Mad Hedge Biotech and Healthcare Letter

October 23, 2025

Fiat Lux

Featured Trade:

(SUGAR-COATING NOTHING)

(ABT)

Mad Hedge Biotech and Healthcare Letter

October 23, 2025

Fiat Lux

Featured Trade:

(SUGAR-COATING NOTHING)

(ABT)

Mad Hedge Biotech and Healthcare Letter

March 18, 2025

Fiat Lux

Featured Trade:

(WHEN THE MARKET GIVES BACK WHAT IT ONCE TOOK AWAY)

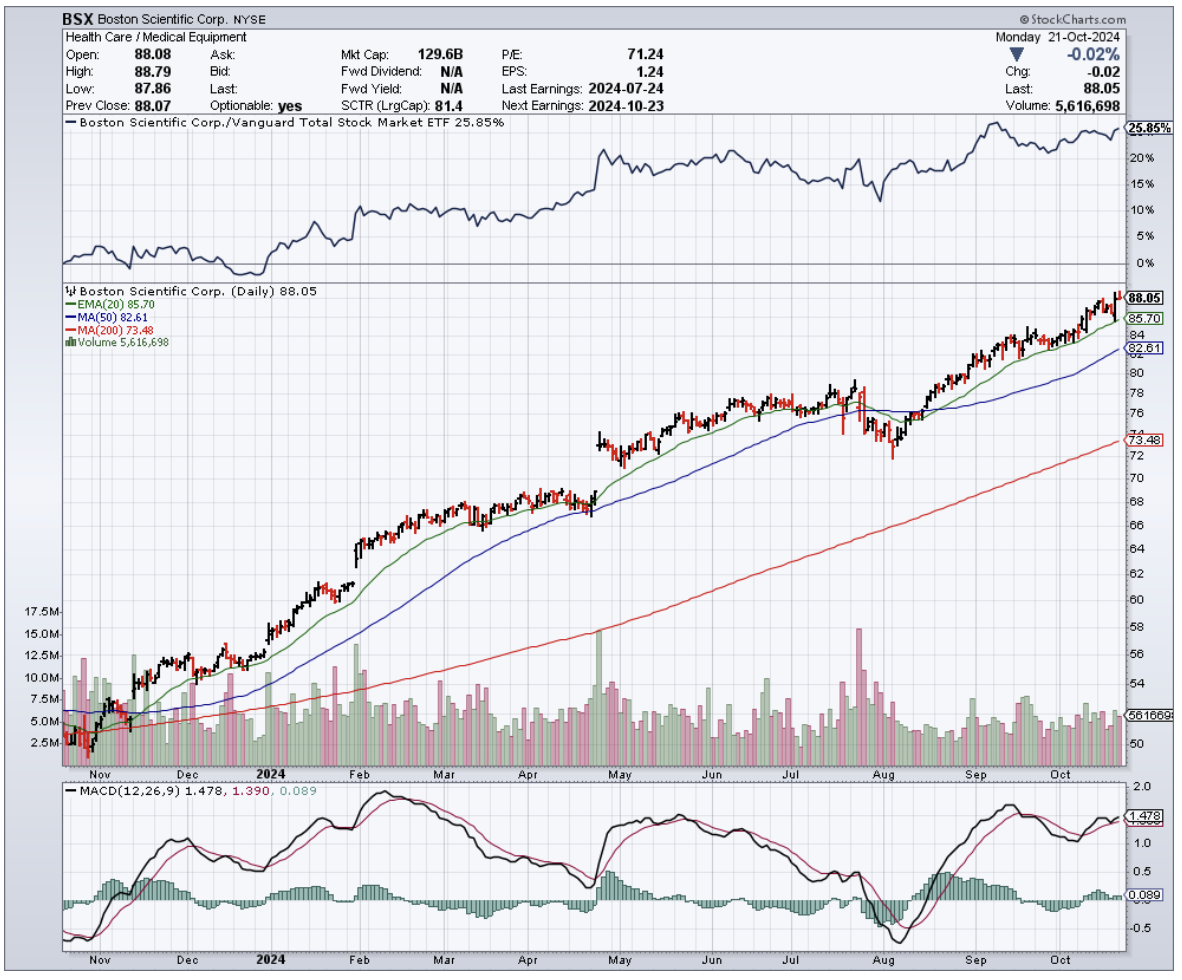

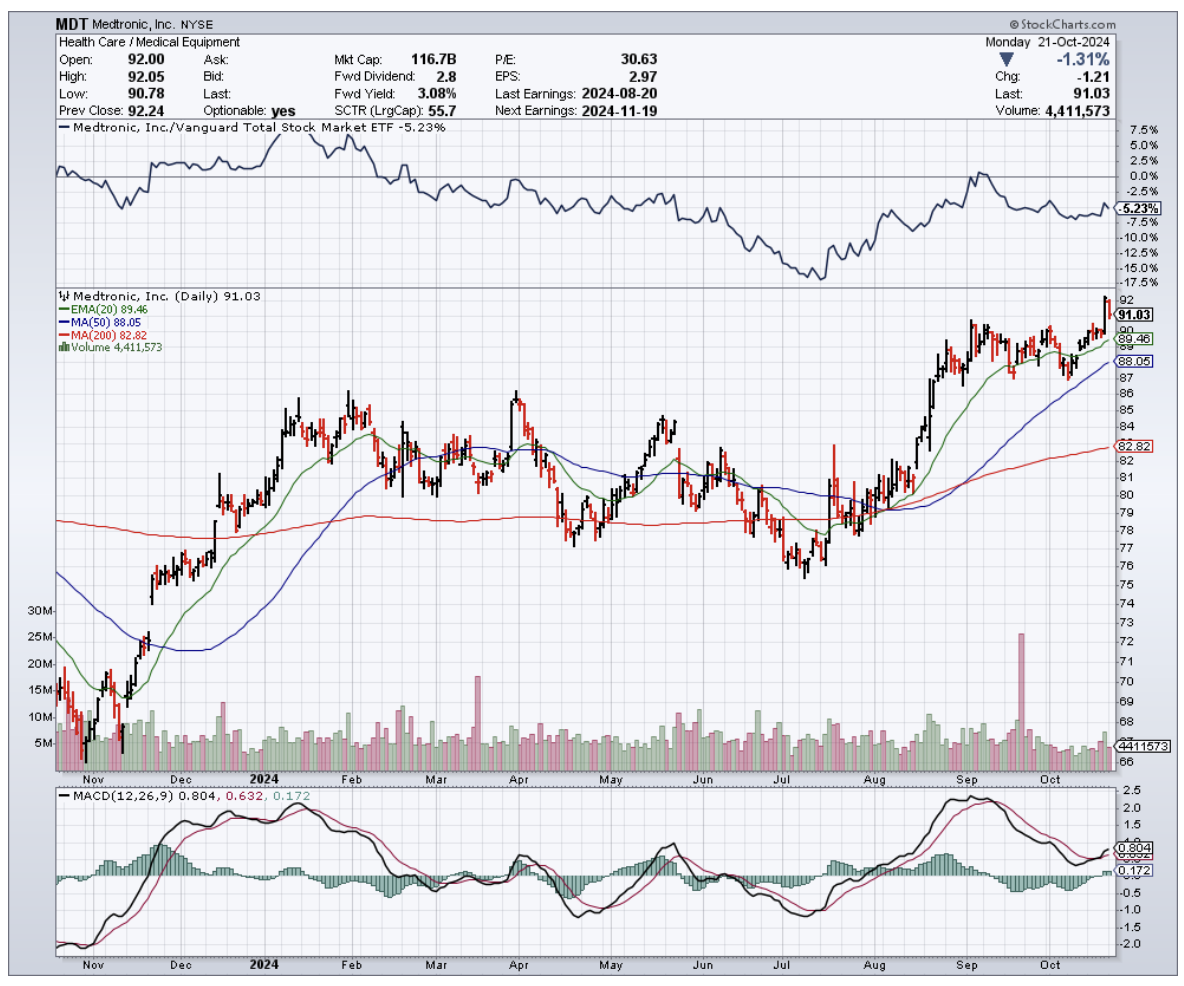

(ABT), (ISRG), (SYK), (BSX)

If Wall Street had a confessional booth, I'd be first in line. "Forgive me, market gods, for I underestimated how quickly sentiment could shift."

