Mad Hedge Technology Letter

November 20, 2019

Fiat Lux

Featured Trade:

(MY CURRENT TECHNOLOGY TRADING STRATEGY),

(GOOGL), (MSFT), (APPL), (ADBE), (AKAM), (VEEV), (FTNT), (WKDAY), (TTD)

Mad Hedge Technology Letter

November 20, 2019

Fiat Lux

Featured Trade:

(MY CURRENT TECHNOLOGY TRADING STRATEGY),

(GOOGL), (MSFT), (APPL), (ADBE), (AKAM), (VEEV), (FTNT), (WKDAY), (TTD)

Some might say that we were due for a revaluation of growth tech stocks.

They have contributed greatly in this nine-year bull market.

Profit-generating software stocks are the order of the day.

Tech has led the overall market higher after projected quarterly earnings growth of -9% came in better than expected at -5%.

We have ebbed and flowed from pricing in a full-out recession in mid-2020 to now believing a recession is further off than first thought.

The pendulum swing ruptured many growth stocks from Workday (WKDAY) to The Trade Desk, Inc. (TTD) plummeting 30%.

We have retraced some of those losses but momentum in share appreciation has shifted to the perceived safer variation of tech stocks.

Investors have cut volatility and headed into bulletproof companies of Apple (AAPL), Google (GOOGL), and Microsoft (MSFT).

These companies have significant competitive advantages, Teflon balance sheets, and print money.

The tech markets just about priced in the U.S - China trade war in the fall as broad-based volatility plummeted because of optimism around making a deal.

This, in turn, has boosted chips stocks along with investors front running the 5G revolution and the administration granting Huawei a reprieve was a cherry on top.

The Mad Hedge Technology Letter has taken every dip to initiate new longs in safe trades like software companies Adobe (ADBE) and Veeva Systems (VEEV).

Tech is at the point that all loss-making companies are out of the running for tech alerts because the moment there is a recession scare, these shares drop 10% and often don’t stop until they lose 30%.

Now there is a deeply embedded set of narrow tech leadership by a few dominant tech companies buttressed by a select set of second-tier software stocks.

I would put PayPal (PYPL) and Twitter (TWTR), which I currently have open trades on, in the ranks of the second tier and they should do well as long as economic growth does better than expected.

Their share prices dipped on weak guidance and the bad news appears to have been shaken out of these names.

Professional investors could also be hanging on to meet end-of-year performance targets.

I do expect unique entry points on software stocks that drop after bad future guidance.

Profitability has moved to the fore as the biggest factor in holding a name or not.

Newly minted IPOs have fared even worse showing the markets' waning appetite for loss makers like Uber (UBER) and Lyft (LYFT).

Loss-making companies often tout their ability to change the world and disrupt industry, but that has been discovered as nothing more than a ruse.

They aren’t disrupting the way we change the world. For example, Uber is a dressed-up taxi service and the new CEO has failed to create any new momentum in the unit economics that spectacularly fail by any type of metric.

Even worse for these growth stocks, as the economy starts to falter, there will be even less appetite for them, and even more appetite for safer tech stocks.

A worst-case scenario would see Uber drop to $10 and Lyft to $20.

New all-time highs have crystalized with Google (GOOGL) under the gauntlet of regulation hysteria displaying the domination of these big tech machines.

The ongoing, consistent rotation out of growth and into value hasn’t run its course yet and fortunately, by identifying this important trend, our readers will be well placed to advantageously position themselves going into 2020.

Growth stocks won’t make a comeback anytime soon and deteriorating conditions could trigger renewed synchronized global monetary policy easing and central bank stimulus.

And yes, more negative rates.

I believe Oracle (ORCL), Fortinet (FTNT), Akamai Technologies, Inc. (AKAM) could weather the storm next year.

Tech growth is slowing and trade uncertainty is high, and readers must have a sense of urgency to avoid the losers in this scenario.

U.S. economic growth could slow to 1.3% next year, avoiding a recession, and the lack of enterprise spend will reduce software sales and combine that with peak smartphone growth and it won’t be smooth sailing.

