Mad Hedge Technology Letter

May 8, 2019

Fiat Lux

Featured Trade:

(ELBOWED OUT OF THE WAY BY APPLE)

(SPOT), (AAPL)

Mad Hedge Technology Letter

May 8, 2019

Fiat Lux

Featured Trade:

(ELBOWED OUT OF THE WAY BY APPLE)

(SPOT), (AAPL)

Global Market Comments

May 7, 2019

Fiat Lux

Featured Trade:

(HOW TO EXECUTE A VERTICAL BULL CALL SPREAD)

(AAPL)

(THE CODER BOOM)

Global Market Comments

May 6, 2019

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, OR HERE’S ANOTHER BOMBSHELL),

(DIS), (QQQ), (AAPL), (INTU), (GOOGL), (LYFT), (UBER), (FCX))

I was all ready to write this week that massive monetary stimulus created by the Federal Reserve will cause the stock market to continue its slow-motion melt up.

The president had other ideas.

As of this writing, the US will impose without warning a surprise 25% increase in tariffs on $200 billion worth of Chinese imports, effective Friday, or in four days.

Clearly, the trade negotiations are not going as well as advertised by the administration. My bet is that the stock market won’t like this. All I can say is that I’m glad I’m 90% in cash and 10% in a Walt Disney vertical bull call spread that expires in nine trading days.

The bigger and unanswerable question is whether this is just a negotiating strategy already well known by the Bronx Housing Authority that sets up a nice dip to buy? Or is it this the beginning of a long overdue summer correction?

Nobody knows.

Certainly, the rally was getting long in the tooth, rising almost every day in 2019, with NASDAQ reaching new all-time highs. Those who kept their big-cap technology stock through the sturm und drang of the December meltdown have been rewarded handsomely. Index players reigned supreme.

However, we live in unprecedented times. Never before has a stock market received this much artificial stimulus at an all-time high unless you hark back to the Tokyo 1989 top. Japanese shares are now trading at 43% lower than that high….30 years later. We all know that our own decade-old bull market will eventually end in tears, but will it be in days, weeks, months, or years?

I had plenty of great wisdom, wonderful sector selections, colorful witticisms, and killer stock picks to serve up to you this week, but they have all be outrun by events. There’s nothing to do now but wait and see how the market responds to this tariff bombshell at the Monday morning opening.

After three months of decidedly mixed data, the information flow on the economy suddenly swung decidedly to the positive. The jobs data could have been more positive.

Of course, the April Nonfarm Payroll Report was a sight to behold. It came in at 263,000, about 80,000 more than expected, and more than makes up for last month’s dismal showing. It was a bull’s dream come true. This is what overheating looks like fueled by massive borrowing. Play now, pay later.

The headline Unemployment Rate fell a hefty 0.2% to 3.6%, the most since 1969 when the Vietnam War was raging, and the economy was booming. I remember then that Levi Strauss (LEVI) was suffering from a denim shortage then because so much was being sent to Southeast Asia to use as waterproof tarps. Wages rose 3.2% YOY.

Professional and Business Services led at a massive 76,000 jobs, Construction by 33,000 jobs, and Health Care by 27,000 jobs. Retail lost 12,000 jobs.

The ADP came in at a hot 275,000 as the private hiring binge continues. Then the April Nonfarm Payroll Report blew it away at 263,000. The headline unemployment rate plunged to a new 49-year low at 3.6%.

Consumer Spending hit a decade high, up 0.9% in March while inflation barely moved. Is Goldilocks about to become a senior citizen?

Apple (AAPL) blew it away with a major earnings upside surprise. The services play is finally feeding into profits. Stock buybacks were bumped up from $100 billion to $150 billion. Don’t touch (AAPL) up here with the stock just short of an all-time high. How high will the shares be when Apple’s revenue split between hardware and software revenues is 50/50?

Pending Home Sales jumped 3.8% on a signed contract basis. No doubt the market is responding to the biggest drop on mortgage rates in a decade. At one point, the 30-year fixed rate loan fell as low as 4.03%. Avoid housing for now, it’s still in a recession.

