Mad Hedge Technology Letter

June 24, 2022

Fiat Lux

Featured Trade:

(GETTING REAL WITH HOME-SHARING TECH)

(ABNB)

Mad Hedge Technology Letter

June 24, 2022

Fiat Lux

Featured Trade:

(GETTING REAL WITH HOME-SHARING TECH)

(ABNB)

Airbnb’s (ABNB) stock has about halved from $206 at the tech market peak of 2021 to around $100 today.

The strength in the first half of 2021 resulted from the optimism coalescing in travel circles about the reverse of shelter-at-home lifestyle to unfettered international travel.

Remember back then, increasingly more countries were allowing Americans into their land with proof of 2 Pfizer shots.

The $130 to $206 rise was simple an overshoot.

Sentiment was at a generational low during 2020 and the upside was merely a result of the extreme reverse of great pessimism to ultra-optimism.

At a micro level, Airbnb’s business model mirrored the same sentiment of the 2020 tsunami of travel cancellations.

Bad optics has been a staple for CEO Brian Chesky.

Then the onslaught of arbitrary refunds to customers alienated the Airbnb host.

They slowly changed their policy to remove “extenuating circumstances” as a reason to get a full refund.

It wasn’t that I had a problem with Airbnb going to $206.

Like many tech growth stocks, they tend to go parabolic during good times.

Tech firms with better balance sheets haven’t halved in value like Airbnb.

That being said, Airbnb is not worth the current $60 billion and a 74 P/E ratio is too expensive at a fundamental level.

After halving, I still think the valuation is a tad bit too generous.

I believe the company is worth $60 billion only if interest rates are close to zero and not the 3.1% we have today on the 10-year US treasury.

The company is worth significantly less in its current form in 2022 and as rates accelerate from 3.1% to 3.5 or 4%, I expect the company to be worth $45 billion.

On the demand side, travel is a lot more expensive now than ever.

I am not only talking about airfare, but also airport car transfers, price for baggage, entertainment, food, and accommodation which are all trending above 40%-80% depending on the item in tourist areas.

However, Americans are making summer of 2022 the “revenge” trip of a lifetime.

The pre-pandemic overtones of fear of missing out (FOMO) and you only live once (YOLO) are back stronger than ever on short-form video platforms like TikTok and Instagram.

One might believe Airbnb stock should be cruising on auto pilot, right?

Well, the revenge travel of summer 2022 is already baked into the price of the stock since this behavior was largely understood 6-8 months before.

The drop in shares has to do more with the lack of incremental demand that will follow the summer of 2022 as the US barrels towards a recession.

Yes, travel will decelerate fast after summer 2022 as Americans blow their load while failing to reload for the 2nd half of 2022.

This is awful news for Airbnb stock.

Another element is gas prices.

The cost of gas and groceries is about to explode as Americans need to fill up their tank and buy groceries for Independence Day celebrations all in unison.

The pitiful energy infrastructure that has been gutted by the current administration won’t be able to handle the elevated demand.

This will 100% limit the budget of Airbnb for Americans.

Airbnb posted an average daily rate (ADR) of $168.46 in Q1, up 5.3% YoY.

However, its growth has decelerated from previous quarters and I expect it to fall even more later this year.

Until we capitulate, the downtrend likely won’t reverse because the business model isn’t that bad and they do boast a monopoly.

Mad Hedge Technology Letter

February 16, 2022

Fiat Lux

Featured Trade:

(AIRBNB SURGES AHEAD)

(ABNB)

Better book your summer vacation this year right now as home-sharing rental platform Airbnb (ABNB) revealed growth surpassing pre-pandemic performance and global travel is back with vengeance.

It’s highly likely that travel restrictions continue to fall by the wayside, opening up what could become the most furious travel season in the history of the human race.

This has spurred consumers to book their summer vacation rental many months in advance and it appears that no amount of supply will satisfy the summer travel season of 2022.

People have been dreaming about international travel for the past 2 years.

Airbnb has capitalized from their position as the nimble option, along with not having to provide the hardware to the final product.

They are just an internet platform that owns no houses.

Hotel companies like Marriott and Hilton have had empty hotels sitting idly while consumers choose to stay in a more rural setting for the past 2 years, within driving distances of big cities.

Another positive trend is Airbnb users choosing more expensive accommodations, which I understand with business travel reformatting itself to go straight into an Airbnb-based house or apartment.

The highest cost also relates to bigger unit sizes as home offices need to be absorbed into living situations.

