Mad Hedge Biotech and Healthcare Letter

January 21, 2025

Fiat Lux

Featured Trade:

(THE ONLY TIME FIGHTING YOURSELF MAKES MONEY)

(ABBV), (AMGN), (SDZNY), (CHRS), (PFE), (JNJ), (ALVO), (TEVA), (SNY), (BMY)

Mad Hedge Biotech and Healthcare Letter

January 21, 2025

Fiat Lux

Featured Trade:

(THE ONLY TIME FIGHTING YOURSELF MAKES MONEY)

(ABBV), (AMGN), (SDZNY), (CHRS), (PFE), (JNJ), (ALVO), (TEVA), (SNY), (BMY)

If I had a dollar for every time someone told me the biotech sector was overvalued, I'd have enough to fund my own drug development program.

Yet here we are, watching the global immunology market rocket from $55 billion to $166 billion in just a decade, with the sector projected to hit $192 billion by 2028.

If you're wondering why big pharma keeps pouring billions into autoimmune research - and believe me, this question came up in every meeting last week - the answer is simple: we've barely scratched the surface.

Despite thousands of PhDs burning midnight oil in labs from Boston to Basel, we still don't have effective treatments for systemic lupus erythematosus, scleroderma, or even something as visible as vitiligo.

Want to see where the smart money is going? Look no further than the biosimilar stampede into AbbVie's (ABBV) Humira territory.

Like bargain hunters at a Black Friday sale, everyone's getting in line: Amgen (AMGN) with Amjevita, Sandoz (SDZNY) with Hyrimoz, Coherus (CHRS) with Yusimry, and Pfizer (PFE) with Abrilada.

And just when you thought the party was over, here comes Amgen's Wezlana challenging Johnson & Johnson's (JNJ) Stelara, followed by Alvotech (ALVO) and Teva's (TEVA) Selarsdi.

But here's where it gets interesting. I've identified four companies that are trading at valuations that would make Benjamin Graham smile.

First up is AbbVie, trading at 15.96x earnings (11.9% below sector median), with projected EPS growth to $15.21 by 2027.

Their dynamic duo of Rinvoq and Skyrizi is performing like a biotech version of Batman and Robin.

Rinvoq sales hit $1.61 billion in Q3 2024, up 45.4% year-over-year, while Skyrizi broke $3 billion, thanks to its mid-2024 FDA approval for ulcerative colitis.

