Mad Hedge Technology Letter

March 5, 2019

Fiat Lux

Featured Trade:

(MEET THE PREMIER DINOSAUR OF OUR TIME),

(HPQ), (LNVGY), (DVMT), (AAPL)

Mad Hedge Technology Letter

March 5, 2019

Fiat Lux

Featured Trade:

(MEET THE PREMIER DINOSAUR OF OUR TIME),

(HPQ), (LNVGY), (DVMT), (AAPL)

Stay away from HP Inc. (HPQ).

If you want the definition of a legacy tech company, then we have found one of the premier dinosaurs of our time.

The first iteration of Hewlett Packard was in the 1960s when they partnered with Sony to manufacture digital equipment.

They are widely considered the founders of the Silicon Valley establishment that snowballed into what it is today.

In 1939, the Silicon Valley company was established in a one-car garage in Palo Alto by Bill Hewlett and David Packard and initially produced a line of electronic test equipment for Walt Disney.

The garage is classified as a California State historical landmark.

It then developed its products enough to hail itself as the world's leading PC manufacturer from 2007 to 2013, a 6-year reign at the top.

Its long history doesn’t mean the trajectory has been heightened, the company has presided over some major messes such as its purchase of the ill-fated PDA firm Palm and the once discount PC manufacturer Compaq.

HP has had a great seat being able to observe the massive shifts in the tech scene, but unfortunately, its own business model and revenue stream have not been one of the main recipients of this major shift.

According to market research firm IDC (International Data Corporation), China’s Lenovo (LNVGY) recently eclipsed HP (HPQ) becoming top dog in the global PC (personal computers) market.

Lenovo supplanted HP bagging market share of 24.6% on the back of a joint venture with Fujitsu in May 2018 that fueled major incremental gains.

HP still commanded 23.6% share in Q4 2018 among laggards of the likes of Dell (DVMT), Apple (AAPL), and Acer Group with shares of 16.5%, 7.2%, and 6.7%, respectively.

The downtrodden numbers signify that demand for HP personal computers is waning and this is just the tip of the iceberg.

The personal computer industry has been growing in the single digits the last few years and is no more the uber growth industry it once was at the outset of the century.

Last quarter only saw HP’s personal systems segment revenue increase 2.3% YOY.

Total unit sales dropped 3% YOY.

HP blamed the 1% slide on notebook shipments and an 8% decline in desktop shipments.

Evidence tells us that consumers are increasingly valuing mobility more than ever and giving ground to smartphones is inevitable.

Making matters worse, smartphone companies such as Apple, Microsoft, and Google produce outstanding desktop computers that seamlessly integrate into a rich ecosystem.

Consumers are repeatedly buying computers and phones of the same brand that can easily mesh cohesively, a nod to continuity that consumers love.

Professional work stations have also taken the form of an onslaught of one brand of manufacturer whether it be Android-based Microsoft products of iOS-based Apple.

I can vouch for rarely finding someone with a package of Apple’s iPhone and an HP desktop as a professional work hybrid solution unless they are forced by external circumstances.

Essentially, HP is on the wrong side of the pivot to mobile and the lack of innovation is hurting them in a multi-faceted way.

These companies that fail to evolve have a tendency to act as if market conditions never change, only for one bad earnings report to morph into a string of misses tanking the share price.

I believe HP is on that train to nowhere and its lack of investment into creating more advantageous business opportunities sticks out like a sore thumb right now when you compare them to other tech heavyweights.

CEO of HP Dion Weisler had the quote of the century telling analysts on the call that “we’re now engaging on a new battlefield and it’s called online.”

This quote is a microcosm of the state of HP and reflects poorly on the leadership.

One of HP’s largest cash cows is the printing supplies business and for management to blame “online” forces on crimping sales is an insult to shareholders.

“Online” consumer business has been around for more than 30 years, and to reference this external force as a new engagement dragging down sales condemns this company to pariah-status.

Management must wake up and smell the coffee and understand that if selling overpriced print ink and printers was a god given right then HP is doomed strategically.

An unexpected 3% revenue drop in the printer supplies business was written in the stars, and HP has been lucky to even reap what they have to this point.

It’s an ongoing renaissance for consumer prices in a deflationary environment and finding cheaper alternatives is just an Amazon.com visit away.

Selling ink and toner cartridges is a high-margin business that has no business being a high-margin business.

The EMEA region (Europe, Middle East and Africa) printing supplies revenue cratered 9% as most of the world rather buy cheaper alternatives online where they can price compare easily.