Hotels have the handicap of needing to renovate their existing stock of rooms since the hotel layout is simply not as attractive as it once was.

Airbnb has a massive advantage here that will lead to margin expansion.

Customers need fast Wi-Fi, a kitchen to at least make their morning coffee, and more amenities that a personal home might offer such as a washing machine.

Even if there is another pandemic on the horizon, the work from home narrative will fortify itself for good with no back-to-office plans in sight.

Airbnb would benefit as Airbnb-hosted units are the best choice for remote workers.

I have noticed that Airbnb hosts have really improved the internet connection at their houses to adjust for the change in connectivity demand.

Airbnb has reimagined itself since the beginning of the pandemic when the company cut thousands of jobs and considered delaying its initial public offering as travel crumbled to a halt around the world.

After the initial pain, business boomed as workers no longer had to be in traditional offices five days a week and could work from anywhere.

Almost half of the number of nights booked in the fourth quarter were for stays of a week or longer and one in five were for stays of a month or more.

This validates my thesis of Airbnb being a sticky product, because they have essentially bolstered their product to perform better during a health crisis relative to competition.

Longer and more expensive stays also mean higher commissions for Airbnb.

Taking a small sample of January 2022, bookings were 25% higher than in 2019, which bodes well for the rest of 2022 as everyone I know is itching to not only travel but to spend more and to make visits to far-flung places.

Pointing to margins as another signal of success – Airbnb has increased them from minus 5% back in 2019 to 27% in 2021.

The company has explicitly said that the growth of incremental supply won’t come from institutional investors, but individual retail units that realize inflation is so bad that they need the extra $10,000 per year to supplement their life standard.

With all the positivity, it is no surprise that Airbnb’s stock has responded to this improving sentiment and shares are up 25% in the last three weeks.

I would wait for a pullback to put new capital to work in this company, but Airbnb is poised to roar ahead in 2022 if international travel opens up and mask mandates are dropped, which appear inevitable.

Global Market Comments

February 4, 2022

Fiat Lux

Featured Trades:

(FEBRUARY 2 BIWEEKLY STRATEGY WEBINAR Q&A),

(PYPL), (PLTR), (BRKB), (MS), (GOOGL), (ROM), (MSFT), (ABNB), (VXX), (X), (FCX), (BHP), (USO), (TSLA), (EDIT), (CRSP)

Below please find subscribers’ Q&A for the February 2 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Incline Village, Nevada.

Q: Thoughts on Palantir Technologies Inc. (PLTR)?

A: Well, we got out of this last summer at $28 because the CEO said he didn’t care what the share price does, and when you say that, the market tends to trash your stock. But Palantir is also in a whole sector of small, non-money-making, expensive stocks that have just been absolutely slaughtered. And of course, PayPal (PYPL) takes the prize for that today, down 25% and 60% from the top. So, we’re giving up on that whole sector until proven otherwise. Until then, these things will just keep getting cheaper.

Q: Given the weakness in January, do you think we still have to wait until the second half of the year for a viable bottom?

A: Definitely, maybe. If things are going to happen, they are going to happen fast; we got the January selloff, but that’s nowhere near a major selloff of 20%. And the fact is, the economy is still great so that’s why this is a correction, not a bear market. At some point, you want to buy into this, but definitely not yet; I think we take another run at the lows again sometime this month. We just have to let all the shorts come out and take their profits so they can reestablish again.

Q: Why are bank stocks struggling?

A: A lot of the interest rate rises that we’re getting now were already discounted last year—banks had a great year last year—so they were front running that move, which is finally happening. To get more moves out of banks, you’re going to have to get more interest rate rises, which we will get eventually. We still like the banks long term, we still like financials of every description, but they are taking a break, especially on the “sell everything” index days. A lot of the recent selling was index selling—banks have a heavy weighting in the index, about 15%. So, they will go down, but they will also be the ones that come back the fastest. We’re seeing that in some of the financials already, like Berkshire Hathaway (BRKB) and Morgan Stanley (MS) which are both close to all-time highs now.

Q: What about the situation with Russia and Ukraine?

A: It’s all for show. This is a situation where both the US and Russia need a war, or threat of a war, because the leaders of both countries have flagging popularity. Wars solve those problems—that’s why we have so many of them by the United States. We’ve been at war essentially for most of the last 40 years, ever since Ronald Reagan came in.

Q: I didn’t exit my big tech positions before the crash, should I just hang onto them at this point?

