Global Market Comments

July 3, 2025

Fiat Lux

Featured Trade:

(JULY 2 BIWEEKLY STRATEGY WEBINAR Q&A)

(SPY), (NVDA), (MSFT), (META), (SNOW), (GOOGL), (DHI), (LEN), (KBH), (FXE), (FXA), (FXY), (FXY), (GLD), (SLV), (PPLT), (ALB), (SQM), (NEM), (ABX)

Global Market Comments

July 3, 2025

Fiat Lux

Featured Trade:

(JULY 2 BIWEEKLY STRATEGY WEBINAR Q&A)

(SPY), (NVDA), (MSFT), (META), (SNOW), (GOOGL), (DHI), (LEN), (KBH), (FXE), (FXA), (FXY), (FXY), (GLD), (SLV), (PPLT), (ALB), (SQM), (NEM), (ABX)

A huge new buyer may eventually enter the gold market.

That could be a year off, maybe two, or three at the most.

I’ll give you a hint who: your taxes will pay for it.

If true, it could send the price of the barbarous relic soaring above $5,000, or even $50,000 an ounce, a target long led by the tin hat Armageddon crowd.

When I spoke to a senior official at the Federal Reserve the other day, I couldn’t believe what I was hearing.

If the American economy moves into the next recession with rising inflation, a near certainty, its hands will be tied. It dare not cut rates for fear of further fanning the flames.

At that point, our central bank’s primary tool for stimulating US businesses will become utterly useless, ineffective, and impotent.

What else is in the tool bag?

How about large-scale purchases of Gold (GLD)?

You are probably as shocked as I am by this possibility. But there is a rock-solid logic to the plan. As solid as the vault at Fort Knox.

The idea is to create asset price inflation that will spread to the rest of the economy. It already did this with great success from 2009-2014 with quantitative easing, whereby almost every class of debt securities was hoovered up by the government.

“QE on steroids” would involve large-scale purchases of not only gold, but stocks, government bonds, and exchange-traded funds as well.

If you think I’ve been smoking California’s largest cash export (it’s not almonds), you would be in error. I should point out that the Japanese government is already pursuing QE to this extent, at least in terms of equity-type investments.

And, as the history buff that I am, I can tell you that it has been done in the US as well, with tremendous results.

If you thought that President Obama had it rough when he came into office in 2009, it was nothing compared to what Franklin Delano Roosevelt inherited.

The country was in its fourth year of the Great Depression. US GDP had cratered by 43%, consumer prices had crashed by 24%, the unemployment rate was 25%, and stock prices had vaporized by 90%.

Mass starvation loomed.

Drastic measures were called for.

FDR issued Executive Order 6102 banning private ownership of gold, ordering citizens to sell their holdings to the US Treasury at a lowly $20.67 an ounce.

He then urged Congress to pass the Gold Reserve Act of 1934, which instantly revalued the government’s holdings at $35.00, an increase of 69.32%. These and other measures caused the value of America’s gold holdings to leap from $4 to $12 billion.

Since the US was still on the gold standard back then, this triggered an instant dollar devaluation of more than 50%. The high gold price sucked in massive amounts of the yellow metal from abroad creating, you guessed it, inflation.

The government then borrowed massively against this artificially created wealth to fund the landscape-altering infrastructure projects of the New Deal.

It worked.

During the following three years, the GDP skyrocketed by 48%, inflation eked out a 2% gain, the unemployment rate dropped to 18%, and stocks jumped by 80%. Happy days were here again.

However, in the 21st-century version of such a gold policy, it is highly unlikely that we would see another gold ownership ban.

Instead, the Fed would most likely move into the physical gold market, sitting on the bid for years, much like it did in the 2010s Treasury bond market for five years. Gold prices would increase by a multiple of current levels.

It would then borrow against its new gold holdings, plus the 4,176 metric tonnes worth $40 billion at today’s market prices already sitting in Fort Knox, to fund a multibillion-dollar tax cut.

Yes, this all sounds like a fantasy. But negative interest rates were considered an impossibility only a few years ago.

The Fed’s move on gold would be only one aspect of a multi-faceted package of desperate last-ditch measures to resuscitate the economy at some point in the future. The time to start buying gold is RIGHT NOW!

