As the biotechnology world is ever-evolving, with several companies going public every few months, let me share some of the most promising names that recently emerged.

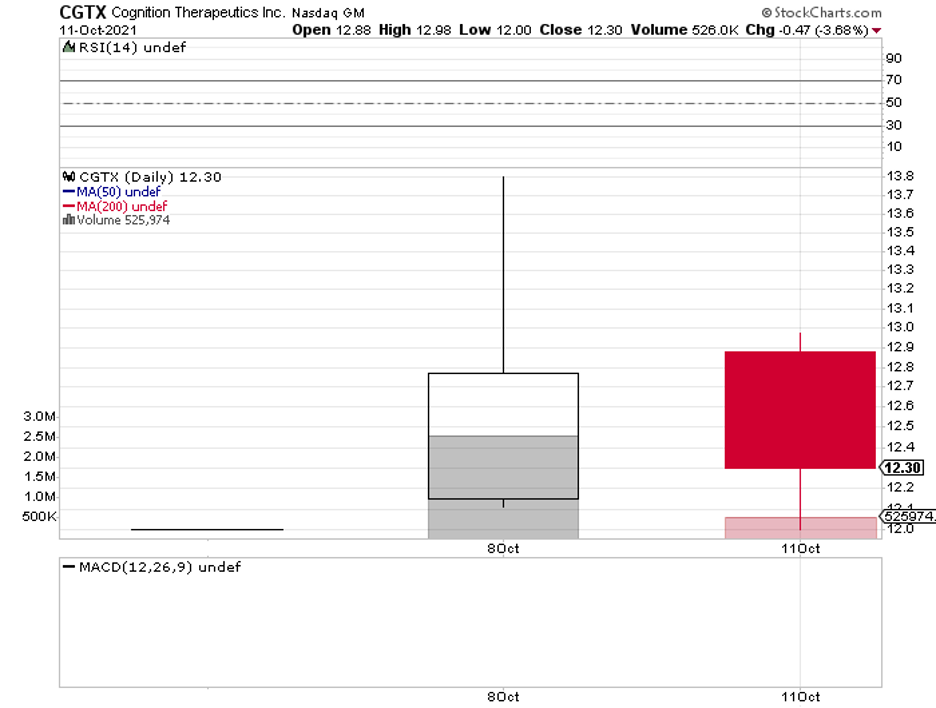

The first is Cognition Therapeutics (CGTX), a company working on treatments for Alzheimer’s disease and macular degeneration.

Its most promising candidate is an Alzheimer’s treatment called CT1812, which is currently under Phase 2 trials. Looking at the timeline, CGTX expects to release topline data by 2023.

With the expected growth of the aging population, focusing on treating various forms of Alzheimer’s is a promising direction for Cognition Therapeutics.

In fact, the global market for this neurodegenerative disease is projected to grow from $2.9 billion in 2018 to a whopping $10.5 billion by 2025.

So far, the major competitors of Cognition Therapeutics in this area include Biogen (BIIB), Eli Lilly (LLY), AbbVie (ABBV), Novartis (NVS), and Takeda (TAK).

