Global Market Comments

April 8, 2022

Fiat Lux

Featured Trade:

(WEDNESDAY, JUNE 29, 2022 LONDON STRATEGY LUNCHEON)

(APRIL 6 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (TSLA), (TLT), (TBT), (AAPL), (IBB), (GOOGL), (ADBE), (NVDA), (FXE), ($BTCUSD)

Global Market Comments

April 8, 2022

Fiat Lux

Featured Trade:

(WEDNESDAY, JUNE 29, 2022 LONDON STRATEGY LUNCHEON)

(APRIL 6 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (TSLA), (TLT), (TBT), (AAPL), (IBB), (GOOGL), (ADBE), (NVDA), (FXE), ($BTCUSD)

Below please find subscribers’ Q&A for the April 6 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley.

Q: The iShares Biotechnology ETF (IBB) is down quite a bit—do I wait a bit longer to put on a debit call spread LEAPS for the end of this year and possibly the end of 2024?

A: This is really one of the two most interesting parts of the market right now. The biotech stocks have been absolutely destroyed over the past year—down 70, 80, 90% in some cases; and at that level, the worst-case scenario is in the price. Maybe we bounce along the bottom for another year. In the best case, these things all double or triple or even go up 10 times. We’re very close to putting on a 2024 call spread in the best biotech names, and if you get the Mad Hedge Biotech Letter (Click here for the link), you already know what they are because the downside risk on these things is getting close to nil, and the upside is 10 times. I like that kind of math—when the upside versus the downside is 10 to 1 in your favor. When I see specific LEAPS opportunities, I’ll send them out to you, but the answer is: not yet. We’re getting very close on biotech, however.

Q: I sold about a third of my ProShares UltraShort 20+ Year Treasury (TBT) position at $22.00 for a nice 40% gain, thank you very much. Should I hold the rest for a while? And is there a significant upside for 2022?

A: I’ve been telling everyone: hold those shorts. I know those of you who put on the December $150-$155 vertical bear put spread or the December $145-$150 vertical bear put spread already have substantial profits, but the time value on these options is still large, so there is still quite a lot of these profits to be made hanging on to all of your put spreads in the ProShares UltraShort 20+ Year Treasury Bond ETF (TLT). And is there a substantial downside from here? I think yes! If the Fed goes to a half-point rate hike schedule for the next 4 meetings, the (TLT) is absolutely going down to a $105 or $110 level or so. So, keep those shorts and add to shorts on rallies. We came close. I said sell on a $6 point rally and we got a $5 point rally. I didn't pull the trigger, and of course, now we’re here at new lows.

Q: Are we close to buying LEAPS in tech?

A: Yes, I think that once this current meltdown finishes, I want to go back in there. But I want to go long-dated.

Q: What does rapid unwind of the Fed balance sheet mean for the markets?

A: It’s terrible! The Fed has a balance sheet close to $9 trillion dollars. Before the financial crisis of ‘07, it was $800 million dollars, and in fact, in the last 4 years, it has gone up from $20 trillion to $30 trillion. So these are just bubblicious levels for the Fed to own. And what is QT or quantitative tightening? They sell those bonds. And of course, everyone knows they’re going to sell, so they’re dropping bids for bonds like crazy right now—that's why you’re getting the meltdown in the (TLT). This is bad for the stock market; there’s no world in which the stock market goes up with sharply rising interest rates. The best case is that you give up 20% and then make some of it back, and then give up 20% and then make some of it back. So yeah, expect to hear a lot about QT. We only ended QE or quantitative easing about 3 weeks ago, and it looks like we may go straight into QT as soon as May. And boy, the bond market is sure reflecting that today.

Q: How long will wage inflation last? Can I count on 10% pay increases forever?

A: No, it will last until the next recession. I have a feeling that the unemployment rate will hit all-time lows next month—probably 3.2% or 3.3%. And we’re essentially at a full employment economy right now. What happens next? Recession probably in one or two years. Then those wage hikes disappear completely, and people start getting laid off, and goodbye to inflation of all kinds since 60% or 70% of the inflation calculation is wage cost.

Q: What is a good age to retire?

