Global Market Comments

February 26, 2020

Fiat Lux

SPECIAL GOLD ISSUE

Featured Trade:

(THE ULTRA BULL ARGUMENT FOR GOLD),

(GLD), (GDX), (ABX), (SLV), (PALL), (PPLT)

(TESTIMONIAL)

Global Market Comments

February 26, 2020

Fiat Lux

SPECIAL GOLD ISSUE

Featured Trade:

(THE ULTRA BULL ARGUMENT FOR GOLD),

(GLD), (GDX), (ABX), (SLV), (PALL), (PPLT)

(TESTIMONIAL)

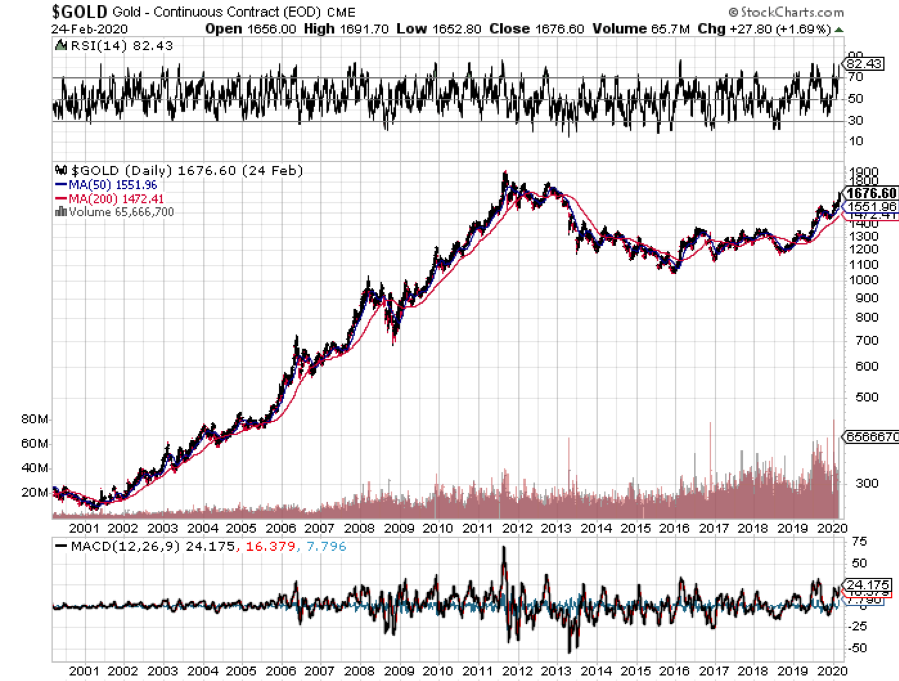

With global stock markets in free fall and interest rates everywhere headed to zero, the outlook for gold has gone from strength to strength.

Shunned as the pariah of the financial markets for years, the yellow metal has suddenly become everyone’s favorite hedge.

Now that gold is back in fashion, how high can it really go?

The question begs your rapt attention, as the Coronavirus has suddenly unleashed a plethora of new positive fundamentals for the barbarous relic.

It turns out that gold is THE deflationary asset to own. Who knew?

I was an unmitigated bear on the price of gold after it peaked in 2011. In recent years, the world has been obsessed with yields, chasing them down to historically low levels across all asset classes.

But now that much of the world already has, or is about to have negative interest rates, a bizarre new kind of mathematics applies to gold ownership.

Gold’s problem used to be that it yielded absolutely nothing, cost you money to store, and carried hefty transactions costs. That asset class didn’t fit anywhere in a yield-obsessed universe.

Now we have a horse of a different color.

Europeans wishing to put money in a bank have to pay for the privilege to do so. Place €1 million on deposit on an overnight account, and you will have only 996,000 Euros in a year. You just lost 40 basis points on your -0.40% negative interest rate.

With gold, you still earn zero, an extravagant return in this upside-down world. All of a sudden, zero is a win.

For the first time in human history, that gives you a 40-basis point yield advantage by gold over Euros. Similar numbers now apply to Japanese yen deposits as well.

As a result, the numbers are so compelling that it has sparked a new gold fever among hedge funds and European and Japanese individuals alike.

Websites purveying investment grade coins and bars crashed multiple times last week, due to overwhelming demand (I occasionally have the same problem). Some retailers have run out of stock.

