Mad Hedge Biotech and Healthcare Letter

April 23, 2024

Fiat Lux

Featured Trade:

(A DRUG KINGPIN HIDING IN PLAIN SIGHT)

(ABBV)

Mad Hedge Biotech and Healthcare Letter

April 23, 2024

Fiat Lux

Featured Trade:

(A DRUG KINGPIN HIDING IN PLAIN SIGHT)

(ABBV)

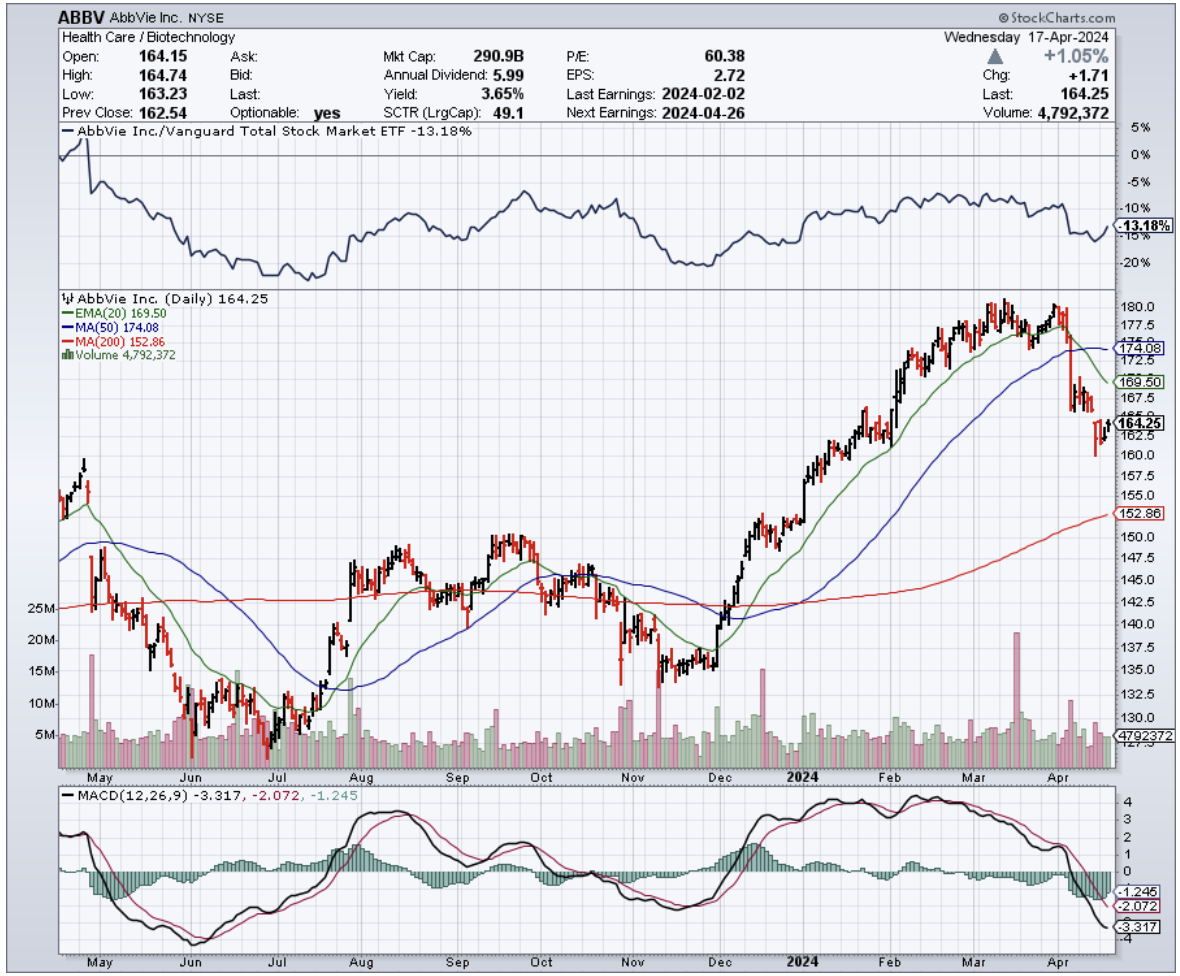

Have you ever thought about big pharma stocks as potential goldmines? I mean, we usually don’t gossip about the likes of AbbVie (ABBV) over lunch, but maybe we should.