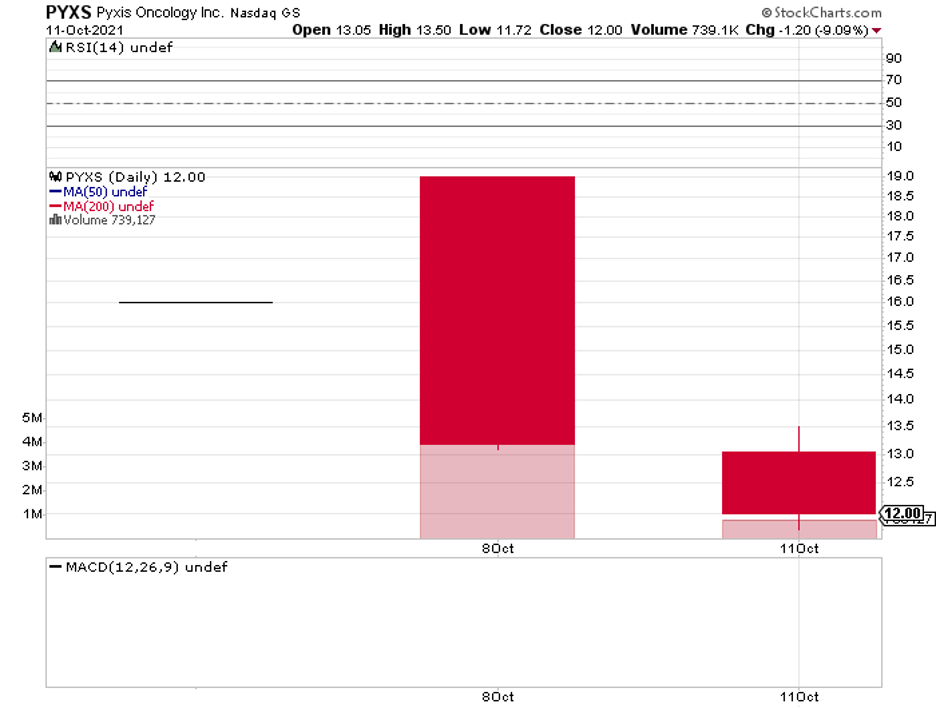

The second promising biotech company is Pyxis Oncology (PYXS), which is a spinoff from Pfizer (PFE).

Pyxis is focused on developing next-generation treatments targeting difficult-to-treat types of cancer.

Basically, the company’s goal is to create therapies that can directly kill tumor cells. It also wants to get rid of the underlying problems that lead to the uncontrollable spread of tumors and the weakening of the immune system.

To do this, Pyxis has come up with novel antibody drug conjugate (ACT) candidates and other monoclonal antibody (mAb) pipelines.

Its lead candidate is called ADC PYX-201, a potential treatment for non-small cell lung cancer and breast cancer.

The goal of ADC PYX-201 is to target actively multiplying tumors while boosting the immune response of the patient’s body. Pyxis plans to submit it as a non-small cell lung cancer treatment candidate by mid-2022.

If approved, then ADC PYX-201 will be under patent protection until 2037.

This holds great potential for Pyxis’ cashflow, as the market for non-small cell lung cancer worldwide is anticipated to rise from $6.2 billion in 2016 to over $12 billion by 2025.

With this potential of ADC treatments, Pyxis can expect competition from the likes of AstraZeneca (AZN), Gilead Sciences (GILD), GlaxoSmithKline (GSK), and ImmunoGen (IMGN).