And last week, the virus went pandemic as silver rocketed 8.6% and others like Palladium (PALL) were also frenetically bid.

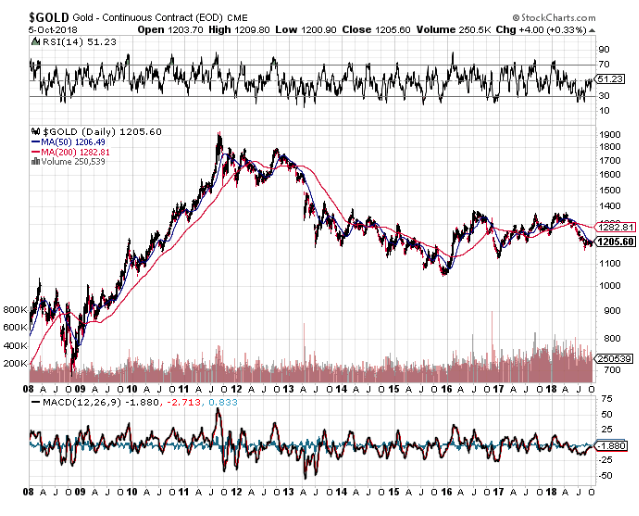

So I’ll take this opportunity to review a short history of the gold market (GLD) for the young and the uninformed.

Since it last peaked in the summer of 2011 at $1,927 an ounce, the barbarous relic was beaten like the proverbial red-headed stepchild, dragging silver (SLV) down with it. It faced a perfect storm.

Gold was traditionally sought after as an inflation hedge. But with economic growth weak, wages stagnant, and much work still being outsourced abroad, deflation became rampant.

The biggest buyers of gold in the world, the Indians, have seen their purchasing power drop by half, thanks to the collapse of the rupee against the US dollar. The government increased taxes on gold in order to staunch precious capital outflows.

Chart gold against the Shanghai index, and the similarity is striking, until negative interest rates became widespread in 2016.

In the meantime, gold supply/demand balance was changing dramatically.

While no one was looking, the average price of gold production soared from $5 in 1920 to $1,400 today. Over the last 100 years, the price of producing gold has risen four times faster than the underlying metal.

It’s almost as if the gold mining industry is the only one in the world which sees real inflation, since costs soared at a 15% annual rate for the past five years.

This is a function of what I call “peak gold.” They’re not making it anymore. Miners are increasingly being driven to higher risk, more expensive parts of the world to find the stuff.

You know those tires on heavy dump trucks? They now cost $200,000 each, and buyers face a three-year waiting list to buy one.

Barrick Gold (GOLD), the world’s largest gold miner, didn’t try to mine gold at 15,000 feet in the Andes, where freezing water is a major problem, because they like the fresh air.

What this means is that when the spot price of gold fell below the cost of production, miners simply shut down their most marginal facilities, drying up supply. That has recently been happening on a large scale.

Barrick Gold, a client of the Mad Hedge Fund Trader, can still operate, as older mines carry costs that go all the way down to $600 an ounce.

No one is going to want to supply the sparkly stuff at a loss. So, supply disappeared.

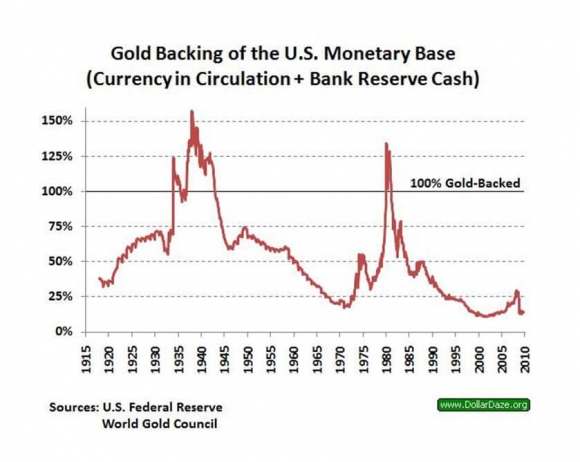

I am constantly barraged with emails from gold bugs who passionately argue that their beloved metal is trading at a tiny fraction of its true value, and that the barbaric relic is really worth $5,000, $10,000, or even $50,000 an ounce (GLD).