Manufacturing cartridges with ink inside it is not high-tech and is due for a margin reckoning.

Apparently, HP has technology that can detect counterfeit ink, but isn’t ink just ink?

HP classifies ink not branded HP as counterfeit ink, once again, a vividly low barrier to entry screaming overpriced.

Such a low-tech competitive advantage should be pounced on - we are seeing that in real time and rightly so.

If business and consumers aren’t allowed to use outside ink to place inside of non-HP cartridges, the business will migrate to non-HP, cheaper replacements such as Canon while either filling up ink cartridges themselves or substituting a cheaper alternative.

The dialogue on the conference call was shocking, appearing if HP executives were caught off-guard from this magical thing called the “internet” and the competition derived from it could potentially suppress sales.

I was leaning towards becoming bearish HP before this earnings report and the awful performance vindicated my initial prognosis.

I am bearish HP – sell on any and every rally.

Global Market Comments

March 4, 2019

Fiat Lux

Featured Trade:

(THE MARKET FOR THE WEEK AHEAD, or THE RECESSION HAS BEGUN),

(SPY), (TLT), (GLD), (AAPL)

I hate to be the one to fart in church here, but the long-feared recession has already started.

It’s not a conventional recession defined by two back to back quarters of negative GDP growth, although you have a tough time convincing anyone in the besieged auto, real estate, or agricultural sectors of that.

No, this is more of a growth recession. US GDP growth peaked at a 4.4% annualized rate during the second quarter of 2018. The third quarter came in at 3.4% and the four quarter at only 2.6%. Consensus forecasts for Q1 2019 are well below 1%, thanks to the government shutdown.

That means the growth rate has fallen by an eye-popping 76% in nine months! By the way, the government has told us that economic growth has been rising this entire time. But want the stimulus from the 2017 tax bill were spent, there were no more bullets left.

If it were just the GDP data that was falling off a cliff, I wouldn’t be so worried. However, the weakness is confirmed by a raft of other data. The ten year US Treasury bond (TLT) remains stuck around 2.75%, an incredibly low figure given that we are ten years into an economic recovery.

Corporate earnings growth forecasts going forward are now at zero. To see a market multiple of 18X for stocks with no growth and prices that are just short of all-time highs defies belief. This will all lead us to a REAL recession sometime in the near future.

What we are left with is a market of very low return, high-risk trades, not the kind you want to pursue, let alone bet the ranch on.

I believe that when the BIG ONE finally arrives, it won’t be all that bad. I’m looking for a short, sharp recession of maybe six months in duration. There really isn’t that much leverage in the system that can blow up. It might even not be worth selling out all your stocks to avoid it, especially if it results in a giant tax bill.

You would also be selling in front of my coming Golden Age for the United States when a huge demographic tailwind brings a new era of prosperity. If you are smart enough to get out at the top now, will you also be clever enough to get back in at the bottom? Or will you sell more instead, like you did in December?

Merger fever hit the gold industry with Barrick Gold (GOLD) taking a run at Newmont Mining (NEM), the world’s first and second largest producers. It’s all about efficiencies of scale. Take this as a long-term bottom in gold prices.

The China tariff hike was postponed indefinitely, and Chinese stocks love it. Import duties will stay at 10%, instead of rising by 25% starting last Friday. We knew it was never going to happen.

Some 95% of the China trade deal is now already priced into the market. If a deal DOESN’T get done and goes the way of the North Korean negotiations, the market will very quickly back out that 95%.

Poor economic data was to be found everywhere you looked. Wholesale Inventories rose sharply, up 1.1% in another recession indicator. US Factory Orders came in incredibly weak at 0.1% in December when 0.6% was expected. Recession indicator number one million. Limit your risk.

Our friend Jay stayed dovish again, but markets yawned this time. How much mileage can you get from the same vague assertion? Shorts are about to swarm the market. Take profits on all longs.

The US Dollar hit a three-week low. The Fed’s dovish leanings are hammering the buck. Keep loading the boat with weak dollar plays, like emerging markets (EEM).

Bonds got crushed delivering their worst week in five months, down three points as the great “crowding out” begins. Massive corporate borrowing can’t compete with government borrowing, so rates are rising sharply. This is the beginning of the end. Sell short the (TLT).