Persistent urban legends and Internet rumors claim that the vault is actually empty or filled with fake steel bars painted gold.

That is, until Treasury Secretary Steven Mnuchin visited the vault on his way to view the solar eclipse at government expense in August 2017.

He says the gold is still there. But only if you believe Steve Mnuchin. A lot don’t.

We’ll never know for sure. Visitors are not allowed.

Global Market Comments

January 23, 2025

Fiat Lux

Featured Trades:

(WHY WATER WILL SOON BE WORTH MORE THAN OIL),

(CGW), (PHO), (FIW), (VE), (TTEK), (PNR),

(WHY WARREN BUFFETT HATES GOLD),

(GLD), (GDX), (ABX)

After seven years in the penalty box, gold is finally starting to come alive, and the Armageddon crowd is absolutely loving it. Maybe after ten years of rising, stocks are finally expensive on a relative basis?

These are the guys who are perennially predicting the collapse of the dollar, the default of the US government, hyperinflation, and the end of the world.

Better to keep all your assets in gold and silver, store at least a year’s worth of canned food, and keep your untraceable guns well-oiled and supplied with ammo, preferably in high-capacity magazines.

If you followed their advice, you lost your shirt.

I have broken many of these wayward acolytes of their money-losing habits. But not all of them. There seems to be an endless supply emanating from the hinterlands.

The “Oracle of Omaha” Warren Buffet often goes to great lengths to explain why he despises the yellow metal.

The sage doesn't really care about the gold, whatever the price. He sees it primarily as a bet on fear. I imagine he feels the same about Bitcoin, the modern tulips of our age.

If investors are more afraid in a year than they are today, then you make money on gold. If they aren't, then you lose money.

The only problem now is that fear ain’t working.

If you took all the gold in the world, it would form a cube 67 feet on a side, worth $5 trillion. For that same amount of money, you could own other assets with far greater productive earning power, including:

*All the farmland in the US, about 1 billion acres, which is worth $2.5 trillion.

*Seven Apple’s (AAPL), the second largest capitalized company in the world at $731 billion.

Instead of producing any income or dividends, gold just sits there and shines, making you feel like King Midas.

I don't know. With the stock market at an all-time high and oil trading at $75/barrel, a bet on fear looks pretty good to me right now.

I'm still sticking with my long-term forecast of the old inflation-adjusted high of $2,300/ounce.

It is just a matter of time before emerging market central bank buying pushes it up there. And who knows? Fear might make a comeback too.

Those in the investment business are well used to the Armageddon crowd. These are the guys who are perennially predicting the collapse of the dollar, the default of the US government, hyperinflation, and the end of the world.

Maybe after 11 years of rising, stocks are finally expensive on a relative basis?

Their perennial recommendations are to keep all your assets in gold and silver, store at least a year’s worth of canned food, and keep your untraceable guns well-oiled and supplied with ammo, preferably in high capacity magazines.

If you followed their advice, you lost your shirt.

I have broken many of these wayward acolytes of their money-losing habits. But not all of them. There seems to be an endless supply emanating from the hinterlands.

The “Oracle of Omaha” Warren Buffet often goes to great lengths to explain why he despises the yellow metal.

The sage doesn't really care about the gold, whatever the price. He sees it primarily as a bet on fear. I imagine he feels the same about Bitcoin, the modern tulips of our age.

If investors are more afraid in a year than they are today, then you make money on gold. If they aren't, then you lose money.

The only problem now is that fear ain’t working.

If you took all the gold in the world, it would form a cube 67 feet on all sides, worth $5 trillion. For that same amount of money, you could own other assets with far greater productive earning power, including:

*All the farmland in the US, about 1 billion acres, which is worth $2.5 trillion.

*Two Apple’s (AAPL), the largest capitalized company in the world at $3 trillion.

Instead of producing any income or dividends, gold just sits there and shines, making you feel like King Midas.

I don't know. With the stock market at an all-time high, and oil trading at $70.49/barrel, a bet on fear looks pretty good to me right now.

I'm still sticking with my long-term forecast of the old inflation-adjusted high of $2,300/ounce. But it might be very long term.

It is just a matter of time before emerging market central bank buying pushes it up there. And who knows? Fear might make a comeback too.

