Mad Hedge Technology Letter

November 29, 2018

Fiat Lux

Featured Trade:

(SALESFORCE KNOCKS IT OUT OF THE PARK)

(CRM), (AAPL), (PYPL), (ADBE), (TWLO), (MSFT), (AMZN)

Mad Hedge Technology Letter

November 29, 2018

Fiat Lux

Featured Trade:

(SALESFORCE KNOCKS IT OUT OF THE PARK)

(CRM), (AAPL), (PYPL), (ADBE), (TWLO), (MSFT), (AMZN)

It’s been a grueling winter for tech stocks and countless number of positive earnings reports have fell on deaf ears.

Will the bloodletting stop?

Not if Salesforce (CRM) has something to say about it!

And if you thought that tech’s secular tailwinds had vanished, this latest earnings report confirmed that software stocks are alive and are as potent as ever.

That is why I have identified software stocks as the best tech play in the current late-stage economic cycle.

At the Mad Hedge Lake Tahoe Conference, I clearly telegraphed that companies do not pour capital into capex for large and risky projects at this late stage, they search for the additional incremental dollar by arming their staff with optimal and efficient software programs to squeeze more juice out of the lemon.

Salesforce is a great example of this.

Moving forward, Salesforce is on the A-team of the software squad, and ideally positioned to harpoon any whales that come near their boat.

Companies are looking to double down on software initiatives at this point which is another reason why annual IT budgets have shot through the roof.

I have met countless CEOs who guide thousands of staff throughout branches around the world and they told me that one of the big in-house additions has been integrating Salesforce as the main customer relationship management system deleting legacy systems of yore that have pooped out.

The switch bears fruits immediately with operations supercharged like a 5-star high school football prospect on his first month of ‘roids.

Simply put, everything just works a lot better with access to this software.

What CEO wouldn’t want that?

Even more salient is that Salesforce has promoted itself as the emblematic tech growth stock promising to smash $16 billion of annual revenue by next year.

I love that Salesforce commits to ambitious sales targets and always delivers the goods.

A talking head on a prominent financial TV show went on record saying that Apple is the key to the tech narrative perpetuating, I would completely disagree with this statement.

Everyone and his mother have absorbed that Apple iPhones sales have plateaued, I am honestly sick of hearing the same story in the news over and over again.

That is why Apple has been trying to morph into a software and service stock. They are doing a great job at it by the way.

The real conclusive acid test to the tech story are these high growth software stocks because they should be the ones outperforming at this stage in the economic cycle.

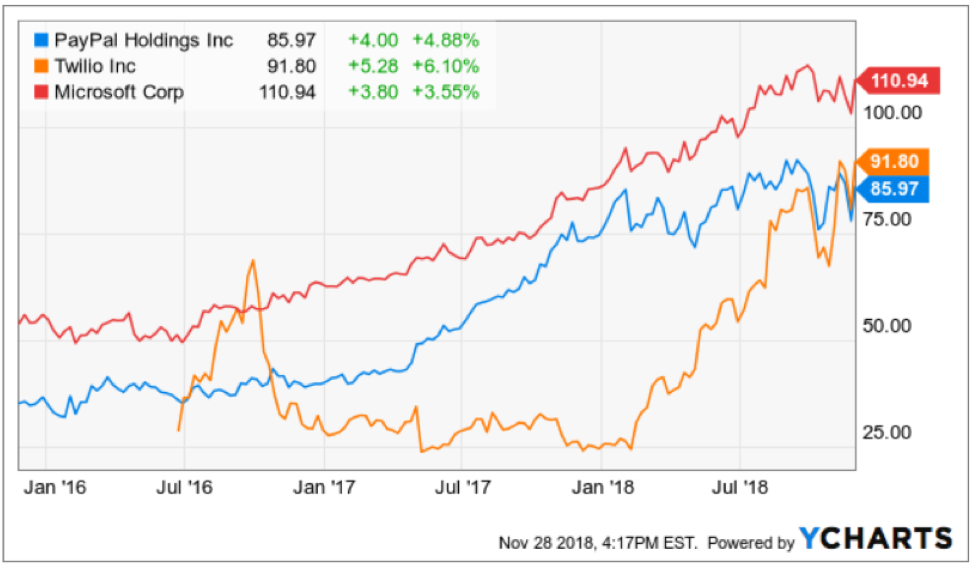

If companies tilted towards software like Salesforce, Twilio (TWLO), PayPal (PYPL), Microsoft (MSFT), and Adobe (ADBE), just to name a few of the crown jewels of software stocks, start laying eggs then I would admit the tech story is dead.