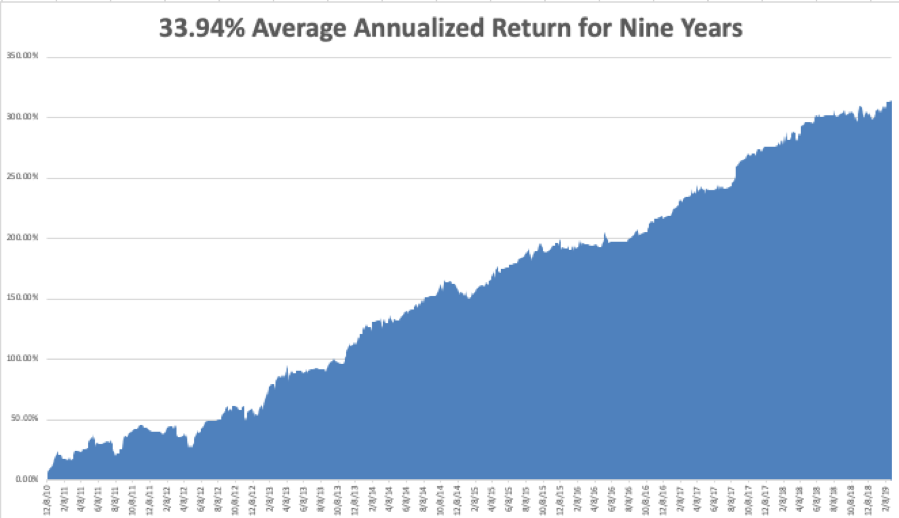

February came in at a hot +4.16% for the Mad Hedge Fund Trader. My 2019 year-to-date return ratcheted up to +13.64%, a new all-time high and boosting my trailing one-year return back up to +31.90%.

My nine-year return clawed its way up to +313.78%, another new high. The average annualized return appreciated to +33.94%.

I am now 80% in cash, 10% long gold (GLD), and 10% short bonds (TLT). We have managed to catch every major market trend this year, loading the boat with technology stocks at the beginning of January, selling short bonds, and buying gold (GLD). I am trying to avoid stocks until the China situation resolves itself one way or the other.

As for the Mad Hedge Technology Letter, it is short Apple (AAPL).

Q4 earnings reports are pretty much done, so the coming week will be all about jobs, jobs, jobs.

On Monday, March 4, at 10:00 AM EST, December Construction Spending is published.

On Tuesday, March 5, 10:00 AM EST, December New Home Sales are out.

On Wednesday, March 6 at 10:00 AM EST, the February ADP Employment Report is out, a measure of private sector hiring.

Thursday, March 7 at 8:30 AM EST, we get Weekly Jobless Claims.

On Friday, March 8 at 8:30 AM EST, we get the February Nonfarm Payroll Report is released. The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I’m taking the kids to see Hello Dolly in San Francisco. This was one of my parents’ favorite Broadway musicals, and they used to sing the songs around the house all day long. However, it won’t be the same without the late Carol Channing.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

March 1, 2019

Fiat Lux

Featured Trade:

(OH, HOW THE MIGHTY HAVE FALLEN),

(BRK/A), (AXP), (AAPL), (BAC), (KO), (WFC), (KHT),

(AMGEN’S BIG WIN), (AMGN), (SNY), (REGN)

Going through Warren Buffet’s letter to the shareholders of Berkshire Hathaway (BRK/A) you can’t help but notice that his performance nosedived from a breathtaking 21.9% in 2017 to a much more sedentary 2.8% last year. That is with an S&P 500 down -4.4%, including dividends.

That compares to my own 23.67% profit for 2018. But Warren has a much higher bar to reach. He does this with a staggering market capitalization that was pegged at $496 billion as of today. At best, the combined buying power of my Trade Alerts is only about a billion dollars.

And here is the stunning piece of information that should have been the headline. Warren has $112 billion in cash and equivalents, some 22.58% of the total, and an all-time high. That means buying stocks at these levels is the least attractive in the fund’s 57-year history.

Buffet would much rather buy back his own stock. He is willing to pay a premium to book value but only when it trades at a discount to intrinsic value, as he did in size during the fourth quarter of 2018.

Which raises one screaming great question. If Warren Buffet isn’t buying stocks, why should you?

Buffet isn’t even buying Apple, which he only started soaking up in 2017. It now is his second largest holding, with an average cost of $140. I’m amazed that the stock didn’t get crushed on this news, but then we live in a constantly amazing world these days.

The big change in Berkshire Hathaway over the years is that it is becoming more of an operating company and less of an investing one. That is because Buffet is increasingly buying entire companies, rather than exchange-traded stocks. One of the reasons for his cash hoard that an effort to buy a company for high double-digit billions of dollars fell through last year.

