Mad Hedge Biotech & Healthcare Letter

June 18, 2020

Fiat Lux

Featured Trade:

(ABBVIE JOINS THE CORONA FRAY),

(ABBV), (REGN), (LLY), (GMAB), (RHHBY), (AMGN), (JNJ), (NVS), (GSK), (MRK), (AZN), (SNY), (AGN), (PFE)

Mad Hedge Biotech & Healthcare Letter

June 18, 2020

Fiat Lux

Featured Trade:

(ABBVIE JOINS THE CORONA FRAY),

(ABBV), (REGN), (LLY), (GMAB), (RHHBY), (AMGN), (JNJ), (NVS), (GSK), (MRK), (AZN), (SNY), (AGN), (PFE)

Mad Hedge Biotech & Healthcare Letter

June 11, 2020

Fiat Lux

Featured Trade:

(THE BIOTECH MERGER BOOM ACCELERATES)

(AZN), (GILD), (BMY), (ABBV), (AGN), (TAK), (CI), (SNY), (JNJ), (UNH), (RHHBY), (LLY)

Nothing can ever be absolutely shocking in the biotechnology and healthcare world.

I’ll admit though that the reports on AstraZeneca’s (AZN) interest in acquiring Gilead Sciences (GILD) surprised me.

The two companies touched base last month on a potential acquisition deal.

If this rumor turns into a reality, then we’re looking at what could be the biggest healthcare deal to date.

That’s saying something considering the massive mergers we’ve seen in the past years.

So far, the biggest biotechnology and healthcare deal is the $87.6 billion acquisition of Celgene (CELG) by Bristol-Myers Squibb (BMY) in 2019.

In the same year, AbbVie (ABBV) acquired Allergan (AGN) for a whopping $83.8 billion, making it the third biggest deal in the healthcare sector to date.

The year 2018 paved the way for two more massive deals in the form of Takeda’s (TAK) $81 billion acquisition of Shire, which ranks fourth overall, and Cigna’s (CI) $68.4 billion deal with Express Scripts (ESRX) in seventh place.

Fifth on the list is by Sanofi’s (SNY) $73.5 billion deal with Aventis in 2004.

Although it has been two decades since it happened, the $72.5 billion merger of Glaxo and SmithKline Beecham in 2000 still counts as one of the biggest deals in the industry. This agreement gave birth to GlaxoSmithKline (GSK).

Prior to Bristol-Myers Squibb and Celgene deal, it was Pfizer’s (PFE) $87.3 billion acquisition of Warner-Lambert in 1999 that topped the list.

AstraZeneca’s current market capitalization is roughly $140 billion. Meanwhile, Gilead Science’s market cap stands at approximately $96 billion.

With all these in mind, the AstraZeneca-Gilead Sciences merger is estimated to reach roughly $250 billion on top of the significant synergies expected throughout the years.

If these two health industry heavyweights merge, then their newly formed company would become the third biggest healthcare company in the world behind Johnson & Johnson (JNJ), which has a market cap of $384.55 billion, and UnitedHealth Group (UNH) with $293.85 billion.

Looking at this potential merger in the context of the coronavirus race, it’s safe to say that the combined efforts of AstraZeneca and Gilead would create a COVID-19 titan.

AstraZeneca’s partnership with the University of Oxford resulted in a COVID-19 vaccine candidate that was recently selected as one of the top five candidates worthy of US government support through Trump’s Operation Warp Speed program.

Meanwhile, Gilead’s antiviral medication Remdesivir has been constantly hailed as the standard of care for COVID-19 treatment since the pandemic broke.

The drug which was previously marketed as an HIV medication is now expected to generate $2 billion in sales as a COVID-19 treatment in 2020 alone.

In 2022, Remdesivir is estimated to rake in roughly $7.7 billion in sales. After that, the antiviral drug is projected to generate annual sales somewhere between $6 billion and $7 billion.

Although everything is hypothetical, let’s take a quick look at where each company stands at the moment outside their COVID-19 efforts.

AstraZeneca has been a consistent strong stock market performer throughout the years.

In the first quarter of 2020, sales improved in practically all of AstraZeneca’s territories. Although it has a diversified portfolio of drugs and a robust pipeline, the company’s hottest segment is its oncology business.

A good example of this is non-small cell lung cancer treatment Tagrisso, which is starting to live up to expectations as the next mega-blockbuster for AstraZeneca.

The cancer drug’s first quarter sales reached an impressive $982 million, showing off a 56% jump year over year.

This is promising considering that its competitors include Roche’s (RHHBY) Tarceva and Eli Lilly’s (LLY) Cyramza.