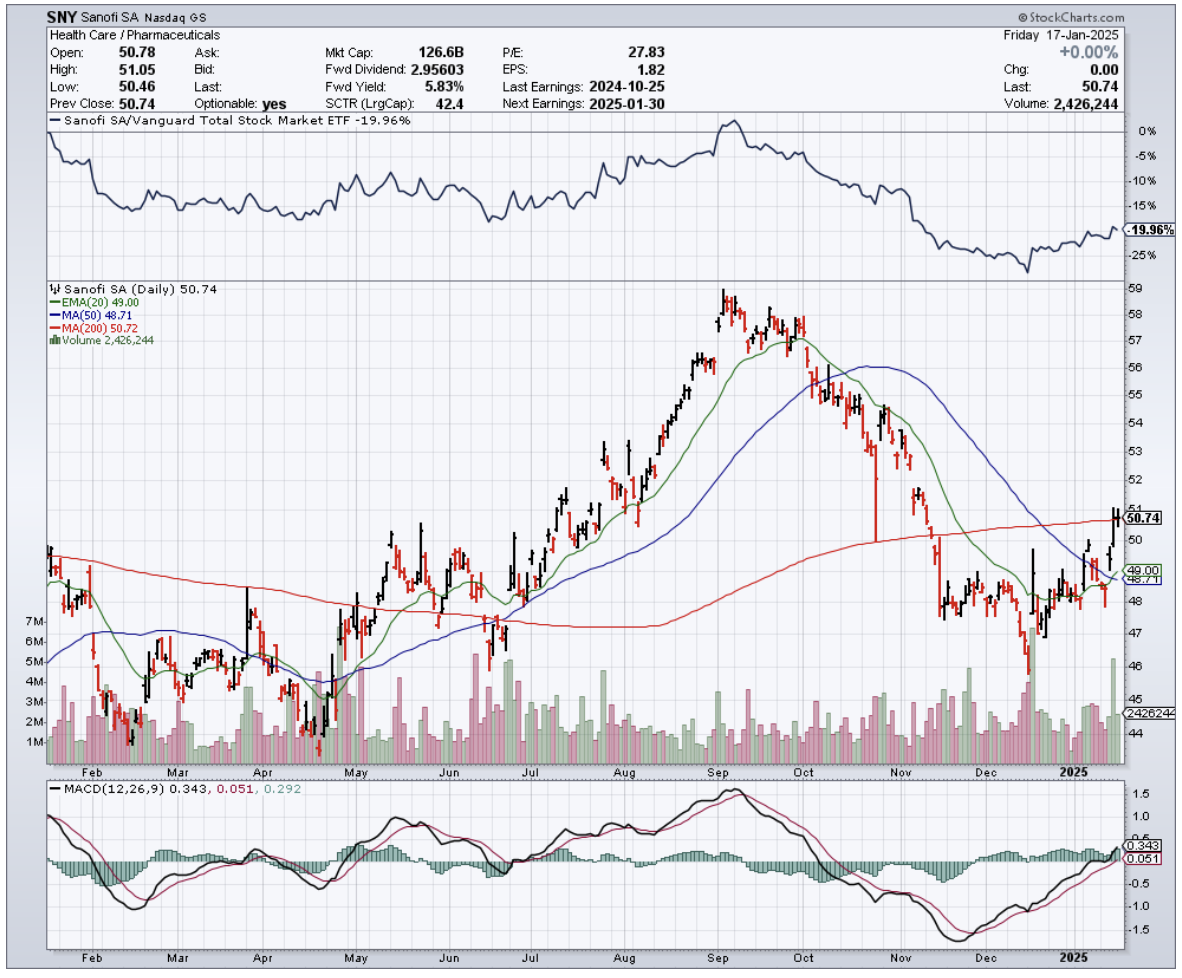

As for Sanofi (SNY)? Now we're talking value. At 11.7x earnings - 35.39% below sector median and 1.3% below its 5-year average - it's like finding a Ferrari priced like a Fiat.

Their star player Dupixent raked in 3.48 billion euros in Q3 2024, up 22.1% year-over-year and 5.2% quarter-over-quarter.

Then, there’s Teva Pharmaceuticals. Trading at a P/E ratio of 7.88x - that's 56.5% below the sector median - while projecting non-GAAP EPS growth to $3.6 by 2028.

But here's the kicker: their clinical trial data reads like a biotech investor's dream. Their new drug duvakitug achieved 47.8% clinical remission in ulcerative colitis patients versus 20.45% for placebo (p=0.003).

In Crohn's disease? Even better - 47.8% endoscopic response compared to 13% for placebo (p<0.001).

Finally, there's Bristol-Myers Squibb (BMY). Yes, it's trading at 47.5x earnings (162.1% above sector median), but here's where patience pays off - their P/E ratio is expected to drop to 8.82x by 2027.

Meanwhile, Zeposia sales jumped 19.5% year-over-year to $147 million in Q3 2024, while Sotyktu showed consecutive quarterly growth.

The cherry on top? These companies are paying you to wait. We're talking dividend yields from 3.8% to 4.41% - try getting that from your savings account.

Looking at these numbers reminds me of the tech sector in the late 1990s, but with one crucial difference - these companies are actually making money, lots of it.

They generate significant cash flow and have strong balance sheets, unlike many of the high-flying tech companies of the dot-com era that were burning through cash with no clear path to profitability.

While others are chasing the next meme stock or crypto moonshot, smart investors are quietly positioning themselves in companies that are literally changing the face of medicine.

Remember, buying umbrellas in the summer heat has always been my style.

Right now, the immunology sector is experiencing its own kind of summer, and these four stocks are your umbrellas.

The forecast? Growth storms ahead.