Still, Warren bought $43 billion worth of public stocks in 2018 and only sold $19 billion worth. These are his five largest public shareholdings and his percentage of outstanding shares:

American Express (AXP) – 17.9%

Apple (AAPL) – 5.4%

Bank of America (BAC) – 9.5%

Coca-Cola (KO) – 9.4%

Wells Fargo (WFC) – 9.8%

Warren likes to break up his entire holdings into five “groves”, as there are too many companies to follow individually.

1) Wholly owned companies where Berkshire has 80%-100% stakes, such as the BNSF railroad and Berkshire Hathaway Energy.

2) Publicly listed equities like those listed above

3) Companies controlled with third parties, like Kraft Heinz (KHT)

4) US Treasury bills

5) Property/Casualty Insurance operations like GEICO that generate an enormous free cash float

Buffet described the enormous tax benefits his company received from the 2017 tax bill. It amounted to the government’s indirect ownership of Berkshire shares falling, which he humorously calls “AA” shares, from 35% to 21% at no cost whatsoever. That greatly increased the value of the remaining shares.

Warren spent the rest of his letter talking about the Great American Tailwind. Since he started investing on March 11, 1942, one dollar invested in the S&P 500 has grown to an eye-popping $5,288! That works out to an average annualized compound return of 11.8% a year.

The end result has been the greatest creation of wealth and rise in standards of living in human history.

That is a tough record to beat.

Global Market Comments

February 21, 2019

Fiat Lux

Featured Trade:

(SHORT SELLING SCHOOL 101),

(SH), (SDS), (PSQ), (DOG), (RWM), (SPXU), (AAPL),

(VIX), (VXX), (IPO), (MTUM), (SPHB), (HDGE),

Global Market Comments

February 11, 2019

Fiat Lux

Featured Trade:

(THE MARKET FOR THE WEEK AHEAD, or DON’T STAND NEXT TO THE DUMMY),

(AAPL), (MSFT), (TSLA), (VIX), (TLT), (TBT), (FXI)

When I was a war correspondent (Cambodia, Laos, Iraq, Kuwait, Indonesia), my seniors gave me a sage piece of advice that saved my life many times.

“Don’t stand next to the dummy.”

Don’t go near the guy wearing the Hawaiian shirt, NY Yankees baseball cap, and aviator sunglasses. You want to be dressed in the same color as the troops and blend in as much as possible. Otherwise, the enemy will aim at the dummy and hit you.

As much as I tried, at 6’4” I was never going to blend in anywhere in Asia. So, I went into the stock market instead.

Now 50 years later, I am facing another dummy problem. Except that the next hit I may take will be of the financial kind rather than the metallic one.

The reaction to the Trump tax cuts is going to be far worse than any benefits the privileged class was able to reap from the cuts in the first place. Listening to the proposals aired, I shudder: A maximum 70% tax rate, the end of special estate tax treatment, a millionaire’s surtax, and the banning of corporate share buybacks.

It’s that last one that that will be particularly damaging for the US economy. Often, a company’s best possible investment is in its own shares where returns are frequently higher than possible through investing in their own business. Just think of all those shares Apple (AAPL) bought at $25, now at $170, and Microsoft (MSFT) picked up at $10.

This is one of the only occasions were management and shareholder interests are one and the same. The event is tax-free as long as you don’t sell your shares. And companies don’t have to pay dividends on stock they have retired, boosting profits even further.

The media loves pandering to the most extreme views out there. I know because I used to do it myself. Cooler heads will almost certainly prevail when the tax code is completely rewritten again in two years. Still, one has to worry.

The week had plenty for we analysts and strategists to chew on.

Is the Fed pausing because of political pressure or an economy that is falling apart? Neither answer is good for equity holders. Start cutting back risk while you can. There are lots of bids on the way up, but none on the way down as December showed.

There has lately been a rising tide of weak data to confirm the negative view.

Factory orders nosedived 0.6% in November, the worst in a year. Funny how nobody wants to make stuff ahead of a recession. ISM Non-Manufacturing Index Cratered to 56.7. Should we be worried? Hell, yes! Why are we getting so many negative data points and stocks keep rising?

Farm sector bankruptcies are soaring, hitting a decade high. Apparently, the trade wars and global warming aren’t working for them. Ironically, ag prices are about to take off to the upside when a Chinese trade deal gets done. Buy the ags for a trade.

Tesla (TSLA) cut prices again in a blatant bid for market share and global domination. The low-end Tesla 3 price drops to $42,900. Next stop $35,000. Too bad they laid off my customer support personnel to cut costs. I can’t find my AM radio.