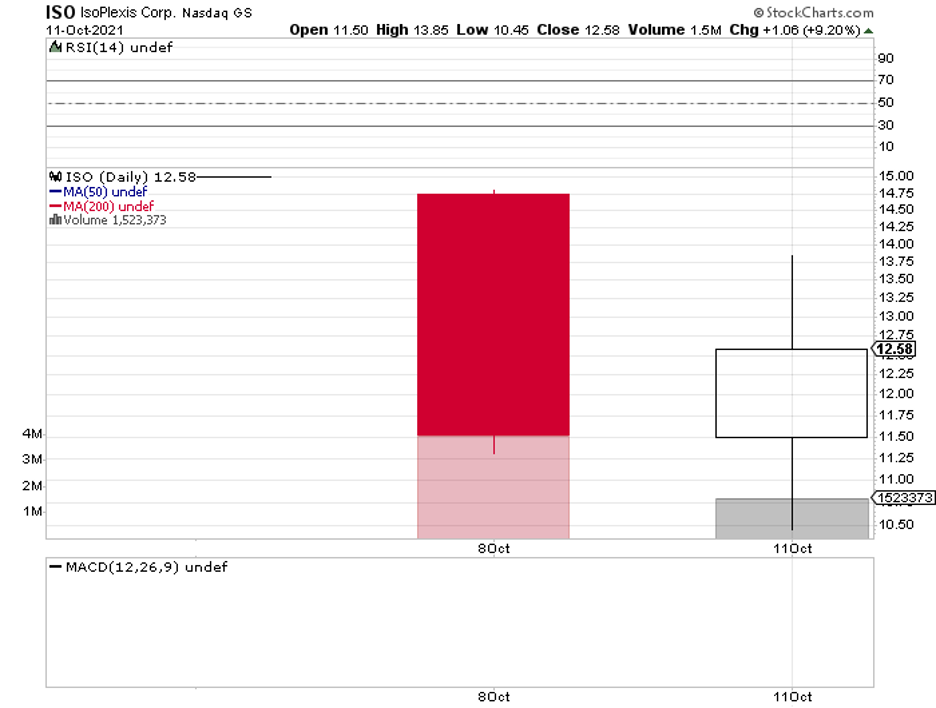

The last name on today’s list is IsoPlexis Corporation (ISO).

This company is the first to focus on dynamic proteomics and single-cell biology in an effort to develop “walk-away automation” products that aid in shortening the therapeutic development timelines by acquiring “multiplexed proteomics with very low sample volumes that reflect in vivo biology to clarify lead candidates.”

In layman’s terms, IsoPlexis is working on a technology that aims to identify every protein in the body to speed up the development of new therapies for rare diseases.

This is a lucrative business, with IsoPlexis targeting at least $34 billion in the total addressable market.

Considering that IsoPlexis is a pioneer in this field, it is possible for it to gain the lion’s share of the segment and position itself as an undisputed leader for years.

More importantly, IsoPlexis can use its patented technology, “Proteomic Barcoded,” to expand the use cases to cover other lucrative markets.

For example, IsoPlexis can apply its technology to cancer immunology and targeted oncology by predicting the progression of cancer cells in the body.

Adding cell therapies to the company’s pipeline is also a very realistic possibility since its technology can be utilized to create CAR-T cell therapies as well.

In fact, IsoPlexis’ approach is already being used in developing treatments for leukemia and melanoma.

Another profitable avenue for IsoPlexis’ technology is the vaccines sector.

Since the development of vaccines requires profiling the responses of the respiratory and immune systems, the company’s data would accelerate the entire process.

So far, the major rivals of IsoPlexis in this space include Thermo Fisher Scientific (TMO) and Bio Rad Laboratories (BIO).

While all these biotech companies offer promising products and technologies, they’re all still in the early stages of development.

This makes them high-risk investments and are likely suitable for those who are willing to invest in the long term.

For those who want to see movement faster and sooner, it might be best to watch these stocks from the sidelines.

https://www.madhedgefundtrader.com/wp-content/uploads/2021/10/cgtx-oct14.png708936Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-10-14 16:00:502021-10-20 14:07:39What's New in Biotech

Choosing winners among biotechnology and healthcare stocks these days isn’t easy.

Since the year started, the sector has been marred with several unexpected disappointments like the 50% decline of crowd favorites Acadia Pharmaceuticals (ACAD) and Sarepta Therapeutics as well as the 33% fall of the ever-dependable FibroGen (FGEN).

So, how can investors pick a winner?

One tactic is taking a peek at what Wall Street analysts are doing, noting which among the companies they’re following are trading the farthest below the estimated price points.

Among the names on the list, a particular stock stands out as a strong contender these days: Vertex Pharmaceuticals (VRTX).

Although it’s one of the most widely known biotechnology companies today, Vertex actually started in a garage of a Harvard-trained chemist, Joshua Bogner, who left his cushy job at one of the most illustrious big pharma companies at that time, Merck (MRK), to pursue his vision.

The company’s raison d’être was a major selling point for a lot of talented and idealistic scientists in that era.

That is, Vertex wanted to find cures for the most challenging diseases and do this in an unbureaucratic setting.

Since then, Vertex’s goal has been straightforward: tackle the most complex and toughest diseases and deliver breakthrough treatments that offer tangible benefits to patients.

Over the years, the company has managed to keep this goal at the forefront of its efforts, starting with its work on the devastating genetic disorder called cystic fibrosis (CF).

Vertex’s work on CF took over a decade, but it eventually led to an impressive franchise that helped with the treatment of patients.