But it’s not.

Salesforce is poised to continue its ascent and that basically means quarterly sales growth in the mid-20s for the foreseeable future.

There is an addressable market of $200 billion and the pipeline is rich as ever could be.

Salesforce has really turned the corner with free cash flow and profitability. It was only a few years ago they were turning in heavy losses, but this new Salesforce will be even more profitable as the network effect makes the sum of the parts and each add-on cloud-based software tool even more valuable.

Companies just love the breadth of functionality that Salesforce offers and their pension for product enhancement is really owed to CEO Marc Benioff who never shies away from calling his peers out and never cuts corners.

In fact, Marc Benioff is one of the good guys in an increasingly rotting Silicon Valley, part of this has to do with him growing up as a local lad in Burlingame, just a stone throw from his newly built palatial Salesforce Tower gracing downtown San Francisco’s picturesque skyline.

Benioff has more skin in the game as a local and publicly supported Proposition C, effectively a bill that would charge a homeless tax on big earning corporations in San Francisco.

Benioff has also promised to fund any subsequent legal attack that attempts to unravel this homeless tax putting his money where his mouth is.

Benioff noted that he has seen no softness in the macro spending environment.

And even with all the crazy headlines spinning around in the media, there has been no material impact from any supposed peak or downshift in the business environment.

Not only is Salesforce dredging up SME deals at a fast rate, they are quickly targeting the big kahunas.

The number of deals generating more than $1 million was up 46% YOY in the third quarter.

The volume of $20 million-plus relationships is also growing significantly.

In the past quarter, Salesforce renewed and expanded a 9-figure relationship with one of the largest banks in the world.

Salesforce is able to upsell their cloud tools to customers and these firms eat up the Einstein built-in functionality that uses artificial intelligence to improve the existing software.

North America comprised 71% of total revenue which is why this software company will reap the rewards for any extension of this economic cycle because they are largely domestic and best in show.

Salesforce beat and raised its outlook calming the frayed nerves of investors looking to dump software stocks.

Just look at the billings growth that was anticipated at 19%, Salesforce smashed it by 8% coming in at 27%.

Not only are they scooping up new customers, but renewals have been just as robust.

The truth is that Salesforce can’t roll out enough cloud-based software products to meet the insatiable demand.

All of this backs up my thesis that software stocks will be the outsized winners of 2019.

The FANGs are not dead, I rather hold an Amazon (AMZN) or Apple (AAPL) long term if I had the choice.

But at this stage, investors should be piling into all the crème de la crème software stocks.

Avoid them at your peril.

At our weekly Monday staff meeting, coworkers were griping and grimacing about their failed internet connections and annoying glitches to their favorite e-commerce sites during the mad rush to find the best deal during Black Friday and Cyber Monday.

Internet traffic was that torrential when sites were driven offline for minutes and some, hours by a bombardment of gleeful shoppers hoping to splash their credit card numbers all over the web on sweet discounts.

The crashing of system servers epitomizes the robust transition to online commerce that has most of us pinned to our devices surfing our go-to platforms all day long.

According to data from Adobe (ADBE) analytics, Black Friday sales jumped 23.6% YOY to $6.22 billion, and it was the first time in history that mobile sales broke the $2 billion threshold.

It is a clear victory for e-commerce and, in particular, mobile shopping that has become more integrated into modern tech DNA.

Mobile sales comprised 33.5% of total sales and were up from 29.1% last year, signaling that more is yet to come from this transcending movement that is shoving everything from content, digital ads, entertainment, banking and pretty much everything you can think of to your handheld smartphone.

CEO of Kohl’s (KSS) Michelle Gass confirmed the e-commerce strength by saying, “80 percent of traffic online came from mobile devices.”

The beauty of this movement is that it’s not an “Amazon (AMZN) takes all” scenario with other players allowed to feast on a growing size of the e-commerce pie.

“Click and collect” has been a strategy that has paid off handsomely with sales up 73% YOY during the shopping holidays.

This all supports my prior claim that e-commerce is one of the most innovative and dynamic parts of technology especially the grocery space, and the buckets full of capital attempting to reconfigure the e-commerce spectrum is creating an enhanced customer experience for the final buyer resulting in better products, superior delivery methods, and cheaper prices.

