Global Market Comments

May 16, 2025

Fiat Lux

Featured Trade:

(MAY 14 BIWEEKLY STRATEGY WEBINAR Q&A),

(TSLA), (BLK), (SPY), (TLT), (WMT), (LLY), (UNH), (KKR), (NVDA), (ABNB), (GLD)

Global Market Comments

May 16, 2025

Fiat Lux

Featured Trade:

(MAY 14 BIWEEKLY STRATEGY WEBINAR Q&A),

(TSLA), (BLK), (SPY), (TLT), (WMT), (LLY), (UNH), (KKR), (NVDA), (ABNB), (GLD)

Mad Hedge Technology Letter

February 14, 2025

Fiat Lux

Featured Trade:

(AIRBNB DOES JUST ENOUGH)

(ABNB)

Americans still have money to travel, so ignore all those wacky reports that the consumer is about to go missing.

Granted, I wouldn’t say people are flush with cash, but enough to go on holiday and pay for short-term rentals from the likes of good ‘ol company Airbnb (ABNB).

The big takeaway from Airbnb’s earnings report is that the tech rally will continue albeit it in a choppier form than we are generally used to.

But it will keep chugging along, translating into traders and investors buying the big dips when tech stocks go on discount.

That dip buying is what prevents stocks from real weakness, which is something more like a 10% or 20% drop.

Have you noticed that tech stocks hardly go down anymore?

Well, there is money waiting like a parachute to a paratrooper, and this dynamic will underpin the market even though I admit that tech stocks are expensive and losing steam in their internal business models.

Cross-border travel drove a majority of nights booked in the APAC region.

Its North American business, where there were signs of slowing demand last summer, also saw faster growth with a “mid-single digits” gain in nights booked during the holiday season. That’s “driven by broad strength of underlying travel trends within the region,” the company said, while also citing higher pricing of stays and strength in short-term bookings and entire homes.

Booking’s growing 8.5% is nothing to throw a parade over, but the market delivered the stock a 14% return at the time of this writing.

I remember for that type of sumptuous pop, we used to need 30% or more in revenue expansion, and tech just isn’t delivering on that, and it is a sign of the times of Silicon Valley running out of great ideas.

We are still living on Steve Jobs’ ideas for better or worse.

Zuckerberg is still doing the Facebook and Instagram thing, and CEO of Airbnb Brian Cheksy is still doing the short-term rental thing.

His other ideas aren’t stupid, but they won’t move the needle.

Chesky is doubling down on “other products.”

Airbnb will invest $200 million to $250 million into launching and scaling those new products starting in May. His plans are to build on the experiences business for tours, classes, and workshops, and offering add-on amenities during stays such as personal chefs, midweek cleaning, and in-home massages.

Airbnb’s co-host marketplace, which allows homeowners to hire fellow hosts to manage their rentals, is really a nothing-burger.

Getting someone more ruthless to squeeze out higher profits from a rental is not some revolutionary idea, nor will it attract new shareholders.

It is basically hiring a property manager for a short-term rental. It also scales very poorly and is not an efficient use of time.

I am also not sold on the “experiences” business and find it overreaching.

Just the other day, I opened Airbnb’s homepage only to be forced and overruled into an “experience” page of the location I was hoping to search for even though I still hadn’t found a rental unit.

I had to click out of it, wasting my precious time.

Luckily, after I reloaded the page, Airbnb didn’t force-opt me again into their marginal experience page, and I was able to search for my rental.

After all these years, call me arrogant, but I think I know enough to plan my trip and don’t need tech companies to hold my hand or put digital sensors up my butt.

In fact, I will call Airbnb out, their service has been getting incrementally crappier the last few years, but they have a monopoly so they get away with it. Life is unfair, isn’t it?

Tech companies risk alienating many customers, but Airbnb is still a great buy-the-dip company and gives us brilliant insight into the health of the North American consumers.

Buy the dip in tech and ABNB until you shouldn’t.

Mad Hedge Technology Letter

November 8, 2024

Fiat Lux

Featured Trade:

(AIRBNB IS IN THE DOG HOUSE)

(ABNB)

Revenue increased 10% from $3.4 billion a year earlier, and that is where the problem lies for Airbnb (ABNB).

Growth rates of 10% are a problem in technology.

The mantra of scaling out and monetizing is all but expected for growing tech companies.

Something in the ballpark of 30% and higher is something that shareholders would prefer to see.