A: The big ones—yes. The Apples (AAPL), the Googles (GOOGL), the Amazons (AMZN) —they’re only going to drop about 20% at the most, maybe 25%, and then they’ll go to new highs, probably before the end of the year. If you’re good enough to get out and get back in again on a 20% move, go for it. But most people can’t do that unless they’re glued to their screens all day long. So, if you have stock, keep the stock; if you have options, get out of the options, because there the time decay will wipe you out before a turnaround can happen. This is not an options environment, unless you’re playing on the short side in the front month, which is what we’re doing.

Q: When you send out the trade alerts, I have a hard time getting them executed. How do you advise?

A: Move the strike price, go out in maturity, and you can get our prices at slightly higher risk. Or, just leave it and, quite often, people’s limit orders get done at the end of the day when the algorithms have to dump their positions at the close because they’re not allowed to carry overnight positions. Also, even if you get half of my trade alerts, you’re doing pretty good—we’re running at a 23% rate in 6 weeks, or 200% annualized. And remember, when I send out a trade alert, you’re not the only one trying to get in there, so you can even go onto a similar security. If I recommend Alphabet (GOOGL), consider going over to Microsoft (MSFT), because they all tend to move together as a group.

Q: I am sitting on a 16% profit in the ProShares Ultra Technology (ROM), which you recommended. Should I take the money and run, and get back in at a lower price?

A: Yes, this is just a short covering rally in a longer-term correction, and you make the money on the volume. You win games by hitting lots of signals, not hanging on to a few home runs where people usually strike out.

Q: You said inflation will be short lived, so why would there be 9 interest rates after the initial 4?

A: It’s going to take us 8 interest rates just to get us back to the long-term average interest rate. Remember the last 2% is totally artificial and only happened because there was a financial crisis 13 years ago. So, to normalize rates you really need to get overnight rates back up to about 3.0%. And that means 12 interest rate hikes. If you don’t do that, you risk inflation going from controllable to uncontrollable, and that is the death of the Fed. So, that’s why I expect a lot more interest rate rises.

Q: Will the tension between Russia and the Ukraine affect the market?

A: No, it hasn’t so far and I don’t expect it to. Although, it’s hard to imagine going through all of this and not seeing a shot fired. When that one shot gets fired, then maybe you get a down-500-point day, which it then makes back the next day.

Q: Anything to do with Alphabet (GOOGL) announcing its 20 to one split?

A: No, it’s too late. We had a trade alert out on a Google 20 call spread which we actually took profits on this morning. So, nice win for the Mad Hedge Technology Letter there. There’s nothing to do with these splits, it’s not like they’re going to un-announce it, this isn’t a risk-arbitrage situation where there’s always an antitrust risk hovering over the deal that may crash it. This is pretty much a done deal and doesn’t even happen until July 1. People think bringing the share price from $3,000 down to $150 makes it available for a lot more potential retail buyers, which it does. It also makes call spreads on the options a lot cheaper too. When we put out these alerts, we can only do one or two contracts, even tying up $10,000—divide that by 20 and all of a sudden your cheapest Google call spread cost $500 instead of $10,000.

Q: Can you speak about the liquidity on your strikes? Sometimes we’re trading against strikes that have no open interest.

A: Whenever you put in an order for one strike, even if there’s nothing outstanding on that strike, algorithms will arbitrage against that strike—where your order is—against all the other strikes on the whole options chain. So, don’t worry if you have limited open interest or no open interest on our trade alerts. They will get done, and it may get done by some algorithm or some market maker taking more of another strike, that’s how these things get done. It’s all thanks to the magic of computers.

Q: Do you have thoughts about Freeport-McMoRan (FCX)? I have some profitable LEAP positions open.

A: It’ll go higher, keep them. And I like the whole commodity space, which means iron ore (BHP), copper, steel (X), etc.

Q: Would you trade Barclays iPath Series B S&P 500 VIX Short-Term Futures ETN (VXX) at this point?

A: No, because we’re dead in the middle of the recent range. That’s a horrible place to enter—you only enter (VXX) on extremes on the upsides and the downside.

Q: What should I do about Airbnb (ABNB) at this price? They’ve been profitable for 2-3 years, with revenues rising.

A: I think Airbnb is one of the best run companies in the world, and I expect their earnings to keep growing like crazy, especially once we get out of the pandemic. I am also a very frequent Airbnb user, having stayed in Airbnb’s in at least 10 countries, so I’m a big fan of them. The stock just got dragged down by the small tech bust but it will come back. This is a “throwing the baby out with the bathwater” situation.

Q: Are there any good LEAPS candidates now?