Topping it all off, the Fed made no move on interest rates. Like this was going to be a surprise? This may be the mantra for the rest of 2019. The big revelation that the Fed will start ending quantitative tightening now and not wait until September, as indicated earlier. More rocket fuel for the stock market. Let the bubble continue.

Uber (UBER) hit the Road for its IPO with valuations being cut daily, from a high of $120 billion to a recent low of $90 billion. The issue goes public on Friday morning. Rival Lyft (LYFT) definitely peed on their parade with their ill-fated IPO plunging 33%.

It wasn’t all Champaign and roses. San Francisco home prices fell for the first time in seven years. The median price is now only $830,000, down 0.1% YOY. Back up the truck! Clearly a victim of the Trump tax bill, this market won’t recover until deductions for taxes are restored. That may take place in two years….or never!

The Mad Hedge Fund Trader suffered a modest setback with the sudden collapse of copper prices last week, thus giving up all its profit in Freeport McMoRan (FCX). Global Trading Dispatch closed the week up 14.48% year to date and is down -1.48% so far in May. My trailing one-year retreated to +18.85%.

Reflecting the huge sector divergence in the market, the Mad Hedge Technology Letter leaped to another new all-time high on the back of two new very short-term positions in Intuit (INTU) and Google (GOOG), which we picked up after the earnings debacle there. Some 11 out of 13 Mad Hedge Technology Letter round trips have been profitable this year.

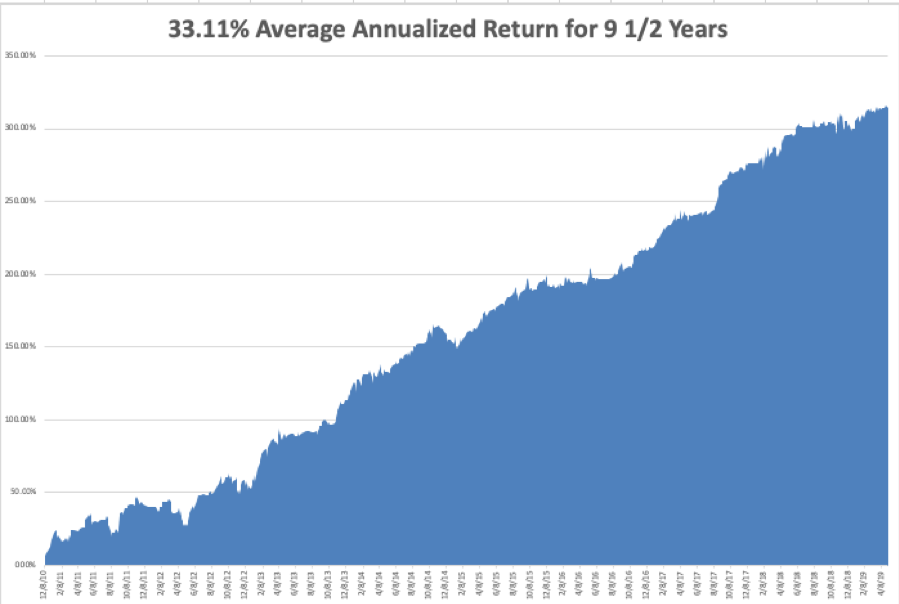

My nine and a half year profit shrank to +314.62%. The average annualized return backed off to +33.11%. With the markets at all-time highs and my Mad Hedge Market Timing Index forming a 2 ½ month high, I am now 90% in cash with Global Trading Dispatch and 80% cash in the Mad Hedge Tech Letter.

The coming week will be pretty boring after last week’s excitement, at least on the hard data front.

On Monday, May 6, Occidental Petroleum (OXY), now engaged in a ferocious takeover battle for Anadarko, reports. So does (AIG).

On Tuesday, May 7, 3:00 PM EST, we obtain March Consumer Credit. (LYFT), one of the worst performing IPOs this year, gives its first ever earnings report.

On Wednesday, May 8 at 2:00 PM, we get the most important earnings report of the week with Walt Disney (DIS), along with (ROKU).

