Mad Hedge Technology Letter

December 9, 2020

Fiat Lux

Featured Trade:

(HOT TECH IPO YEAR CONTINUES)

(AIRBNB), (DOORDASH)

Mad Hedge Technology Letter

December 9, 2020

Fiat Lux

Featured Trade:

(HOT TECH IPO YEAR CONTINUES)

(AIRBNB), (DOORDASH)

December’s dazzling array of fresh public companies about to hit the markets indicates how strong the tech markets really are.

Many tech firms have returned over 100% year to date.

Aside from the U.S. housing market, tech is the only industry that has strengthened in 2020; and imagine if the economy is rejuvenated by a vaccine, then 2021 could be a year to remember.

Headlining the various tech start-ups coming to market are food delivery app DoorDash Inc. and accommodation platform Airbnb Inc. ready to start trading this week in long-awaited listings.

Not only are they going public, but they also raised their price range with Airbnb valued at as much as $42 billion at the top end of the revised range.

This indicates a healthy appetite to absorb these new shares.

The price target range will be between $56-$60 and at that price, these shares are a no-brainer buy and hold for the long term.

The boosted price targets put both tech companies among the five biggest U.S. IPOs of 2020.

The two companies are hoping to raise a combined $6.2 billion at the top of their price ranges.

IPOs on U.S. exchanges have already raised a record $156 billion this year and much of that is connected to all-time low interest rates which makes sense for corporates to go on a debt binge.

Broader sentiment is starting to really turn with many investors coming back from the sidelines after the market chaos in the early days of the pandemic - and the hoopla over the final outcome of the U.S. election.

Now the uptick in demand is meeting the issuance of shares from Airbnb and DoorDash and this could quickly spiral into a huge surge in shares from these two well-known brands.

That’s not the only action coming to town.

Affirm Holdings Inc., which allows online shoppers to pay for purchases such as Peloton bikes in installments and online video-game company Roblox Corp are next.

It’s highly probable that they score valuations over tens of billions of dollars.

ContextLogic Inc., the parent of online retailer Wish, launched its share sale on Monday. It’s aiming to raise as much as $1.1 billion at a fully diluted valuation of $17 billion.

Airbnb is aiming to be valued at as much as $42 billion in its IPO, while DoorDash could hit a valuation of about $35 billion.

This valuation is more than double DoorDash's private valuation it surpassed in a summer 2020 fundraising round.

The company has been the beneficiary of the insatiable demand for meals delivered to shelter-at-home customers.

Airbnb had been valued at $18 billion after tapping the debt markets in early spring at the height of pandemic delirium.

The company was damaged by the downturn in travel spending and border bans but has recently seen a spike in customers seeking longer-term, domestic rentals.

Airbnb’s IPO is also seen as management’s way to cash out many long-term employees that have stipulations in their contracts that Airbnb must go public by 2021 to profit off their vested shares.

This has been a year to remember for tech IPOs and we are steamrolling into 2021 with a hot debt market and tech unstoppable.

Examples are plentiful such as Enterprise software Snowflake Inc., which has soared more than 200% since its listing to a $110 billion public market valuation.

December’s cohort of soon-to-be public entities - all based in the San Francisco Bay Area – lean towards consumers stuck at home with extra time and cash on their hands.

If the virus can trend downwards as the weather turns hotter in the spring, which is the most likely scenario, that could set a stage for a major reversal in the U.S. economy and tech will be one of the major recipients.

At this point, tech is holding the rest of the market up as energy, retail, transport has tanked.

Even precious metals have been replaced by the digital gold bitcoin in the safe haven trade.

Airbnb is definitely the best of the group and a solid buy on the dip candidate.

The 30% drop in revenue year to date won’t last forever and as they start to mature and rebuild their business as international borders slowly start to open again - this is a strong buy.

Mad Hedge Technology Letter

August 28, 2020

Fiat Lux

Featured Trade:

(THE MISHAP OF THE CENTURY)

(AIRBNB)

The dumbest feeling person in tech right now has to be CEO and Co-Founder of Airbnb Brian Chesky.

The short-term accommodation platform was valued at $31 billion in its last funding round in 2017 and this year was the year that Chesky and Co. had earmarked to go public.