Just look at the top tech company right now, Nvidia and the breathtaking 126% revenue growth year over year is an example of what I am talking about.

A measly 10% won’t cut it, and it explains the hard sell-off in shares in the travel platform this morning.

It’s true that the company isn’t a cash burner, and the company noted a $2.8 billion tax benefit during the third quarter of 2023, but to really fetch that premium on the stock market, investors will need to see demonstrably higher growth rates and better profitability.

Average daily rates increased 1% from a year ago to $164 in the third quarter, signaling a cooling down of revenue opportunity.

If per-night revenue isn’t growing fast, then Airbnb will need to make that up on the volume.

This is starting to look and feel like a company that won’t be able to scale their product.

Remember that acquiring a listing on Airbnb is an intensive process for the property owner, and the 12% in commission Airbnb requires is probably at the upper limit of what they can ask.

Airbnb said adjusted EBITDA for the third quarter was $2 billion, up 7% year over year.

Gross booking value, used by Airbnb to track host earnings, service fees, cleaning fees, and taxes, totaled $20.1 billion in the third quarter. The company reported 123 million nights and experiences booked, up 8% from a year ago.

Airbnb said it saw hosting growth across all regions and market types during the third quarter. The company said in its shareholder letter that it has more than 8 million active listings and has worked to improve listing quality. Airbnb has removed more than 300,000 listings since last year.

In 2021, the stock was priced at over $200, and fast forward to today, it is languishing at $135 after another 8% selloff.

Even more prevalent, the stock has also been punished as non-AI stocks and AI stocks have bifurcated into two separate paths.

Airbnb has been talking up getting into other businesses like experiences, and I don’t believe that will move the needle in terms of revenue growth.

Property management is another sub-sector they are talking about to expand, but again, I don’t see that as a solution, and that type of work is incredibly labor intensive, which tech companies should stay away from.

At a time when tech companies are looking to automate to look to go on auto-pilot, Airbnb is going the other way and will need more human labor.

Labor costs have been trending higher, and property management will never be an industry where a tech company can just substitute with an algorithm.

Many of times, when tech and real estate intertwine, the Frankenstein company loses its way and doesn’t succeed.

Airbnb will just need to settle for a lower premium than most other tech stocks. I would stay away from this stock for now and head to higher ground to ride the bandwagon of AI.

Mad Hedge Technology Letter

August 9, 2024

Fiat Lux

Featured Trade:

(WARNING SIGNS LITTER THE TECH NARRATIVE)

(ABNB), (BKNG), (EXPE)

It was early.

The real recession doesn’t kick into gear for another quarter or so.

This was just a quick fake-out.

The bond market freaking out and pricing in 1.25% Fed Funds’ cuts was a generous gift to tech stocks.

Why do I say that?

It is a dip in which we can get into tech prices at cheaper prices – probably the last time before the U.S. election.

We are starting to receive confirmation from many earnings reports that the consumer is starting to get cold feet.

The pullback in consumer strength runs the whole gamut from home improvement to restaurant eating.

I cover tech and the weakness is multi-pronged stemming from hardware to software.

The latest to ring the alarm about sluggish consumer spending was the digital accommodation platform Airbnb (ABNB).

Airbnb earned sales of $2.7 billion for the same quarter last year and now they have told investors that for next year they plan to target $2.5 billion of sales.

The culprit blamed by Airbnb management is the American consumer.

Americans are shortening their Airbnb stays and soon they could be sacrificing Airbnb altogether. Although we aren’t at that point yet, US consumers simply can’t stomach this new wave of price increases for the cost of living, and reigning back discretionary travel is this logical item to shave from the budget.

The second quarter continued a trend of decelerating bookings growth for Airbnb. The total value of all bookings through Airbnb grew 11% year over year to $21.2 billion for the three-month period. That's down from 12% booking growth in Q1, 15% growth in the final quarter of 2023, and 17% growth in September-ended third quarter of 2023.

In 2022 and 2023, Airbnb, Booking Holdings (BKNG), and Expedia Group (EXPE) benefited from a bounce-back in travel after the harsh lockdowns prevented many types of travel in 2020 and into 2021. So-called revenge travel powered strong sales growth for the companies. But the picture appears to be shifting.

It is hard to see the US consumer just bouncing back with a V-shaped trajectory and that could affect Airbnb sales.

Reports out of high costs states like Washington and New York peg $150,000 per year in income as “lower middle class.”