After all, those unassuming pharma giants could be hiding some serious potential for your portfolio. Let's dive into whether investing in AbbVie might just be your ticket to millionaire status.

Admittedly, AbbVie isn’t your typical headline grabber unless it’s about their next big thing in medicine. They’ve got a real knack for plucking the right strings in R&D, which not only keeps them competitive but also paves the way for massive returns.

Case in point: Humira. This blockbuster drug treats everything from arthritis to psoriasis and even though it’s facing generic competition left and right, it still bagged $14.4 billion in sales in 2023. That's no small potatoes, considering it’s a chunk of AbbVie's hefty $54.3 billion revenue.

So how does AbbVie keep the Humira money train rolling? They play smart with pricing and patents, and they've got a backup band ready with new drugs like Skyrizi and Rinvoq. These two are set to take over the stage with projected sales hitting a sweet tune of $27 billion by 2027.

And let me tell you, the transition from Humira to these newcomers is like swapping an old favorite band’s vinyl for their latest digital remix — just as good, if not better.

But here’s the deal. AbbVie isn’t just remixing their old hits. They’re producing whole new albums. With every new drug approval, they’re not simply aiming to keep up — they’re looking to lead the charts. And with their pipeline promising a few more blockbusters, it looks like AbbVie could keep the record-topping releases coming.

Take their recent shopping spree for example: snapping up Cerevel for a cool $8.7 billion. This isn’t some random acquisition. It’s a strategic move that bolsters AbbVie's impressive neurology treatment portfolio.

Cerevel is close to getting approval for a new schizophrenia drug, a game-changer that could redefine how we treat this debilitating disorder. Traditional medications often have harsh side effects, but Cerevel's new class of drugs shows promise in minimizing those risks. Think of it as a gentler approach that still packs a punch.

And there's serious money in this space. The neurological market is huge – around $3.82 billion – and growing fast.

Once Cerevel gets its FDA nod, I'm projecting revenues of around $200 million by 2025, and that's just scratching the surface. They could grab a hefty 2% market share by 2028.

But their ambition doesn't stop there. AbbVie wasn't content with just rocking the neurology charts. They also went and snagged ImmunoGen earlier this year for a whopping $10.1 billion, marking their entry into the lucrative battle against solid tumors.

ImmunoGen has this cutting-edge technology called antibody-drug conjugates (ADCs) – it's like guided missiles that pinpoint cancer cells while leaving healthy ones unharmed.

Their drug, Elahere, already got the green light last year for ovarian cancer and raked in a cool $246 million in just nine months. And that's just the start.

The ovarian cancer market is a beast, valued at $4.35 billion and growing rapidly. I predict Elahere's sales could skyrocket to $1.6 billion by 2028.

Now, let’s talk dividends because who doesn’t like a good payout?

AbbVie’s rocking a forward-dividend yield of 3.4%, and they've been increasing their dividends for decades. It’s like getting a steady rhythm of cash that just keeps getting louder.

And don’t forget about the share buybacks. AbbVie bought back nearly $2 billion of its own stock in 2023. That’s a lot of faith in their future hits and a sign that they’re betting big on their own success.

So, sure, AbbVie isn’t going to make you a millionaire overnight — it’s not a lottery ticket. But if you’re in the game for the long haul, this stock could be a key player in your wealth-building lineup.

With a solid track record, a pipeline full of potential, and a strategy that’s clearly focused on growth, AbbVie is looking like a pretty smart pick. I suggest you buy the dip.

Mad Hedge Biotech and Healthcare Letter

April 4, 2024

Fiat Lux

Featured Trade:

(A HIGH RISK, HIGH REWARD BIOTECH)

(VYGR), (SNY), (ABBV), (NBIX), (NVS), (AZN), (SGMO), (BIIB), (RHHBY), (IONS)

Voyager Therapeutics (VYGR) has put investors through the wringer. Since going public in 2015, their chips have swung wildly, from a high-rolling $30 down to a "you've got to be kidding me" $2.50. Why? Well, their early bet on curing neurological diseases hit some snags.