The company was the beneficiary of a secular tech tailwind aided by missteps from a dinosaur hotel industry and carved out a unique product linking hosts and travelers for the purpose of filling in short-term accommodation.

Skirting regulation was the cherry on top.

Airbnb pockets a commission of 6% of the total booking amount, meaning they are overwhelmingly reliant on volume to build sales.

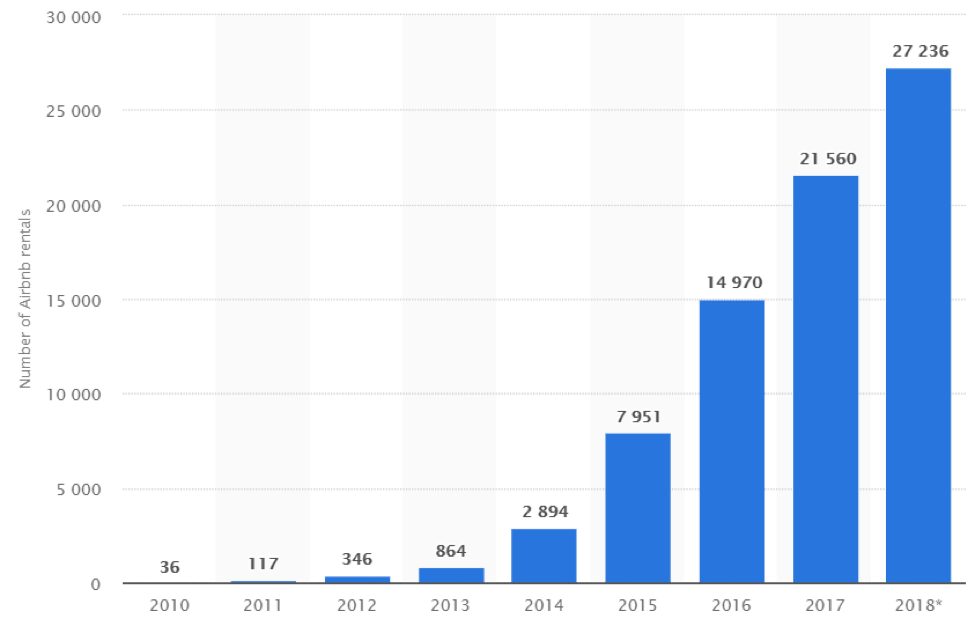

There are more than 7 million homes in 220 countries and regions that have earned over $80 billion since the company started.

Like many things in life – a window of time is all you get.

Last year was that window of time when a smorgasbord of private tech unicorns delivered public markets new tradable assets such as Uber, Peloton, Pinterest, and Lyft.

Even though these stock shares performed worse than expected, it offered long time employees and shareholders a chance to finally cash in.

After going public, any loss from underperforming shares would be absorbed by the public.

Airbnb’s management even had enough time to observe ex-CEO of Uber Travis Kalanick sell off $1.7 billion in stock following the end of the company’s IPO lockup period highlighting the ample period of time Airbnb had to come to the public markets if they wanted to in 2019.

The 2019 loss of $322 million in the first nine months was no big deal and mainly attributed to ramping up marketing.

Then the coronavirus suddenly took the world by storm and everything changed.

Brian Chesky’s arrogance has cost his shareholders $20 billion.

What about the future?

The next “disruptor” of Airbnb could appear in 24 months as well – who knows?

Operations will cost more in 24 months and not less, and a healthy supply of units is not guaranteed to be the same if hosts mass foreclose on properties or a mirror image competitor who attempts to undercut Airbnb appears.

It is rumored that close to 1 out of 3 Airbnb hosts are reliant on their monthly Airbnb income to pay mortgages, which would suggest a poor formula in this type of souring economic climate.

This entire short-term rental industry buttressed by tech platforms could be due for a wholesale washout.

How bad is the situation now?

Airbnb took a hit to the tune of over $50 million in booking revenues over the past several weeks in strategic cities that are close to coronavirus hot zones.

The home-sharing startup’s booking revenues cratered across 17 key international cities over a span of five weeks starting at the beginning of February, and the pain isn’t over yet as cities and countries go into full-blown lockdowns and crisis mode.

At first, it was just China, whose Airbnb’s booking revenues dropped 25%, losing $17.6 million, but that was just the canary in the coalmine.