Some other retailers spicing up their e-commerce strategy are dinosaur big-box retailer’s intent to defend their business from the Amazon death star.

If you can’t innovate in-house, then “borrow” the innovation from somewhere else.

That is exactly what Target (TGT) has chosen to do announcing last week that it would grant free 2-day shipping with no minimum sale threshold.

The tactic is bent on undercutting Walmart (WMT) who currently operate a 2-day free shipping policy with a minimum order of $35.

Most shoppers will buy in bulk easily eclipsing the $35 per order mark minimizing the rot of small orders.

And if they aren’t eclipsing the $35 per order mark, it demonstrates the firm’s offerings lack the diversity and quality to compete with Amazon.

Capturing the incremental sale squarely rests on the e-tailers ability to coax out the buyers’ impulses to move on the can’t-miss items.

The lesser known retailers fail miserably at matching the lineup of products that Amazon can roll out.

The bountiful product selection at Amazon leads customers to pay for 3, 4, 5, 6 or more items on Amazon.com.

That said, I am bullish on Walmart’s e-commerce strategy. The “click and collect” strategy has shown to be an outsized winner increasing industry sales of this type 120% YOY.

Walmart is at the center of this strategy and they are refurbishing their supercenters to accommodate this growth in collecting from the curb.

Effectively, this gives customers the option to skip the queue instead of bracing the hoards and navigating the crowds of shoppers in the supercenter.

Other changes are minor but will help, such as offering online product location maps to customers beforehand and allowing customers to pay for large items like big-screen televisions on the spot.

The biggest windfall is derived from the cataclysmic demise of Toy “R” Us, giving Walmart a new foothold into the toy business.

Walmart is beefing up toy items by 40% in the stores and layering that addition with another 30% increase in their e-commerce division.

Adobe’s upper management recently said in an interview that interactive toys have been a wildly popular theme this year amid a backdrop of the best holiday shopping season ever recorded.

Another attractive gift selling like hotcakes are video games, titles boding well for sales at Activision (ATVI), EA Sport (EA), and Take-Two Interactive (TTWO).

Reliant IT infrastructure will be a key component to executing these holiday sales bonanzas.

Clothing retailer J. Crew and home improvement chain Lowe's (LOW) were grappling with sudden disruptions to their IT systems before they managed to get back online.

More than 75 million shoppers parade the internet to shop during Black Friday and Cyber Monday, and the opportunity cost swallowed to a tech glitch is a CEO’s worst nightmare.

Ultimately, what does this all mean?

Focusing on the positive side of the surging holiday sales is the right thing to do because the avalanche of momentum will have a knock-on effect on the rest of the economy.

Certain companies are positioned to harvest the benefits more than others.

Amazon guided its 4th quarter estimates conservatively and is in-line to beat top and bottom line forecasts.

Other pockets of strength are Walmart’s tech pivot, albeit from a low base. Walmart still has more room to maneuver and they are in the 2nd inning of their tech transformation snatching the low-hanging fruit for now.

Another interesting e-commerce company swinging its elbows around is Etsy (ETSY).

They sell vintage and handmade craft adding the personalized touch that Amazon can’t destroy.

Margins will be higher than the typical low-cost, value e-commerce platform, but scaling this type of business will be more difficult.

Sales grew 41% sequentially and just in time for a winter holiday blowout.

Etsy became profitable in 2017 after three straight loss-making years, and 2018 is poised to become its best year ever.

The profitability bug is hitting Etsy at the perfect time with its EPS growth rate up 36% sequentially.

They report at the end of February and I expect them to smash all estimates.

There are some deep ramifications for the long term of e-commerce that is beginning to suss itself out.

For one, shipping times will continue to be slashed with a machete. If you are enjoying the 2-day free shipping from Amazon and Target now, then wait until 2-day becomes 1-day free shipping.

Then after 1-day free shipping, customers will get 10-hour shipping, and this won’t stop until goods are shipped to the customer’s door in less than 1-hour or less.

This is what the massive $50 billion in logistical investments over the next five years by the likes of Uber and Amazon are telling us.

It will take years for the efficiencies to come to fruition, but it is certainly in the works.

In the next five years, America’s logistics infrastructure will have to accommodate the doubling of e-commerce packages from 2 billion to 4 billion per year.

Another trend is that omnichannel offerings are sticking and won’t go away anytime soon.

It was once premised that online sales would destroy brick and mortar, yet moving forward, a mix of different sales channels will be the most efficient way of moving goods in the future.