The Mad Hedge Technology Letter has the pulse of the tech market and will show you how to navigate this minefield.

Global Market Comments

November 19, 2019

Fiat Lux

Featured Trade:

(BLACK FRIDAY DISCOUNT OFFER FOR THE MAD HEDGE TECHNOLOGY LETTER),

(ADBE), (EBAY), (PANW)

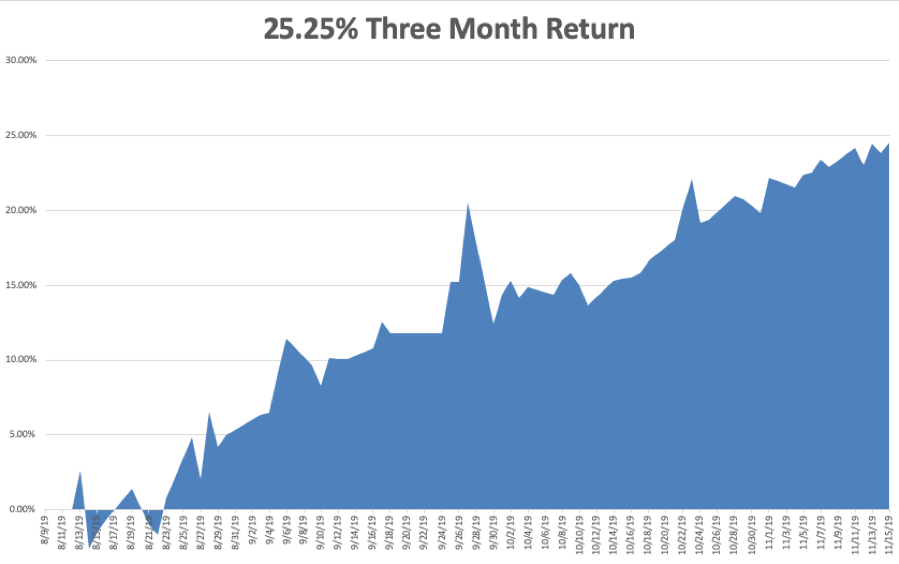

The Mad Hedge Technology Letter has been on an absolute tear lately.

It has posted an eye-popping 25.25% net profit since August. The last 14 consecutive trade alerts have been profitable, a success rate of 100%. Some 20 out of the last 22 trade alerts have been profitable, a success rate of 90.9%.

We nailed the 27.3% move in the multimedia software company, Adobe (ADBE). We killed the 23.28% pop in e-commerce leader eBay (EBAY). And we hit a total home run with a positively ballistic 30.42% gain in cybersecurity giant Palo Alto Networks (PANW).

And here’s the method to our madness. While no one was looking, the stock market has made a dramatic shift from buying in large-cap tech techs to smaller cap ones. In order words, we’ve moved from the FANGs to the mini FANG’s, and WE CAUGHT ALL OF IT!

Which brings me to the topic at hand. You absolutely HAVE to get in on this move, the most important of the year. And I’m going to make it incredibly easy for you to do so. For here at Mad Hedge Fund Trader, Black Friday comes early.

I am offering the Mad Hedge Technology Letter at an insanely bargain-basement price of $998. That is a full 61% discount to the $2,500 list price offered on our website.

I’m not doing this to make money. I am chopping prices so YOU can make money. And there is nothing I like better than happy, money-making customers. For focusing in on this one crucial sector will be the most important investment decision you make in your lifetime.

With the Mad Hedge Technology Letter, you will get:

*A three times weekly morning newsletter covering the most important technology stocks and trends of our time.

*Technology trade alerts sent out at market sweet spots telling when and where best to enter the market.

*Trade alerts sent out at market tops on where best to take profits or stop out of the rare losers.

*Invitations to biweekly Strategy Webinars with live Q&A.

*The best customer support in the industry with same day answers to all questions.

*Access to a searchable ten-year database of technology research.