And that poor number comes in the context of expected growth of roughly plus $30 million if booking revenues had continued growing at the same pace of nearly 35% the firm saw in those markets over the same period last year.

In total, the China business registered a negative swing of nearly $48 million because of the virus.

Even though the virus originated in Wuhan, the contagion quickly spread to Shanghai, Beijing, Seoul, Singapore, Hong Kong and Tokyo wreaking havoc on Airbnb listings.

Western cities are going through the same barrage of Airbnb cancellations and non-bookings in the tourist meccas of Paris, London, Prague, Barcelona, Milan, Rome, and New York.

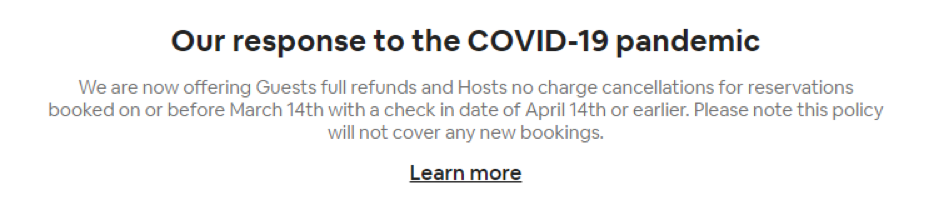

Airbnb has now enacted an extenuating circumstances policy allowing guests to cancel eligible reservations without charge, and the host is required to refund the reservation, irrespective of the previously contracted cancellation policy.

I unquestionably blame Chesky for the bleak situation Airbnb is grappling with in terms of bringing the company to public markets.

They secretly filed for an IPO in 2020 at only half the valuation Airbnb fetched pre-virus.

He failed to do what many unicorn leaders accomplished, which was, by hell or high water, transfer risk to the public market during the late innings of the economic cycle (or before) which we can almost convincingly say ended in January 2020.

Was it worth eking out the extra year or two of growth for another 10% “growth” of incremental value?

The greediness has been exposed and now briskly punished.

Now the company has no room for error while going into full-on damage control for the foreseeable future.

The economic mayhem has put a premium on tech companies with positive cash flow, high margins, competitive advantage, and profits.

A company like Microsoft perfectly illustrates this character set while Airbnb just clung onto its start-up growth model for too long when it easily had the chance to become profitable two years ago.

Avoid Airbnb shares when they hit the public markets – no need to care for damaged goods.

My bet is that ultimately, Google will use this crisis to steal Airbnb’s business and there is nothing they can do about it. They are in the process of developing a property rental platform eerily similar to Airbnb.

Mad Hedge Technology Letter

March 18, 2020

Fiat Lux

Featured Trade:

(LOOK FOR A “V” WITH TECH EARNINGS)

(BABA), (BKNG), (EXPE), (TRIP), (NFLX), (SPOT)

(AMZN), (GOOGL), (TWTR), (SNAP), (PINS)

Expect poor earnings results for almost every tech company as a result of the coronavirus.

The base case for the tech industry is that we are already in the middle of a recession.

The main reason for this is the expected demand/supply disruptions in the wake of Covid-19 that will dramatically drive a wedge in the profit potential which could last through mid-summer.

The silver lining is that the recovery will be robust; but we most likely won’t experience that until the 3rd quarter.

In the short-term, the path of least resistance is more weakness in tech shares, as the U.S. has failed to find enough test kits for possible coronavirus positive patients.

This means that the number of patients infected with coronavirus will be backloaded and as the test kits finally find their way to the masses, the number of sick patients will mushroom.

The Norwegian University of Science and Technology has urged all Norwegians to return home citing a “poorly developed healthcare and infrastructure” as the specific reason to vacate U.S. soil.

It is not possible for tech shares to bottom until there is a strong surge of coronavirus, which is almost a given because of the lax preparation and policy missteps beforehand.

The U.S. is now registering over 1,000 cases per day and growing.

My negative assessment was validated by the U.S. Central Bank, who chose to cut interest rates by 100 basis point and the market opened down 12% following the announcement.

The tech market is now pricing in a slew of bankruptcies and the realization of more pain is forcing sellers to take risk off the table at almost any price.