A: I’m not doing any LEAPS until we reach the final cataclysmic selloff of the correction. Otherwise, the time value will run against you enormously; I’d rather wait for better prices.

Q: Do you see a cataclysmic selloff?

A: Yes, I do. Maybe in a few more weeks, and maybe next week if we get a really hot 8%+ inflation rate—that would really kill the market.

Q: What will tell you if inflation is ending or slowing labor?

A: Labor is 70% of the inflation calculation. So, when these huge pay awards slow down, that's when inflation slows down. By the way, a lot of pay increases that are happening now are catch-up from the last 40 years of no pay increases for American workers in real inflation adjusted terms. So, a lot of this is catch-up—once that’s done, you can forget about inflation. Also, the long-term pressure of technology on prices is downwards, so allow that to reignite deflation, and that will be your bigger issue over the long term.

Q: What should I do about Editas Medicine Inc (EDIT) or CRSPR Therapeutics AG (CRSP)?

A: Don’t touch the sector, it’s out of favor. Let this thing die a slow death. When they come up with profitable products, that’s when the sector recovers. So far, everything they have works in labs but there are no mass-produced Crispr products, they’re trying for mass production on sickle cell anemia and a couple of other things, but still very early days in CRSPR technology.

Q: When will this recording be posted?

A: In two hours, it will be posted on the website. Go to “My Account” and you’ll find the last 13 years of recorded webinars.

Q: What do you mean by “stand aside from Foreign Exchange”?

A: The volatility in the foreign exchange market is just so low compared to equities and bonds, it’s not worth trading right now. When you can trade everything in the world—foreign exchange is at the bottom of the list. If I see a good entry point, I’ll do a trade; but do I trade Tesla (TSLA) with a volatility of 100%, or foreign exchange with a volatility of 5%? Those are the choices.

Q: Should I do any short plays in oil (USO)?

A: Generally, you don’t want to short any commodity unless you're a professional; I say that having been short beef futures when Mad Cow Disease hit in 2003 and you had three limit-up days in a row in the futures market. That happens in the commodity areas—liquidity is so poor compared to stocks and bonds that if you get caught in one of these one-way moves, you can’t get out. So that is the risk; and I’ve known people who have gone bust trading oil both long and short, so this is for professionals only. With stocks you get vastly more data and information than you do in the commodity markets where industry insiders have a much bigger advantage.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy!

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

The Aga Sophia Mosque in Istanbul

Mad Hedge Technology Letter

December 13, 2021

Fiat Lux

Featured Trade:

(THE POTENTIAL NORMALIZATION OF 2022)

(ABNB), (BKNG), (ZM)

The last 2 years haven’t been a walk in the park for tech traders.

Before March 2020, the bull market and the trading patterns that followed were largely predictable.

Sure, there were our run-of-the-mill selloffs, but nothing like the Covid selloff of 2020.

Then the ensuing reversal that took us to new highs was a sugar high Fed-induced bounce that we are still buoying from, and that boost is largely wearing off.

As we near the end of 2021, it’s hard to believe that it’s been almost 2 years since the daily trading headline became a health care-driven headline.

There is the growing consensus that in the latter part of 2022, a synchronized global recovery story will emerge as the strongest plausible scenario.

This means that day-to-day business conditions which include international travel could revert back to what we had prior to March 2020 or a competing version of it.

I won’t get into the vaccine semantics of it, but a moderate health solution is only positive for tech stocks.

The “shelter at home” tech trade of 2020 was a one-off drawn-out event, and with normalization around the corner, we will return to the catalysts that originally drove tech shares — earnings growth, revenue growth, and financial engineering.

The lingering effects of this latest variant could start to wind down by early spring which will give way to the world of higher interest rates and costlier financing, but higher interest rates solving the inflation crisis.

Naturally, many things could side-swipe this scenario like another covid variant deadlier than the ones spreading around now.

If there is some iteration of normalization involved next year, a tech stock that will squarely harvest the gains from its strategic position at the intersection of the internet and remote working is accommodation sharing platform Airbnb (ABNB).

Airbnb will blast off from the biggest developing trend in the global economy today: workplace flexibility.

Like with Zoom (ZM) video conferencing tech making it possible to work from home. Airbnb makes it possible to physically work from any home, anywhere, and anytime.

While it’s not fair to draw a direct correlation from workplace flexibility to increasing Airbnb profits, it is clear that the company is poised to grow alongside the Web 3.0 revolution which will focus on decentralization, openness, and greater user utility.