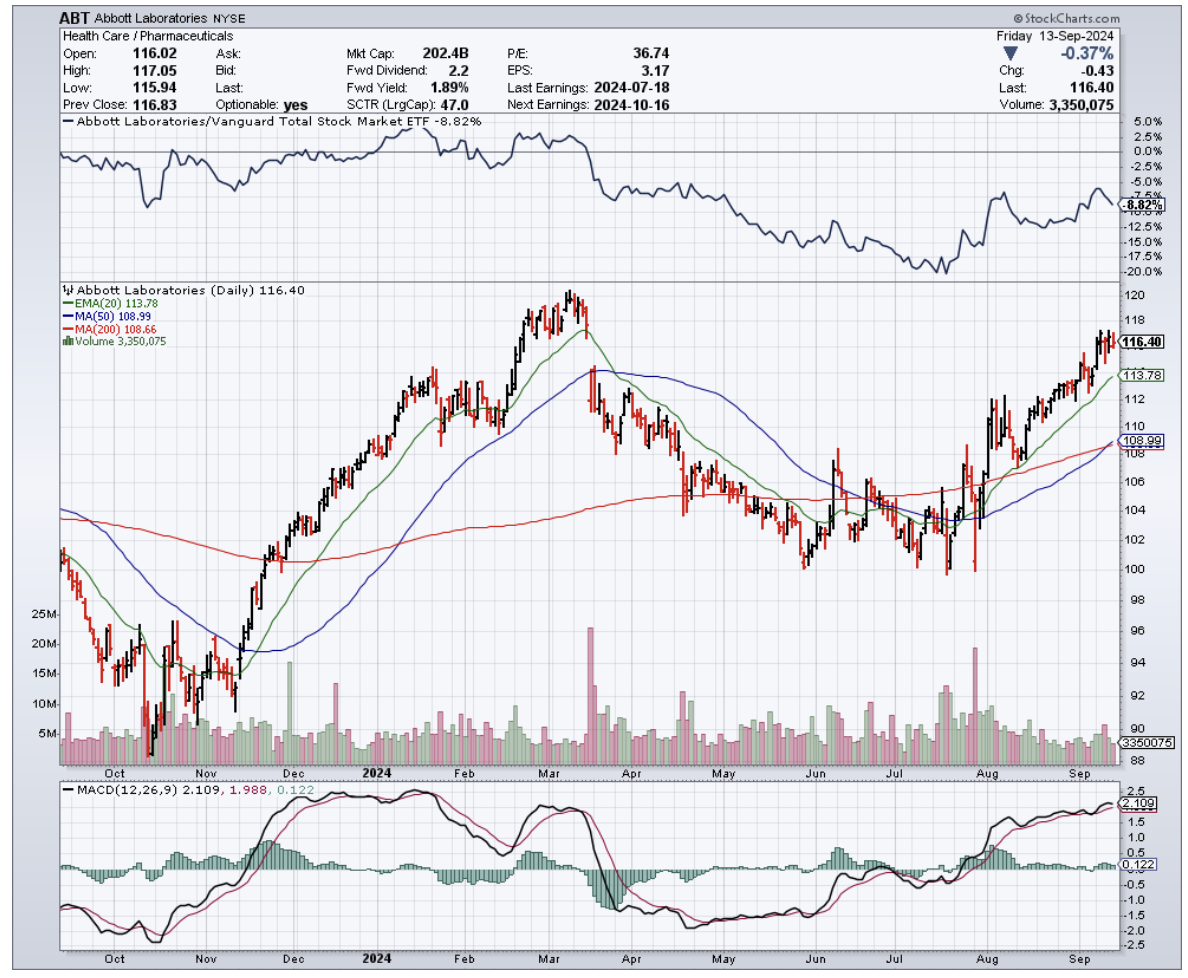

When I last wrote about Abbott Laboratories (ABT), the market was treating this medical device powerhouse like last week's leftovers—despite growth that would make most CEOs weep with joy.

Fast forward a few months, and Abbott's stock has rocketed 25%, outpacing the broader medical device sector by about 20%.

It has kept stride with Boston Scientific (BSX) while leaving Intuitive Surgical (ISRG) and Stryker (SYK) eating dust.