*Invitations to Mad Hedge Strategy Luncheons around the world (the last one was in Zermatt, Switzerland).

In order to take advantage of this one time only offer, please click here.

Let me give you a warning. We are only accepting 25 orders at this deep discounted one-time offer so it’s a first-come, first-served basis.

I look forward to working with you.

John Thomas

CEO & Publisher

The Mad Hedge Technology Letter

Mad Hedge Technology Letter

June 24, 2019

Fiat Lux

Featured Trade:

(YOU COULD DO A LOT WORSE THAN ADOBE)

(ADBE)

The bull rally isn’t dead – that is the biggest takeaway from Adobe’s (ADBE) overperformance and recent earnings beat.

They will keep posting positive earnings results unless there is some type of seismic shift that deteriorates its competitive advantage.

The company continues to show no mercy by expanding revenue 25% year-over-year to $2.74 billion in the quarter just reported.

Adobe’s portfolio of solutions is the gold standard for creating and managing the world’s digital experiences through its apps and cloud products.

Software stocks are the optimal late cycle stocks and I have been whacking every bush in the outback to spread the message that instead of opting for hardware, software protects investors from many of the treacherous traps out there now.

But the most regenerative trends out there are many companies are bypassing or delaying, exorbitant capital projects like new chip factories or new hardware product lines because of the high-risk nature of the economy peaking, in place of fine-tuning processes that are directly correlated to higher software procurement.

This stock fits that procurement bill with millions of consumers dependent on critical apps like Adobe Photoshop and PDF for personal and professional endeavors.

I know I am!

A ceaseless pipeline of enterprises the world over is relying on Adobe every day to help them transform their businesses and the success is vividly showing up in the numbers.

The branding power and the continuous product innovation and services, the deep investment in technology platforms, and a robust ecosystem of partners are enabling Adobe to serve millions of customers swelling the top line.

The expanding addressable markets in the creativity, document, and customer experience management categories are an opportunity that has never been greater.

Adobe Creative revenue was $1.59 billion demonstrating 22% year-over-year growth.

Mobile is the main catalyst in the Digital Media space and Adobe is experiencing significant increases in mobile traffic and member sign-ups for Adobe’s offerings.

This is the gilded age of creativity, and the vision for the Creative Cloud is to be the creativity platform for all.

This has catapulted Adobe’s creative portfolio into must-have apps for professional content creators.

And we are just skimming the surface of how deeply creative content will penetrate into users' lives.

Whether you are a burgeoning student, an experienced designer, a commercial YouTuber, or a marketer, storytelling is the focal point to the way you communicate and connect.

The key part of the Creative Cloud growth strategy is appealing to new audience of users and Adobe is executing this tactic on all levels.

Adobe Spark, a product that easily turns ideas into compelling stories, graphics, and webpages, is swiftly gaining traction among creators from the classroom to the boardroom.

Spark traffic on web and mobile has more than doubled year-over-year.

They have enhanced their vision of platforms to include social media outlets like Facebook, Instagram, and YouTube.

Premiere Rush is rapidly becoming the solution of choice for YouTubers and social video creators. Premiere Rush is now available on Android in addition to iOS, Mac, and Windows.

When we boil down the nuts and bolts to find out the growth drivers, I am convinced about the upselling and retention of assets inciting new user growth driven by numerous global initiatives to generate demand, including targeted campaigns and promotions, leveraging the funnel of users coming to Creative Cloud through mobile apps and online engagement.

This helps continue focus on new categories including immersive media and new segments such as social media creators, Creative Cloud Photography plan subscriptions, Adobe Premiere Pro single app subscriptions in the video category, and Creative Cloud enterprise.

Adobe Stock is the fast-growing service for stock images, videos, and millions of additional creative assets grew greater than 25% year-over-year.

With Adobe Document Cloud, they are reimaging how consumers can scan, edit, collaborate, sign, and share documents in the cloud and mobile era.