On Thursday, May 9 at 8:30 the Weekly Jobless Claims are produced. At the same time, we get the March Producer Price Index. Dropbox (DBX) reports.

On Friday, May 10 at 8:30 AM, we get the Consumer Price Index. The Baker-Hughes Rig Count follows at 1:00 PM. (UBER)’s IPO will be priced at the opening. Viacom (VIA) Reports.

As for me, I’ll be watching the Kentucky Derby on Saturday. The field is wide open, now that the favorite, Omaha Beach, has been scratched.

As I will be attending the Las Vegas SALT conference during the coming week, the Woodstock of hedge fund managers, I will take the opportunity to rerun some of my oldies but goodies. We also have recently enjoyed a large number of new subscribers so I will be publishing several basic training pieces.

Maybe it was something I said?

For more on the SALT conference, please click here (you must be logged in to your account to access this piece).

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

May 3, 2019

Fiat Lux

Featured Trade:

(LAST CHANCE TO ATTEND THE LAS VEGAS MAY 9 GLOBAL STRATEGY LUNCHEON)

(APRIL 3 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (LYFT), (TSLA), (TLT), (XLV), (UBER),

(AAPL), (AMZN), (MSFT), (EDIT), (SGMO), (CLLS)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader May 1 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

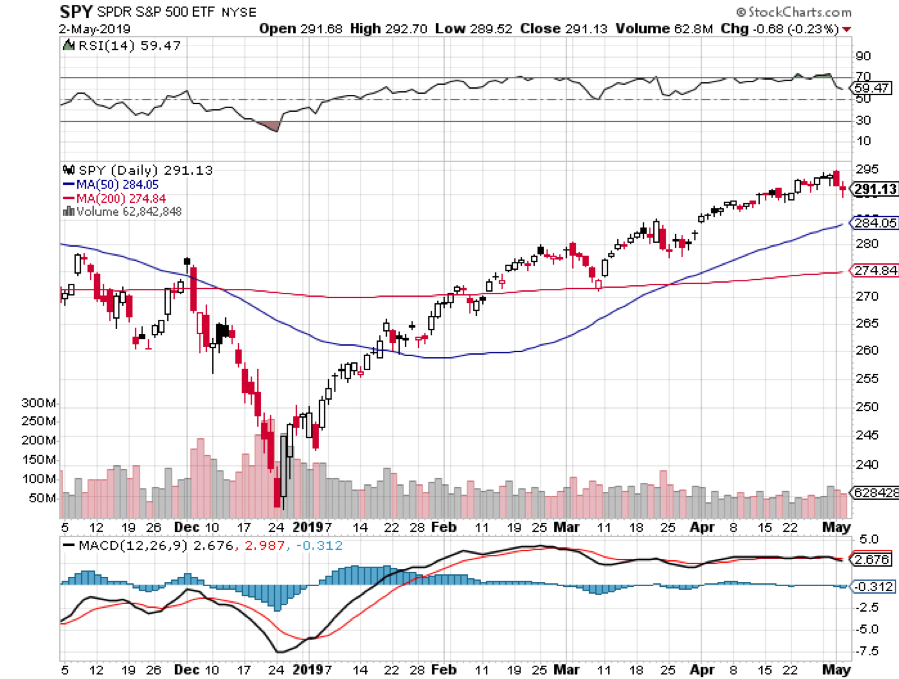

Q: Your old target for the (SPY) was $292.80; we’re clearly above that now. What’s your new target and how long will it take to get there?

A: My new target on the S&P 500 (SPY) is $296.80. You’re looking at $295 on the (SPY), so we’re almost there. However, we’re grinding up too slowly so I can’t give you an exact date.

Q: Will Fed governor Jay Powell give in to pressure from Trump who wants him to drop rates? Does he have any sway over the process?

A: Officially he has no sway, but every day Trump is tweeting: “I want QE back, I want a 1% rate cut.” And if that happened, the economy would completely blow up—an interest rate cut with the market at an all-time high and 3.25% GDP growth rate would be unprecedented, would deliver a short term gain and long term disaster.

Q: What do you think about the Uber (UBER) IPO?