China trade talks (FXI) hit the skids, taking the stock market down with it as an administration official concedes they are “nowhere close to a deal” with the deadline 3 weeks off. Trump desperately needs a deal while the Chinese don’t, who think they can do better under the next president. If you disagree with this view in China, your organs get harvested and sold on the open market.

The European economy is also going down the drain with the EC’s forecast of economic growth cut from 1.9% to 1.3%. The US-China trade war is cited as a major factor. The global synchronizes slowdown accelerates. Looks like they’ll have more time to drink cheap wine and smoke Gauloises.

The Volatility Index (VIX) hit $15 and that seems to be the bottom for the time being. The market was more overbought than at any time since July. Is the “fear gauge” signaling that happy days are here again? I doubt it. Don’t whistle past the graveyard.

The Mad Hedge Market Timing Index is entering danger territory with a reading of 67 for the first time in five months. Better start taking profits on those aggressive leveraged longs you bought in early January. Your best performers are about to take a big hit. The market has since sold off 500 points, proving its value.

There wasn’t much to do in the market this week, given that I am trying to wind my portfolio down to 100% cash as the market peaks.

I stopped out of my short portion in Apple when my stop loss was triggered by pennies. The second I was out, it began a $6 selloff. Welcome to show business.

I used a major 3 ½ point rally in the bond market to put on a new double short position there. The yield on the ten-year US Treasury bond has to plunge to 2.40% in a month, a three-year low, for me to lose money on this position. It’s a bet that I am happy to make.

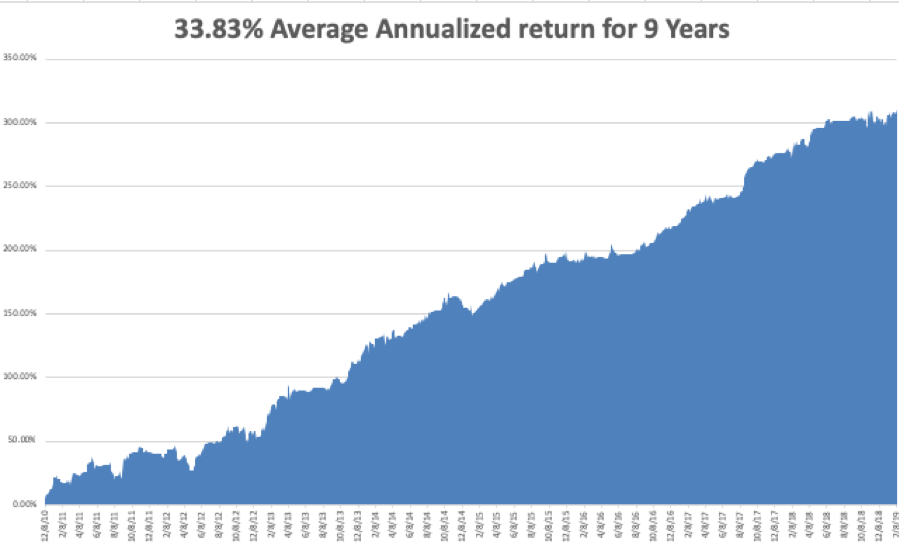

My 2019 year to date return leveled out at +10.03%, boosting my trailing one-year return back up to +35.75%.

My nine-year return maintained +310.17%, a new high. The average annualized return stabilized at +33.83%.

I am now 70% in cash and triple short the bond market.

Government data is finally starting to trickle out now that the government shutdown is over.

On Monday, February 11 there is nothing of note to report. Everything important is delayed.

On Tuesday, February 12, 10:00 AM EST, we get the January NFIB Small Business Index. Earnings for Activision Blizzard (ATVI) are out and should be a complete disaster, along with Twilio (TWLO).

On Wednesday, February 13 at 8:30 AM EST, the all-important January Consumer Price Index is published. Barrick Gold (GOLD) reports.

Thursday, February 14 at 8:30 AM EST, we get Weekly Jobless Claims. We also get December Retail Sales which should be good.

On Friday, February 15, at 8:30 AM EST, the February Empire State Index is out. The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I will be battling my way through the raging snowstorms of the High Sierras trying to get over Donner Pass to my Lake Tahoe estate. Unless I clear the six feet of snow off the roof soon, or the house will get crushed from the weight as it did three years ago.

Where are all those illegal immigrants hanging out in front of 7-Eleven now that I need them?

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

February 7, 2019

Fiat Lux

Featured Trade:

(THE DEATH OF THE COLLEGE DEGREE),

(GOOGL), (IBM), (AAPL), (BABA), (BIDU)