In the first quarter of 2021 alone, sales in this segment reached $1.7 billion.

Expanding on its work, Vertex has explored genetic therapies and set up a collaboration with Moderna (MRNA) in 2016.

Using the latter’s well-established expertise in messenger RNA technology, the companies are expected to come up with more aggressive and advanced CF treatments in the coming years.

Given these developments, Vertex reiterated its 2021 sales guidance to be somewhere in the range of $6.7 and $6.9 billion. Meanwhile, sales of its CF franchise are estimated to peak at $9 to $10 billion—if not higher—by 2024.

Aside from its work on CF, Vertex has also been pouring resources on developing treatments for severe sickle cell anemia and beta thalassemia, a rare blood disorder.

In fact, the company has been looking into these developments as the next major revenue stream, as seen in its bolstered collaboration deal with CRISPR Therapeutics (CRSP).

In this deal, Vertex paid the smaller biotechnology company $900 million upfront plus a potential addition of $200 million following the first regulatory approval of their therapy, CTX001.

While this may sound like a hefty deal to some, Vertex actually values CTX001 at roughly $11 billion.

CTX001, which is a one-time therapy, is priced at roughly $1 million per patient. At this point, the market for beta thalassemia is valued at $32 billion.

Needless to say, this would make CTX001 a massive income generator in the next few years.

Considering the lucrative market for beta thalassemia, though, it’s no surprise that several competitors have emerged to grab their share as well.

Some companies, such as Novartis (NVS) and Acceleron (XLRN), offer maintenance drugs for the disease.

Meanwhile, others like Protagonist Therapeutics (PTGX) and Ionis Pharmaceuticals (IONS) are attempting to develop treatments that would become direct competitors of CTX001.

However, the closest rivals of the Vertex-CRISPR candidate are from Bluebird Bio (BLUE) and Editas Medicine (EDIT).

While this has become a crowded space, Vertex and CRISPR remain the leaders in this segment, as most of the other candidates are still in the investigation phase.

Since it was founded in the 1980s, Vertex has remained true to its vision of tackling some of the toughest diseases out there.

While big pharmaceutical companies, such as AbbVie (ABBV), decided to expand their portfolio through acquisitions, Vertex leveraged its talent pool and maximized its funds by establishing strategic collaborations instead.

This tactic provided the company with enough elbow room that eventually led to its dominance in the CF space, where it now enjoys a virtual monopoly until at least the next decade.

Meanwhile, it has forged strong relationships with promising biotechnology companies and can very well be on its way to becoming the most dominant force in the rare blood disorder segment.

Overall, Vertex Pharmaceuticals is an attractive stock with an impressive portfolio and an even more impressive pipeline.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-08-19 16:00:572021-08-24 19:50:28A Low-Profile Biotech Winner

After Biogen’s (BIIB) work with Aduhelm, another biopharmaceutical company has made notable progress: Bayer (BAYRY).

Merely six weeks after DA01 landed in the clinic, Bayer’s Parkinson’s disease drug candidate is getting into the fast lane.

This marks one of the major pipeline candidates that the German company picked up from its $1 billion acquisition of Versant Ventures in 2019.

DA01 is described as a “pluripotent stem cell-derived dopaminergic neuron therapy.”

In layman’s terms, Bayer collects donor cells that have the ability to develop into any other cell type in the body.

It will then engineer these versatile cells to turn into neurons that have the capacity to produce the neurotransmitter dopamine—aka the chemical your nervous system uses to transmit messages to nerve cells.

Those engineered neurons will then be transplanted into a part of the brain, called the putamen, which is in charge of our movements and learning.

What we know so far is that the next phase of the trial will determine the safety and tolerability of the cell transplantation a year following the procedure.

This will also tell us more about the cell survival rate after the transplant and the motor effects a year or two following the procedure.

Like Biogen’s Alzheimer’s candidate, the fast-track designation with the FDA could open doors for a speedy review or even an accelerated approval for Bayer’s DA01.

Aside from transplanting engineered cells into patients’ brains, the company is also looking into other options for Parkinson’s.