A: Never. I can’t tell you how many friends I’ve had who retire and die within a year. I had one friend retire and he died the next day. What you could do is keep your old job and cut your hours by half, or you could retire from your old job to go on to a new job that you love, like opening a restaurant or a job built around your lifetime hobby, whatever that is. As long as you stay engaged, you keep Alzheimer’s at bay and you’re an active contributing person to society. As soon as you stop doing that and just start doing something like golf, your days are numbered.

Q: What factors will create a recession in 2022?

A: Well I don't think that's going to happen; that would be like multiple 1% rate rises by the Fed, and the Fed completely panicking like we said, and causing a premature recession. But I do think that by 2024 rates will be so high that we will get a recession, probably a short one, maybe 6 months. A lot also depends on the war and if Europe can replace their Russian gas/oil fast enough or they go into an oil shock and recession there.

Q: Will the Fed destroy the economy in order to save it?

A: Yes, they will, if we get inflation up into the teens, which we saw in the 1980s, they absolutely will raise rates. And then I think the 10-year made it to 12% in the early 80s when Volcker was around, and the overnight rate got to 18%. And I know that because I bought a coop in New York City with a mortgage rate of 18%. I took out one of the first floating rate mortgages and by the time I sold the house, the mortgage rate had dropped down to 11% and the value of the home had doubled.

Q: Google (GOOG), Adobe (ADBE), and Apple (AAPL) spreads are treading water.

A: That is a sign that these are the stocks that will lead the next recovery. So, only 20% down, top to bottom, in Apple while all other stocks were getting hammered for 40% or more means Apple is going to lead any recovery in the market. Watch these big tech stocks carefully—they are the new leaders, they just don’t know it yet.

Q: What will inflation do to the housing market? Should I sell or hold my investment properties?

A: Keep them. Housing is one of the biggest beneficiaries of inflation. Not only do the house prices go up, so does everything that goes into the house, like the copper, steel, lumber, kitchen appliances, etc. You really have the best play on inflation, and I don’t think interest rates will kill the housing market. I think all that will happen is people will move from 30-year fixed to 5-year adjustables, as they have done in previous high interest rate cycles.

Q: Where is the buy territory on the Mad Hedge Market Timing Index?

A: Below 20. It’s almost impossible to lose money when you buy at a market timing index of 20. You may get a day or two visit down into the teens, but if you hang on, that’ll become a big moneymaker for you. That’s been working for me for 50 years—it should work for you too.

Q: Do the chips and transports breaking down worry you about the general market?

A: No, I think they’re discounting a recession that isn’t going to happen. Remember half of all the recessions discounted in the market don’t actually happen, and I think that these are one of those non-recessionary selloffs. But it may take them a couple of months to figure out that this bull market still has a couple of years of life to it and that it’s too early to sell. By the way, once people realize that they discounted the recession too early, what are they going to pour back into the fastest? The semiconductor stocks. That's why I’ve got a laser focus on NVIDIA (NVDA).

Q: If there is no recession coming, are the retailers getting too oversold?

A: Yes, but in the world that’s out there, where you really only want to own two or three of the best sectors and avoid the other 97, retailers are the ones you want to avoid—unless there's some specific single company story that you know about.

Q: Housing prices can’t fall when there's such enormous demand coming from millennials, right?

A: That’s true. In fact, the number of houses that need to be built to meet this demand is anywhere from one to five million, so this is a shortfall that will take at least a decade to address, and house prices don’t fall in that situation. They may appreciate at a slower rate, but they will appreciate, nonetheless.

Q: Is there any level where you would consider a call spread in the TLT?

A: Well, I had the April $127-$130 vertical bull call spread and I had my head handed to me. So somewhere, but clearly not yet—again, it depends a lot on what the Fed does and how fast.

Q: What’s the outlook for the Euro (FXE), (NVDA)?

A: Lower. Until the Ukraine War ends, they get an economic recovery, and they wean themselves off of Russian energy and move over to American energy. And that's at least a year down the road, so I’m not rushing into any European investment—stocks, bonds, or currencies.

Q: Are rising interest rates good for banks?

A: Yes, but right now those benefits are being offset by recession fears which will probably go away in a couple of months. So that kind of makes banks a strong buy right here.

Q: When the Shanghai lockdown ends, will it create another surge in commodity prices?

A: Absolutely, yes. China is the world's largest consumer of commodities, and the restoration of any of their purchasing power will certainly be great for all commodity prices—food, energy, metals, you name it.