Pop-up stores have been an intriguing phenomenon of late, and surprisingly, 60% of consumers still require interaction with the product to be convinced it's worthy of buying.

Certain products such as fashionable dresses and designer shoes must be given a whirl before a decision can be made. This won’t change anytime soon.

The timing of the sales and marketing push has been moved forward as competitors are eager to get a jump on one another.

Management is agnostic to the timing of the sale.

Thus, discounted sales will show up a week before Thanksgiving as pre-Thanksgiving sales in the future elongating the holiday shopping season cycle by starting it early and delaying the finish of it.

Lastly, the record numbers prove that the e-commerce renaissance and the pivot to mobile is not just a flash in the plan.

What does this mean for tech equities?

The temporal tech sell-off of late is largely a result of outside macro forces and is not indicative of the overall health of the tech sector that has experienced record earnings.

If the markets can keep its head above the February lows, it sets up an intriguing December fueled by Americans flashing their digital wallets on online platforms.

Mad Hedge Technology Letter

November 7, 2018

Fiat Lux

Featured Trade:

(THE RELIABILITY OF ADOBE)

(ADBE), (GOOGL), (ZEN), (TWLO), (SQ)

Tech companies have a habit of suddenly coming and going because of the nature of the relentless environment that spits out losers and celebrates winners.

It’s hard-pressed to find software companies that pass the test of time but there is one that is healthily chugging along that most people know quite well.

Adobe (ADBE) was established 35 years ago in co-founder John Warnock's garage.

This legacy software company’s name, Adobe, was named after the Adobe Creek in Los Altos, California, which ran behind Warnock's house.

Adobe cut its teeth in an era when tech CEOs were not larger-than-life cult figures, and all Adobe has done is quietly infiltrating its way into everybody’s devices by way of Adobe Flash Player and its smorgasbord of useful software applications.

Adobe acquired Macromedia in 2005 which was responsible for building Adobe Flash Player.

This Macromedia software has been developed and distributed by Adobe Systems ever since the purchase and its functions involve viewing multimedia contents, executing rich internet applications, and streaming audio and video. Flash Player can run from a web browser as a browser plug-in or on supported mobile devices.

Flash player was its second hit success software program after its Adobe Acrobat and Reader software introduced PDF, the Portable Document Format, which is still ubiquitously used today even after all these years.

Most software companies are relatively new to the scene and like companies I have recently written about such as Zendesk (ZEN) and Twilio (TWLO), they can brag about growing sales of 30% or 40% plus per year.

Adobe isn’t too shabby itself growing sales at over 24% annually – remarkably high for such an ancient tech company.

The company’s strengths are similar to that of Apple (AAPL) – high-quality products and high profitability.

There will be no back-to-back doubling of the stock like some hyper-growth tech stocks because Adobe doesn’t subscribe to the type of growth trail that Square (SQ) has blazed.

What you can expect from Adobe is a slow grind up in share price stoked by its outperforming EPS expansion and acceptable sales growth of mid-20%.

Its annual operating margins have essentially tripled since the beginning of 2015 from around 10% and now boasts an Apple-like 30%.

There are no bones about it – Adobe has high-quality software across its diversified portfolio.

Other Adobe software products universally soaked up are its stable array of graphic design software such as Adobe Photoshop and Adobe Dreamweaver.

Adobe has also ventured into video editing, animation, and visual effects with Adobe Premiere Pro.

Not only that, Adobe has forayed into more conventional types of software such as digital marketing management software and server software.

Simply put, Adobe’s assortment of digital media software products has a religious-like following especially for iOS users.

As you might have guessed correctly, the lion’s share of Adobe’s revenue stream stems from its software as a service (SaaS) segment contributing 80% to the top line.

More narrowly, the digital media segment makes up almost 70% of the subscription-based revenue. This division will expand at least 20% each year boding well for Adobe to maintain its 20% plus sales growth that any legacy software company would sacrifice a right leg to achieve.

It’s digital marketing software products rub up against stifling competition in Alphabet (GOOGL) amongst others and contribute a less robust 30% to overall sales.

I am less bullish on this part of the business because they have it rough competing against one of the Fangs, the path of less resistance clearly sides with its bread and butter of the digital media offerings.

Its subscription-based pricing model was the catalyst for boosting profitability causing the stock to experience massive price gains. The stock has doubled in the past two years which is unheard of for most legacy software companies.