In October 2020, it shelled out $2 billion upfront to acquire Asklepios BioPharmaceutical or AskBio for its gene therapy research on Parkinson’s.

Roughly 1 million people in the US are suffering from Parkinson’s disease—a number that’s greater than the combined number of patients diagnosed with Lou Gehrig’s disease, multiple sclerosis, and muscular dystrophy.

What’s worse is that this is expected to climb to 1.2 million by 2030.

In terms of treatment cost, the combined expenses for Parkinson’s, including medical bills and lost income, are estimated to reach about $52 billion annually in the US alone.

The medications alone already amount to an average of $2,500 per year, with therapeutic surgery reaching up to $100,000 per person.

This is why it comes as no surprise that several companies have been working towards figuring out a more potent treatment or even cure for Parkinson’s.

One of the frontrunners is Prevail Therapeutics, a New York-based biotechnology company that’s focused on developing a gene therapy for this disease.

Following a successful Series B financing round in 2019, in which it secured $50 million in investments, the company eventually attracted the attention of big pharma.

By December 2020, it was acquired by Eli Lilly (LLY) for $880 million with the promise to help the smaller biotech company develop three of its most promising Parkinson’s candidates.

Another Parkinson’s-centered biotech company is Axovant Gene Therapies, which has been working on a single-dose treatment for neurodegenerative disease.

Its pipeline proved to be promising, as seen in its $74.7 million public offering just last February 2020, with the company maintaining its solid footing amid the pandemic.

By November, it rebranded itself as Sio Gene Therapies (SIOX).

Outside the US is Irish biotech firm Inflazome, which is working on a unique treatment for Parkinson’s.

Unlike the other candidates, the goal of Inflazome’s drug is to directly deliver the treatment to the affected neurons. That is, it plans to pass through the blood-brain barrier.

Its research attracted the Michael J. Fox Foundation, which granted it $1 million in funding, in March 2019.

Since then, the company’s progress has attracted the attention of other major biopharmaceutical companies with Roche (RHHBY), ultimately landing the acquisition in September 2020.

Of course, talks about neurodegenerative diseases wouldn’t be complete without Biogen.

On top of its Alzheimer’s work, the Massachusetts biotechnology giant has been collaborating with San Francisco-based Parkinson’s company Denali Therapeutics.

The two have been working on the development of three small molecular drugs for $560 million in upfront payments plus $465 million in equity investment into the smaller biotech.

In addition to these, we’re still waiting on what the rest of the major biopharmaceutical companies would come up with in the future.

Given that the likes of AbbVie (ABBV), Merck (MRK), Pfizer (PFE), and AstraZeneca (AZN) have all signed up publicly via the Critical Path for Parkinson's (CPP) consortium to tackle this debilitating disease, it’s safe to say that there’s hope for the future of this sector.

After Biogen’s (BIIB) work with Aduhelm, another biopharmaceutical company has made notable progress: Bayer (BAYRY).

Merely six weeks after DA01 landed in the clinic, Bayer’s Parkinson’s disease drug candidate is getting into the fast lane.

This marks one of the major pipeline candidates that the German company picked up from its $1 billion acquisition of Versant Ventures in 2019.

DA01 is described as a “pluripotent stem cell-derived dopaminergic neuron therapy.”

In layman’s terms, Bayer collects donor cells that have the ability to develop into any other cell type in the body.

It will then engineer these versatile cells to turn into neurons that have the capacity to produce the neurotransmitter dopamine—aka the chemical your nervous system uses to transmit messages to nerve cells.

Those engineered neurons will then be transplanted into a part of the brain, called the putamen, which is in charge of our movements and learning.

What we know so far is that the next phase of the trial will determine the safety and tolerability of the cell transplantation a year following the procedure.

This will also tell us more about the cell survival rate after the transplant and the motor effects a year or two following the procedure.

Like Biogen’s Alzheimer’s candidate, the fast-track designation with the FDA could open doors for a speedy review or even an accelerated approval for Bayer’s DA01.

Aside from transplanting engineered cells into patients’ brains, the company is also looking into other options for Parkinson’s.