To hammer my point home, in the time of writing this article, the global number infected by coronavirus jumped from 180,000 to 196,000.

From that quick bump up, the coronavirus cases in the U.S. jumped from 4,538 to 5,853.

The revenue softness will bleed into earnings season and some tech stocks will experience a 20% decline in quarterly revenue and others will fare better with a 2% decline.

A broader problem is the disorderly market malfunctioning pervading through market trading.

Desperate rate cuts and multiple circuit breakers halting the flow of trading are ravaging investor confidence in an American economy that is known for its interconnectedness and integration.

The health solution must have a strong element of isolation and disconnection, meaning the U.S. economy will be sacrificed in the short-term.

Just as baffling, the Central Bank is out of ammunition and will not be able to cure future crises.

The U.S. has no choice but to throw financial stimulus after stimulus to keep companies afloat.

The tech firms facing a larger drop off will be Alibaba Group Holding (BABA), the giant China-based e-tailer, and online travel agency stocks Booking.com (BKNG), Expedia Group (EXPE) and TripAdvisor (TRIP).

Online travel companies face dramatic demand reduction and are the first tech product that gets hacked off in a global and fast-spreading pandemic.

Borders are closed, airlines are practically shuttered, and there is no use case for online travel apps when people are “hunkered down” and advised not to leave their homes.

Alibaba bears the brunt of the COVID-19 crisis, given its entrenched operations in the epicenter of the virus’ initial outbreak, they simply won’t be able to access supplies when factories are locked down and logistics are delayed.

Even Amazon noted that their Prime 1-day delivery was in bad shape because of the same reasons, but they have done well selling out of most household products so don't quite face the same trials of poor tech earnings.

Online ad platforms face a reckoning as well, such as Pinterest (PINS), Twitter (TWTR), and Snap (SNAP) who are dependent on brand advertising and will likely face pullbacks.

These second-tier online ad companies face a slide of around 10% year over year.

The heavy hitters will experience their own type of weakness, with Alphabet (GOOGL) and Facebook facing a 5% revenue drop.

Google’s brand advertising business will face pressure and its travel advertising segment (10-15% of total revenue) will endure significant downside.

Amazon.com (AMZN) will only endure low single-digit number weakness in revenue because many consumers turn to e-commerce ordering at home instead of going out.

Netflix (NFLX) and Spotify Technology (SPOT) are likely to experience immaterial disruptions as well as any top of the line premium digital content that can be devoured at home.

Mad Hedge Technology Letter

March 16, 2020

Fiat Lux

Featured Trade:

(HOW AIRBNB BLEW IT)

(AIRBNB)

The dumbest feeling person in tech right now has to be CEO and Co-Founder of Airbnb Brian Chesky.

The short-term accommodation platform was valued at $31 billion in its last funding round in 2017 and this year was the year that Chesky and Co. had earmarked to go public.

The company were the beneficiary of a secular tech tailwind aided by missteps from a dinosaur hotel industry and carved out a unique product linking hosts and travelers for the purpose of filling in short-term accommodation.

Airbnb pockets a commission of 6% of the total booking amount, meaning they are overwhelmingly reliant on volume to build sales.

There are more than 7 million homes in 220 countries and regions that have earned over $80 billion since the company started.

Like many things in life – a window of time is all you get.

Last year was that window of time when a smorgasbord of private tech unicorns delivered public markets new tradable assets such as Uber, Peloton, Pinterest, and Lyft.

Even though these stock shares performed worse than expected, it offered long time employees and shareholders a chance to finally cash in.

After going public, any loss from underperforming shares would be absorbed by the public.

Chesky gloated that a need for cash wasn’t driving the company to go public, but rather a desire to give investors the option to sell their stock now that Airbnb is more than ten years old.

Airbnb’s management even had enough time to observe ex-CEO of Uber Travis Kalanick sell off $1.7 billion in stock following the end of the company’s IPO lockup period highlighting the ample period of time Airbnb had to come to the public markets if they wanted to in 2019.

The 2019 loss of $322 million in the first nine months was no big deal and mainly attributed to ramping up of the marketing side of the business to add the final gloss to the lips before finally delivering dollars back to the stakeholders.

Then the coronavirus suddenly took the world by storm and the world changed.