There has also been a huge migration shift from wealth moving out of blue states to red states in the hope of maintaining purchasing power through these high inflation times.

The fact of the matter is that $35 trillion in Federal debt is the most important topic for this upcoming U.S. President Election, but this topic has been completely sidelined from the national discourse.

This surely means higher debt down the road and a further deterioration in the US consumer profile.

Tech companies with large moats around their business models will get through these times, but for Airbnb, they don’t have this type of moat because consumers don’t necessarily need to travel. Consumers do need to eat, sleep, and drive a car to work.

They can simply just delay travel for a few years before they reload financially.

It is high time to unload stocks like Airbnb even if they are leaders in the home-sharing sub-sector in tech.

Airbnb shares are down around 32% in the past few months highlighting the need for overly expensive tech stocks to adjust to the new reality.

I do believe there is another leg down in shares before an optimal window to buy on the dip presents itself, but that appears to be around $90-$100 per share.

Global Market Comments

June 14, 2024

Fiat Lux

Featured Trade:

(TESTIMONIAL),

(JUNE 12 BIWEEKLY STRATEGY WEBINAR Q&A),

(NVDA), (AVGO), (ARM), (GM), (TSLA), (SQM), (FMC), (ALB), (AAPL), ($VIX), (AMZN), (MO), (NFLX), (ABNB)

Below please find subscribers’ Q&A for the June 12 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Incline Village, NV.

Q: How will Nvidia (NVDA) trade post-split?

A: Well, it’ll probably keep going up, because I think the year-end target—the old $1400, which is now $140—is still good. And I have a whole bunch of LEAPS, which are post-split $40, $50, $60 in-the-money, and I’m just keeping those. It’s a good cash management tool to have. So, even $500 points in the money, you’re still looking at about 20% returns by the end of the year on a January LEAPS. If you can buy the January 2025 $70-$71 LEAPS for 83 cents that’s a 20.48% profit at expiration in six months. So if you want a safe, very high return, that is the best way to do it in the financial markets, is to go way in the money. LEAPS will still pay you a lot of money amazingly. This trade will disappear someday but it’s there now and I’m taking it. Screw 90-day T-bills—I’m going into $500 in-the-money LEAPs on Nvidia, which pays four times as much.

Q: Is Broadcom Inc (AVGO) the next Nvidia?

A: There is no next Nvidia—the next Nvidia is Nvidia. Buy Nvidia on a 20% decline, which I think we may get sometime this summer. That’s a dip you want to buy for a year-end run to $140. Also, Broadcom isn’t exactly undiscovered at this point. It has doubled since October, while Nvidia is up 4 times. So if the bargain in the market for you is double in six months, I’m not sure you should be in the market. That said, I put out a report on split candidates last week and (AVGO) is very high on the list.

Q: What’s the best way to trade split candidates?

A: I actually just wrote a newsletter about this last week. There are in fact 36 high-priced, good money-earning split candidates, and I listed them all. You can buy really any of those if you’re looking for a high-priced stock that is growing. And management has a huge incentive to do splits because it makes the stock go up faster, and they’re all paid in stock options. So that is another reason you go into these. The best way to trade splits is buying the candidates because the biggest move is on the announcement of the split—you usually get 10%, 15%, or even 20% returns on the announcement.

Q: How do you envision AI in 10 years?

A: Well, it’s unimaginable. I can tell you from experiencing a lot of these big technology changes—it’s always tremendously underestimated by the markets, and you can safely bet on that. It’ll go up a lot more than you realize. That’s what happened when we jumped from six track tapes to cassettes, Betamax to VHS, teletypes to faxes, and faxes to emails. I thought Steve Jobs was crazy when he introduced the iPhone. Nobody makes money in handsets. But he proved me wrong. That makes my $240,000 DOW by 2030 projection completely reasonable.

Q: What will inflation do for the rest of the year, and how will it affect stocks?

A: Inflation will go flat to down for the rest of the year. And that is being driven by artificial intelligence—the greatest deflationary product ever created in the history of the economy. It’s unbelievable the rate at which AI is replacing real people in jobs. If you want a good example of that, I had to call Verizon yesterday to buy an international plan, and I never even talked to a human. They listed out three international plans in a calm, even male voice, and I picked one. Or go to McDonald's where $500 machines are replacing $40,000 a year workers. This is going on everywhere at the same time at the fastest speed I have ever seen any new technology adopted. So buy stocks, that’s all I can say.