In October 2020, it shelled out $2 billion upfront to acquire Asklepios BioPharmaceutical or AskBio for its gene therapy research on Parkinson’s.

Roughly 1 million people in the US are suffering from Parkinson’s disease—a number that’s greater than the combined number of patients diagnosed with Lou Gehrig’s disease, multiple sclerosis, and muscular dystrophy.

What’s worse is that this is expected to climb to 1.2 million by 2030.

In terms of treatment cost, the combined expenses for Parkinson’s, including medical bills and lost income, are estimated to reach about $52 billion annually in the US alone.

The medications alone already amount to an average of $2,500 per year, with therapeutic surgery reaching up to $100,000 per person.

This is why it comes as no surprise that several companies have been working towards figuring out a more potent treatment or even cure for Parkinson’s.

One of the frontrunners is Prevail Therapeutics, a New York-based biotechnology company that’s focused on developing a gene therapy for this disease.

Following a successful Series B financing round in 2019, in which it secured $50 million in investments, the company eventually attracted the attention of big pharma.

By December 2020, it was acquired by Eli Lilly (LLY) for $880 million with the promise to help the smaller biotech company develop three of its most promising Parkinson’s candidates.

Another Parkinson’s-centered biotech company is Axovant Gene Therapies, which has been working on a single-dose treatment for neurodegenerative disease.

Its pipeline proved to be promising, as seen in its $74.7 million public offering just last February 2020, with the company maintaining its solid footing amid the pandemic.

By November, it rebranded itself as Sio Gene Therapies (SIOX).

Outside the US is Irish biotech firm Inflazome, which is working on a unique treatment for Parkinson’s.

Unlike the other candidates, the goal of Inflazome’s drug is to directly deliver the treatment to the affected neurons. That is, it plans to pass through the blood-brain barrier.

Its research attracted the Michael J. Fox Foundation, which granted it $1 million in funding, in March 2019.

Since then, the company’s progress has attracted the attention of other major biopharmaceutical companies with Roche (RHHBY), ultimately landing the acquisition in September 2020.

Of course, talks about neurodegenerative diseases wouldn’t be complete without Biogen.

On top of its Alzheimer’s work, the Massachusetts biotechnology giant has been collaborating with San Francisco-based Parkinson’s company Denali Therapeutics.

The two have been working on the development of three small molecular drugs for $560 million in upfront payments plus $465 million in equity investment into the smaller biotech.

In addition to these, we’re still waiting on what the rest of the major biopharmaceutical companies would come up with in the future.

Given that the likes of AbbVie (ABBV), Merck (MRK), Pfizer (PFE), and AstraZeneca (AZN) have all signed up publicly via the Critical Path for Parkinson's (CPP) consortium to tackle this debilitating disease, it’s safe to say that there’s hope for the future of this sector.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-07-22 15:00:352021-07-31 02:57:00Another Step Closer to Neuro-Victory

Spinoffs have historically been known to deliver healthy returns for their investors.

A good example is PayPal (PYPL), which grew sevenfold since 2015 following its spinoff from eBay (EBAY).

A more recent example is Carrier Global (CARR), which tripled its shares amid the pandemic after its spinoff from United Technologies (UTC) last year.

Basically, spinoffs allow smaller segments of companies to thrive on their own or push high-growth divisions to expand faster.

Over the past months, the cheapest stocks found in the S&P 500 have recently spun off pharmaceutical companies: Viatris (VTRS) and Organon (OGN).

Viatris is a spinoff of Pfizer (PFE), which merged with Mylan, while Merck (MRK) jettisoned Organon (OGN) just last month.

Both are brand new and still under the radar, particularly among investors who don’t follow healthcare updates.

While these two have yet to impress the market, both exhibit potential that could make them promising long-term prospects.

Viatris holds an extensive portfolio of drugs courtesy of Pfizer’s Upjohn unit and Mylan’s pipeline.

The list includes the previously top-selling Lipitor, Viagra, Lyrica, and even Norvasc from Pfizer. It also has Mylan’s income-generating EpiPen along with the company’s HIV/AIDS therapies and 7,500 marketed products across the globe.