Mad Hedge Biotech and Healthcare Letter

November 19, 2024

Fiat Lux

Featured Trade:

(HONEY, I SHRUNK THE MARKET CAP)

(ABBV), (BMY), (AVNX)

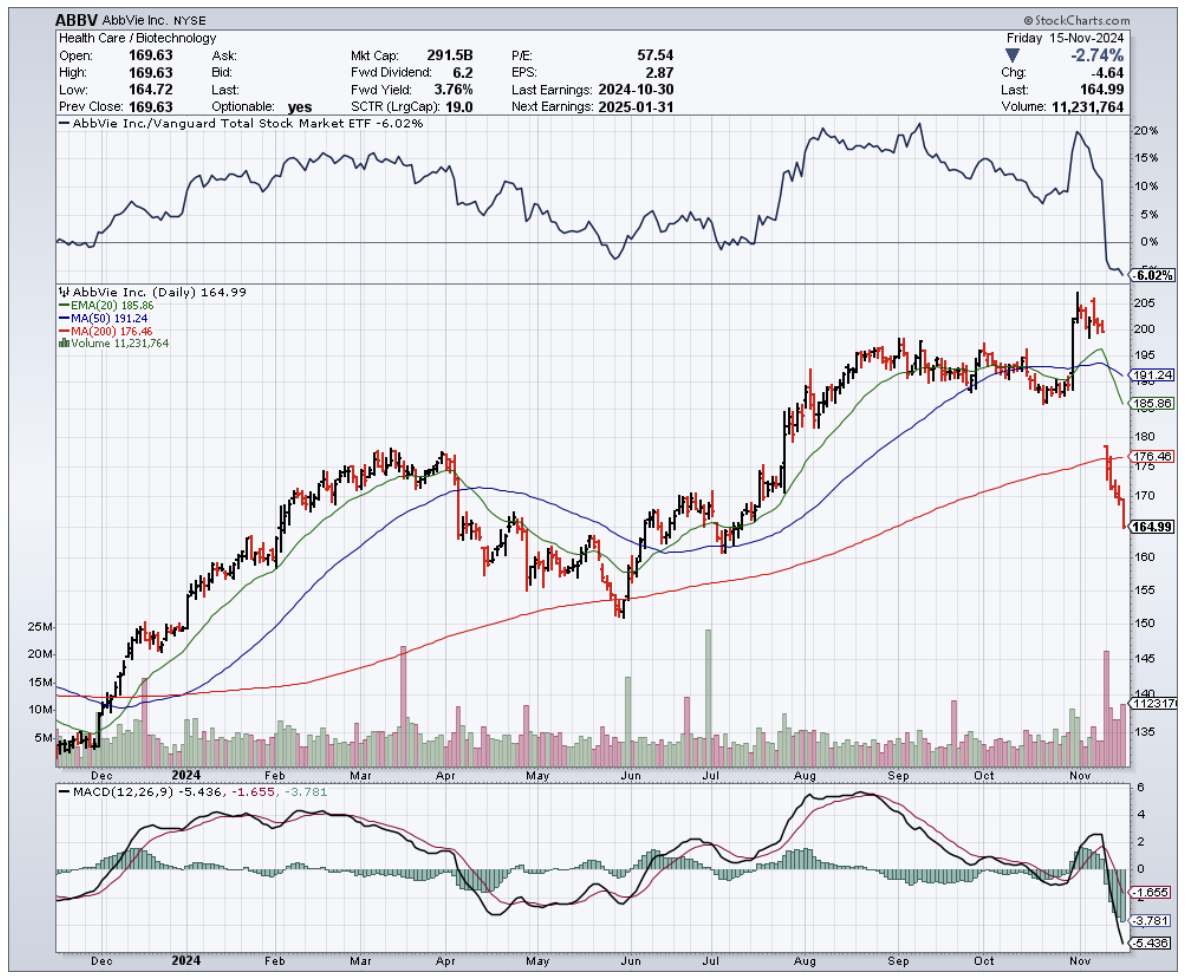

If you've ever wondered what $9 billion in disappointment looks like, ask the folks at AbbVie (ABBV). They've just learned the hard way that even the most promising psychiatric drugs can pull a vanishing act worthy of Houdini when it comes to clinical trials.