No longer does Adobe need to manufacture the ancient CD of yore physically delivering it to customers, users can briskly download these products directly from the official website, receive constant upgrades over broadband internet, and pay Adobe monthly for their humble services.

In fact, any investors looking for some hot software stocks only need to find companies that recently shifted to a subscription-based pricing model. It’s pretty much a license to print money if the software quality can backup the monthly costs for the user.

I can tell you that Adobe’s software has remained world class, embedded at the heart of most digital devices at home and in the office, and who would have thought that just a little shift to the pricing model would have doubled the stock price?

Well, instead of one-off sales, Adobe can book revenue month after month, and year after year demonstrating the supercharged effect of shifting to a recurring revenue stream model.

Highlighting the pivot to profitability is Adobe’s three-year EPS growth rate of 48% turning this company into a mammoth software company with a $117 billion market cap.

Another positive for Adobe’s future sales are its fertile addressable markets in Europe and Asia.

There is ample room to expand in these geographical regions with Europe already chipping in with almost $2 billion of revenue per year and Asia with another $1 billion.

Future harvests look even more bountiful.

These two regions make up almost 40% of sales and as the Asian middle class is poised to elevate a giant swath of its people to middle class, Adobe will be a handsome beneficiary of this trend as middle-class families tend to pump out more university graduates who migrate to software-based occupations.

Even though Adobe isn’t the sexiest name out there, it certainly is in the category of “safe.”

In no way do I see an eradication of its embedded software spread widely throughout the tech universe.

Its digital media software tools are best-in-show and loyally followed with a long-lasting revenue stream that has room to grow abroad.

Do not expect Adobe to debut any earth-shattering products, but I fully anticipate Adobe to become even more profitable to the point that they might offer a dividend or reallocate capital to shareholders through stock buybacks.

Apple has similar strengths in its business model, albeit on a much grander scale.

I feel that Adobe doesn’t get the credit it deserves because of its steady as it goes drivers that keep motoring higher in an industry that adores groundbreaking products that revolutionize the world.

I would wait for a major sell-off because a double in two years has bid up the stock to expensive levels represented in its premium forward PE multiple of 35.

However, as the conclusion of the mid-term elections offers some certainty to the market, tech stocks could get swept up in a positive rush to round out the year.

Luckily for Mad Hedge Tech readers, this is the golden age for software companies and we are just scratching the surface of the capability software efficiencies can deliver to small and large companies across every bit of the economy.

Another Apple-like similarity is that Adobe is annually voted one of the best places to work according to Fortune, stacked up against companies represented across the full economic spectrum and not just tech.

If you have a kid, tell him to find a job in San Jose, he or she could find worse places to cut a paycheck.

Mad Hedge Technology Letter

September 12, 2018

Fiat Lux

Featured Trade:

(HOW TO PLAY “SOFTWARE AS A SERVICE”),

(AMZN), (IBM), (ADBE), (CRM), (BABA), (CSCO), (SAP), (ORCL), (GOOGL)

If you have read any of our content in the first year of the Mad Hedge Technology Letter, the content is distinctly bullish technology stocks.

A fundamental driver propelling this cogent argument is the dominant Software-as-a-Service (SaaS) industry booming inside the confines of Silicon Valley.

If you want to boil down your tech investment thesis to one indispensable rule – only invest in tech companies that carve out prominent SaaS businesses.

If you stick with this nostrum, you will be delivered profits in spades.

We have recently taken in a swarm of new tech letter subscribers and understanding the panacea that is SaaS will entrench your portfolio in a glorious position to reap untold profits.

What is SaaS?

SaaS is a distribution method in which software is diffused to paid subscribers, usually on an annual, reoccurring payment plan, and the software is remotely stored on a centralized cloud platform awaiting use.

Unsurprisingly, SaaS remains the most lucrative segment of the cloud market.

In 2017, the tech industry did $60.2 billion in annual SaaS sales, that number is poised to explode to $117.1 billion in 2021.

The near doubling of sales underscores the robust nature of these tech firms setting up businesses of this ilk, and the positive effects dripping down to the bottom line.

Simply put, no SaaS business, no reason to invest.

SaaS isn’t the only cloud revenue companies can carve out. Tech firms also offer platform-as-a-service (PaaS) and infrastructure-as-a-service (IaaS).

However, SaaS is by far the prominent growth lever in the high-margin cloud industry.