It is highly probable that Brian Chesky’s lack of urgency means that Airbnb management has botched the best and last window of opportunity to go public – the window is now officially closed.

No tech company will go public in 2020 unless there is a sudden 180-degree turnaround in market sentiment which will only happen if the coronavirus disappears tomorrow - which it won’t.

Airbnb’s investors and long-time workers will still be patiently waiting for their big payday.

Even if you hit on the argument that the travel industry will rebound with zeal within 24 months, industry competition and the dynamics in this sphere will likely be more cutthroat, and not less.

The next “disruptor” of Airbnb could appear in 24 months as well – who knows?

Operations will cost more in 24 months and not less, and a healthy supply of units are not guaranteed to be the same if hosts mass foreclose on properties or a mirror image competitor who attempt to undercut Airbnb appears.

It is rumored that close to 1 out of 3 Airbnb hosts are reliant on their monthly Airbnb income to pay mortgages which would suggest a poor formula in this type of souring economic climate.

This entire short-term rental industry buttressed by tech platforms could be due for a wholesale washout.

How bad is the situation now?

Airbnb took a hit to the tune of over $50 million in booking revenues over the past several weeks in strategic cities that are close to coronavirus hot zones.

The home-sharing startup’s booking revenues cratered across 17 key international cities over a span of five weeks starting at the beginning of February, and the pain isn’t over yet as cities and countries go into full-blown lockdowns and crisis mode.

At first, it was just China, whose Airbnb’s booking revenues dropped 25%, losing $17.6 million, but that was just the canary in the coalmine.

And that poor number comes in the context of expected growth of roughly plus $30 million if booking revenues had continued growing at the same pace of nearly 35% the firm saw in those markets over the same period last year.

In total, the China business registered a negative swing of nearly $48 million because of the virus.

Even though the virus originated in Wuhan, the contagion quickly spread to Shanghai, Beijing, Seoul, Singapore, Hong Kong and Tokyo wreaking havoc on Airbnb listings.

Western cities are going through the same barrage of Airbnb cancellations and non-bookings in the tourist meccas of Paris, London, Prague, Barcelona, Milan, Rome, and New York.

Airbnb has now enacted an extenuating circumstances policy allowing guests to cancel eligible reservations without charge, and the host is required to refund the reservation, irrespective of the previously contracted cancellation policy.

February’s numbers make March’s numbers look radiant as the company is staring in the face of revenue down 85-90% in many important markets for the month of March.

And just to put the stake through the heart, it’s not only Airbnb dealing with the downturn in bookings. Expedia Group, which owns VRBO, Hotels.com, has revealed it expects a $40 million hit to operating profit in the first quarter.

The damage is broad-based and the worst of the contagion has not hit U.S. shores yet, which could culminate in a lockdown of strategic U.S. cities as well worsening Airbnb’s fiscal outlook.

I unquestionably blame Chesky for the bleak situation Airbnb is grappling with in terms of bringing the company to public markets.

He failed to do what many unicorn leaders accomplished, which was, by hell or high water, transfer risk to the public market during the late innings of the economic cycle (or before) which we can almost convincingly say ended in January 2020.

Was it worth eking out the extra year or two of growth for another 10% “growth” of incremental value?

The greediness has been exposed and now briskly punished.

Apparently, the risk was worth it in his eyes and now the company has most likely lost over half its value in 2 weeks.

Now the company has no room to fail while going into full-on damage control for the foreseeable future and hopes it can still go public during the next window of opportunity, whenever that will be.

It is yet to be determined if Airbnb will have illogical management at the helm next time around.

This is really the death of the tech IPO for this economic cycle – put a fork in it.

Mad Hedge Technology Letter

March 14, 2019

Fiat Lux

Featured Trade:

(AIRBNB’S SECOND THOUGHTS),

(AIRBNB)

In an unusual U-turn, Airbnb co-founder Nathan Blecharczyk revealed sudden skepticism on his companies’ odds of going public in 2019.

The base case was that Airbnb was on schedule to be listed in mid-2019.

Blecharczyk fueled confusion by going on record saying that Airbnb “are taking the steps to be ready to go public in 2019. That doesn’t mean we will go public in 2019.”

The company is currently valued at $31 billion.