A: I wouldn’t touch it with a 10-foot pole—they’ve been cutting valuations almost every day. At one point they were going to value the company at $120 billion dollars, now they’re at $90 billion and they may even lower it from there. The last car sharing IPO (LYFT) dropped 33% from its high. I would stay away from all of the IPOs once they’re listed. The rule is: only buy these things when they’re down 50%. Warren Buffet never buys IPOs, nor do I.

Q: What do you think about buying or selling Lyft?

A: I would wait a couple of months for Lyft to find its true price. Then you’ll have something to trade against.

Q: Do you think the bad news is over on Tesla (TSLA)? Is it time to buy? Or is it going bankrupt?

A: The whole world knew that the electric car subsidy would be cut in January, so what customers did was accelerate their orders in the 4th quarter, which took us all the way up to $380 in the shares, and then created a vacuum in the Q1 of this year. It reported the first quarter last week—they were disastrous orders, and the company is cutting back overhead as fast as possible as if it’s going into a recession, which it kind of is. The question is whether or not sales will bounce back in Q2 with the smaller subsidy. I happen to think they will. But we may not see 2018 Q4 sales levels again until 2019 Q4.

Q: Why has healthcare (XLV) been so awful this year?

A: There’s an election next year and both parties promise to beat up on the healthcare industry with drug control pricing and other forms of regulation. Of course, the current president promised free competition in drug prices; but then he moved to Washington DC and found the drug industry lobby, and nothing was ever heard again on that front. It’s a very high political risk sector, but there is some great value at these levels in the healthcare industry in the long term. I’m about to start the Mad Hedge Biotech and Health Care newsletter imminently.

Q: Should I buy the (TLT) $120-$123 call spread now?

A: That's a very aggressive trade, I would wait and go with strikes for in the money, and then only on a big dip. Don’t reach for a trade when the market is at an all-time high.

Q: Should I be shorting Tesla down here?

A: Absolutely not, your short trade was at $380, $350, $330 and $300. Down here, you run the risk of a surprise tweet from Elon Musk causing the stock to go $50 against you. Buy the way, he’s already announced that he’s buying $10 million worth of shares in his next capital raise.

Q: What do you think about CRISPR stocks long term, like Editas Medicine (EDIT), Sangamo Life Sciences (SGMO), and Cellectis (CLLS)?

A: These are probably the best bunch of 10 baggers long term. Short term they are afflicted with the same problems impacting all of healthcare—promises of regulation and price control on all of their products ahead of an election. So, hold for the long term; short term I’d only be buying the really big dips. Did I mention that I’m about to start the Mad Hedge Biotech and Health Care newsletter imminently?

Q: Is your May 10th market top forecast still good?

A: Well we’re getting kind of close to May 10th. I made this prediction based on an inverting yield curve two years ago. However, that target did not anticipate interest rates topping out for the 10-year US Treasury bond at 3.25%. Nor did it consider the Fed canceling all interest rate hikes for the year. Without the artificial stimulus, the market would certainly have already rolled over and died. That said, I still have a week to go.

Q: Should I be selling my long term holds in the FANGS, like Apple (AAPL), Amazon (AMZN), and Microsoft (MSFT)?

A: For the long term, no. However, we know from December that these things can get hit with a 40% drawdown at any time. As long as you can handle that, they always bounce back.

Q: What will happen to Venezuela? Any trades?

A: The only related trades would be in the oil market (USO). If we get a coup d’ etat which installs a new pro-American president, which could be at any time, that could lead to a selloff in oil for a couple of days as 1 Million barrels of crude per day come back on the market, but probably no more than that.

Q: With current national debt and budget deficits, when will interest in gold kick in?

A: Very simple: when the stock market goes down, you want to buy gold. It’s the hedge that everyone will chase after, and inflation is just around the corner.

Q: Do you need me to place any Kentucky Derby bets?

A: Me being the cautious guy I am, I pick the horse with the best odds and then I bet him to show. That almost always works.

Q: What about pot stocks?

A: I’ve never liked them very much; after all, how hard is it to grow a weed? The barriers to entry are zero. All of these pot companies coming up now are not really pot stocks as much as they are marketing companies, so you’re buying their distribution capability primarily. That said, I’m having breakfast with the CEO of a major pot company next week, so I’ll be writing about that once I get the inside scoop.