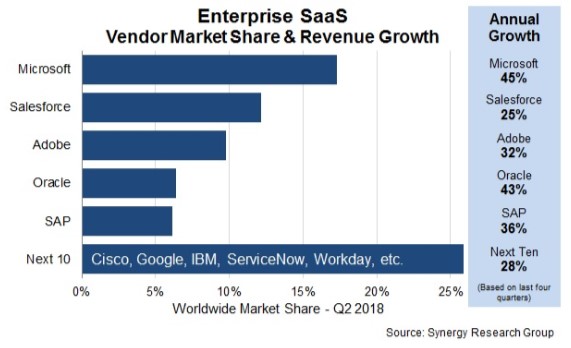

The indomitable presence inside the SaaS industry is Bill Gates’ creation Microsoft (MSFT).

Microsoft leads all companies with a 17% global share of the SaaS market.

The Redmond, Washington, outfit blew past stalwart Salesforce (CRM) nine quarters ago.

Microsoft’s sizzling SaaS business is an oversized contributor to its 45% revenue growth rate, which is head-and-shoulders above the industry average.

Salesforce (CRM), Adobe (ADBE), Oracle (ORCL) and SAP (SAP) fill out the top five largest global SaaS businesses, but it is really a tale of two stories.

Oracle and SAP, which are competing in the same market, are grappling with legacy database businesses and legacy tech, which are punished by investors.

John Dinsdale, a chief analyst at Synergy Research Group, mentioned two outliers of “Cisco (CSCO) and Google too who are making ever-bigger inroads into the SaaS market” leveraging Cisco’s multitude of software assets and Google’s G Suite.

The thing that makes SaaS the x-factor for tech companies is that inevitably every company from every walk of life will adopt this mode of software, giving legs to this distribution model.

Vendors are scrambling to put together some resemblance of a SaaS product together, and this trend is a vital contributor to an industry that is growing 32% YOY worldwide.

Kevin Cochrane, chief marketing officer of SAP Customer Experience lay bare his thoughts about this type of service describing it as the “Golden Age of SaaS.”

Companies are becoming digital first from end to end, explaining the sharp rise in IT professional salaries and rise in quality software products.

As we look around the corner to the IaaS part of the cloud industry, which is growing at around 30% YOY, there is one dominant player, and everybody knows its name.

Amazon (AMZN) is the No. 1 vendor with Microsoft, Alibaba (BABA), Google, and International Business Machines Corporation (IBM) trailing behind.

The top four IaaS players have carved out a total of 73% of the global market ravaging any resemblance of competition.

Amazon is the industry standard with the best record of customer success.

If Amazon branched off into the SaaS industry, it could unlock an additional $100 billion in annual revenue.

A shift into this direction could pad Amazon’s margin’s even more after successfully boosting North American e-commerce margins from 2.4% to 4.7%.

It’s not entirely inconceivable that Amazon could break the $2 trillion valuation in three to five years, as its revved up digital ad business registered growth of 129% YOY last quarter.

Microsoft seized the runner-up position in the IaaS market to Amazon by growing 98% YOY with sales eclipsing $3.1 billion in 2017.

Wherever you turn, whether toward the cloud business or gaming, investors can find Microsoft making sales.

Microsoft has been a favorite of the Mad Hedge Technology Letter and it’s hard pressed to find a better public tech company in operation now.

The SaaS industry is not a one-size-fits-all proposition.

Thus, there is abundant room for niche offerings that quench companies’ demand for specific services.

This is the reason why cloud companies have participated in a non-stop buying binge of smaller companies that fit their needs.

Microsoft purchased developer favorite GitHub for $7.5 billion earlier this year, and similar examples are scattered all over the tech ecosphere.

Artificial Intelligence (AI) will be the kicker that powers SaaS performance to new heights because incorporating this groundbreaking technology will enhance functionality and, in return, raise profits for all involved.

The scalability of SaaS products has allowed companies to offer software for affordable prices allowing the smallest of firms to adopt a digital-first strategy.

This software connects with other software seamlessly integrating an array of productive apps that help teams overperform and overdeliver.

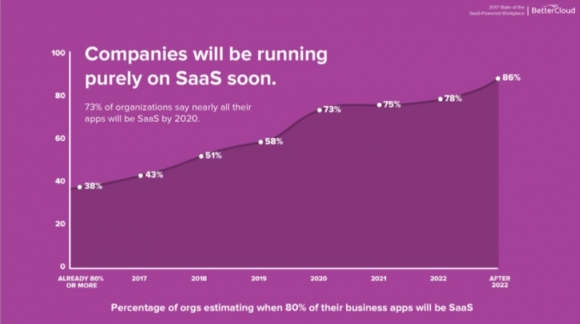

In the American workplace, 73% of companies will be exclusively using SaaS to function by 2020.