As for its 2020 revenue forecast, AstraZeneca is reported to rake in $25 billion, from which it will generate approximately $7.5 billion in operating profit.

On the other hand, Gilead also has an impressive portfolio that it can bring to the table.

In the first quarter of 2020, the company earned $5.47 billion in revenue compared to the $5.20 billion it generated in the same period last year.

Despite the decline in its hepatitis products from $790 million in the first quarter of 2019 to $729 in the same period of 2020, Gilead’s HIV line made up for the loss by bringing in over $4 billion in sales compared to the $3.6 billion it earned last year.

Not only that, some of Gilead’s other candidates are exciting.

For example, rheumatoid arthritis drug Filgotinib is expected to become another blockbuster and generate $5 billion in revenue annually.

Meanwhile, the anti-tumor treatment Magrolimab is estimated to rake in $3 billion in peak sales.

With the company’s older drugs still capable of generating strong revenue and its new candidates showing their potential for revenue expansion, Gilead can be assured of a continued cash flow well into the 2030s.

Regardless of whether this rumored mega-merger pushes through, both Gilead and AstraZeneca are attractive stocks worthy of their premium valuations.

Mad Hedge Biotech & Healthcare Letter

October 1, 2019

Fiat Lux

Featured Trade:

(THE PLAYERS GUIDE TO BIOTECH INVESTING)

(AMGN), (PFE), (NOVN), (ABBV), (ABT),

(AGN), (ROG), (GSK), (CELG), (JNJ), (BMY)

You can’t watch a game without a program, and the lineup for biotech and healthcare is truly astonishing. No surprise then that the fields account for more or less than 17% of US GPD.

Here is a listing of the biggest $100 billion plus products you have never heard of. The good news is that you have just stumbled across a sector that will generate no less than a staggering $1.4 trillion in sales over the next five years.

That means it’s certainly worth your time getting to know this field. With this amount at stake, it’s no wonder companies manufacturing these blockbuster drugs are sparing no expense to fight off patent vultures.

A good example is Amgen (AMGN), which recently won its case to extend the patent life of rheumatoid arthritis biological Enbrel against Novartis AG’s (NOVN) biosimilar arm Sandoz. Since each extra hour added to patent life means millions of dollars (and sometimes billions) in sales, the additional 10 years of exclusivity for Enbrel is a massive victory for Amgen.

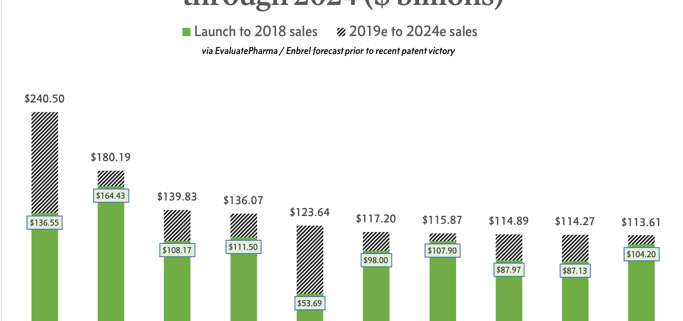

In a recent study released by Evaluate Pharma, Enbrel was ranked third in the top 10 biggest sellers up to 2024. The forward-looking consensus projection anticipates Amgen’s golden goose to hit roughly $140 billion in total revenues in five years – a truly impressive performance particularly for a drug that has been around for more than 20 years. However, Enbrel’s longevity pales in comparison to the other behemoths in the biopharma realm.

Up until 2018, Pfizer’s (PFE) Lipitor held the title of earning the highest lifetime sales in the industry. Since its launch in 1997, the cholesterol drug has raked in $164.4 billion in revenues so far with the number estimated to reach $180 billion by 2024. Lipitor’s success is highlighted more by the fact that it's under a small molecule status and holds approval for a very narrow indication.

Overtaking Lipitor to take the top spot is AbbVie’s (ABBV) rheumatoid arthritis treatment Humira, which closed with $20 billion in sales in 2018 alone. While some AbbVie investors frown upon the over-reliance of the company on Humira, it appears that the efforts to protect the drug has paid off big time.

With patent protection (132 approved patents!) safeguarding its exclusivity in the market, Humira is projected to reach a total of $240 billion in revenues by 2024. Clearly, the rewards they’ve been reaping show no signs of abating anytime soon.