Q: Is Tesla (TSLA) a LEAPS candidate?

A: Yes but wait for it to take a run at the $700 low that we saw last month. We probably won’t get there, but $800 this time around is probably a great LEAPS candidate for Tesla going forward. I expect them to meet all of their goals for production this year.

Q: Won’t Bitcoin ($BTCUSD) keep falling if equity markets are lower?

A: Yes, but we don’t have that much lower to go in equity markets—maybe 10%. So just as we’re looking to buy equities and the smaller technology stocks on dips, we're also looking to buy Bitcoin on dips. If we can get back into the $30,000 handle, that might be a ripe buy territory for all the cryptocurrency plays.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

April 1, 2022

Fiat Lux

Featured Trade:

(THE CREATIVE CLOUD IS OVERSOLD)

(ADBE), (AAPL), (GOOGL)

Creative software giant Adobe (ADBE) has ironclad support at $440 on a technical basis and I am willing to go on a 13-day excursion with the underlying stock.

That being said, the macroeconomic picture leaves a lot to be desired and one could literally say that 100 times.

Many of the risks have yet to be unlocked if one rolls through the list of them like hyperinflation, spiking energy costs, the military conflict, rising rates, poor global government, and the list really could be added to for infinity at this point.

No need to beat a dead horse.

However, this breathtaking relief rally has turned into something that is probably more than just a relief rally and has told us investors one thing.

There is still way too much liquidity in the system and it’s still sloshing around.

And although I missed the bottom of the relief rally, I seek to benefit off the next stage of it with ADBE and GOOGL which are two highly sought-after tech stocks with a proven track record and whose technical picture looks positive in the short-term.

The cheat sheet for this exam is Apple (AAPL) whose bounce from $150 to $180 really summed up what’s going on in the tech ecosystem.

The best of breed is harvesting the bulk of the gains, and instead of fighting it from the other side, I’ll just traverse on the side of Apple and ride it up with them.

The dip-buying has been almost violent in this rally and although I do believe there will be some reduction in the pace of the up moves, it’s almost impossible to go completely bearish against tech right now.

Another key insight into recent stock movement is that the nominal size of the stock market at this point is so gigantic in terms of market cap that the leverage inside of it is causing volatility to go nuts.

I don’t think this will resolve itself in the near future and this sets the stage for some series of epic up moves moving forward to the second half of the year as a large swath of negativity has been priced into the news.

Tech could go back to its overshooting the rest of the market narrative and names like ADBE and GOOGL will perform splendidly with this type of boost.

Let’s get into the weeds and explain why I really do like ADBE as a standalone company?

The massive slide over the past few months was nothing structural. ADBE posted market-beating earnings for the first quarter, growing cloud revenue, one of the biggest markets in the tech world, to more than $2 billion. The firm has also been steadily shot up the digital subscription revenue ladder.

Yes, their product lines are slowing but they are at the cutting edge of digital innovation which with its terrific brand has great pricing power.

ADBE has transformed itself into a software behemoth, more than tripling its revenue since 2010. The company is famous for its namesake PDF-reader and photo-editing software Photoshop.

However, ADBE’s bread and butter is a full suite of software products monetized through a recurring subscription model.

ADBE transitioned from selling boxed software to recurring subscriptions in 2013 and revenues have gone parabolic since.

Readers must be practical at this point and not focus attention on the low end of tech.

Tightening conditions in the capital markets mean that there will be less resources to throw at the poor-quality tech names.

Practicality should be the foot forward with readers piling into the best of tech like APPL, AMZN, GOOGL, ADBE, and MSFT.

Don’t get too cute here.

Traders never go bankrupt from taking a profit.

Mad Hedge Technology Letter

February 11, 2022

Fiat Lux

Featured Trade:

(THE GROWING CLOUT OF TWILIO)

(TWLO), (ADBE), (CRM), (GOOGL), (AAPL)

Twilio (TWLO) cranked the ball out of the ballpark in its latest quarterly performance.

For a company that’s been burning cash for years, such as 2021’s performance of negative $950 million, analysts expected another few years of losses.

That’s not the only loss, the years before were saddled with unprofitable times like the $490 million burnt in 2020 and they still haven’t recorded a single profitable year yet.