Q: What’s your opinion on Arm Holdings (ARM)?

A: I love it. There are very few serious companies in the chip area, and this is one of them.

Q: Do you expect gold mining stocks to continue upward?

A: Yes, but the better play here is the metal. Gold and silver aren't being held back by inflation while the miners are. Plus, the main buyers in the market now are the Chinese, and they don’t buy gold miners—they buy gold, silver, copper, platinum, and uranium outright.

Q: What about Tesla (TSLA) long-term? Kathy Woods's target is $2000 long-term.

A: I think Kathy Woods is right. But we have to get through the nuclear winter in the EV space first, where suddenly the market got saturated. I think Tesla is the only one who could come out of this alive by cutting costs and advancing technology, as they have always done. When I bought my first Tesla Model S1 in 2010, the battery cost $32,000. Now it’s $6,000, and you get a lot more range. Did (GM) offer an equivalent cost improvement with internal combustion engines? So, yes, never bet against Elon Musk—that’s a good 25-year lesson on my part, and should be for you too.

Q: Can you elaborate on the lithium trades?

A: I listed three names in my letter last week, (SQM), (FMC), (ALB), and the only thing you know for sure is that they’re cheap now. They could stay cheap for another six or 12 months. But when you get a turnaround in the global EV market and the manufacturers start screaming for more lithium, and all of the lithium stocks will double, or triple and they’ll do it fairly quickly. You can’t beat a market bottom for getting involved. Just look at my above (NVDA) trade. Not only would they be good stocks buy, but it would be a good LEAPS buy down here because then you could get 4 or 5 times your money on a small move.

Q: Can you suggest Amazon (AMZN) LEAPS?

A: January 2025 $195-200 just out of the money, should give you a return of about 120% over the next 6 months. That gets you the annual yearend run-up. And that’s my conservative position. My aggressive ones are all in Nvidia.

Q: Do you think zero-day options have permanently forced the Volatility Index ($VIX) to the $12 handle?

A: Yes, I do; it’s killed that market. Something like 40% of all the option traders on the CBOE were trading the ($VIX) from the short side. Shorting the ($VIX) now would be madness. That has to bring tough times for that whole industry. Trading call spreads at a $12 volatility, you’re better off buying the LEAPS because the LEAPS give you much bigger returns with much less risk. And a $12 ($VIX) means you’re getting your LEAPS at half the historic price. I’m just waiting for a new market low to start pumping out the LEAPS recommendations. All the more reason to sign up for the Mad Hedge Concierge Service to get an early read into the LEAPS recommendations. For more information on that, contact support at support@madhedgefundtrader.com

Q: What will happen to Apple (AAPL) after the 11% surge?

A: It goes to $250 by the end of the year. Now that it has the kiss of AI on it, people will pour into it.

Q: Why is value lagging?

A: Because AI is entirely a growth story, and you look at all the domestic value stocks, they’re going absolutely nowhere. Value has been in the dog house for years and I’m in no hurry to get in there.