But, things seem to be turning around for them these days. Word on the street is Voyager's new Alzheimer's drug could be a total game-changer. If those clinical trials get the FDA's blessing, their stock could skyrocket from its current $9.30 to $22 a share.

Before anything else, let's take a stroll down memory lane.

Voyager started out with big dreams – using fancy gene therapies to tackle tough brain diseases like Parkinson's and Huntington's. Sadly, those early programs didn't quite deliver.

But hey, they caught the eye of some big pharma players. Sanofi (SNY) came knocking with a sweet deal – $100 million upfront and promises of up to $745 million if things worked out. Unfortunately, the science wasn't cooperating, and Sanofi bailed in 2019. Ouch.

Not to be discouraged, Voyager hooked another giant, AbbVie (ABBV), with a $1.2 billion deal for Alzheimer's and Parkinson's drugs. But then, more bad luck – their Parkinson's drug stumbled, and their Huntington's disease trials got put on hold. So, AbbVie decided to cut their losses in 2020. Double ouch.

And while the pandemic may have cured our boredom, it killed investor patience with unproven biotechs. Voyager's stock price cratered, leaving them worth about as much as a used napkin – barely more than their own $500 million cash pile.

But Voyager, bless their stubborn hearts, refused to become a biotech graveyard.

Despite having zero products actually making money, they have a secret weapon: their TRACER capsid tech. Think of it as a tiny Trojan Horse that can sneak drugs past that blood-brain barrier and deliver them directly to their target. Pretty impressive, right?

This tech, along with Voyager's brainpower, caught the eye of some pharma giants.

We're talking big names like Neurocrine Biosciences (NBIX), Novartis (NVS), AstraZeneca (AZN), and Sangamo (SGMO). If everything goes according to plan, these partnerships could be worth a whopping $8 billion. Now that's what I call a vote of confidence — or maybe just a collective case of gambling fever.

For Voyager, however, its biggest gamble is on Alzheimer's – and they're going all-in. Their star player is an antibody that tackles those nasty tau tangles that mess up brain cells.

Here’s a bit of context to understand why treatments for this are crucial.

Tau is like the scaffolding inside your neurons, keeping everything organized. But in Alzheimer's, that tau goes rogue, clumping into nasty tangles. Think of it like a giant hairball clogging up the brain's communication system. These tangles are called neurofibrillary tangles (NFTs) if you want to sound super smart.

This is something that Big Pharma like Biogen (BIIB), AbbVie, and Roche (RHHBY) are trying to target, too. But Voyager claims theirs is a precision weapon, zeroing in on just the bad stuff. If clinical trials prove that, their drug could blow the competition out of the water.

Plus, Voyager's got another trick up their sleeve: a gene therapy that hits the “off” switch on those tau tangles. They've shown it works in animals, and Biogen and Ionis (IONS) are already testing something similar in humans. But Voyager's got the edge – theirs is a one-time shot, so no more of those painful spinal taps.

That’s not all. Voyager is also tinkering with these new virus capsules that can sneak gene therapies straight into brain cells. And get this – they're even working on ways to ditch the viruses altogether and target nerves directly. Pretty cutting-edge stuff.

So, is Voyager a surefire win? Heck no.

Let's be realistic. It's going to be a while before Voyager actually makes money from these drugs. But there'll be exciting news along the way—science proving their ideas work.

Remember, the tricky thing with gene therapies is that everyone's chasing the same dream: how to get these treatments where they need to go quickly, cheaply, and safely. It's tough to predict who'll crack the code, even for the experts.

What's noteworthy about Voyager is that they keep reeling in those big pharma partners. Sure, the first two deals fizzled out, but not before Voyager pocketed a ton of cash. That kept them afloat, and now their stock's not such a dumpster fire.

But, let’s face it. Voyager's track record isn't exactly a parade of victories. Progress has been slow, and that's just the way it is in this industry.

If they pull off a miracle cure, they'll be worth billions, maybe tens of billions. Remember when Intellia Therapeutics (INTL) hit that $10 billion mark? That's the kind of payoff we're talkin' about.

Still, Voyager needs to deliver some serious wins, or those partners will vanish again. However, it’s worth considering that when a big player like Novartis, who knows this gene therapy game, partners up... that's gotta mean something, right? Even without results from human trials, it's a sign Voyager might be onto something big.