So for Chief Executive Officer of Twilio Jeff Lawson to tell us that he expects Twilio to be profitable in 2023 is a gamechanger.

This guy has elevated Twilio to the dominant provider of business-to-consumer communications tools, powering messages such as the Uber notification you receive after ordering a ride, into an estimated $79 billion market for software to help optimize customer experiences.

Busting out the “P word” when many analysts were expecting to count the losses is a big deal for growth tech and TWLO can expect a new breed of institutional investors to enter the fold because of their positive signaling.

It’s not only them.

They have been tactical in a series of aggressive moves adding new companies to their core like Segment.

Segment, the customer data platform provider that Twilio purchased in 2020 for $3.2 billion is one of the reasons why the juice might be worth the squeeze.

It was the company’s biggest acquisition to date and the most-watched by investors.

The integration of Segment is expected to enhance the bulk of Twilio’s product portfolio.

It effectively functions as a repository of continually updated first-party customer information that businesses can use to improve marketing and support, with the goal of fostering loyalty and higher sales.

The timing of the deal was critical given Apple’s (AAPL) stricter data treatment and Google’s (GOOGL) narrowing of its web-tracking software.

At the same time, the acquisition of Segment nudged Twilio towards the direction of competing with Silicon Valley stalwarts like Salesforce (CRM) and Adobe (ADBE).

A key difference between Twilio and its rivals is the ability for developers within businesses to conveniently build customized programs on top of the company’s base tools.

Not only did management indicate that profitability is arriving next year, but they signaled strong revenue growth of over 30% for the next three years.

Easily said, TWLO is morphing into an indestructible force that is harnessing soon-to-be profitability, growth, and future success all wrapped into one company.

In this era, it’s hard to get all broad strategies working simultaneously because most tech firms will sacrifice profits for growth.

On top of that, management shared that they fully expect gross margins to surpass 60% in the long-term translating into a highly profitable company.

That’s the beauty of the software as a service (SaaS) model, the scalability works well inside the financial parameters which is why companies like Adobe and Salesforce bust out such great metrics.

Three other acquisitions Lawson believes will make a difference are Engage for the marketer, which is still very early in its cycle, most recently, a software called Frontline, which can be used by frontline workers and even sales teams to be more efficient, and lastly, Flex for the contact center.

All indications show this is nowhere near a “pandemic stock” and the fourth-quarter revenue jumping to 54% to $842.7 million while guiding for $865 million next quarter validates that.

This communication as a software company is sticky as can be and has a valid use case in many different apps that need to link the back-end interfaces with customer functionality.

TWLO will move from strength to strength going forward and this software company has a real chance to make its mark as not just a company considered second tier, but even a flight to safety type of tech stock which are few and far between.

The stock is still highly volatile which makes it easy to add on the big dips, but readers should avoid the small dips.

I am bullish TWLO.

Mad Hedge Technology Letter

December 6, 2021

Fiat Lux

Featured Trade:

(THE HAWKS ARE HERE)

(ROKU), (ZM), (TWLO), (SNAP), (SQ), (MSFT), (CRM), (ADBE)

Higher inflation is something this tech bull cycle hasn’t dealt with, and it’s starting to rear its ugly head in the form of volatility and spades of it.

The Fed will have to increase interest rates or face runaway inflation that will crash the economy, but increasing interest rates will also make lives harder for tech companies.

As we try to understand the pace of interest hikes, certain tech companies will fare much better in this inflationary environment than others. To deduce the winners from the losers, investors should understand exactly how inflation affects each particular tech company.

Talk has gone from the Fed moving early to raise short-term rates, to the Fed moving even in early spring which in turn is spooking risk markets from cryptocurrencies, the S&P, and the Nasdaq.

Fed Chair Jerome Fed has done a poor job communicating his sudden hawkish tone and the market has had to quickly reprice risk assets because of the surprising nature of the hawkishness.

In the short-term, tech stocks will need some time to digest this new expectation, which I see as quite healthy, but short-term tough to swallow.

Fed Cleveland President Loretta Mester told the media she is “very open” to scaling back the Fed’s asset purchases at a faster pace so it can raise interest rates a couple of times next year if needed so this isn’t just one guy in Powell trying to move the needle.

Clearly, the Fed is moving in unison, and they threaten to become a major force in moving markets which is all we care about.