This kind of market whiplash reminds me of reporting from Tokyo trading floors in the 1980s—fortunes changing direction faster than a day trader after espresso, fundamentals barely shifting while sentiment performed aerial gymnastics.

So what changed? Abbott became a flight-to-safety darling.

While economic storms gather, it sits comfortably in its non-elective procedure fortress, with minimal tariff exposure and a recent legal victory reducing liability concerns.

The irony? Sentiment has now sprinted ahead of business performance. While Abbott remains a leader, its valuation leaves little room for missteps.

And if I'm overpaying for med-tech, I might as well reach for Boston Scientific instead, where growth is comparable but the valuation looks more reasonable.

Abbott’s fourth-quarter results weren’t showstopping, but they were reassuring.

Revenue landed slightly below expectations in some areas, but crucial segments—like Medical Devices—delivered strong results. Meanwhile, profit margins surprised pleasantly, reinforcing Abbott’s operational strength.

Overall revenue grew 9% organically, with Medical Devices leading at 14% growth.

The Diagnostics division posted just 1% growth, but that’s misleading—strip out COVID-19 testing effects, and underlying growth jumps to 6%.

Margins impressed, too. Gross margin improved to 56.9%, and adjusted operating income climbed 10%.

Abbott even managed a narrow revenue beat while missing slightly on EBITDA and free cash flow, largely due to tax timing that caught most analysts off guard.

I've spent decades analyzing companies across multiple sectors, and I can tell you Abbott’s medical device business deserves genuine admiration.

It maintained 14% growth from start to finish—a remarkable consistency while competitors slowed from 9.5% to 9.2% growth during the same period.

Looking at the fourth-quarter specifics, Structural Heart shone with 23% growth, outpacing Boston Scientific’s 20% and Medtronic’s 12%.

The Diabetes segment posted an impressive 20% growth, more than doubling DexCom’s 8%. Even in slower segments like Cardiac Rhythm (7%) and Neuromodulation (8%), Abbott still outperformed key competitors.

The bottom line: Abbott is executing at an exceptional level across its device portfolio.

Even its Diagnostics business, with 6% underlying growth, holds up well against Roche’s 8% and substantially outperforms Siemens Healthineers’ anemic sub-1% and Danaher’s 2% contraction.

There are three developments that investors should be paying attention to.

First, Abbott’s exposure to new tariffs is minimal—just 5% of COGS from Mexico and 1% from China. This translates to a low single-digit EPS impact, barely a rounding error in today’s environment.

Second, TriClip may have more growth potential than I previously thought. Recent data from Edwards Lifesciences’ (EW) competing Evoque device showed no mortality benefit and only modest hospitalization improvements.

This lets Abbott position TriClip as the safer approach without sacrificing quality-of-life benefits.

Third—and most significant—Abbott won a crucial legal victory in October regarding its infant formula.

A jury unanimously found the company not at fault in a necrotizing enterocolitis case, though the judge recently granted a new trial.

With 10,000 cases still pending, this development could strengthen Abbott’s settlement position and potentially cap damages below $1 billion—substantial but manageable.

I expect slight moderation next year, but Abbott should still deliver 7% growth over the next three to five years.

Newer products like Lingo (blood glucose monitoring for non-diabetics) are performing well, with significant potential in Amulet and upcoming PFA and lithotripsy offerings.

On margins, I expect EBITDA to climb above 28% within four years, with free cash flow margins reaching high-teens to low-20%.

This should drive high single-digit to low double-digit FCF growth—performance that typically earns management teams effusive praise.

Valuation, however, is challenging after the recent surge. My former 5x revenue multiple only gets to around $125, while a more aggressive 6x model approaches $150—making me about as comfortable as a cat in a dog show.

I’m surprised by how quickly sentiment shifted on Abbott, likely due to investors seeking safety amid economic uncertainty.

Whether this outperformance has staying power remains uncertain, but Abbott is certainly delivering growth that matches or exceeds competitors across most business lines.

For now, I'm watching Abbott with the same fascination I once had for Sierra mountain expeditions—impressed by the ascent but keenly aware that the air gets thinner the higher you climb.

After all, what's that old market adage? Oh right—the view is spectacular, but nobody rings a bell at the top.