Their great hope, emraclidine – a name that sounds like it could either cure schizophrenia or clean your bathtub – recently face-planted in not one, but two Phase 2 trials.

Dr. Roopal Thakkar, AbbVie's Chief Scientific Officer, probably wishes this particular day came with a reset button, as the company's experimental once-daily pill performed with all the therapeutic punch of a sugar tablet in treating schizophrenia.

Somewhere, in a parallel universe, there's probably a version of Dr. Thakkar who didn't just watch $40 billion in market value evaporate faster than a teenager's allowance at a gaming convention.

Unfortunately, in our universe, AbbVie's stock took a 12.6% nosedive to $174.43.

But here's where it gets interesting, in that peculiar way that only Wall Street can manage. While AbbVie was having its very bad, no-good day, Bristol Myers Squibb (BMY) was practically dancing in the streets.

Their shares shot up 11% faster than you can say "competitive advantage." Why? Because their own schizophrenia drug, Cobenfy (another name that sounds like it came from the same random pharmaceutical name generator), just got the FDA's blessing.

Talk about impeccable timing.

Let's put this in perspective: We're talking about a global market worth $7.90 billion in 2023, projected to balloon to $11.35 billion by 2030. And it's not just about money.

The World Health Organization tells us there are 24 million people worldwide living with schizophrenia.

In the U.S. alone, it affects between 0.25% and 0.64% of adults, according to the National Institute of Mental Health. That's roughly the population of a small city, all waiting for better treatment options.

Meanwhile, other players in this high-stakes game are making moves that would impress a chess grandmaster.

Take Teva Pharmaceutical Industries (TEVA), busy cooking up a long-acting injectable version of olanzapine.

Or Alkermes plc (ALKS), sitting pretty with their $1.17 billion in revenue for 2022, thanks partly to their own injectable antipsychotic, Aristada.

Then there's H. Lundbeck A/S (HLBBF), the Danish company that spends 18% of its $2.7 billion revenue on R&D, like a scientist with an unlimited coffee budget.

And let's not forget the plucky underdog, Anavex Life Sciences Corp. (AVXL), burning through cash like a marathon runner through calories ($31.6 million in losses for 2022) while chasing their own psychiatric breakthrough.

Their compound, ANAVEX 3-71, sounds like a droid from Star Wars but might just be the next big thing in schizophrenia treatment. Or not.

That's the beauty and terror of biotech investing – you never quite know if you're backing the next breakthrough or the next spectacular failure.

AbbVie, thankfully, isn't exactly heading for the poorhouse. Their blockbuster drug Humira raked in $21 billion in 2022 alone – enough to buy everyone in New Zealand a really nice dinner.

The truth is, navigating the biotech market is less like following a recipe and more like trying to predict where lightning will strike while riding a unicycle.

So here's your biotech shopping list, served with a side of market reality.

AbbVie's spectacular face-plant has created a buying opportunity for the patient investor (that $21 billion Humira cushion makes for a soft landing).

Bristol Myers Squibb is strutting around with their fresh FDA approval like they own the place (and right now, they kind of do).

And if you're feeling particularly adventurous, Anavex Life Sciences offers a lottery ticket that might just pay off.

Whatever you choose, just remember to keep your antacids handy.

Mad Hedge Biotech and Healthcare Letter

November 5, 2024

Fiat Lux

Featured Trade:

(DANCING WITH SHADOWS)

(RHHBY), (SGMO), (LLY), (BIIB), (ABBV)

In 1906, Dr. Alois Alzheimer first encountered what he called a “mysterious” mental illness, examining the brain of a 55-year-old woman who had died under strange neurological circumstances.

Over a century later, that mystery hasn’t let up. We’re still scratching our heads—and burning through money.

By 2050, Alzheimer’s is projected to cost the U.S. healthcare system $1.3 trillion, more than the entire GDP of Australia.

