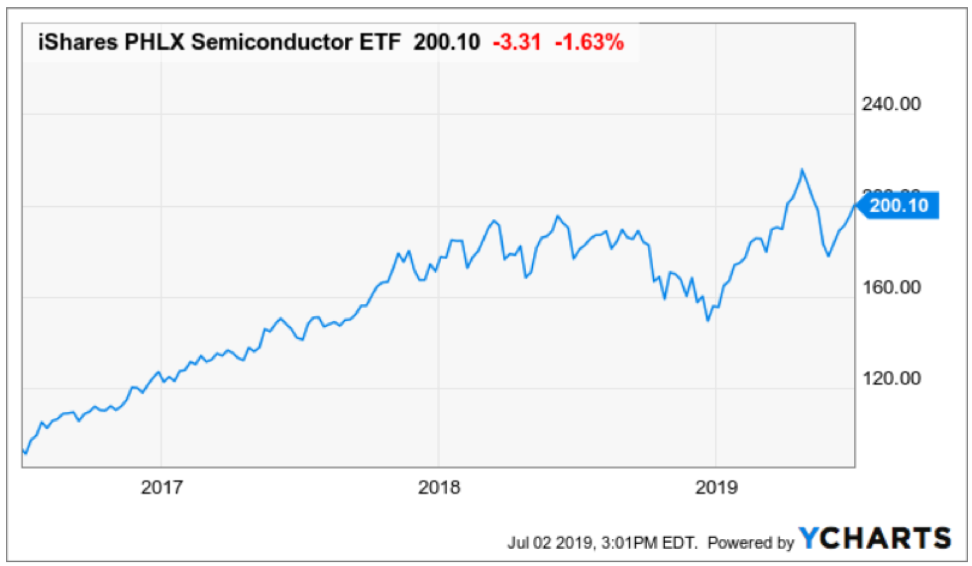

The overwhelming victors of the G20 were the semiconductor companies who have been lumped into the middle of the U.S. and China trade war.

Nothing substantial was agreed at the Osaka event except a small wrinkle allowing American companies to sell certain chips to Huawei on a limited basis for the time being.

As expected, these few words set off an avalanche of risk on sentiment in the broader market along with allowing chip companies to get rid of built-up inventory as the red sea parted.

Tech companies that apply chip stocks to products involved with value added China sales were also rewarded handsomely.

Apple (AAPL) rose almost 4% on this news and many investors believe the market cannot sustain this rally unless Apple isn’t taken along for the ride.

Stepping back and looking at the bigger picture is needed to digest this one-off event.

On one hand, Huawei sales comprise a massive portion of sales, even up to 50% in Nvidia’s case, but on the other hand, it is the heart and soul of China Inc. hellbent on developing One Belt One Road (OBOR) which is its political and economic vehicle to dominate foreign technology using Huawei, infrastructure markets, and foreign sales of its manufactured products.

Ironically enough, Huawei was created because of exactly that – national security.

China anointed it part of the national security apparatus critical to the health and economy of the Chinese communist party and showered it with generous loans starting from the 1980s.

China still needs about 10 years to figure out how to make better chips than the Americans and if this happens, American chip sales will dry up like a puddle in the Saharan desert.

Considering the background of this complicated issue, American chip companies risk being nationalized because they are following the Chinese communist route of applying the national security tag on this vital sector.

Huawei is effectively dumping products on other markets because private companies cannot compete on any price points against entire states.

This was how Huawei scored their first major tech infrastructure contract in Sweden in 2009 even though Sweden has Ericsson in their backyard.

We were all naïve then, to say the least.

Huawei can afford to take the long view with an Amazon-like market share grab strategy because of possessing the largest population in the world, the biggest market, and backed by the state.

Even more tactically critical is this new development crushes the effectiveness of passive investing.

Before the trade war commenced, the low-hanging fruit were the FANGs.

Buying Google, Amazon, Apple, Netflix, and Facebook were great trades until they weren’t.

Things are different now.

Riding on the coattails of an economic recovery from the 2008 housing crisis, this group of companies could do no wrong with our own economy flooded with cheap money from the Fed.

Well, not anymore.

We are entering into a phase where active investors have tremendous opportunities to exploit market inefficiencies.

Get this correct and the world is your oyster.

Get this wrong, like celebrity investors such as John Paulson, who called the 2008 housing crisis, then your hedge fund will convert to a family office and squeeze out the extra profit through safe fixed income bets.

This is another way to say being put out to pasture in the financial world.

My point being, big cap tech isn’t going up in a straight line anymore.

Investors will need to be more tactically cautious shifting between names that are bullish in the period of time they can be bullish while escaping dreadful selloffs that are pertinent in this stage of the late cycle.

In short, as the trade winds blow each way, strategies must pivot on a dime.

Geopolitical events prompted market participants to buy semis on the dips until something materially changes.

This is the trade today but might be gone with one Tweet.

If you want to reduce your beta, then buy the semiconductor chip iShares PHLX Semiconductor ETF (SOXX).

I will double down in saying that no American chip company will ever commit one more incremental cent of capital in mainland China.

That ship has sailed, and the transition will whipsaw markets because of the uncertainty in earnings.

The rerouting of capital expenditure to lesser-known Asian countries will deliver control of business models back to the corporation’s management and that is how free market capitalism likes it.

Furthermore, the lifting of the ban does not include all components, and this could be a maneuver to deliver more face-saving window-dressing for Chairman Xi.

In reality, there is still an effective ban because technically all chip components could be regarded as connected to the national security interests of the U.S.

Bullish traders are chomping at the bit to see how these narrow exemptions on non-sensitive technologies will lead to a greater rapprochement that could include the removal of all new tariffs imposed since last summer.

The risk that more tariffs are levied is also high as well.

I put the odds of removing tariffs at 30% and I wouldn’t be surprised if the administration doubles down on China to claim a foreign policy victory leading up to the 2020 election which could be the catalyst to more tariffs.

It’s difficult to decode if U.S. President Trump’s statements carry any real weight in real time.

The bottom line is the American government now controls the mechanism to when, how, and the volume of chip sales to Huawei and that is a dangerous game for investors to play if you plan on owning chip stocks that sell to Huawei.

Artificial intelligence or 5G applications chips are the most waterlogged and aren’t and will never be on the table for export.

This means that a variety of companies pulled into the dragnet zone are Intel (INTC), Nvidia (NVDA), and Analog Devices (ADI) as companies that will be deemed vital to national security.

These companies all performed admirably in the market following the news, but that could be short lived.

Other major logjams include Broadcom’s future revenue which is in jeopardy because of a heavy reliance on Huawei as a dominant customer for its networking and storage products.

Rounding out the chip sector, other names with short-term bullish price action are Qualcomm (QCOM) up 2.3%, Texas Instruments (TXN) up 2.6%, and Advanced Micro Devices (AMD) up 3.9%.

(AMD) is a stock I told attendees at the Mad Hedge Lake Tahoe conference to buy at $18 and is now above $31.

Xilinix (XLNX) is another integral 5G company in the mix that has their fortunes tied to this Huawei mess.

Investors must take advantage of this short-term détente with a risk on, buy the dip trade in the semi space and be ready to rip the cord on the first scent of blood.

That is the market we have right now.

If you can’t handle this environment when there is blood in the streets, then stay on the sidelines until there is another market sweet spot.

Mad Hedge Technology Letter

July 1, 2019

Fiat Lux

Featured Trade:

(THE DEATH OF HARDWARE)

(AAPL), (CRM), (NFLX), (HUAWEI)