I know it's hard to justify investing in small biotechs with a losing streak, especially when they're tackling the toughest diseases out there. But after digging into Voyager, I can see its potential.

Worst case scenario? Their drugs flop. But that can happen to any biotech, even those with huge valuations and decades of trying.

As for Voyager, this biotech has been around the block. They've clearly got some promising science, and their stock is cheap. For me, that's enough to take a small position and see what happens.

Mad Hedge Biotech and Healthcare Letter

February 15, 2024

Fiat Lux

Featured Trade:

(TACKLING THE BIG C)

(PFE), (BNTX), (BMY), (ABBV), (AZN)

Super Bowl Sunday: not just a day for football fanatics but a golden opportunity for brands to shine brighter than the halftime show, captivating over 100 million pairs of eyes.

Amid the usual suspects of beers, cars, and fizzy drinks, an unexpected name popped up on the screen: Pfizer (PFE). The Big Pharma titan threw its hat in the ring with a multimillion-dollar message that could be summed up as a toast to science itself.

Here’s how Pfizer’s ad went: animated legends of science — from Newton to Einstein, alongside Rosalind Franklin and Katalin Karikó — belting out an ode to medical milestones to the tune of Queen’s “Don’t Stop Me Now.” Add a dash of whimsy with a cameo from penicillin and a crooning tardigrade, culminating in the heartwarming sight of a young cancer survivor leaving the hospital to applause.

This cinematic piece wasn’t just about selling a product; it was about selling a dream, one where science leads the charge against cancer, underscored by Pfizer’s new rallying cry, "Outdo Yesterday," and a nudge towards LetsOutdoCancer.com.

Shrouded in mystery is the exact price Pfizer paid for this 60-second spectacle — shortened from its original 90-second glory.

But, my sources say that the pharma giant shelled out around $6.5 million to $7 million for half that time, making Pfizer’s splurge no drop in the bucket, especially juxtaposed against a recent $15 million pledge to the American Cancer Society.

This grand gesture comes at an important milestone, marking Pfizer’s 175th year and a concerted push to cast a vibrant, forward-looking shadow across its brand, appealing to the public, investors, and its own ranks alike.

After all, it’s an open secret that Pfizer’s looking to weather a storm, with its COVID-19 vaccine sales dwindling.

Despite riding high on the COVID-19 vaccine wave in partnership with BioNTech (BNTX), raking in roughly $57 billion across 2021 and 2022, Pfizer's financial seas have been anything but calm. The stock’s dramatic descent from its late 2021 peak paints a picture of uncertainty, rooted in the sobering performance of its COVID-19 titans, Comirnaty and Paxlovid.

Yet, as we can see, Pfizer’s narrative isn’t one of gloom. Stripping away the pandemic’s shadow reveals a company in robust health, with a 7% operational growth and a record seven FDA nods in 2023 alone.

Speaking of making it rain, Pfizer's not just throwing its COVID-earned billions around for kicks. For example, they've laid down a cool $43 billion on the table to bring oncology biotech Seagen into the fold.

This acquisition isn't your everyday shopping spree either. It's a move designed to transform Pfizer into the leader of the antibody-drug conjugate (ADC) movement in cancer therapy, potentially beating the likes of Bristol Myers Squibb (BMY), AbbVie (ABBV), and AstraZeneca (AZN).

Think of this move as the biopharma eyeing Seagen's $3 billion in 2023 revenue and saying, "Let's crank this up to $10 billion by 2030." Ambitious? Absolutely. But if anyone's got the blueprint to make it happen, it's Pfizer.

The pivot to cancer isn’t just a strategic shift but a play for the heartstrings of a global audience. With cancer touching lives universally, Pfizer’s Super Bowl gambit seeks to transcend its COVID-19 narrative, aiming for a connection that’s both deeper and more universal. The deliberate omission of its vaccine from the ad speaks volumes, aiming to bridge divides in a viewership as diverse as the Super Bowl’s.

Still, the true measure of its Super Bowl splash — beyond the ad’s immediate sparkle — may lie in subtler indicators, from stock movements to talent retention and a potential surge in interest around its cancer-fighting mission.

Whether this move translates into a long-term win for Big Pharma titan remains to be seen, but for now, the spotlight isn’t just on the Chiefs’ victory but on Pfizer’s leap into the hearts and minds of millions, championed by science and the indomitable spirit of innovation. I suggest you buy the dip.