Document Cloud revenue in Q2 was a record $296 million and they grew Document Cloud ARR to $921 million driven by continued strength in Acrobat subscription adoption.

Mobile is the next frontier for digital documents and our flagship apps.

Adobe Reader for mobile and Adobe Scan continue to metastasize in popularity.

Adobe Scan, which allows you to capture everything from documents to forms, whiteboard sketches or business cards, and turn them into picture-perfect, high-quality PDFs, is now the leading scanning app in iOS and Android.

Adobe Sign, the cloud-based electronic signature solution, is another winner with customers including Merck, Hitachi, and Iowa State University.

They are using Adobe Sign to provide optimal customer experience, close out deals, and win business.

The quality of the company’s apps is far-reaching with many firms turning away from Amazon and joining Adobe in droves.

The Digital Media ARR growth has been leveling down from 30%-plus range in the last couple of quarters, and investors have begun to be concerned about the long-term trajectory.

Adobe still possesses the potential for unit conversions internationally, but domestic sales will drive the business in the short term.

Even more attractive, the company is insulated from the China ruckus.

The company is one of my favorite software stocks and is part of an exclusive club of 5-7 software stocks that are part of my long-term must-buys.

This is an effective bet on the expansion and continuous development of the digital content industry.

Even if certain formats were to blow up like a Facebook, content will evolve into some other form and Adobe will be on top of the game attempting to deliver a first rate of tools to support these new operations.

Adobe is a core enterprise stock and most businesses from big to small pay for one of their services, for example, the bare minimum is likely to result in a company paying for Adobe’s PDF viewer to capture the best method of handling PDFs.

Adobe simply does a great job of providing and supporting creative software applications to drive productivity.

And I love that this company isn’t reliant on any one tool to drive profits, being a one-trick pony in this climate has forced other companies to seriously overreach in risk and addressable market.

Wait for shares to come down for $300, traders will need a better entry point as shares have bolted from the barn door.

Mad Hedge Technology Letter

June 13, 2019

Fiat Lux

Featured Trade:

(THE TRADE WAR MOVES DOWN MARKET)

(DOCU), (PSTG), (ZUO), (MSFT), (PYPL), (ADBE)

To understand the consequences of the global trade war, just take a look at the second-tier software companies.

There has been softness in the latest earnings reports and guidance signaling a lukewarm upcoming summer.

The best-case scenario is the likes of DocuSign (DOCU) and Zuora (ZUO) rallying into the end of the year.

That is hardly a given considering the global turmoil has shifted supply chains in every which way as well as denting overall demand.

Cloud-based companies have seen meaningful weakness this earnings season, even some of them absorbing heavy losses in the wake of their quarterly results, but analysts aren’t ready to write off this industry yet.

Referencing the latest industry survey, 20 software companies reported results in the last month, and of those, only six saw a positive response in their stock prices.

DocuSign and Pure Storage (PSTG) were among names that got clobbered, along with cloud-computing plays like Cloudera Inc., Nutanix Inc., Box Inc., and Pivotal Software Inc.

The current malaise in software is due to higher valuations and macroeconomic issues which subsequently elevates uncertainty.

There is no reason to go hysterical over this, and in no way, shape, or form, does this signal an imminent implosion of cloud companies, any incremental caution may be reversible if macro indicators and sentiment rebound.

And this rebound can be swift once all the stars align together.

Adding to the comfort is that some of the sharp drawdowns were company-specific reasons.

MongoDB Inc. or Zscaler Inc., were coming off strong year-to-date advances in their shares and it was time to take profits before the next upward explosion.

Cybersecurity company Zscaler, is appropriately accounting for outperformance and have already been crushing higher than normal expectations.

DocuSign eclipsed expectations on some metrics but disappointed on others, such as billings growth.

This disappointing miss punished the company with a drop of 15% in the pre-market session, as DocuSign grew sales by 27%, a lower rate than in previous quarters.

Management blamed the poor performance to an elongated sales cycle.

Bulls were hoping for a beat-and-raise quarter and instead got in-line numbers with some soft spots around the periphery.