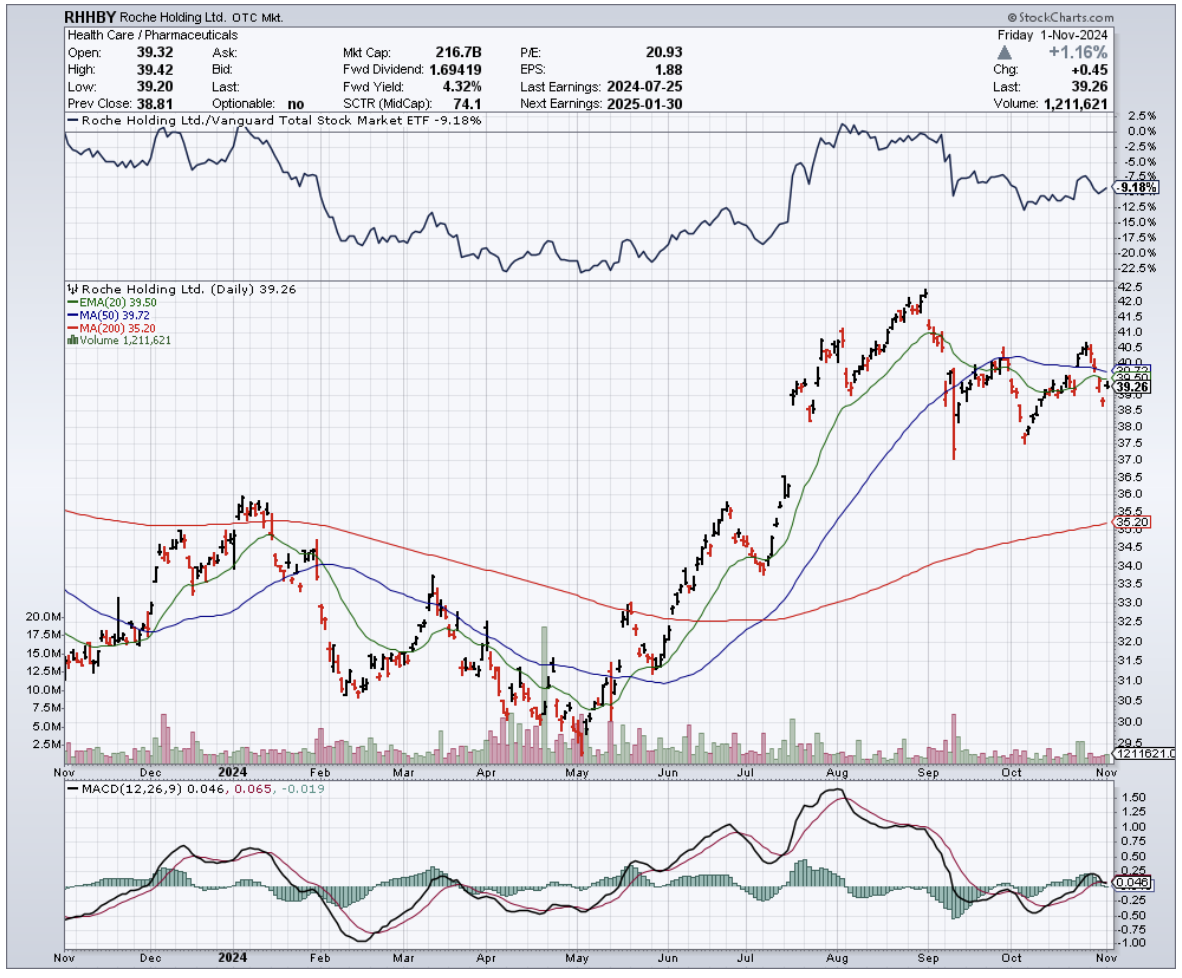

But something’s happening at Roche (RHHBY) that’s got my scientific spidey senses tingling.

Roche has been chasing Alzheimer’s solutions for over two decades, pouring resources into this elusive brain burglar that defies every rule in the book.

And yet, here they are—undaunted, driven by a noble (and, yes, profitable) goal to relieve the massive toll AD takes on patients, families, and entire healthcare systems.

It hasn’t been smooth sailing; setbacks and “whoops, not this time” moments have kept things bumpy. Recently, though, I’ve been seeing hints of a breakthrough that just might bring this long, shadowy dance with Alzheimer’s closer to the light.