As this new iteration of the internet takes hold and continues to spread, Airbnb's unique business structure will result in revenue produced from the sheer number of workers doing staycation remote working adventures.

This is a real thing.

Workers now go somewhere for a month then change their location to take in a different environment.

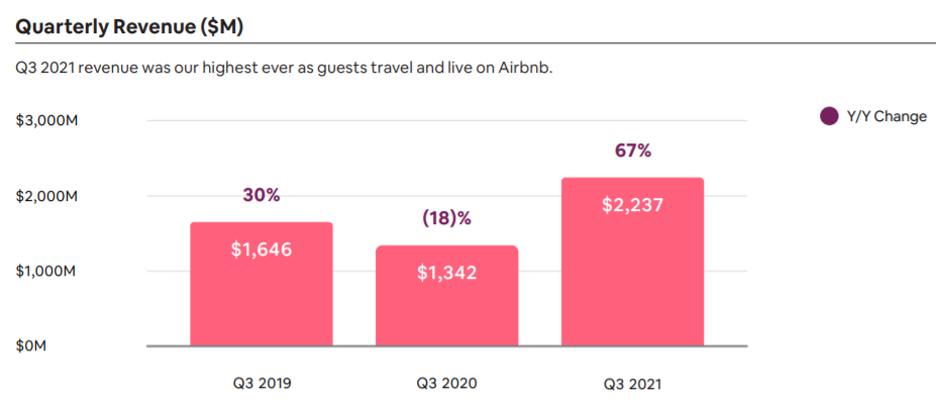

Riding this ongoing revolution and the steady reopening of global travel, Airbnb posted record revenue of $2.2 billion during its third quarter, which was 36% above Q3 2019.

If you want to look at the red-headed stepchild of the accommodation sharing platform services, then take a look at Booking.com (BKNG).

It’s not nearly as useful a platform as Airbnb and their exorbitant commission becomes quite prohibitive to hosts and users.

No wonder they do not grow their host volume like Airbnb.

Airbnb’s products also sell itself with the name of the company becoming a verb, while Booking.com is still reliant on spam-like internet searches using Google search to ramp up engagements.

This turns into an expensive marketing spend while Airbnb spends minimal to attract the next incremental customer.

ABNB shares have experienced a recent 20% pullback on the omicron threat, and I believe it’s a good time to start dollar cost averaging here into ABNB shares in the case that a bigger travel load 6 months from now follows through.

The upside to ABNB shares could be quite large if the business world somewhat normalizes next year because this scenario isn’t priced into ABNB shares yet.

Mad Hedge Technology Letter

November 15, 2021

Fiat Lux

Featured Trade:

(THE GEM OF TRAVEL TECH ACCELERATES)

(ABNB)

Airlines are bracing for a tsunami of travelers for the upcoming Christmas season and it’s no surprise — people are itching to get out of their homes for good reason.

What the news reports don’t tell you is that many of these travelers are on their way to an Airbnb (ABNB), where they will not only stay a weekend to sample the local zeitgeist, but will make their Airbnb a work-from-home office for 4 weeks or perhaps more.

The side effects from the pandemic have indicated to companies that technologies like Zoom and DocuSign make it possible to work from home.

Airbnb makes it possible to work from any home.

And this newfound flexibility is triggering a revolution in how we travel because for the first time ever, millions of people can now travel anytime, anywhere for any length, and even live anywhere on Airbnb.

I firmly believe that this trend toward more flexibility will only accelerate.

The pandemic has suddenly untethered tens of millions of people from the need to go into an office.

In recent months, some of the world's largest companies —Procter & Gamble, Amazon, Ford, PricewaterhouseCoopers — have announced increased flexibility for employees to work remotely.

This is just the beginning as I fully expect more companies to follow their lead.

I am witnessing several trends as a result of this travel revolution.

Can you believe now that Mondays and Tuesdays are currently Airbnb’s highest growing days of the week to travel?

This is a paradigm shift in the way we think about movement and cross-border living.

Second, now people are traveling everywhere, literally everywhere. During the pandemic, over 100,000 cities have had at least one booking on Airbnb. And that includes 6,000 towns and cities that received their first booking ever on Airbnb. The third trend is people aren't just traveling on Airbnb, they're now living full time on Airbnb.

Long-term stays on Airbnb, classified as a stay up to 28 days or more, remain Airbnb’s fastest-growing category by trip length.

People are traveling with Airbnb for extended vacations, relocation, temporary housing, student housing, and many other reasons.