Investors aren’t in a charitable mood and the sensitive mood around geopolitics has made investors more agitated with a shorter leash.

There was a tone of a broader deceleration in software demand prompting stronger names to get comingled together, but the bulk of this negative price action has been overdone.

Even further down the pecking order, results from smaller cloud firms have pointed to more fundamental issues, and these stocks have emerged as a particularly weak sub-sector.

A number of these companies reigned in their forecasts, a trend that has buttressed analyst caution over the group.

Considering that many companies have labored and there exist clear narrative similarities, it’s hard not to surmise that some real systemic pains in infrastructure exist.

Many in the industry are acutely aware of the growing chorus of companies blaming competition or poor sales execution.

Lower growth rates are effectively the predominant reason for lower stock prices in this group of cloud companies.

On the flipside of this weaker cloud growth are the heavy hitters who are throwing around their weight getting through largely unscathed.

If any of these bigger cloud companies can fuse together a business model with no China exposure, then shares are likely stable to upward trending.

A company like Adobe (ADBE) is a perfect company to look at with an unpretentious yet steady growth rate and wildly successful products.

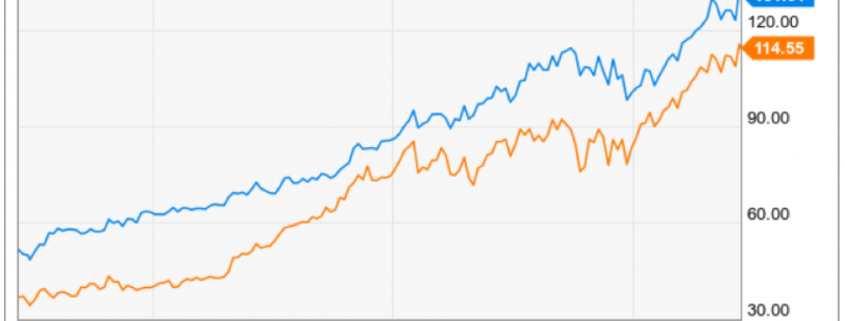

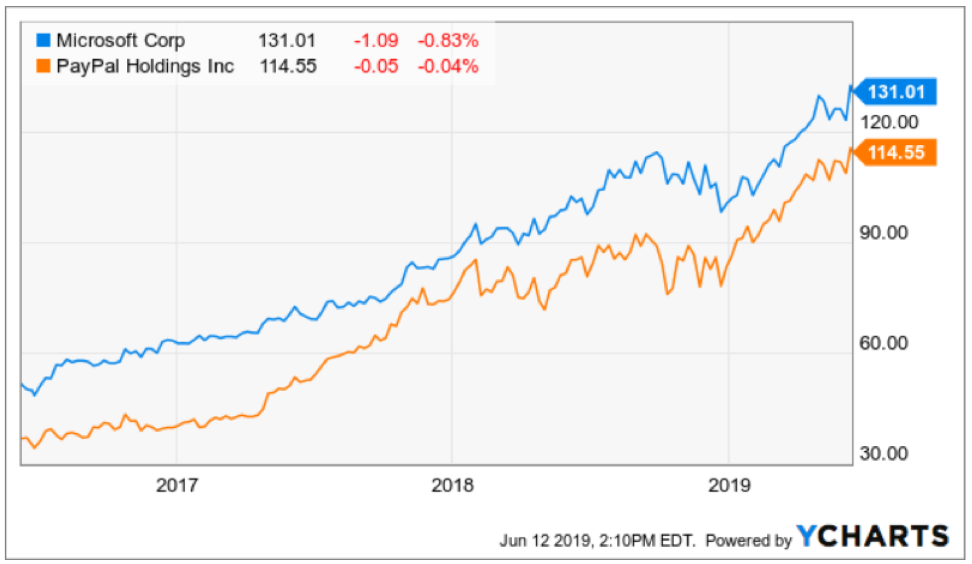

If we were to look at more growth-based companies with larger scale, then PayPal (PYPL) and Microsoft (MSFT) epitomize the type of cloud companies that are thriving in this environment and if geopolitics subsides, take on another 10% in sales.