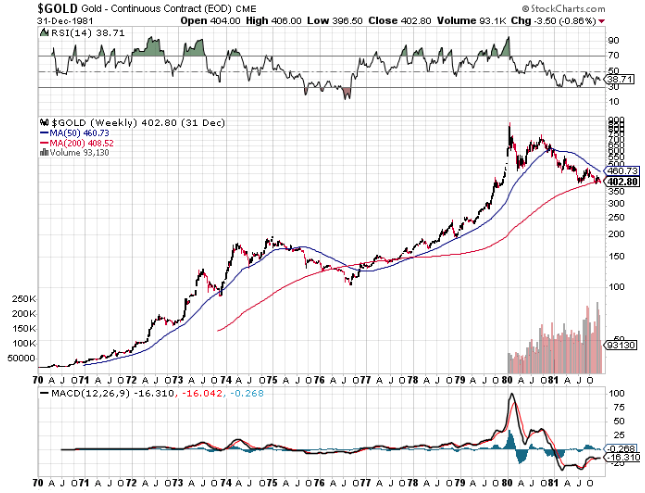

They claim the move in the yellow metal we are seeing now is only the beginning of a 30-fold rise in prices, similar to what we saw from 1972 to 1979, when it leapt from $32 to $950.

So, when the chart below popped up in my inbox showing the gold backing of the US monetary base, I felt obligated to pass it on to you to illustrate one of the intellectual arguments these people are using.

To match the gain seen since the 1936 monetary value peak of $35 an ounce, when the money supply was collapsing during the Great Depression, and the double top in 1979 when gold futures first tickled $950, this precious metal has to increase in value by 800% from the recent $1,050 low. That would take our barbarous relic friend up to $8,400 an ounce.

To match the move from the $35/ounce, 1972 low to the $950/ounce, 1979 top in absolute dollar terms, we need to see another 27.14 times move to $28,497/ounce.

Have I gotten your attention yet?

I am long term bullish on gold, other precious metals, and virtually all commodities for that matter. But I am not that bullish. These figures make my own $2,300/ounce long-term prediction positively wimp-like by comparison.

The seven-year spike up in prices we saw in the seventies, which found me in a very long line in Johannesburg, South Africa to unload my own Krugerrands in 1979, was triggered by a number of one-off events that will never be repeated.

Some 40 years of unrequited demand was unleashed when Richard Nixon took the US off the gold standard and decriminalized private ownership in 1972. Inflation then peaked around 20%. Newly enriched sellers of oil had a strong historical affinity with gold.

South Africa, the world’s largest gold producer, was then a boycotted international pariah and teetering on the edge of disaster. We are nowhere near the same geopolitical neighborhood today, and hence, my more subdued forecast.

But then again, I could be wrong.

In the end, gold may have to wait for a return of real inflation to resume its push to new highs. The previous bear market in gold lasted 18 years, from 1980 to 1998, so don’t hold your breath.

What should we look for? The surprise that your friends get out of the blue pay increase, the largest component of the inflation calculation.

This is happening now in technology and is slowly tricking down to minimum wage workers. When I visit open houses in my neighborhood in San Francisco, half the visitors are thirty-somethings wearing hoodies offering to pay cash.

It could be a long wait for real inflation, possibly into the mid-2020s, when shocking wage hikes spread elsewhere.

I’ll be back playing gold again, given a good low-risk, high-return entry point.

You’ll be the first to know when that happens.

As for the many investment advisor readers who have stayed long gold all along to hedge their clients' other risk assets, good for you.

You’re finally learning!

Global Market Comments

December 3, 2019

Fiat Lux

Featured Trade:

(WHY WATER WILL SOON BE WORTH MORE THAN OIL),

(CGW), (PHO), (FIW), (VE), (TTEK), (PNR), (BYND),

(WHY WARREN BUFFETT HATES GOLD),

(GLD), (GDX), (ABX), (GOLD),

Global Market Comments

May 8, 2019

Fiat Lux

SPECIAL GOLD ISSUE

Featured Trade:

(THE ULTRA BULL ARGUMENT FOR GOLD),

(GLD), (GDX), (ABX), (SLV), (PALL), (PPLT)

(TESTIMONIAL)

Global Market Comments

January 30, 2019

Fiat Lux

Featured Trade:

(WHY WATER WILL SOON BE WORTH MORE THAN OIL),

(CGW), (PHO), (FIW), (VE), (TTEK), (PNR),

(WHY WARREN BUFFETT HATES GOLD),

(GLD), (GDX), (ABX),

Global Market Comments

October 25, 2018

Fiat Lux

Featured Trade:

(THE LAZY MAN’S GUIDE TO TRADING),

(ROM), (UXI), (BIB), (UYG),

(THE NEXT THING FOR THE FED TO BUY IS GOLD),

(GLD), (GOLD), (GDX), (ABX), (NEM)

Global Market Comments

October 9, 2018

Fiat Lux

SPECIAL REPORT ON GOLD

Featured Trade:

(TAKING A LOOK AT GOLD LEAPS),

(GLD), (ABX), (AMZN)

As incredible as it may sound, I’m starting to hear good things about gold. That’s amazing as the barbarous relic has been the red headed step child of the financial markets for the past six years. Not since the yellow metal peaked in 2011 have I heard the talk so bullish.

You can thank central banks which have become the principal buyers of gold in 2018. China is always the largest buyer. It has been joined by Russia, which is avoiding American trade sanction, and Kazakhstan. Now Poland has joined the fray. Central banks have accounted for a stunning 264 metric tonnes of purchases this year, or some 9.3 million ounces.

You can thank the coming return of inflation in the US economy, gold’s best friend. With a 4.2% GDP growth rate in Q2, the return of rapidly rising prices is just a matter of time. We here in Silicon Valley have grown inured to ever rising prices for everything. You in the rest of the country are about to get the bad news.

You can thank Amazon (AMZN) founder Jeff Bezos for pouring gasoline on the fire. By giving 250,000 US workers a 25% pay increase from $12 to $15, he has created a national short squeeze for minimum wage workers. If McDonald’s (MCD), Target (TGT), and Wal-Mart (WMT) join the fray, as they must or lose workers, wage inflation will go national.

Yes, you can remind me that rising interest rates are a terrible backdrop against which to own gold. The Federal Reserve has essentially promised us four more 25 basis point rate hikes by next summer. That would take the overnight rate to 3.25%, a historically "normalized” rate.

But what happens when the rate hikes stop? Gold takes off like a scalded chimp.

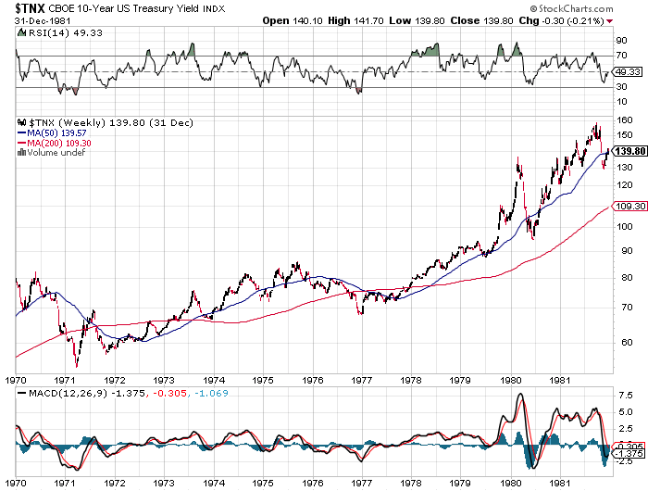

It is in fact a myth that gold can’t perform in a raising rate environment. When you look at gold’s “golden age” during the 1970’s when the barbarous relic rocketed from $34 to $900, a 24-fold increase, interest rates were rising almost as fast.

Over the same time period, the ten-year US Treasury yield soared from 5% to 16%. At the end of the day, investors fear inflation far more than high interest rates.

So when you believe that an oversold asset is about to turn but don’t know when, what is the best course of action?

Long Term Equity Anticipation Securities, or LEAPS, are a great way to play the market when you expect a substantial move up in a security over a long period of time. Get these right and the returns over 18 months can amount to several hundred percent.

At market bottoms these are a dollar a dozen. At all-time highs they are as scarce as hen’s teeth. However, scouring all asset classes there are a few sweet ones to be had.

Today, you can buy the SPDR Gold Shares ETF (GLD) January 2020 $120-$125 call spread for $1.60. For those who are new to the Mad Hedge Fund Trader, that involves buying the January 2020 $120 call and selling short the January 2020 $125 call.

This has the attributes of reducing your cost and minimizing the cost of time decay while giving you highly leveraged upside exposure over a long period of time.

If the price of gold rises by $11.20, from $113.80 to $125, a mere 9.8% by the January 17 option expiration date, the profit on this trade will amount to 212.5%. In order words, a $1,000 investment will become worth $3,125 if gold simply returns back to where it was in April.