I’ve illustrated how there has been a massive boost in inherent demand for Airbnb units with the merging of travel and work, but the thing that gets me excited is the supply side of the equation.

Now finally, more people than ever are interested in hosting.

Airbnb ended Q3 with the most active listings ever.

Demand is driving more supply. In fact, Airbnb’s highest supply growth is in their highest-demand destinations, particularly in North America and Europe.

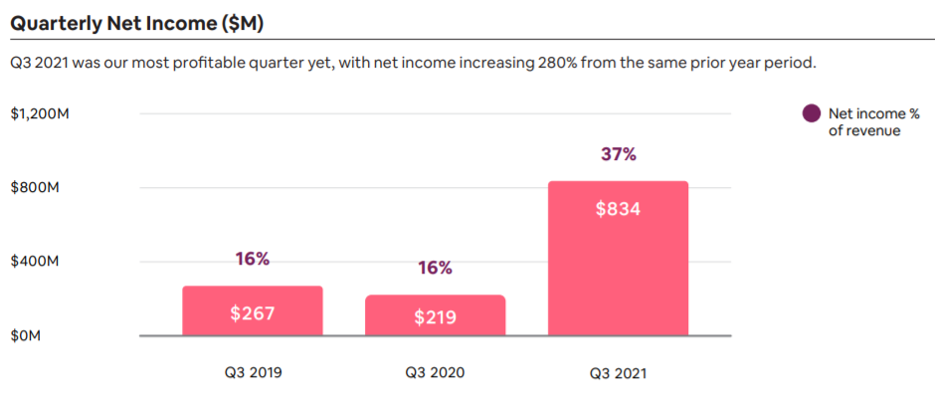

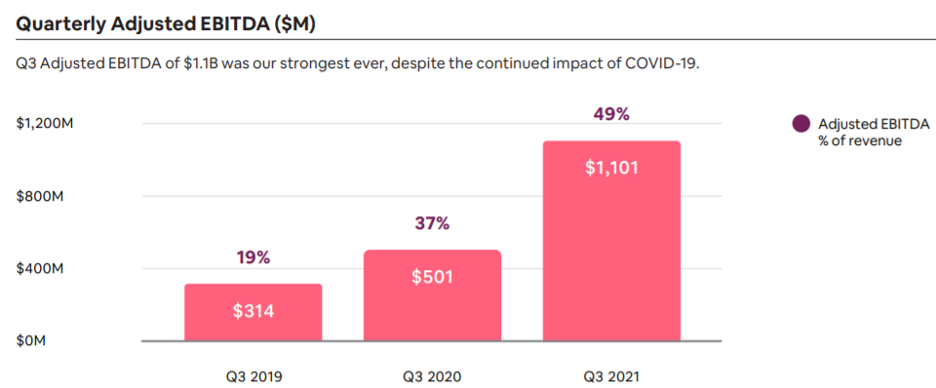

The travel rebound that began earlier this year accelerated in the third quarter resulting in Airbnb's best quarter yet recording revenue of $2.2 billion surpassing 2019 by 36%.

Net income of $834 million was the highest ever, nearly four times larger than a year ago.

Gross booking value of $11.9 billion slingshots above 2019's levels by 23%

Airbnb now has 4 million hosts, and 90% of hosts are individual meaning they specifically latched onto Airbnb’s platform to become a first-time host.

These units are only listed on Airbnb translating into Airbnb possessing the best quality of rental units and in high volume.

No other platform can lay claim to the depth of Airbnb’s business and companies like Tripadvisor.com, Expedia.com are miles behind the curve and still over-reliant on Google’s search engine to manufacture leads that translate into costly customer acquisition fees.

Airbnb now has a simple 10-step process to become a host where they’ve radically reduced the number of steps.

They’ve made it easier to host and the conversion rate for people starting to lease their space flow is up.

On no night, are Airbnb supply-constrained globally.

Before the pandemic, most people were narrowly stuck in their search parameters.

However, now, over 500 million searches have used flexible searches. More than 40% of searches, guests are flexible on where or when they're traveling, and as Airbnb management has become brilliant at predicting the onslaught of demand before it comes to fruition, they have also been stellar at adding the corresponding supply at the right moment in a preemptive fashion.

Airbnb has really moved the profitability needle and future quarters will see a hockey stick-shaped effect on revenue and EPS.

Any pullback should be bought and, to be honest, Airbnb really has hit the sweet spot as the world’s digital housing agent.

I am highly bullish on Airbnb for the year 2022 and beyond.