To date, Viatris has fallen roughly 30% from its average price target. It’s not for the subpar performance of its products though. This is mostly attributed to the lack of attention from investors and possibly a bit of skepticism from some analysts.

However, Viatris has a really good value proposition.

The main goal of the biggest names in the biopharmaceutical sector, such as Johnson & Johnson (JNJ), Eli Lilly (LLY), AbbVie (ABBV), AstraZeneca (AZN), GlaxoSmithKline (GSK), Bristol-Myers Squibb (BMY), and Gilead Sciences (GILD), is to develop and launch the best-in-class treatments to market.

To achieve that, these industry giants are granted a set period to exclusively sell and market each new drug that gains approval.

This would allow them to command a premium price, which in turn would give them the money to fund the next round of research and development needed to come with the next generation of newer and improved versions of the treatment.

However, not everyone can afford those premium prices.

So when the periods of exclusivity end, there are companies like Mylan—now Viatris—that are allowed to manufacture generic versions of those branded drugs and sell them at lower prices.

The list of drugs with soon-to-expire patents for which Viatris has been working on creating biosimilars or generic versions include Humira from AbbVie, which recorded peak sales at $20 billion; Eylea from Regeneron (REGN), which peaked at $7.5 billion; and even Allergan’s Botox, which peaked at $5 billion.

Viatris is also working on biosimilars for Roche’s (RHHBY) cancer treatments Avastin, which had peak sales of $7 billion, and Perjeta, which peaked at $5 billion.

Obviously, Viatris will not reach the same height of success as the companies that created those branded drugs.

But, if it manages to achieve even only 10% of those numbers, then it can generate roughly $4 to $5 billion in sales—and that’s just the tip of the iceberg.

So far, Viatris owns at least 1,400 approved molecules applicable in roughly 10 therapeutic segments.

It has roughly 350 products in its pipeline at the moment, with each item estimated to generate approximately $100 million to $500 million in sales.

With its current performance and access to 165 countries and territories, Viatris is expected to generate roughly $224 billion in global sales annually.

With all these in mind, Viatris’ value proposition looks impressively strong to me.

More importantly, this Pfizer spinoff has the capacity to become the world’s first dominant generic and biosimilar drug manufacturer, with its revenues potentially becoming comparable to major pharmaceutical companies at some point.

The same value proposition could be behind Organon, as this newly spun-off company markets Merck’s off-patent drugs.

While the move to separate from its parent company has yet to show tangible results, Organon is projected to rake $6.1 billion to $6.4 billion in revenue for 2021, with annual sales expected to rise in mid-single digits and dividends anticipated to be about 3%.

The biosimilars market is still relatively young, with only 60 biosimilars approved in the EU and 29 in the US thus far. In total, those represent a market worth approximately $17 billion.

Conservative estimates project that the global biosimilars market will be worth $692 billion by 2027, considerably outpacing the mainstream pharmaceutical sector.

Given their potential and prospect for future gains, the low prices for companies like Viatris and Organon present rare opportunities to grab long-term investments.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-07-13 14:00:032021-07-18 21:45:54Spinoff Stocks Poised for Long-Term Growth

There is a huge possibility that the first person to ever live to a thousand years old has been born in our lifetime.

That’s according to experts on life longevity. They also say that sooner rather than later, we’ll simply be checking ourselves into hospitals or clinics once every decade.

Pretty much how you’d bring your car in for a service, that’s how we’ll keep our bodies working at peak condition for centuries.

As far-fetched as it sounds, it’s undeniable that dreams of achieving immortality are as old as mankind itself.

One of the leading experts on this is the Human Longevity, Inc., which has leading genomics expert J. Craig Venter and billionaire Peter Diamandis as its founders.

Although it’s still not yet a publicly-traded company, Human Longevity, Inc. has been collaborating with cancer diagnostics firm Neogenomics (NEO).

Admittedly, NEO’s $5.32 billion market capitalization doesn’t really boost that much confidence in this company.