The co-founder resisted in offering a specific explanation in why the company is hesitant in pulling back from the public market, but part of the factors could boil down to the Brexit mess currently ongoing at 10 Downing Street and the trade war between America and China creating uncertainty around crucial Airbnb housing markets.

Executing the IPO is another quandary where the Securities and Exchange Commission (SEC) shuttered its IPO division during the government shutdown and its staff has not regained full capabilities.

The global economic slowdown has made IPO investors nervous and the slew of IPOs planned for 2019 could take rolling rain checks to ensure the stability of newly minted shares.

This is not the only problem roiling Airbnb.

Taxes.

Municipalities are sick of being shafted from the outsized revenues pocketed by Airbnb.

Hotels have been incessantly complaining that they are on the leash for taxes that Airbnb does not have to face even though they are directly competing.

Things are about to change.

Let’s take the state of Maryland as an example.

Hosts are now pre-warning potential guests that they are on the hook for 15.5% in taxes upon arrival.

The sticker shock could have the effect of killing demand or reducing it severely.

Another bill before the Senate Budget and Taxation Committee would force short-term rental brokers to collect the 6% Maryland sales and use tax at the time of booking and pass on the fees to the state.

And this is just the beginning when you consider the onslaught of regulation other states are grappling with.

Take for instance, Maryland’s neighbor Washington D.C.

The capital has come down heavy-handed on the short-term rental platform forbidding property owners renting out 2nd homes.

They have also limited the days owners can rent out their house if they are not currently present in the city forcing owners to stick around to maximize revenue.

As of now, D.C. taxes Airbnb and other short-term rental companies 14.5% and the company has aired its grievances claiming favoritism towards the local hotel industry.

City councilors have cited figures as much as $96 million over four years of potential lost taxes.

Airbnb has been painted as the scapegoat by many jurisdictions around America when you consider that traditional hotels are taxed at 13% if averaged out in the largest 150 cities.

In many cases, Airbnb is treated not as a hotel and is responsible to self-report its occupancy and revenue data giving them a chance to find loopholes to push large amounts of revenue streams through unscathed.

Governments are also dealing with additional headaches of a wave of displacement for regular payroll jobs because of the domination of Airbnb units.

This whole situation will go from bad to worse because local government is frothing at the mouth when they understand the potential tax windfall they could seize from these online platforms.

Whether legitimate or not, states could cite taxes on hotels as a starting point and start purging Airbnb of revenue through cumbersome charges, fees, licenses, penalties, and regulation.

Airbnb could end up with a bunch of Miami Beach markets on their books with the situation on the ground turning into a slugfest.

The state is at war with property owners who rent out their unit short-term with owners trying to skirt the law.

Any rentals of less than 6 months have been illegal in Miami for years.

Fines were small amounts just three years ago but the tsunami of demand to rent units at tourist hot-spots has ignited the debate of short-term rentals and the pros and cons to business and the community.

The fines have exploded to $20,000 for each citation and the local government has bombarded owners with over $8 million in fines since 2016.

Complicating the matter, owners are often not even the culprits renting out the units.

Tenants who sign up for legitimate leases are running the show themselves muddying the situation in who is liable for the fine – the owner or the tenant?

Short-term rentals have generated over $10 million in taxes to Miami-Dade County in 2018, but the state is continuing to take the stance that this tax would have flooded their coffers plus more from hotels.

This sets up a dire situation in which Airbnb will need to report quarterly earnings 4 times per year and explain to analysts and investors alike the state of regulations and engagement with authorities.

I believe the situation will deteriorate with both sides entrenching more looking to get what they want potentially turning into a legal circus.

Tech firms are known to play hardball and brinkmanship encourages rapid growth, however, this will be harder as a public company.

Airbnb is on the way to ex-growth as mounting financial and regulatory burdens are engulfing the firm.

Better to get their ducks all in a row and supercharge growth one last time before the founders finally get their big payday.

Delaying the IPO is a risky move, but if they can squeeze out a few local victories from a New York, London, or another high market revenue driver and the fact they have been cash flow positive for the last few years, look for them to rush into the IPO and cash out.

And when that time comes, Airbnb’s ultimate competitive advantage of paying minimal taxes in many locales could be dead and buried and the company might become a shell of its former self.

I’ve seen crazier things happen.