Mad Hedge Biotech and Healthcare Letter

October 22, 2024

Fiat Lux

Featured Trade:

(TICK TALK)

(AAPL), (ABT), (BSX), (MDT), (RMD), (INSP), (DXCM), (PODD)

While waiting two hours to vote at the Incline Village Library this weekend, I counted the number of smartwatches in the line.

Seemed like everyone was checking their heart rates in the cold. One woman's Apple Watch even suggested she sit down after standing too long in the 40-degree weather.

That got me thinking about the billions flowing into medical wearables - and where that money should really be going instead.

Let's start with some sobering numbers about atrial fibrillation (AFib), the crown jewel of smartwatch detection capabilities.

Yes, Apple's (AAPL) 2020 study showed their watches can detect 84% of AFib cases during monitoring sessions. Sounds impressive, until you dig deeper.

Of the 50 million Americans wearing smartwatches, these devices identify only about 5,000 new AFib cases annually - a mere 0.083% of the 6 million Americans affected by the condition.

Plus, the real money tells a different story. The U.S. performs 250,000 ablation procedures yearly, creating a $3.2 billion market growing at 10% annually.

Abbott Laboratories (ABT), Boston Scientific (BSX), and Medtronic (MDT) dominate this space, with combined annual revenues of $12.4 billion from their cardiac rhythm management divisions alone.

Those 5,000 smartwatch-detected cases? They represent just 2% of annual ablation procedures. Not exactly the revolution we've been promised.

The story doesn't improve when we look at sleep apnea detection.

While Apple and Samsung tout their sleep-monitoring capabilities, their watches identify only about 60,000 of the 2 million new sleep apnea cases diagnosed yearly - that's 3% of new diagnoses.

Meanwhile, ResMed (RMD) and Inspire Medical Systems (INSP) generated combined revenues of $4.8 billion last year from sleep apnea treatments.

The smartwatch contribution to their patient pipeline is barely a rounding error.

Still, it’s not like this sector is a complete waste. The global smartwatch market stands at $58 billion and is projected to reach $98 billion by 2027, growing at 10.5% annually. Impressive, until you compare it to the traditional medical device market: $495 billion, reaching $718 billion by 2029.

The cardiac monitoring device segment alone represents $24.5 billion, expanding at 6.9% annually.

More importantly, traditional medical device companies are growing their revenues faster than smartwatch detection is adding to their patient base.

But, like I said, don't write off the sector entirely. The next generation of smartwatches promises some intriguing possibilities.

Continuous blood pressure monitoring could tap into a $23 billion market.

Non-invasive glucose tracking might crack the $28 billion diabetes monitoring space by 2027.

Enhanced sleep diagnostics could open up another $12.8 billion in opportunities.

So what's the smart play here?

Near term, keep your focus on established leaders like Abbott and Medtronic. Their upcoming Q4 earnings reports will tell us more about traditional patient acquisition trends than any smartwatch sales figures.

Watch for FDA clearances too - Abbott's new cardiac mapping system, expected in Q1 2025, could be a game-changer.

Looking out 12-24 months, keep your eye on companies like Dexcom (DXCM) and Insulet (PODD) as glucose monitoring moves mainstream.

ResMed's new sleep diagnostic platforms, launching mid-2025, could redefine how we think about sleep medicine.

Meanwhile, Boston Scientific's push into AI-enhanced cardiac monitoring might just bridge the gap between consumer tech and serious medical devices.

For long-term thinkers, watch for companies developing hybrid solutions that combine traditional devices with consumer tech.

The real breakthrough will come when medical device makers start acquiring wearable technology companies. That's when you'll know the revolution is real.

Remember, following the patient flow matters more than following the hype flow. Just like timing your visit to avoid a two-hour voting line, timing in the market is everything.

And right now, the time is right for medical device stocks, not their flashier smartwatch cousins.

Mad Hedge Biotech and Healthcare Letter

September 24, 2024

Fiat Lux

Featured Trade:

(KNOW WHEN TO HOLD ‘EM)

(LLY), (NVO), (VKTX)

Mad Hedge Biotech and Healthcare Letter

September 19, 2024

Fiat Lux

Featured Trade:

(THE KING’S SPEECH)

(ABT), (DXCM), (LLY), (NVO)

Warren Buffett once said, “Time is the friend of the wonderful company.” If that's true, Abbott Laboratories (ABT) must be Father Time's BFF because this centenarian healthcare heavyweight has been befriending our wallets for longer than most of us have been alive.