If you’re more aggressive than I am (unlikely), you can buy the SPDR Gold Shares ETF (GLD) January 2020 $125-$130 call spread for $1.00, That would give you a maximum potential profit of 400%. In order words, a $1,000 investment will become worth $5,000 if gold simply return back to its February 2018 high.

A number of other fundamental factors are coming into play that will have a long-term positive influence on the price of the barbarous relic.

The only question is not if, but when the next bull market in the yellow metal will accelerate.

All of the positive arguments in favor of gold all boil down to a single issue: they're not making it anymore.

Take a look at the chart below and you'll see that new gold discoveries are in free fall. That's because falling prices from 2011 to 2018 caused exploration budgets to fall off a cliff.

Gold production peaked in the fourth quarter of 2015 and is expected to decline by 20% in the following four years.

The industry average cost is thought to be around $1,400 an ounce, although some legacy mines such as at Barrack Gold (ABX) can produce it for as little as $600.

So why dig out more of the stuff if it means losing more money?

It all sets up a potential turn in the classic commodities cycle. Falling prices demolish production and wipe out investors. This inevitably leads to supply shortages.

When the buyers finally return for the usual cyclical macro-economic reasons, there is none to be had, and price spikes can occur which can continue for years.

In other words, the cure for low prices is low prices.

Worried about new supply quickly coming on-stream and killing the rally?

It can take ten years to get a new mine started from scratch by the time you include capital rising, permits, infrastructure construction, logistics and bribes.

It turns out that the brightest prospects for new gold mines are all in some of the world's most inaccessible, inhospitable, and expensive places.

Good luck recruiting for the Congo!

That's the great thing about commodities. You can't just turn on a printing press and create more, as you can with stocks and bonds.

Take all the gold mined in human history, from the time of the ancient pharaohs to today, and it could comprise a cube 63 feet on a side.

That includes the one-kilo ($38,720) Nazi gold bars with stamped German eagles upon them which I saw in Swiss bank vaults during the 1980's when I was a bank director there.

In short, there is not a lot to spread around.

The long-term argument in favor of gold never really went away.

That involves emerging nation central banks, especially those in China and India, raising gold bullion holdings to western levels. That would require them to purchase several thousand tonnes of the yellow metal!

Venezuela has also been a huge gold seller to head off an economic collapse, thanks to the disastrous domestic policies there.

When this selling abates, it also could well shatter the ceiling for the yellow metal.

Tally ho!

Global Market Comments

October 1, 2018

Fiat Lux

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD,

or DON’T NOMINATE ME!),

(AMZN), (NVDA), (AAPL), (MSFT), (GLD), (ABX), (GOLD),

(JOIN US AT THE MAD HEDGE LAKE TAHOE, NEVADA,

CONFERENCE, OCTOBER 26-27, 2018)

I have a request for all of you readers. Please do not nominate me for justice of the Supreme Court.

I have no doubt that I could handle the legal load. A $17 copy of Litigation for Dummies from Amazon would take care of that.

I just don’t think I could get through the approval process. There isn’t a room on Capitol Hill big enough to house all the people who have issues with my high school background.

In 1968, I ran away from home, hitchhiked across the Sahara Desert, was captured by the Russian Army when they invaded Czechoslovakia, and had my front teeth knocked out by a flying cobblestone during a riot in Paris. I pray what went on in Sweden never sees the light of day.

So, I’m afraid you’ll have to look elsewhere to fill a seat in the highest court in the land. Good luck with that.

The most conspicuous market action of the week took place when several broker upgrades of major technology stocks. Amazon (AMZN) was targeted for $2,525, NVIDIA (NVDA) was valued at $400, and JP Morgan, always late to the game (it’s the second mouse that gets the cheese), predicted Apple (AAPL) would hit a lofty $270.

That would make Steve Jobs’ creation worth an eye-popping $1.3 trillion.

The Mad Hedge Market Timing Index dove down to a two-month low at 46. That was enough to prompt me to jump back into the market with a few cautious longs in Amazon and Microsoft (MSFT). The fourth quarter is now upon us and the chase for performance is on. Big, safe tech stocks could well rally well into 2019.

Facebook (FB) announced a major security breach affecting 50 million accounts and the shares tanked by $5. That prompted some to recommend a name change to “Faceplant.”