All that pressure is causing component and labor costs to rise. Companies that don't have enough pricing power to pass those costs on to their customers will likely see their gross and operating margins shrink.

This matters because tech companies offer some of the most generous salaries in the U.S. and substantial increases in pay hurts them the most.

Higher interest rates attract more consumers and businesses to put more money in higher-yield bonds and savings accounts.

There are 3 ways that higher rates are actually a gut punch to tech growth companies.

First, they increase the costs of borrowing incremental capital to expand a business. In more cases than not, tech growth companies rely on borrowed money because their operation is not yet sustainably profitable. That's bad news for high-growth tech companies, which are burning cash with widening losses.

Second, it reduces the long-term estimates for a company's earnings and free cash flow (FCF) growth meaning their underlying stock price is rerated downwards in the anticipation of this new reality.

Loss accruing tech companies commonly suffer an exodus as their underlying shares are repriced to reflect higher costs.

Just this morning we saw Roku (ROKU), Zoom Video Communications (ZM), Snap (SNAP), Twilio (TWLO), Square (SQ) breach 52-week lows.

The breadth of the market has been hollowed and the goalposts have indeed narrowed because of the hawkish tone at the Fed.

Lastly, higher interest rates drive institutional money into fixed income.

They do this largely by taking profits from crypto, tech stocks, or moving their stash on the sidelines then resurfacing the money into “safer” assets that anticipate weakening bond yields at the longer end of the curve.

So I won’t sit here and say sell all and every tech stock, it’s more nuanced than that.

I executed one position in December and that was Microsoft (MSFT) and it got pulled down with the broader market.

More importantly, I didn’t bet the ranch.

Ultimately, we still bask in the ideology that the tech bull market isn’t over yet because it isn’t, but this aggressiveness out of the blue has forced the overall tech market to temporarily rest with growth tech suffering major drawdowns.

In doing that, the ceiling for a Santa Claus rally is somewhat capped to the upside.

The Fed could have waited until January.

Sure, there will still be winners in tech and the odds of these winners are driven firmly behind the biggest and best like Microsoft, Amazon, Google, and Apple.

These are the type of companies that have the pricing power to raise prices and get away with it because consumers will be willing to pay it.

Other potential winners include cloud service giants like Salesforce (CRM) and Adobe (ADBE). These again are top-quality software stocks that can pass up higher enterprise software costs to the firms that can pay for it.

It’s entirely possible that the Fed could end up walking back some of these aggressive stances in the interest-raising process next year.

Don’t fight the Fed and don’t expect tech growth stocks to reverse until we receive more clarity with interest rate policy, if a reverse is triggered, it will play out with Apple, Amazon, Google, and Facebook, and Microsoft leading the way higher.

Mad Hedge Technology Letter

October 6, 2021

Fiat Lux

Featured Trade:

(GEMS TO SCOOP UP ON THE CHEAP)

(ADBE)

I know everyone's gotten into a tizzy because of tech stocks falling off the proverbial cliff.

It won’t always be like this.

Tech stocks won’t plunge this dramatically simply because their growth stories are mainly intact.

External events sometimes do this to our sector, and we must brace for the impact, but readers should look forward to a rosier future.

That is why readers must start to plan for which stocks to scoop up on the cheap after the selling subsides.

One ironclad name that readers must dip into is software company Adobe (ADBE).

This stock has been historically hard to find entry points and we are on the way to getting an optimal one.

Creativity has always played a central role in the human experience.

Over the last year, we have all witnessed the way creativity has sustained us.

We've shared photographs with loved ones on different continents, taught art classes to students at their kitchen tables, and launched entirely new businesses online.

Building on decades of leadership, Adobe continues to pave the way in core creative categories, including digital photography and design, while pushing the boundaries across a wide range of emerging categories such as AR and 3D.

Whether it's the latest binge-worthy streaming plus series, a social media video that sparks a movement, or a corporate video, creation and consumption of video is experiencing explosive growth while Adobe is core to these businesses.

In August, they announced an agreement to acquire Frame.io, a leading cloud-based video collaboration platform. Video editing is rarely a solo activity and it's traditionally been highly inefficient. Frame.io streamlines the video production process by enabling editors and key project stakeholders to seamlessly collaborate using cloud-first workflows.

In the digital economy, companies are relying on digital presence and commerce as the dominant channels to drive business growth.