First things first: Abbott's not just any dividend stock. It's a bona fide Dividend King, having hiked its payout for over 50 consecutive years. But let's not get too misty-eyed about history.

What's got my attention is Abbott's current form. This isn't your typical sleepy pharma stock. Abbott's been flexing its muscles across multiple segments, showing growth that could very well be a worthy competition against any Silicon Valley startup.

In the first half of this year, Abbott saw positive growth in all but one segment. The laggard? Diagnostics, which took a hit as COVID-19 testing went the way of the dodo. But hey, you can't win 'em all, right?

Now, let's talk dividends. Abbott's currently yielding a respectable 1.9%, outpacing the S&P 500's measly 1.3%. With a payout ratio of 67%, there's still room for this dividend to grow.

But where's the real excitement? Two words: diabetes care.

Abbott's continuous glucose monitoring devices are hotter than a two-dollar pistol, driving 19% organic growth in the first two quarters. With diabetes becoming a bigger epidemic than we anticipated, this could be Abbott's golden goose.

Just look at the skyrocketing stocks of diabetes-focused companies like Eli Lilly (LLY) and Novo Nordisk (NVO). Different products, same lucrative market.

Abbott's FreeStyle Libre CGM system isn't just some gadget. It’s actually a genuine life-changer that's raking in $1.6 billion in quarterly sales and growing 20% year-over-year. In a market where DexCom (DXCM) is nipping at their heels, that's no small feat.

But Abbott's not resting on its laurels. They're expanding into over-the-counter CGM systems like Lingo and Libre Rio, leveraging a decade of international experience to capture more U.S. market share. It's like they're aiming to slap a diabetes monitor on every wrist in America.

And here's the kicker: the number of people living with diabetes is projected to hit 643 million by 2030 and a whopping 783 million by 2045. If that’s not the definition of a growing market, then I don’t know what is.

But Abbott isn't a one-trick pony. While they're busy trying to corner the diabetes market, they're also cooking up a storm in other areas.

Take their cardiac care lineup, for instance. Abbott's dabbling in electrophysiology with their EnSite X EP System, equipped with something called Omnipolar Technology. Sounds like something out of a sci-fi flick, right? Well, it's making cardiac mapping more precise than a Swiss watchmaker, giving arrhythmia patients a fighting chance.

But that’s not where it ends. Abbott's TriClip system is tackling tricuspid valve repair like a pro wrestler pinning an opponent. And don't get me started on their Esprit dissolvable stent. It's like the James Bond of the vascular world - it does its job and then disappears without a trace.

So, while diabetes care might be Abbott's current chart-topper right now, they've got a whole album of potential hits in the works. From glucose monitors to heart repair, Abbott's making moves that could have investors' portfolios beating as steadily as a healthy heart.

And as for you nervous nellies out there, Abbott's beta value of 0.7 suggests it's more stable than a three-legged stool. Perfect for those of you who break out in hives at the mere mention of volatility.

Now, it hasn't all been smooth sailing. Abbott recently faced a trial over claims its preterm infant formula caused a dangerous disease. But don't start panic-selling just yet.

JPMorgan and Barclays reckon the liability is likely to be smaller than a gnat's appetite. Abbott's management is confident, too, probably because the product in question accounts for a whopping... wait for it... $9 million in revenue. That's pocket change for a company like Abbott.

Looking ahead, Abbott's firing on all cylinders. They're seeing 9.3% organic revenue growth (excluding their COVID products), and they're so confident they've raised their full-year guidance.

Meanwhile, valuation-wise, Abbott's looking pretty good. With double-digit earnings growth expected and an AA-credit rating (better than some countries I could name), this stock could easily outperform the market.

So, what's the bottom line? Abbott's got the stability of a Dividend King, the growth potential of a tech startup, and more irons in the fire than a blacksmith's shop.

It's trading at a fair price, and with its track record of innovation and dividend growth, this could be your ticket to a healthier portfolio. After all, in the race for returns, slow and steady often wins more than just participation trophies. I suggest you buy the dip.