Not only is the weather hot in the summer, but the anti-trust regulators are turning up the heat on certain tech companies on anti-trust concerns.

This could be a time to wait out those stocks and there could be another move to the upside if regulation is weaker than expected.

Global Market Comments

May 17, 2019

Fiat Lux

Featured Trade:

(APRIL 15 BIWEEKLY STRATEGY WEBINAR Q&A),

(MSFT), (GOOGL), (AAPL), (LMT), (XLV), (EWG), (VIX), (VXX), (BA), (TSLA), (UBER), (LYFT), (ADBE),

(HOW TO HANDLE THE FRIDAY, MAY 17 OPTIONS EXPIRATION), (INTU),

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader May 15 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: Where are we with Microsoft (MSFT)?

A: I think Microsoft is really trying to bottom here. It’s only giving up $8 from its recent high, that's why I went long yesterday, and you can be hyper-conservative and only do the June $110-$115 vertical bull call spread like I did. That will bring in a 13.68% profit in 28 trading days, which these days is pretty good. This morning would have been a great entry point for that spread if you couldn’t get it yesterday.

Q: How will tariffs affect Apple (AAPL) when they hit?

A: The price of your iPhone goes up $140—that calculation has already been done. All of Apple's iPhones are made in China, something like 220 million a year. There’s no way that can be moved, they need a million people for the production of these phones. It took them 20 years to build that facility and production capacity; it would take them 20 years to move it and it couldn't be done anywhere else in the world. So, that's why Apple led the charge on the downside and that's why it will lead the charge to the upside on any trade war resolution.

Q: How bad is the trade war going to get?

A: The market is betting now by only going down 1,400 Dow points it will be resolved on June 28th in Osaka. If that doesn’t happen it could get a lot worse. It could get down to my down 2,250-point target, and if it continues much beyond that, then we’ll get the whole full 4,500 points and be back at December lows. After that, you’re really looking at a global recession, a global depression, and ultimately nearing 18,000 in Dow, the 2016 low.

Q: Will global trade wars force US Treasuries down to around 2.10% on the ten year?

A: Yes. Again, the question is how bad will it get? If we resolve the trade war in six weeks, treasuries will probably double bottom here at around a 2.33% yield. If we go beyond that, then 2.10% is a chip shot and we go into a real live recession. The truth is no one knows anything, and we really don’t have any influence over what happens.

Q: How will equities digest and increase in European tariffs for cars?

A: It would completely demolish the European economy—especially that of Germany (EWG) which has 50% of its economy dependent on exports (primarily cars) and mostly to the U.S. And if we wipe out our biggest customer, Europe, then that would spill over here very quickly. Anybody who sells to Europe—like all the big Tech companies—would get slaughtered in that situation.

Q: Is it time to buy the Volatility Index (VIX)?

A: It’s too late to buy (VIX) now. I don’t want to touch it until we get down to that $12-$13 handle again because the time decay on this is enormous. Time decay is more than 50% a year, so your timing has to be perfect with trading any (VIX) products, whether it’s the (VXX), the (VIX) futures, the (VIX) options, or so on. There are countless people shorting (VIX) here, and they will short it all the way down to $12 again.

Q: What should I do about Boeing at this point?

A: We went long, got out, took our profit and caught this rally up to $400 a share. Then (BA) gave it up and it broke down. It’s a really tempting long here. Along with Apple, Boeing has the largest value of exports to China of any company. They have orders for hundreds of airlines from China, so they are an easy target, especially if there is a ramp up in the intensity of the trade war. That said, something like a June $270-$300 vertical bull call spread is very tempting, especially with elevated volatility up here, so I’m watching that very closely. We’re looking for the recertification of the 737 MAX bounce which could happen in the next few weeks; if that does happen it should rally at least back up to 380.

Q: Are your moving averages simple or exponential?