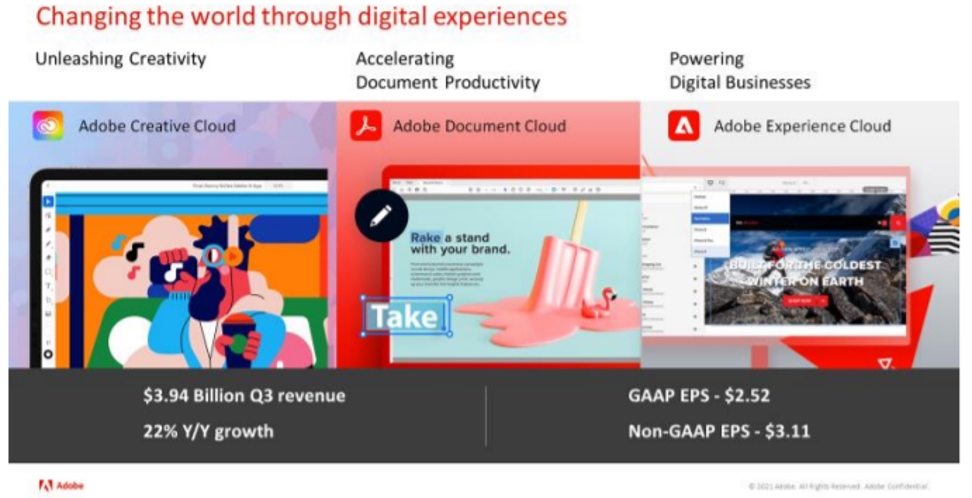

According to the Adobe Digital Economy Index, U.S. consumers spent over $541 billion in e-commerce from January through August, 58% more than what we saw two years ago.

As a result, in Q3, Adobe achieved record revenue of $3.94 billion, which represents 22% year-over-year growth.

The company isn’t just performing in terms of raw revenue, but the 3-Year EPS Growth Rate has stayed in the mid-20% and snowballing in terms of dollars accumulated.

Just to validate what I just said, in 2017, annual earnings were $1.7 billion and fast forward to 2020 and earnings surged to $5.26 billion.

Adobe’s consistency is also the talk of the town with their 3-year revenue growth rate in the mid-20%.

Adobe is really at the sweet spot of their earnings profile, and I can easily see this company growing from a $270 billion market cap today into half a trillion-dollar stock within 4 years with earnings of $8 billion per year.

Naturally, the bread and butter to Adobe is the small and medium-sized businesses (SMB).

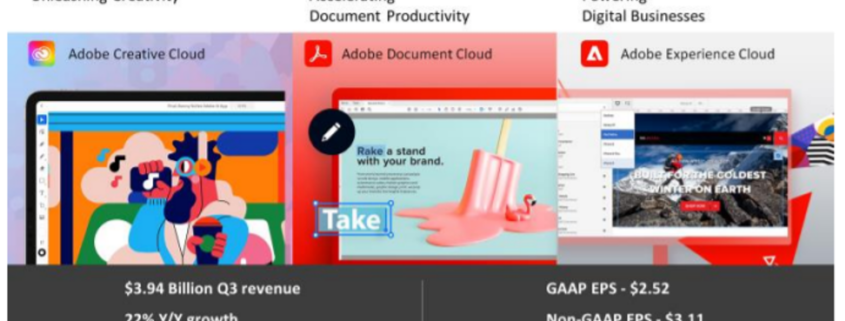

The SMB’s scoop-up products like imaging and video continue to do well — the Acrobat business, which is reflected both in the Creative Cloud and the Document Cloud, is doing well.

Net-net, I would say that the growth prospects for these particular businesses are running smoothly as can be and this is how positive the feedback is from these creative products.

At the end of the day, I think the macro trend that everybody is finding is that a digital presence in commerce, data and insights, and analytics is an x-factor now for anybody doing business.

The behavioral data that Adobe collects in real-time for the productivity division correlates with the marketing message associated with telling creators that they really need to focus on getting their first-party data to be an asset.

Then you add that to the creative products and wow — what a stellar company.

These are seminal trends Adobe is flying on the coattails of, and the robustness of Adobe’s tools significantly differentiates itself relative to competition.

I am bullish Adobe in the long term.