Global Market Comments

December 15, 2021

Fiat Lux

Featured Trade:

(THE MAD HEDGE TRADERS & INVESTORS SUMMIT VIDEOS ARE UP!)

(WHY WARREN BUFFET HATES GOLD),

(GLD), (GDX), (ABX), (GOLD)

Global Market Comments

September 23, 2021

Fiat Lux

Featured Trade:

(THE MAD HEDGE TRADERS & INVESTORS SUMMIT VIDEOS ARE UP!)

(WHY WARREN BUFFET HATES GOLD),

(GLD), (GDX), (ABX), (GOLD)

Global Market Comments

December 4, 2020

Fiat Lux

FEATURED TRADE:

(WHY WATER WILL SOON BE WORTH MORE THAN OIL),

(CGW), (PHO), (FIW), (VE), (TTEK), (PNR), (BYND),

(WHY WARREN BUFFETT HATES GOLD),

(GLD), (GDX), (ABX), (GOLD)

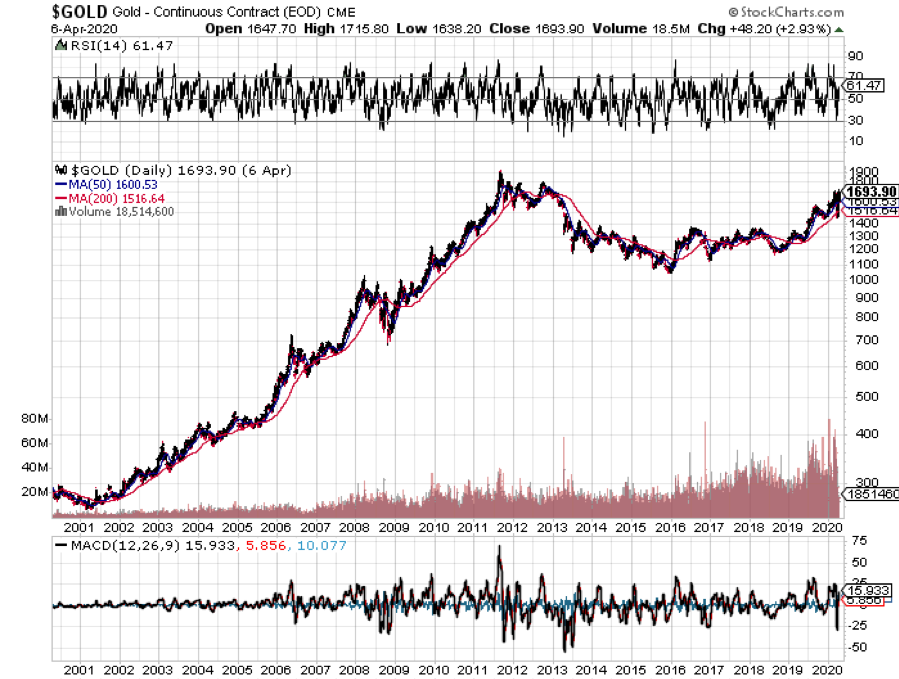

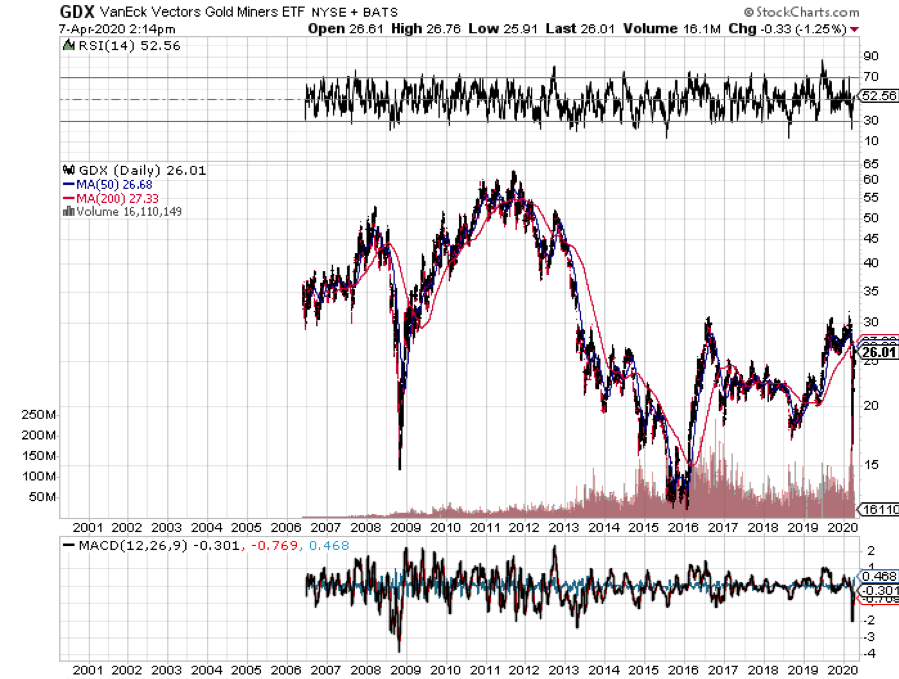

I have been bullish on gold (GLD) for the last three years and the payoff is finally here (click here).

How high could it really go?

The recent massive stimulus measures to fight the Coronavirus-induced depression is certainly bringing forward the rebirth of inflation. The Fed has just increased all of the $17 trillion quantitative easing created globally over the past decade by a staggering 50% in weeks!

This is hugely gold-friendly.

I was an unmitigated bear on the price of gold after it peaked in 2011. In recent years, the world has been obsessed with yields, chasing them down to historically low levels across all asset classes.

But now that much of the world already has, or is about to have negative interest rates, a bizarre new kind of mathematics applies to gold ownership.

Gold’s problem used to be that it yielded absolutely nothing, cost you money to store, and carried hefty transactions costs. That asset class didn’t fit anywhere in a yield-obsessed universe.

Now, we have a horse of a different color.

Europeans wishing to put money in a bank have to pay for the privilege to do so. Place €1 million on deposit on an overnight account, and you will have only 996,000 Euros in a year. You just lost 40 basis points on your -0.40% negative interest rate.

With gold, you still earn zero, an extravagant return in this upside-down world. All of a sudden, zero is a win.

For the first time in human history, that gives you a 40-basis point yield advantage over Euros. Similar numbers now apply to Japanese yen deposits as well.

As a result, the numbers are so compelling that it has sparked a new gold fever among hedge funds and European and Japanese individuals alike.