For those who've been reading my letter since 2008, you know I rarely get excited about big pharma unless there's real meat on the bone. Well, this time there is, and it's called Brainshuttle technology.

If you’ve never heard of it, think of it as a kind of souped-up delivery service for the brain—no, not that kind. This tech helps Roche’s meds cross the blood-brain barrier, that stubborn security guard that only lets a select few molecules into the brain.

It’s great at keeping out random junk but also frustratingly good at blocking drugs we actually want to get in there.

Brainshuttle could change that, allowing antibodies to cross over more easily and making lower doses (and hopefully fewer nasty side effects) possible.

Enter trontinemab, a drug that’s caught a lot of eyes recently. Armed with Brainshuttle, this amyloid-beta antibody is like the brain’s personal pest control.

Early trials are promising: Roche reported that trontinemab is sweeping out amyloid plaque faster than a Roomba on espresso, and all at lower doses.

Less dose, more punch, and fewer side effects? Sounds like the AD holy grail. They’re even eyeing an accelerated approval path with the FDA.

Now, the FDA isn’t exactly known for sprinting to approval—especially with Alzheimer’s drugs—but trontinemab’s early results make it a strong contender.

But Roche isn’t putting all its eggs in one beta basket. AD research has been dominated by amyloid-beta, but there’s another protein that scientists are pretty excited about: tau.

If amyloid-beta is the ringleader, tau is the muscle, the heavy that clogs up brain cells and wreaks havoc.

To tackle tau, Roche has teamed up with Sangamo Therapeutics (SGMO), a company with tech that sounds like it’s straight out of a sci-fi novel—zinc finger molecules.

These little DNA-grabbers are designed to silence the tau gene, essentially telling it to cool it and stop producing the stuff that clogs up the brain.

The partnership also gives Roche access to something else in Sangamo’s arsenal: an adeno-associated virus capsid. (Translation: a delivery mechanism that gets things across the blood-brain barrier.)

If these tools work as planned, Roche may have a real chance to give AD a one-two punch with both amyloid-beta and tau treatments.

But let's be real here. This is still the Wild West of biotech, and Roche has had its share of setbacks.

They recently walked away from a partnership with UCB, returning the rights to an anti-tau antibody called bepranemab.

Even though UCB called the Phase 2a data "encouraging," it apparently didn't meet Roche's internal bar. That's the thing about Alzheimer's drug development - it's about as predictable as my teenager's mood swings.

The competition isn't sleeping either. Eli Lilly (LLY), Biogen (BIIB), and AbbVie (ABBV) are all throwing everything but the kitchen sink at this disease. But Roche's Brainshuttle technology might just be their secret weapon in this fight.

Here's what keeps me optimistic: Roche’s multi-pronged strategy, combining amyloid-beta and tau, might just give them an edge. It’s not guaranteed—far from it—but having multiple avenues does give them a better shot at success.

This is what I call a "chess not checkers" opportunity. The potential payoff is massive - we're talking about a market that could make crypto's best days look like pocket change. But timing is everything.

So, I'll be watching trontinemab's development like a hawk. The Sangamo collaboration is also on my radar - any breakthrough in tau-targeted therapies could be a game-changer.

As always, don’t bet the farm, folks—not even on a biotech darling like this. But if you’re itching to add a little intellectual flair to your portfolio, Roche’s Alzheimer’s gambit is worth a look. Buy the dip, but set those stop losses. After all, even the best-laid plans of mice and biochemists often go awry.

Mad Hedge Biotech and Healthcare Letter

August 13, 2024

Fiat Lux

Featured Trade:

(THE RISE OF THE STEADY EDDIES)

(CNC), (UNH), (PFE), (JNJ), (ABBV), (LLY), (BIO), (UHS), (WAT), (AMGN), (REGN), (VRTX), (CRSP), (MRNA)

Think of the market as a body fighting off an infection. Tech stocks might be the flashy antibodies, but healthcare is the steady, reliable immune system, keeping things stable when the going gets tough. And right now, that immune system is looking stronger than ever.