A: I just use the simple. I find that the simpler a concept is, the more people can understand it, and the more people buy it; that’s why I always try to keep everything simple and leave the algorithms for the computers.

Q: What stocks are insulated from a US/China trade war?

A: None. When the whole market goes risk off, people sell everything. Remember that an overwhelming portion of the market is now indexed with passive investment funds, so they just go straight risk on/risk off. It makes no difference what the fundamentals are, it makes no difference who has a lot of Chinese business or a little—everyone gets hit and everyone will get boosted when the trade war ends. There is no place to hide except cash, which is why I went 100% cash going into this. People seem to forget that cash has option value and having a lot of cash going into one of these situations is actually worth a lot of money in terms of opportunities.

Q: Do you have any thoughts on Uber’s (UBER) bad performance?

A: Yes, the whole sector was wildly overvalued, but no one knew that until they brought it to market and found out the real supply and demand for the issue. The smartest company of the year has to be Lyft (LYFT), which got a nice valuation by doing their issue first and keeping it small. So, they kind of rained on Uber’s parade; at one point, Uber was down 25% from their IPO price. That’s awful.

Q: Is Trump forcing the Fed to drop rates with all this tariff threat?

A: Yes, and if you remember, Trump really ramped up the attacks on the Fed in December. And my bet is at the first sign the trade talks were in trouble, they wanted to lower rates to offset the hit to the U.S. economy. There was no economic reason to suddenly demand huge interest rate cuts last December other than a falling stock market. The tariffs amount to a $72 billion tax increase on the American consumer, felt mostly at the low end, and that is terrible for the economy in that it reduces purchasing power by exactly that much.

Q: Would you buy the dollar as a safe haven trade?

A: No, I would not. The dollar may actually go down some more, especially with the collapse in our interest rates and European interest rates bottoming at negative levels. The best thing in the world in a high-risk environment like this is cash—don’t try to get clever and buy something you think will outperform. You could be disappointed.

Q: Why is healthcare (XLV) behaving so badly?

A: You don’t want to get into political football ahead of an election. That said, they're already so cheap that any kind of recovery could very well take healthcare up big, especially on an individual company basis. This is a sector where individual stock selection is crucial.

Q: Would you buy deep in the money calls on PayPal (PYPL)?

A: Yes, I would. Wait for a down day. Today we’re up slightly, but if we have a weak afternoon and a weak opening tomorrow morning, that would be a good time to add more longs in technology. PayPal is absolutely at the top of the list, as are names like Adobe (ADBE) and Alphabet (GOOGL).

Q: Should I be buying LEAPS in this environment?

A: No; a LEAP is a one-year long term deep out-of-the-money call spread. That was a great December bottom trade. The people who bought leaps then made huge fortunes. We’re too high here to consider leaps for the main market unless it's for something that’s just been bombed out, like a Tesla (TSLA) or a Boeing (BA), where you had big drops—then I would look at LEAPS for the super decimated stocks. But the rest of the market is still too high for thinking about leaps. Wait a couple of months and we may get back to those December lows.

Q: What happened to your May 10th bear market call?

A: Actually, it’s kind of looking good. It’s looking in fact like the market topped on May 2nd. If saner heads prevail, the trade war will end (or at least we’ll get a fake agreement) and the market will go to a new high. If not, then that May 10th target forecast I made two years ago IS the final top.

Q: You’re saying today we’re at a bottom?

A: We’re at a bottom for a short-term trade with a June 21st target. That was the expiration date of the options spreads I did this week. Whether this is the final bottom in the whole down move for a longer term, no one has any idea, even if they try to say differently. This is totally dependent on political developments.

Q: What do you have to say about Lockheed Martin (LMT)?

A: This sector usually does well with a wartime background. Expect that to continue for the foreseeable future. But at a certain point, the defense stocks which have had fantastic runs under Trump will start to discount a democratic win in the next election. If that does happen, defense will get slaughtered. I would be using any future strength to sell out of the whole defense area. Peace could be fatal to this sector.