American companies are using 16 apps on average per day, a 33% jump in the number of apps they were using just two years ago.

The migration to mobile has swallowed up SaaS products as well with more mobile-specific software rolling out to mobile devices.

The meteoric rise of SaaS offerings has cut IT security budgets substantially as security has been delegated to the cloud instead of in expensive in-house security teams.

No longer do tech firms need to beef up guarding their own gates.

Protection is provided on a centralized cloud with a third-party company ensuring safety.

This development has helped a new industry rise – cloud security.

Whether people realize it or not, the SaaS industry is here to stay and will become more prevalent in every industry going forward.

This is incredibly bullish for companies that sell SaaS products as revenue will continue to rise.

________________________________________________________________________________________________

Quote of the Day

“Growth and comfort do not coexist,” – said CEO of IBM Ginni Rometty.

Mad Hedge Technology Letter

July 5, 2018

Fiat Lux

Featured Trade:

(THE HIGH COST OF DRIVING OUT OUR FOREIGN TECHNOLOGISTS),

(EA), (ADBE), (BABA), (BIDU), (FB), (GOOGL), (TWTR)

There is only so much juice you can squeeze from a lemon before nothing is left.

Silicon Valley has been focused mainly on squeezing the juice out of the Internet for the past 30 years with intense focus on the American consumer.

In an era of minimal regulation, companies grew at breakneck speeds right into families' living quarters and it was a win-win proposition for both the user and the Internet.

The cream of the crop ideas was found briskly, and the low hanging fruit was pocketed by the venture capitalists (VCs).

That was then, and this is now.

No longer will VCs simply invest in various start-ups and 10 years later a Facebook (FB) or Alphabet (GOOGL) appears out of thin air.

That story is over. Facebook was the last one in the door.

VCs will become more selective because brilliant ideas must withstand the passage of time. Companies want to continue to be relevant in 20 or 30 years and not just disintegrate into obsolescence as did the Eastman Kodak Company, the doomed maker of silver-based film.

The San Francisco Bay Area is the mecca of technology, but recent indicators have presaged the upcoming trends that will reshape the industry.

In general, a healthy and booming local real estate sector is a net positive creating paper wealth for its local people and attracting money slated for expansion.

However, it's crystal clear the net positive has flipped, and housing is now a buzzword for the maladies young people face to sustain themselves in the ultra-expensive coastal Northern California megacities.

The loss of tax deductions in the recent tax bill make conditions even more draconian.

Monthly rental costs are deterring tech's future minions. Without the droves of talent flooding the area, it becomes harder for the industry to incrementally expand.

It also boosts the costs of existing development/operations staffers whose capital feeds back into the local housing market buying whatever they can barely afford for astronomical prices.

Another price spike ensues with first-time home buyers piling into already bare-bones inventory because of the fear of missing out (FOMO).

After surveying HR tech heads, it's clear there aren't enough artificial intelligence (A.I.) programmers and coders to fill internal projects.

Compounding the housing crisis is the change of immigration policy that has frightened off many future Silicon Valley workers.

There is no surprise that millions of aspiring foreign students wish to take advantage of America's treasure of a higher education because there is nothing comparable at home.

The best and brightest foreign minds are trained in America, and a mass exodus would create an even fiercer deficit for global dev-ops talent.

These U.S.-trained foreign tech workers are the main drivers of foreign tech start-ups.

Dangling carrots and sticks for a chance to start an embryonic project in the cozy confines of home is hard to pass up.

Ironically enough, there are more A.I. computer scientists of Chinese origin in America than there are in all of China.

There is a huge movement by the Chinese private sector to bring everyone back home as China vies to become the industry leader in A.I.

Silicon Valley is on the verge of a brain drain of mythical proportions.

If America allows all these brilliant minds to fly home, not only to China but everywhere else, America is just training these workers to compete against American workers.

A premier example is Baidu co-founder Robin Li who received his master's degree in computer science from the State University of New York at Buffalo in 1994.

After graduation, his first job was at Dow Jones & Company, a subsidiary of News Corp., writing code for the online version of the Wall Street Journal.

During this stint, he developed an algorithm for ranking search results that he patented, flew back to China, created the Google search engine equivalent, and named it Baidu (BIDU).