Websites purveying investment grade coins and bars crashed multiple times last week due to overwhelming demand (I occasionally have the same problem). Some retailers have run out of stock.

So I’ll take this opportunity to review a short history of the gold market (GLD) for the young and the uninformed.

Since it peaked in the summer of 2011, the barbarous relic was beaten like the proverbial red-headed stepchild, dragging silver (SLV) down with it. It faced a perfect storm.

Gold was traditionally sought after as an inflation hedge. But with economic growth weak, wages stagnant, and much work still being outsourced abroad, deflation became rampant (click here).

The biggest buyers of gold in the world, Indian investors, have seen their purchasing power drop by half, thanks to the collapse of the rupee against the US dollar. The government increased taxes on gold in order to staunch precious capital outflows.

You could also blame the China slowdown for the declining interest in the yellow metal, which is now in its sixth year of falling economic growth.

Chart gold against the Shanghai index, and the similarity is striking, until negative interest rates became widespread in 2016.

In the meantime, gold supply/demand balance was changing dramatically.

While no one was looking, the average price of gold production soared from $5 in 1920 to $1,300 today. Over the last 100 years, the price of producing gold has risen four times faster than the underlying metal.

It’s almost as if the gold mining industry is the only one in the world which sees real inflation, since costs soared at a 15% annual rate for the past five years.

This is a function of what I call “peak gold.” They’re not making it anymore. Miners are increasingly being driven to higher risk, more expensive parts of the world to find the stuff.

You know those giant six-foot high tires on heavy dump trucks? They now cost $200,000 each, and buyers face a three-year waiting list to buy one.

Barrick Gold (GOLD) didn’t try to mine gold at 15,000 feet in the Andes, where freezing water is a major problem, because they like the fresh air.

What this means is that when the spot price of gold fell below the cost of production, miners simply shut down their most marginal facilities, drying up supply.

Barrick Gold, a client of the Mad Hedge Fund Trader, can still operate as older mines carry costs that go all the way down to $600 an ounce.