However, Human Longevity’s work with a Big Pharma company like AstraZeneca (AZN), which holds a market cap of $158.14 billion, definitely backs up its claims.

Moreover, AstraZeneca and Human Longevity are already halfway through their 10-year agreement that dates back to 2016.

Basically, what Human Longevity does is sequence an individual’s DNA and combine the information with an extensive list of tests to figure out how long that person will live and what steps can be taken to extend his or her life.

More impressively, the company can use the data to predict a budding disease, such as cancer, even before it exhibits symptoms.

And how much will that cost you?

Right now, the company is charging $25,000 for a comprehensive set of tests and a full profile.

In the end, you’d be given medical information about yourself that amounts to roughly 1 petabyte. For context, that’s 1,000 terabytes or 1 million GB worth of data.

While the cost is definitely high, it’s a good preventive measure to consider if you can spare the cash.

This is because the company can detect the slightest hint of diseases, which are typically at their most treatable phase.

Since the company is founded on the belief that we are all “DNA software-driven species,” it can also determine the disease-producing genes in our systems and use them as “pharmaceutical targets, so that people with those genetic changes don’t die.”

Aside from Human Longevity, another company working on this nice is called Life Biosciences, which was founded in 2017.

Since its launch, Life Biosciences has been acquiring companies left and right to boost its pipelines.

So far, it has at least 6 subsidiaries focused on developing treatments to fight the human aging process.

What makes Life Biosciences different is that it doesn’t focus on the leading causes of death, such as cardiovascular diseases or cancer.

Instead, it tries to figure out what are the underlying causes of the body’s aging. This includes stem cell exhaustion, cellular senescence, chromosomal instability, and even our metabolism.

At their core, Life Biosciences’ belief is that aging itself should not be considered a natural biological result of the passage of time.

Rather, it should be understood as a medical condition—the kind that can be treated in the same way we’d try to find medications or cures for diseases.

While Life Biosciences’ work has yet to earn any FDA approval, the involvement of GlaxoSmithKline (GSK) in its aging research seems to boost confidence in the company’s work.

Apart from GSK, a number of tech billionaires have expressly backed these efforts in the anti-aging field.

The most visible ones include Calico, which is backed by Google and AbbVie (ABBV), and Unity Biotechnology, supported by Jeff Bezos.

While Human Longevity and Life Biosciences have yet to go on IPO, there are already companies working on fields related to life longevity.

The first names that come to mind are the frontrunners of the genome sequencing market, such as Illumina (ILMN), Thermo Fisher Scientific (TMO), and 10x Genomics (TXG).

Smaller companies in this field include bluebird Bio (BLUE), CRISPR Therapeutics (CRSP), and Editas Medicine (EDIT).

Inasmuch as this is difficult to grasp at this stage, there is a massive market for this industry. In fact, the global longevity segment is projected to reach $27 trillion in 2026, which accounts for roughly 20% of the global GDP.

Meanwhile, the global market for human aging is estimated to reach at least $55 billion by 2023.

And those are just conservative estimates.

Making the public accept the idea behind longevity science has not been easy. Even with Big Pharma names backing these innovative companies, people are still wary of the concept.

After all, surveys show that most people would refuse medical treatments to slow their aging and allow them to live up to 120 or older. It’s not surprising why.

Those respondents probably witnessed how their older grandparents and parents spent their final years in pain and were subjected to invasive medical procedures. That makes the entire idea of living so long horrific to them.

However, the future imagined by these companies is different. Through their research, people can live long and still enjoy active and healthy lifestyles.

At this point, the longevity science space remains a playground dominated by a handful of transhumanists and even biohackers.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-07-08 15:00:082021-07-15 15:28:40Turning the Biohackers' Dream to Reality

Mad Hedge Biotech & Healthcare Letter May 27, 2021 Fiat Lux

FEATURED TRADE:

(A SAFE STOCK FOR YOUR PEACE OF MIND) (JNJ), (ABBV), (TDOC), (MSFT)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-05-27 15:02:342021-05-27 20:21:42May 27, 2021

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.