More importantly, Humira’s robust sales, which makes up almost 70% of the company’s profits, has provided AbbVie with the financial capacity to finally get out of the shadow of parent company Abbott Laboratories (ABT) and come up with its own pipeline. As it happens, AbbVie’s efforts towards this direction have already started with the massive purchase of Allergan (AGN) for $63 billion this year.

Apart from Lipitor, Humira, and Enbrel, there are three more blockbuster products with sales that hit the $100 billion mark as of 2018 -- a figure that would make Ecuador proud to claim as their annual GDP. These are Roche Holding Ltd. Genussscheine’s (ROG) chemotherapy drug Rituxan, Amgen’s anemia treatment Epogen, and GlaxoSmithKline’s (GSK) asthma medication Advair.

One biopharma bestseller that leapfrogged a lot of other drugs in the market is multiple myeloma medication Revlimid -- aka the drug that built Celgene (CELG). With an entry date of 2008, this drug is the newest one on the list. While Revlimid’s sales are impressive, what’s actually quite exciting is the fact that its projected revenues easily outstrip its already notable sales of $53.69 billion.

By 2024, this Celgene blockbuster is estimated to reach $123.64 billion in sales. There’s a caveat to this though as Revlimid’s success in the years to come is dependent on how Celgene plans to deal with generic competition chomping at the bit and ready to attack once the drug reaches its 2022 patent expiration date.

Another big-ticket drug that might see a bit of a decline in sales soon is from Johnson & Johnson (JNJ). While the company has always been aggressive when it comes to dominating the market for its Crohn's Disease drug Remicade, an investigation by the Federal Trade Commission (FTC) might put a damper on things soon. According to recent reports, JNJ has been suspected of contracting payers to ensure market control and stave off competitors.

Meanwhile, the three horsemen of Roche, namely, Rituxan, cancer and eye disease medication Avastin, and breast cancer treatment Herceptin, reached a collective amount of $365 billion in total sales. These three are anticipated to stay put on top of the industry in the next five years as well, thanks to their competitive pricing and aggressive strategies to protect their patents.

Rounding out the list is Amgen’s Epogen, which is expected to add $107.90 billion to the already astounding $115.87 billion it generated for the company. Meanwhile, GSK’s Advair, which brought in $113.61 billion, is expected to pour in an additional $104.20 billion by 2024.

Interestingly, the majority of the top 10 franchise drugs are biologics except for Sanofi’s (SAN) ulcer treatment Zantac, Bristol-Myers Squibb Co’s (BMY) heart medication Plavix, Advair, and of course, Lipitor. In fact, this is considered as the primary reason for their capability to fight off potential copycats for years.

In some cases, their monopoly of the market has allowed them to expand to include various other indications in their coverage. The massive sales of biologics are also rooted in their ability to demand big-ticket reimbursements. Unlike their generic competitors, brand recognition alone makes it more convenient for patients to ask for compensation.

Needless to say, the success stories of these drugs make it quite obvious why these biopharma companies employ a battalion of legal experts to fend off the rise of generics. While the onslaught of biosimilars cannot be helped, these lawyers ensure that patients opting for these versions of the medication would find it incredibly difficult to ask for biosimilar reimbursements.

One has to be truly impressed with the selloff in biotech and health care stocks over the past year.

Since May, there were signs that life was returning to this beleaguered sector. Then Mylan decided to raise the prices of it's EpiPen by 400% and it was back to the penalty box.

Let?s gouge poor small children who may die horrible deaths if they can?t afford our product. That sounds like a great marketing and PR strategy. NOT!

Once the top performing sectors of 2015, they went from heroes to goats so fast, it made your head spin.

What I called ?The ATM Effect? kicked in big time.

That?s when frightened investors run for the sidelines and sell their best stocks to raise cash. After all, no one wants to sell other stocks for a loss and admit defeat, at least in front of their clients.

It?s not that the companies themselves were without blood on their hands. Valuations were getting, to use the polite term, ?stretched? after a torrid five-year run.

Gilead Sciences (GILD) soaring from $18 to $125?

Celgene (CELG) rocketing from $20 to $142?

It has been a performance for the ages.

If a financial advisor wasn?t in health care, chances are that he is driving for Uber in a bad neighborhood by now.

Then there was The Tweet That Ate Wall Street.

Presidential candidate Hillary Clinton made clear in a broadcast on September 21, 2015 that the health care industry would be target number one in her new administration.

Her move was triggered by an overnight 5000% price hike for a specialty HIV drug by a minor player in the industry.

Among the reforms she would implement are:

1) Give the government power to negotiate drug purchases with the industry collectively.

2) Allow Medicare to import drugs from abroad to encourage price competition (which I already do with my annual trips to Switzerland).