Mad Hedge Biotech and Healthcare Letter

August 20, 2024

Fiat Lux

Featured Trade:

(POX POPULI)

(BVNRY), (EBS), (GOVX), (SIGA), (CMRX), (TNXP), (TMO), (ABT), (MRNA), (PFE)

Hold onto your hazmat suits because the world of infectious diseases just got a lot more interesting. And if you're someone with a stomach for volatility, you might want to pay attention.

Mpox is back, and it's brought a nasty new cousin to the party. The World Health Organization (WHO) just hit the big red button, declaring the mpox outbreak a public health emergency of international concern (PHEIC). That's fancy talk for "this is serious, people."

Let's break it down. We're not dealing with your garden-variety mpox here. This is a new strain, dubbed Clade Ib, and it's tearing through central Africa like a bull in a china shop.

The Democratic Republic of Congo (DRC) has seen over 15,600 cases so far this year, more than all of last year. And it's not staying put.

Kenya, Burundi, Rwanda, and Uganda are all reporting their first-ever mpox cases. It's like watching a virus go on a world tour, minus the t-shirts and overpriced concessions.

Now, before you start panic-buying toilet paper again, the Centers for Disease Control and Prevention (CDC) says the risk to the U.S. is very low.

But they're still telling healthcare providers to keep their eyes peeled for any funky rashes on patients who've been globe-trotting lately.

So, what do we do with this information? Well, let's talk vaccines.

Bavarian Nordic (BVNRY), the company behind the most widely used mpox vaccine, has seen its stock jump more than 30% since the WHO's announcement. It's like they won the pharmaceutical lottery.

And Uncle Sam's not shy about showing them some love – the U.S. Department of Health and Human Services just placed a $156.8 million order for a bulk vaccine product.

But they're not the only player in town.

Emergent Biosolutions (EBS), another vaccine manufacturer, also saw its stock surge when the news broke.

Even GeoVax Labs (GOVX) saw its stock shoot up 40% yesterday morning. Not bad for a company most people had never heard of last week. They're working on an MVA vaccine – that's Modified Vaccinia Ankara for you science nerds out there. It's the go-to choice for folks with weakened immune systems.

But it's not all sunshine and rainbows in vaccine land.

Siga Technologies (SIGA) released some disappointing trial data for their antiviral drug TPOXX. Turns out, it's not much better than a sugar pill for treating mpox.

Other companies are also jockeying for position.

Chimerix (CMRX) is developing brincidofovir, an antiviral that could potentially treat mpox. Tonix Pharmaceuticals (TNXP) is working on TNX-801, a live-virus vaccine candidate.

And let's not forget the diagnostic giants like Thermo Fisher Scientific (TMO) and Abbott Laboratories (ABT). After all, in the world of infectious diseases, being able to spot the bad guy quickly is half the battle.

Even the big guns of the COVID-19 vaccine world, Moderna (MRNA) and Pfizer (PFE), might decide to flex their mRNA muscles in the mpox arena. And with their track record, who's going to bet against them?

But here's the million-dollar question: Is this a golden opportunity for investors, or a potential minefield? The answer, as always in the stock market, is "it depends."

On one hand, companies directly involved in mpox vaccines, treatments, and diagnostics could see their stocks soar if the outbreak worsens.

On the other hand, the biotech sector is about as stable as a jenga tower in an earthquake. Today's miracle drug could be tomorrow's cautionary tale.

The smart money isn't putting all its eggs in the mpox basket. Diversification is still the name of the game. Remember, this outbreak could fizzle out as quickly as it started, leaving one-trick ponies high and dry.

Plus, let's always keep in mind the wild card in all this: government contracts.

In the world of infectious diseases, Uncle Sam often holds the purse strings. Keep your ear to the ground for any whispers of government funding or contracts. That kind of news can send stocks into the stratosphere faster than you can say "public health emergency."

So, what's the bottom line? The mpox outbreak is creating some intriguing opportunities in the biotech sector. But as with any investment, don't let the fear of missing out cloud your judgment.

And remember, in the stock market, as in epidemiology, it's all about managing risk.

In the meantime, maybe skip that bushmeat sandwich on your next African safari. Just a thought.