Q: Will the Fed be the non-event?

A: Yes, as stated in the Mad Hedge Hot Tips this morning, it will be a non-event and the news is due out in about an hour.

Mad Hedge Technology Letter

May 2, 2019

Fiat Lux

Featured Trade:

(APPLE’S HOME RUN)

(AAPL), (CRM), (GOOGL)

The company that Steve Jobs built is an earnings thoroughbred with money growing out of their ears.

Apple’s earnings report was real confirmation that Apple’s pivot into a services company is overshadowing its drop in iPhone revenue.

They even elevated forward guidance for next quarter.

Being an economic bellwether that it is, the earnings success could point to more bullish momentum for not only the tech sector but the broader market.

The tech strength showing up in the squiggly figures of the sector’s earnings report indicates that the expected earnings recession will be more of a pause rather than a dip that was first expected.

The next bout of bullish strength that permeates through the market will take many tech stocks to higher highs.

The numbers backed up this premise with Q2 2018 revenue from the services category comprising 20% of total revenue in Q2 2019—a rubber stamp of confidence that this isn’t a false dawn after service sales only comprised of 16% of total revenue the prior year.

The death of the smartphone is upon us with most people who can afford a premium one already using one as we speak with no intentions for a quick refresh.

Apple’s strategy of selling expensive iPhones to Chinese nationals is over with iPhone sales getting slaughtered by 17% to about $31 billion—an accelerated decline for a product that has been hamstrung by smartphone rivals in China offering better phones for lower prices.

The $11.5 billion from its services division and the end result of registering revenue in the high end of its $55-59 billion projection for the quarter is a stark shift from the underperformance of 2018 when Chinese iPhones sales were so bad that they stopped reporting the segment altogether.

The $58 billion of quarterly revenue was still a drop of 5% YOY which included $31 billion in iPhone sales, a shell of its former self when they generated $37.5 billion in iPhone sales the same quarter in 2018.

The disruption in handing off the baton to the services brigade caused outsized ructions inside the company causing the stock to plummet 20% last winter.

Wearables put the cherry on top of the sundae expanding at a rate close to 50% during the quarter with AirPods and Apple Watch leading the charge as best sellers.

Apple plans to inject $75 billion on share repurchases and it also approved a 75-cent dividend per share, a 5% increase.

These repurchases could boost Apple’s stock by up to 7% per year offering investors another compelling reason to hold this stock long-term.

The upgraded dimensions of Apple’s business model could finally give investors peace of mind as they wean themselves from Chinese iPhone sales.

Moving forward, the relationship between American tech and the Chinese consumer will be contentious at best, and battling with Huawei on its turf is not a sensible strategy.

Highlighting this weakness were the Greater Chinese revenue registering only $10.2 billion in sales, down from the Q2 2018 tally of $13 billion.

On the positive side, the Chinese weakness is already baked into the pastry ceding way for the services narrative to move to the forefront.

Generating more incremental revenue from its existing base of 1.4 billion Apple accounts is the order of the day.

I initially believed Apple would make major headway in the services segment and foresaw services composing about 25% of total revenue.

However, I didn’t believe they would be able to achieve this for a few years, and the surprise to investors is the velocity of change to the upside in its services business.

Adding the new magazine subscription for $9.99 to its platform is another feather in their cap even though it doesn’t transform the industry.