Mad Hedge Biotech and Healthcare Letter

February 6, 2024

Fiat Lux

Featured Trade:

(SETTING THE TABLE FOR STEADY GAINS)

(ABBV), (ABT), (PFE), (GILD), (DNA), (MRNA), (AMGN), (LLY)

Here's a nugget of wisdom from someone who's sailed the investment waters more times than I've had hot dinners: diversification is your best friend. Think of it as the Swiss Army knife in your investment toolkit.

Now, if there's one treasure you'd want aboard your investment ship, it's a dividend stock. Not just any old stock, though. I'm talking about AbbVie (ABBV).

Since it waved goodbye to its parent company, Abbott Laboratories (ABT), in 2013, it has boosted its dividend payouts by an eye-popping 290%. With a yield hanging around 4% and delivering a 130% total return over the past 5 years, long-term investors undoubtedly struck gold.

Unfortunately, 2023 has turned into the kind of year we'd rather forget. The end of Humira's patent was looming like a dark cloud, threatening to rain on AbbVie's parade by letting generics flood the market. The horror, right?

But, plot twist: the anticipated disaster was more of a light drizzle. Despite the competition, Humira still brought in a cool $11.1 billion. Sure, it's a dip, but not the plunge we feared.

Meanwhile, AbbVie's been on a shopping spree, snapping up Immunogen and Cerevel for a combined total that's a smidgen under $19 billion. It's like they're collecting Infinity Stones, diversifying beyond Humira into areas ripe with potential.

And let's not forget their foray into the realm of Antibody Drug Conjugates (ADCs) — the hot ticket in oncology.

While AbbVie’s not throwing around cash like confetti, like some of their peers including Pfizer (PFE), Gilead Sciences (GILD), Genentech (DNA), they're making notable moves. It's a bit like betting on the dark horse; if their ADCs and CNS ventures hit their stride, we're all in for a treat.

Amidst all this innovation and expansion, AbbVie hasn't lost sight of what gets investors' hearts racing — a solid dividend. It's the kind of steady reliability that's as comforting as your favorite cozy blanket.

As if those aren’t enough, the company just threw us a curveball that's got Wall Street buzzing more than my neighbor's annoying leaf blower on a peaceful Sunday morning.

In its recent earnings report, AbbVie not only beat the revenue expectations for its fiscal fourth quarter but decided to sweeten the deal by raising its long-term sales outlook.

Despite the concerns about Humira, AbbVie still posted fourth-quarter earnings that had their investors nodding in approval, even if they were a tad lower than previous years’ glory days. With revenue hitting $14.3 billion, surpassing the street's guess of $14 billion, it's clear the company isn't just hanging in there; it's throwing punches back.

The immunology portfolio, while taking a 12% hit, isn't down for the count, thanks to Skyrizi and Rinvoq. These two rising stars, which are quickly becoming the Batman and Robin of the biopharmaceutical world, are not just filling Humira's big shoes; they're sprinting.

With the duo’s sales surging by 52% and 63%, respectively, it's no wonder AbbVie is adjusting its binoculars and raising its long-term guidance for these drugs to a whopping more than $27 billion by 2027.

That's a $6 billion jump from their previous forecast. If that doesn't scream confidence, I don't know what does.

And just for a bit of perspective, while AbbVie was basking in the glow of success, its peers had a mixed day at the market. Pfizer took a slight tumble, Moderna (MRNA) and Amgen (AMGN) dipped their toes into the red, while Eli Lilly (LLY) floated up, riding a wave of optimism.

So, as we move forward this 2024, you might be wondering, "What's next for AbbVie?"

Well, if I were a betting man (and let's be honest, investing is betting with extra steps), I'd say we're not likely to see AbbVie pulling a rabbit out of a hat.

But, and it's a big but, we're talking about a company that's as expertly managed as a Michelin-starred kitchen. They've got a knack for serving up share price growth and dividends that leave investors coming back for seconds.

So while AbbVie might not be dangling the next blockbuster breakthrough in front of us, their steady march forward is as promising as finding a shortcut on your morning commute. We might not see the stock skyrocket overnight, but a climb to around $180 per share? That's not just possible; it's on the menu. And right now, with its recent earnings report, it's as good a time as any to pull up a chair to the AbbVie table. Bon appétit.