I am constantly barraged with emails from gold bugs who passionately argue that their beloved metal is trading at a tiny fraction of its true value and that the barbaric relic is really worth $5,000, $10,000, or even $50,000 an ounce (GLD).

They claim the move in the yellow metal we are seeing now is only the beginning of a 30-fold rise in prices, similar to what we saw from 1972 to 1979, when it leapt from $32 to $950.

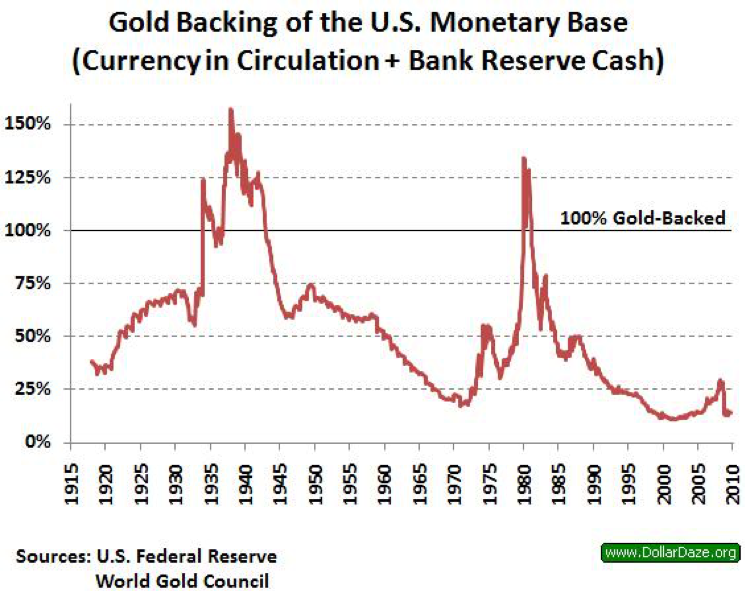

So, when the chart below popped up in my in-box showing the gold backing of the US monetary base, I felt obligated to pass it on to you to illustrate one of the intellectual arguments these people are using.

To match the gain seen since the 1936 monetary value peak of $35 an ounce when the money supply was collapsing during the Great Depression and the double top in 1979 when gold futures first tickled $950, this precious metal has to increase in value by 800% from the recent $1,050 low. That would take our barbarous relic friend up to $8,400 an ounce.

To match the move from the $35/ounce, 1972 low to the $950/ounce, 1979 top in absolute dollar terms, we need to see another 27.14 times move to $28,497/ounce.

Have I gotten you interested yet?

I am long term bullish on gold, other precious metals, and virtually all commodities for that matter. But I am not that bullish. These figures make my own $2,300/ounce long-term prediction positively wimp-like by comparison.

The seven-year spike up in prices we saw in the seventies, which found me in a very long line in Johannesburg, South Africa to unload my own Krugerrands in 1979, was triggered by a number of one-off events that will never be repeated.

Some 40 years of unrequited demand was unleashed when Richard Nixon took the US off the gold standard and decriminalized private ownership in 1972. Inflation then peaked around 20%. Newly enriched sellers of oil had a strong historical affinity with gold.

South Africa, the world’s largest gold producer, was then a boycotted international pariah teetering on the edge of disaster. We are nowhere near the same geopolitical neighborhood today, and hence, my more subdued forecast.

But then again, I could be wrong.

In the end, gold may have to wait for a return of real inflation to resume its push to new highs. The previous bear market in gold lasted 18 years, from 1980, to 1998, so don’t hold your breath.

What should we look for? The surprise that your friends get out of the blue pay increase, the largest component of the inflation calculation.

This is happening now in technology and healthcare, but nowhere else. When I visit open houses in my neighborhood in San Francisco, half the visitors are thirty somethings wearing hoodies offering to pay cash.

It could be a long wait for real inflation, possibly into the mid 2020s when shocking wage hikes spread elsewhere.

You’ll be the first to know when that happens.

As for the many investment advisor readers who have stayed long gold all along to hedge their clients other risk assets, good for you.

You’re finally learning!

Global Market Comments

February 27, 2020

Fiat Lux

Featured Trade:

(GET READY TO TAKE A LEAP BACK INTO LEAPS),

(AAPL), (BA),

(TESTIMONIAL)