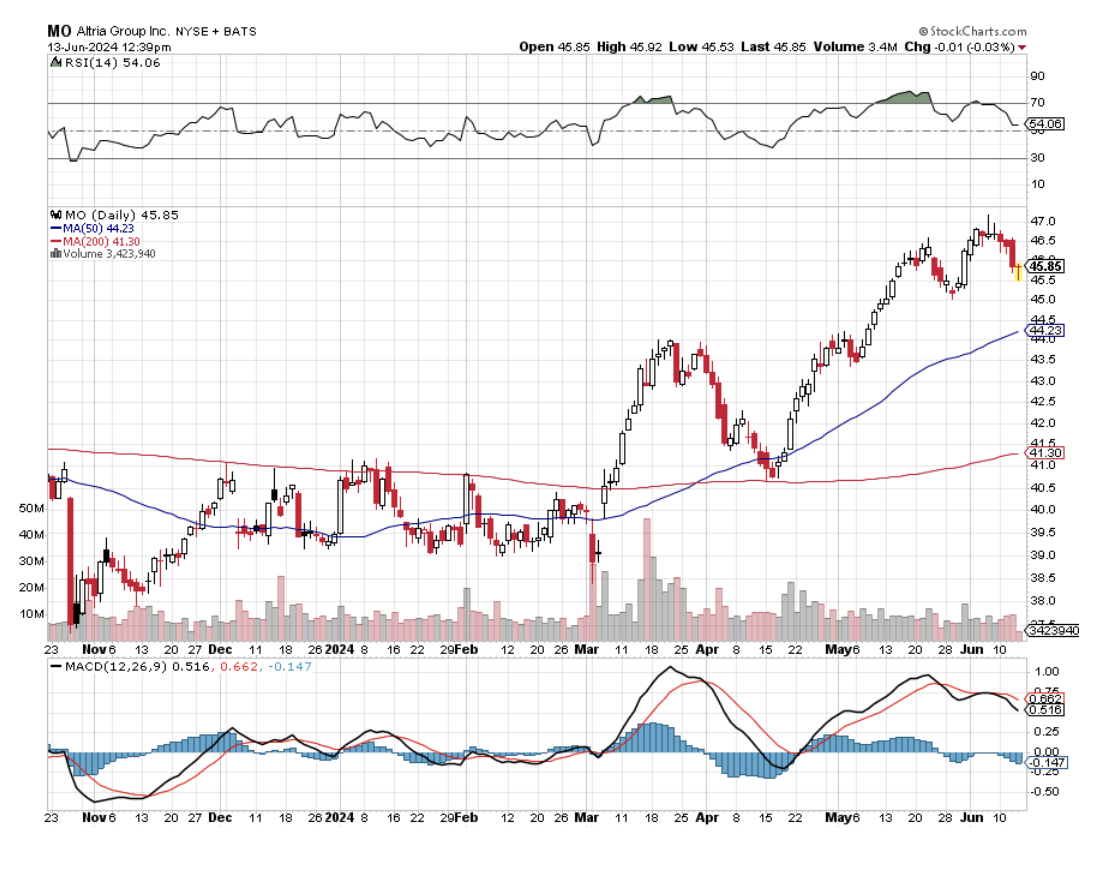

Q: What is the best dividend stock I can invest in right now?

A: That’s an easy one. Altria (MO) has a 9% dividend—you can’t beat that. But you have to hold your nose when you buy this stock because they are in the cigarette business. However, their big growth now is in Asia ex-Japan where the government has a monopoly on tobacco, particularly China. Note that this is not an undiscovered idea; lots of people like a 9% dividend stock and (MO) has already gone up 20% this year, but I think there is still some money to be made here.

Q: How can we subscribe to get early LEAPS recommendations?

A: That would be the Concierge Service. Contact Filomena at customer support, and they will get you taken care of right away.

Q: What about the small nuclear plays?

A: I actually happen to know quite a lot about nuclear plant design, having worked for the Atomic Energy Commission in my youth, and the new designs address every major issue that held back nuclear power with the old 1950s designs. For example, building them underground and eliminated the need for these giant billion-dollar four-foot-thick reinforced concrete containment structures that dot the horizon. Not using pure Uranium alloys that can’t go supercritical is another great idea. So I like them. Are they good stock plays? Not right now. It takes a long time to introduce a new energy technology. Bill Gates is financing a new plant built by Terrapower in Wyoming, and it looks like a fantastic plant, but only Bill Gates could invest at this stage and expect to make money on it. He has very long-term money and you don’t. I would wait until you get a working model plant in the United States before going into these things, but potentially you’re looking at a 10 to 100 times return on your money if it works.

Q: Should I invest in Airbnb (ABNB) because of increased international travel?

A: Yes, we like Airbnb. Especially since they will get a push with the Paris Olympics next month. Not only does that get people to Paris, but it gets people to all of Europe because they usually add on additional trips to a visit to the Olympics.

Q: What would you do in Netflix (NFLX), and what strikes would you use?

A: I would do a LEAPS. Wait for a correction, at least 10%, preferably 20%, and then I would go at the money one year out and that would get you about 100% return. So, that’s the way to do that. This is not LEAPS territory right here —all-time highs are not LEAPS territory. You want to put on LEAPS when everyone else is throwing up on their shoes; the last time they did that was October 26.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, select your subscription (GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or Jacquie's Post), then click on WEBINARS, and all the webinars from the last 12 years are there in all their glory

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

You Only Need One Big Hit to Make a Great Year

Global Market Comments

May 17, 2024

Fiat Lux

Featured Trade:

(MAY 15 BIWEEKLY STRATEGY WEBINAR Q&A),

(GME), (CCI), (ABNB), (TLT), (TSLA), (LMT),

(RTX), (USO), (GLD), (GOLD), (WPM)