Robin Li is now one of the richest people in China with a fortune of close to $20 billion.

To show it's not just a one-hit-wonder type scenario, three of the top five start-ups are currently headquartered in Beijing and not in California.

The most powerful industry in America's economy is just a transient training hub for foreign nationals before they go home to make the real moola.

More than 70% of tech employees in Silicon Valley and more than 50% in the San Francisco Bay Area are foreign, according to the 2016 census data.

Adding insult to injury, the exorbitant cost of housing is preventing burgeoning American talent from migrating from rural towns across America and moving to the Bay Area.

They make it as far West as Salt Lake City, Reno, or Las Vegas.

Instead of living a homeless life in Golden Gate Park, they decide to set up shop in a second-tier American city after horror stories of Bay Area housing starts populate their friends' Instagram feeds and are shared a million times over.

This trend was reinforced by domestic migration statistics.

Between 2007 and 2016, 5 million people moved to California, and 6 million people moved out of the state.

The biggest takeaways are that many of these new California migrants are from New York, possess graduate degrees, and command an annual salary of more than $110,000.

Conversely, Nevada, Arizona, and Texas have major inflows of migrants that mostly earn less than $50,000 per year and are less educated.

That will change in the near future.

Ultimately, if VCs think it is expensive now to operate a start-up in Silicon Valley, it will be costlier in the future.

Pouring gasoline on the flames, Northern California schools are starting to fold like a house of cards due to minimal household formation wiping out student numbers.

The dire shortage of affordable housing is the region's No. 1 problem.

A 1,066-sq.-ft. property in San Jose's Willow Glen neighborhood went on sale for $800,000.

This would be considered an absolute steal at this price, but the catch is the house was badly burned two years ago. This is the price for a teardown.

When you combine the housing crisis with the price readjustment for big data, it looks as if Silicon Valley has peaked or at the very least it's not cheap.

Yes, the FANGs will continue their gravy train, but the next big thing to hit tech will not originate from California.

VCs will overwhelmingly invest in data over rental bills. The percolation of tech ingenuity will likely pop up in either Nevada, Arizona, Texas, Utah, or yes, even Michigan.

Even though these states attract poorer migrants, the lower cost of housing is beginning to attract tech professionals who can afford more than a burned down shack.

Washington state has become a hotbed for bitcoin activity. Small rural counties set in the Columbia Basin such as Chelan, Douglas, and Grant used to be farmland.

The bitcoin industry moved three hours east of Seattle for one reason and one reason only - cost.

Electricity is five times cheaper there because of fluid access to plentiful hydro-electric power.

Many business decisions come down to cost, and a fractional advantage of pennies.

Globalization has supercharged competition, and technology is the lubricant fueling competition to new heights.

Once millennials desire to form families, the only choices are regions where housing costs are affordable and areas that aren't bereft of tech talent.

Cities such as Las Vegas and Reno in Nevada; Austin, Texas; Phoenix, Arizona; and Salt Lake City, Utah, will turn into hotbeds of West Coast growth engines just as Hangzhou, China-based Alibaba (BABA) turned that city into more than a sleepy backwater town with a big lake at its center.

The overarching theme of decentralizing is taking the world by storm. The built-up power levers in Northern California are overheated, and the decentralization process will take many years to flow into the direction of these smaller but growing cities.

Salt Lake City, known as Silicon Slopes, has been a tech magnet of late with big players such as Adobe (ADBE), Twitter (TWTR), and EA Sports (EA) opening new branches there while Reno has become a massive hotspot for data server farms. Nearby Sparks hosts Tesla's Gigafactory 1 along with massive data centers for Apple, Alphabet, and Switch.

The half a billion-dollars required to build a proper tech company will stretch further in Austin or Las Vegas, and most of the funds will be reserved for tech talent - not slum landlords.

The nail in the coffin will be the millions saved in state taxes.

The rise of the second-tier cities is the key to staying ahead of the race for tech supremacy.

_________________________________________________________________________________________________

Quote of the Day

"Twitter is about moving words. Square is about moving money," - said CEO of Twitter, Jack Dorsey, to The New Yorker, October 2013.

Mad Hedge Technology Letter

April 16, 2018

Fiat Lux

Featured Trade:

(THE HIGH COST OF DRIVING OUT OUR FOREIGN TECHNOLOGISTS),

(EA), (ADBE), (BABA), (BIDU), (FB), (GOOGL), (TWTR)