Mad Hedge Biotech and Healthcare Letter

December 28, 2023

Fiat Lux

Featured Trade:

(CLOSING THE YEAR WITH A BANG)

(XBI), (ABBV), (IMGN), (RHHBY), (PFE), (MRK), (AMGN), (VKTX), (TERN)

The biotechnology sector, pretty much like a phoenix rising from the ashes of its recent lackluster performance, is experiencing a renaissance as 2023 draws to a close. The recent spree of high-stakes deals has set the stage for what could be a significant rebound, a situation that savvy investors should watch closely.

In a remarkable display of strategic maneuvering, AbbVie (ABBV) has been on an acquisition tear.

Earlier in December, they've recently snapped up Cerevel Therapeutics for an eye-popping $8.7 billion, only a week after announcing their intent to acquire ImmunoGen (IMGN) for a formidable $10.1 billion.

And in this high-stakes game, Roche Holding (RHHBY) isn't playing second fiddle, having declared their acquisition of Carmot Therapeutics for $2.7 billion.

This flurry of activity isn't just a few isolated incidents. It's actually a trend. Of the 18 biotech acquisitions exceeding $1 billion announced this year, a significant one-third have emerged since October. This surge is like a shot in the arm for the sector, suggesting a much-anticipated uptick.

But let's take a step back and consider the broader picture.

The SPDR S&P Biotech ETF (XBI) has shown some muscle in November and December. However, it's still trailing behind this year, down by 3%, while the S&P 500 has surged by 19.5%.

Now, focusing on the XBI, a temperature check for the sector: trading around $80, it's a steep drop from its heyday in the $140 range during late 2020 and early 2021. It's down nearly 50% from its peak in February 2021.

This isn't just a dip; it's a nosedive.

Looking at the turn of events, it’s possible that the AbbVie-ImmunoGen deal is perhaps the precursor to a more consistent pattern of mergers and acquisitions in 2024. It seems that we've hit the floor and the only way now is up, with M&A activities poised to inject some much-needed vitality into the sector.

In previous years, the biotech valuations took a hit, and understandably, companies were hesitant to settle for offers that undervalued them compared to their pandemic-era zeniths. But this year, the tide has turned.

Notably, the cumulative value of biopharma deals at a whopping $128 billion this year, shooting up from $61 billion in 2022.

Key transactions fueling this jump include Pfizer's (PFE) massive $43 billion deal for Seagen and Merck’s (MRK) $10.8 billion acquisition of Prometheus Biosciences.

The shift in the regulatory landscape is also worth noting.

Antitrust regulators, who initially seemed poised to block deals like Amgen's (AMGN) $27.8 billion acquisition of Horizon Therapeutics, have shown more flexibility. This change in stance is likely emboldening companies to pursue larger deals.

Now, let's talk about the financial clout.

Large-cap biopharma companies are projected to have about $199 billion in cash by year-end. There's a noticeable dip in dividends and stock buybacks, hinting at a strategic pivot towards mergers and acquisitions. It could indicate that we can expect Pharma to maintain an aggressive stance on the M&A front.

So, what's in store for the XBI and investors alike?

This uptick in M&A activity is like untying the strings of a tightly held purse, releasing cash back into the sector. It's a magnet for both specialist and generalist investor interest, a potential boon for the XBI.

Predicting the next wave of M&A is basically like reading tea leaves. Yet, this year has shown a marked preference for biotechs specializing in obesity, immunology, and cancer.

A notable example is the speculation around Pfizer eyeing a deal with a biotech firm developing an anti-obesity pill.

The ripple effect? Shares of Viking Therapeutics (VKTX) and Terns Pharmaceuticals (TERN), both in the obesity pill race, have seen their stocks jump 47% and 62.5%, respectively, in December.

Evidently, the biotech sector, once in the doldrums, is now witnessing a renaissance. This resurgence is marked by major deals reshaping the industry landscape, holding significant implications for 2024 and beyond.

For investors, this sector represents a fertile ground for growth and opportunity. Staying informed and nimble is key to capitalizing on these dynamic developments. The biotech sector, it seems, is back in the game, and how!