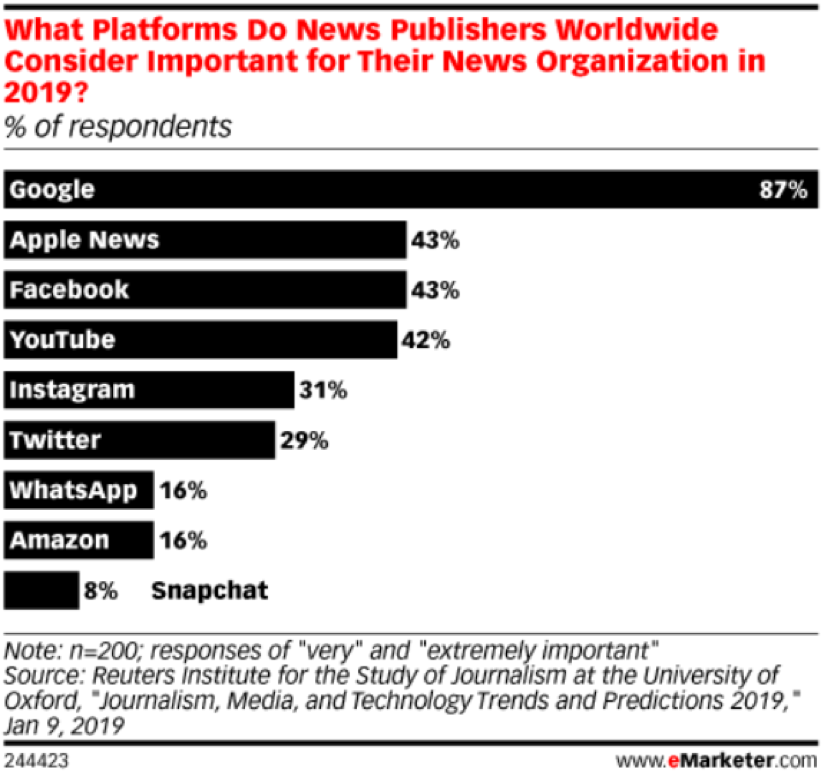

Respondents to emarketer.com made it widely known that Apple as a platform was the second most important platform for news publishers behind Google offering a great opportunity to carve out more income from their new news app.

Apple is still in dire need of attractive video options for its content basket and assets on the market are plenty from live sports, shows, movies, and video games.

My money would be on Cook to prefer video games as a viable growth driver because it resonates deeply with younger audiences from abroad and avoids the polarity of controversial content which societies are increasingly sensitive to.

Another option would be to dive headfirst into the enterprise software business moving towards a Salesforce (CRM) model selecting cloud companies à la carte to integrate into a business cloud.

Many Apple device holders already wield their devices for their own online businesses, and this would represent a solid growth driver if they could make their services more business-friendly.

What can we expect moving forward?

In short, less iPhone sales and more service revenue as a proportion of total revenue.

If Apple can carefully choreograph its downshift of iPhones sales that doesn’t destroy overall revenue and profitability, they will successfully manage in transforming the company into a hybrid service company.

I believe that Apple’s services will contribute around 30% of total revenue by 2020 and this is a big deal that will buoy the stock.

Ultimately, these are happier times for Apple as their bet on services isn’t getting bogged down, eclipsing expectations, and will cement their status as a sure-fire $1 trillion market cap company.

Bravo!

Mad Hedge Technology Letter

April 24, 2019

Fiat Lux

Featured Trade:

(WHO BEAT WHOM IN THE APPLE/QUALCOMM BATTLE)

(QCOM), (INTC), (AAPL)

The 5G bonanza is slithering towards us in a slow yet predictable motion – that was the takeaway from Apple finally conceding that its bargaining positioning was weaker than initially thought.

Apple made amends with chipmaker Qualcomm (QCOM) in the nick of time, let me explain.

Qualcomm is the leader of 5G chip technology, and the two firms decided on a six-year pact that will allow Qualcomm to sell patent licensing to Apple while becoming a crucial supplier of 5G modems to the new iPhone that will roll-out to consumers in the back half of 2020.

Envisioning this 2 for 1 special a few weeks ago was impossible as the brouhaha spilled over into the national media with top executives exchanging barbs.

Qualcomm, to its credit, stayed steadfast on its position and was the bigger winner of the spat.

The rapid reaction in the stock price has vindicated Qualcomm’s initial reluctance to make a cut-price deal with Apple.

The new contract locks in Apple at around $9 per phone in licensing fees, almost double what many analysts were predicting.

Apple also paid a one-time fee of the backlog of patent usage from the past two years that many specialists estimate to be in the $6 billion range.