3) Ban drug companies from using government grants to pay for sales and advertising.

4) Set an out of pocket limit for drugs bought through Obamacare at $250 a month, thus ending customers? blank checks.

5) Set a 20% of revenue minimum which companies must spend on research and development.

She certainly got our attention.

Competition in the drug industry? Yikes! Not what the shareholders had in mind.

Raise your hand if you think Americans aren?t paying enough for their prescription drugs.

Yes, I thought so.

Drug company CEOs aren?t helping their case by flying to press conferences to complain about the proposals in brand new $65 million Cessna G-5?s.

And that Mylan CEO, Heather Bresch? She took home $18 million last year, and she?s just a kid.

Here?s the key issue for health care and biotech for investors. It all about politics.

Even if Hillary does get elected, the government is likely to remain gridlocked for another 4-8 years. The Democrats will almost certainly retake the Senate in 2016, thanks to a highly favorable calendar, and keep it for at least two years.

But the heavily gerrymandered House is another story.

With the current districting map, the Democrats would have to win 57% of the national vote for them to regain a majority in both houses.

That is a feat even Barack Obama could not pull off in 2008, when a perfect storm in favor of his party blew in.

A Hillary appointed liberal Supreme Court could bring an end to gerrymandering, but that is a multiyear process. Texas hasn?t had a legal districting map since 2000.

Even with Democratic control of congress, Hillary won?t get everything she wants.

Remember, Obamacare passed by one vote only after a year of cantankerous infighting, and then, only when a member changed parties (Pennsylvanian Arlen Spector).

That means few, if any, Clinton proposals will ever make it into law. If they do, they will be severely watered down and subject to the usual horse-trading and quid pro quos.

Beyond what she can accomplish through executive order, her election may be largely symbolic.

Therefore, the biotech and health care stocks are a screaming ?BUY? at these levels, provided you ignore Mylan (MYL), now the poster boy for corporate greed.

It?s a political call I can only make after spending years in the White House and a half century following presidential elections.

It?s easy to understand why these stocks were so popular, and are found brimming to overflowing in client portfolios and personal 401ks and IRAs.

We are just entering a Golden Age for biotech and health care.

Profit growth for many firms is exceeding 20% a year. Hyper accelerating biotechnology is rapidly bringing to market dozens of billion dollar earning drugs that were, until recently, considered in the realm of science fiction.

And we have only just gotten started. Cures for cancer, heart disease, arthritis, diabetes, AIDS, and dementia? You can take your pick.

Most biotech and health care stocks have given up all of their 2015 gains. Here is a chance to hoover up the fastest growing companies in the US at 2014 prices.

If you missed biotech and health care the first time around, you?ve just been given a second chance at the brass ring.

Here?s a list of five top quality names to get your feet wet:

Gilead Sciences (GILD) ? Has the world?s top hepatitis cure, which it sells for $80,000 per treatment. For a full report, see the next piece below.

Celgene (CELG) ? A biotech firm that specializes in cancer cures (thalidomide) and inflammatory diseases. It also produces Ritalin for the treatment of ADHD.

Allergan (AGN) ? Has the world?s third largest low cost generic drug business. In addition, it has built a major portfolio of drug therapies through more than two dozen acquisitions over the last decade.

Regeneron (REGN) ? Already has a great anti-inflammatory drug, and is about to market a blockbuster anti cholesterol drug that will substantially reduce heart disease.

HCA Holdings (HCA) ? Is the world?s largest operator of for profit health care facilities in the world.

If you want a lower risk, more diversified play in the area, you can buy the Health Care Select Sector SPDR (XLV). Please note that a basket of stocks is going to deliver a fraction of the volatility of single stocks.

Therefore, we have to be more aggressive with our positioning to make any money, picking call option strikes that are closer to the money.

Johnson and Johnson (JJ) is the largest holding in the (XLV), with a 12.8% weighting, while Gilead Sciences (GILD) is the fourth, with a 5.1% share. For a list of the largest components of this ETF, please click: https://www.spdrs.com/product/fund.seam?ticker=XLV.

The other classic play in this area is the Biotech iShares ETF (IBB) issued by BlackRock (click their link: https://www.ishares.com/us/products/239699/ishares-nasdaq-biotechnology-etf ).

Their largest holding is Biogen (BIIB), followed by Gilead Sciences (GILD), Celgene (CELG), Amgen (AMGN), and Regeneron Pharmaceutical (REGN).

I?ll be shooting out Trade Alerts on biotech and health care names as soon as I think the coast is clear.

Until then, enjoy the ride!