The economic data is definitely moving from universally strong to mixed, with auto and home sales falling off a cliff. Those are big chunks of the economy that are missing in action. If you’re looking for another reason to lose sleep, oil prices hit a four-year high, topping $80 in Europe.

The trade wars are taking specific bites out of sections of the economy, helping some and damaging others. Expect to pay a lot more for Christmas, and farmers are going to end up with a handful of rotten soybeans in their stockings.

Barrick Gold (ABX) took over Randgold (GOLD) to create the world’s largest gold company. Such activity usually marks long-term bottoms, which has me looking at call spreads in the barbarous relic once again.

With inflation just over the horizon and commodities in general coming out of a six-year bear market, that may not be such a bad idea. Copper (FCX) saw its biggest up day in two years.

The midterms are mercifully only 29 trading days away, and their removal opens the way for a major rally in stocks. It makes no difference who wins. The mere elimination of the uncertainty is worth at least 10% in stock appreciation over the next year.

At this point, the most likely outcome is a gridlocked Congress, with the Republicans holding only two of California’s 52 House seats. And stock markets absolutely LOVE a gridlocked Congress.

Also helping is that company share buybacks are booming, hitting $189 billion in Q2, up 60% YOY, the most in history. At this rate the stock market will completely disappear in 20 years.

On Wednesday, we got our long-expected 25 basis-point interest rate rise from the Federal Reserve. Three more Fed rate hikes are promised in 2019, after a coming December hike, which will take overnight rates up to 3.00% to 3.25%. Wealth is about to transfer from borrowers to savers in a major way.

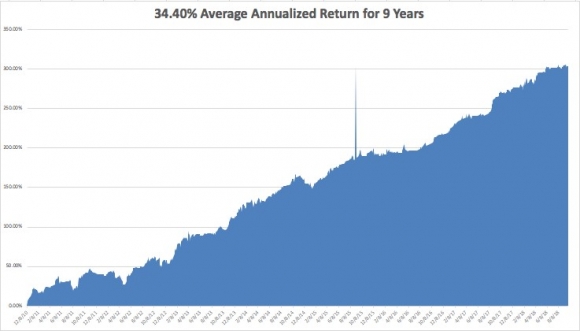

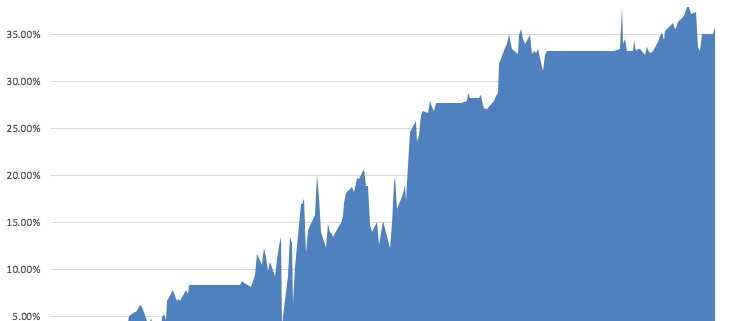

The performance of the Mad Hedge Fund Trader Alert Service eked out a 0.81% return in the final days of September. My 2018 year-to-date performance has retreated to 27.82%, and my trailing one-year return stands at 35.84%.

My nine-year return appreciated to 304.29%. The average annualized return stands at 34.40%. I hope you all feel like you’re getting your money’s worth.

This coming week will bring the jobspalooza on the data front.

On Monday, October 1, at 9:45 AM, we learn the August PMI Manufacturing Survey.

On Tuesday, October 2, nothing of note takes place.

On Wednesday October 3 at 8:15 AM, the first of the big three jobs numbers is out with the ADP Employment Report of private sector hiring. At 10:00 AM, the August PMI Services is published.

Thursday, October 4 leads with the Weekly Jobless Claims at 8:30 AM EST, which rose 13,000 last week to 214,000. At 10:00 AM, September Factory Orders is released.

On Friday, October 5, at 8:30 AM, we learn the September Nonfarm Payroll Report. The Baker Hughes Rig Count is announced at 1:00 PM EST.

As for me, it’s fire season now, and that can only mean one thing: 1,000 goats have appeared in my front yard.

The country hires them every year to eat the wild grass on the hillside leading up to my house. Five days later there is no grass left, but a mountain of goat poop and a much lesser chance that a wildfire will burn down my house.

Ah, the pleasures of owning a home in California!

Good luck and good trading.