Qualcomm has previously stated that Apple owes them $7 billion from the kerfuffle and Apple’s refusal to pay stemmed from their belief that Qualcomm was “double dipping” – a claim based on Qualcomm charging a fee for each iPhone using its patents as well as a fee for the technology itself which Apple felt extortionate.

Ultimately, the jousting wasn’t worth the trouble as the best-case scenario of Apple saving $1 billion in patent fees was overshadowed by the opportunity cost which was significantly higher.

The updated terms see a substantial improvement for Qualcomm over the $7.50 per phone that Apple was paying before.

The end of the saga smells of desperation on CEO of Apple Tim Cook’s behalf, realizing that time was ticking down and competitors such as Huawei have already launched 5G-supported phones.

Apple is, in fact, late to the party and one of the main root causes was the logjam with Qualcomm.

If Apple didn’t come to terms with Qualcomm, suppliers and designers wouldn’t have enough time or supply to prepare to meet the fall 2020 deadline causing Apple to delay the new iPhone.

The worst-case scenario that became a realistic threat was that the new iPhone wouldn’t have been ready until 2021 – Apple shares would have dropped 20% in a heartbeat if this played out.

Avoiding this doomsday scenario is a massive bullish signal for Apple shares and brings forward revenue demand into 2020.

The new iPhone with ironically Qualcomm’s 5G modem technology is also the selling point for iPhone lovers to upgrade to a newer and faster iPhone iteration.

It’s a headscratcher that Tim Cook played his cards in the way that he did, another misstep in a long record of fumbles in the red zone.

Inevitably, scrunching up the production schedule heaps loads of pressure on the existing engineering teams to produce a flawless iPhone.

Apple simply couldn’t wait any longer and CEO of Qualcomm Steven Mollenkopf understood that, leading me to solely blame Tim Cook for this calculated error.

Where do the chips lie after this recent shakeout?

First, this piece of news is demonstrably bullish for Qualcomm and its business model while backloading around $6 billion or so in revenue onto its balance sheet.

In short, Qualcomm hit it out of the park and set itself up for the upcoming insatiable demand for 5G chips while publicly demonstrating they are best in show for 5G infrastructure equipment.

It might turn out to be Qualcomm’s best day in the history of the company and one that employees will never forget inside its headquarters.

This will embolden Qualcomm in the future to fight for the revenue that is rightfully theirs and they won’t be frightened by bigger sharks attempting to persuade them that they should receive a lesser share of the pie.

For Mollenkopf, this is his crowning moment and a pathway to another big-time job, the one day grabbing of the spoils has elevated his reputation.

Apple is a minor winner because of the adequate supply of chips that Qualcomm will provide that guarantees Apple’s engineers clarity instead of dragging itself deeper into a courtroom battle with a company that supplies an integral component to their iPhone.

Hours after the news hit the press, Intel (INTC) waived the white flag issuing a short response admitting they are exiting the 5G smartphone business, a bitter pill to swallow for a legacy company finding it difficult to stay with the big boys.

And if you remember, Intel was initially thought to be the one to provide memory to the 5G smartphone but now that notion is dead as a doornail.

Intel will hope they can capture a fair share of the 5G PC business to make up for the lost opportunity, but as consumers migrate away from PCs, shareholders could sense Intel could be left holding the bag.

Qualcomm has strengthened its stranglehold on the 5G smartphone modem market in an industry that will morph into a worldwide addressable market of $20 billion by 2025.

Even though Huawei just announced they would be willing to sell their 5G chips to Apple, Huawei and South Korea’s Samsung mainly produce chips for their in-house branded smartphones and shun feeding competitors like Apple who require the same chips.

Apple hoped to create some leveraging power to get a better 5G chip deal and loosen the jaws that gave Qualcomm a powerful position over Apple, but Intel quitting this segment left Apple with a series of bad choices and they chose the lesser of the evils.

What does this boil down to?

Qualcomm outmuscled Intel producing faster and better performing chips that supported longer battery life.

Qualcomm simply has better engineering talent.

Intel had an uphill battle in the first place, but it is clear they cut their losses because the writing was on the wall leaving Qualcomm to reap all the benefits.