Skeptical? I get it. We've heard the hype about healthcare before. But this time, it's different.

The Healthcare Select Sector SPDR ETF (XLV) has been on a tear, up 9.3% this year as of Thursday's close. That's nearly keeping pace with the broader S&P 500's 12% gain - a remarkable feat in a market that's been anything but stable.

But what's even more impressive is the turnaround. Back in mid-July, XLV was lagging behind like a three-legged horse in the Kentucky Derby, up only 8.3% while the S&P 500 was showing off with an 18% gain.

In fact, out of the 63 healthcare stocks in the S&P 500, only a dozen have been slacking off since July. The rest? They've been outperforming like it's going out of style.

So what changed?

Well, it wasn't so much that healthcare stocks suddenly discovered the fountain of youth. No, my friends, it was more like the rest of the market decided to take a swan dive off the high board.

You see, while tech stocks were busy doing their best Icarus impression – flying too close to the sun and then plummeting back to earth – healthcare stocks were steady as she goes. It's like the old tortoise and hare story, except in this version, the hare got distracted by shiny objects and ran off a cliff.

Now, let's shine the spotlight on some of the key players driving this healthcare rally.

Remember those health insurers everyone was worried about back in spring? The ones that had investors biting their nails over the future of Medicare Advantage? Well, they've made a comeback.

The S&P 500 Managed Health Care index was down 12% in mid-April, looking about as healthy as a chain smoker with a Big Mac habit. But now? It's up 4.5% since the start of the year.

Companies like Centene (CNC) and UnitedHealth Group (UNH) have bounced back faster than a rubber band on steroids.

And it's not just the insurers. Big Pharma's been flexing, too.

Pfizer (PFE), the company that became a household name faster than you can say "vaccine," is holding steady. Johnson & Johnson (JNJ) is up 2.2%, probably thanks to all that baby powder they're not selling anymore.

Meanwhile, AbbVie’s (ABBV) up 11% since July. These guys are like the Energizer Bunny of the pharma world – they just keep going and going.

But the real showstopper? Eli Lilly (LLY). This biopharma has been on a tear since the beginning of 2024. Up 45% on the year at one point, they've been climbing faster than a squirrel up a tree with a dog in hot pursuit.

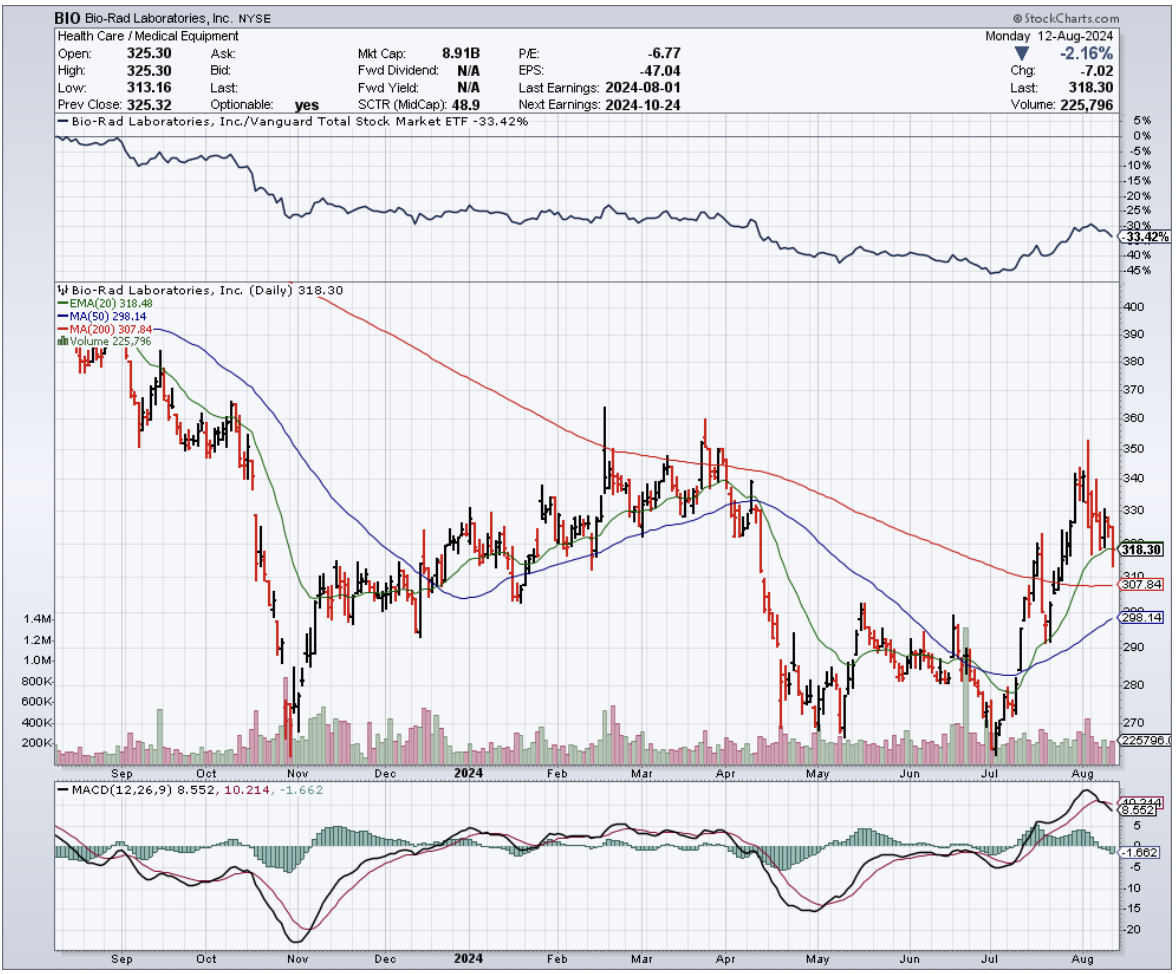

Then, there are companies like Bio-Rad Laboratories (BIO), up 20% since July. Universal Health Services (UHS)? Up 18% since July. Waters (WAT), the life sciences tools folks? Up 15%.

Even the biotechs are out to impress.

Amgen (AMGN), the granddaddy of biotech, is up 10% year-to-date. They're selling drugs like Prolia and Enbrel faster than hotcakes at a lumberjack convention.

And Amgen’s pipeline? It’s packed with potential blockbusters, setting the stage for further expansion in the future.

Gilead Sciences (GILD)? Up 15% year-to-date. Turns out, their COVID-19 treatment, Remdesivir, is back in vogue like bell-bottom jeans. And their HIV and hepatitis C drugs? They're still growing stronger.

But the real rock star of biotech? That'd be Regeneron Pharmaceuticals (REGN). These guys are up over 30% year-to-date. They're treating everything from eye diseases to cancer to inflammation.

Vertex Pharmaceuticals (VRTX) is another one to watch. Up 12% this year, they've got the cystic fibrosis market cornered. And they're not stopping there – they're expanding faster thanks to their collaboration with the likes of Crispr Therapeutics (CRSP).

Now that I’ve mentioned gene therapy, I know you're wondering about Moderna (MRNA). After all, weren’t they the darlings of the COVID era? Well, yes and no.

Their stock's down about 35% year-to-date, but don't count them out just yet. Their mRNA technology is hotter than a jalapeño popper fresh out of the fryer. They might be down, but they're definitely not out.

So, what's the takeaway here? I suggest you keep your eyes peeled on the biotechnology and healthcare sectors. After all, in this market, the best offense might just be a good defense – and what's more defensive than betting on the sector that keeps us all alive and kicking?

Mad Hedge Biotech and Healthcare Letter

August 8, 2024

Fiat Lux

Featured Trade:

(WHEN A+ PROFITS MEET C-VALUATION)

(AMGN), (ABBV), (GILD)

Mad Hedge Biotech and Healthcare Letter

August 1, 2024

Fiat Lux

Featured Trade:

(THE PLAYBOOK FOR A BIOTECH TRIPLE CROWN)

(ABBV), (TEVA), (PFE), (AMGN), (AZN), (BGNE), (LLY), (CERE)