Mad Hedge Technology Letter

November 17, 2023

Fiat Lux

Featured Trade:

(CATCHING OPTIMAL ENTRY POINTS IN TECH)

(AMAT), (SMIC)

Mad Hedge Technology Letter

November 17, 2023

Fiat Lux

Featured Trade:

(CATCHING OPTIMAL ENTRY POINTS IN TECH)

(AMAT), (SMIC)

Buy Applied Materials (AMAT) on the dip.

That was my conclusion after hearing this chip-making stock nose-diving by the most in almost a year.

Rarely do traders get such a good entry point into such a high-quality name.

AMAT has been around forever and it is a tried and tested chip brand that produces high-quality equipment.

It’s noteworthy that a report showed that AMAT faces a US criminal investigation for allegedly violating export restrictions to China, but it’s a storm in a teacup.

It’s not such a big deal, because the bad news will get discounted quickly and the US will probably give AMAT a light slap on the wrist.

It makes no sense to destroy a company that is critical to national security infrastructure.

Maybe a few executives will get laid off and then we move on.

After this issue is swept under the carpet, it’s all systems go for AMAT.

The company is being probed by the Justice Department over dealings with China’s biggest chipmaker, Semiconductor Manufacturing International Corp.

The department is considering whether Applied Materials sold hundreds of millions of dollars of equipment without the proper licenses.

Chip companies are operating under increasingly strict rules imposed by Washington on exports of chip technology to China.

Acquiring licenses to send certain types of machines to Asia is a sign of the times and how national governments are desperate to keep technological know-how in the state.

Applied Materials produced chipmaking gear in Gloucester, Massachusetts, and then shipped it to a subsidiary in South Korea.

It then went to China’s SMIC, the people familiar with the investigation said.

SMIC was placed on a so-called entity list in December 2020 by the Department of Commerce, which cited alleged links between the chipmaker and China’s military.

Semiconductor manufacturers order machinery from Applied Materials and its peers well ahead of opening new factories, which can take more than a year to build and equip.

Though the chip industry has been contending with a slowdown in personal computers and smartphones, Applied Materials Chief Executive Officer Gary Dickerson has argued that artificial intelligence computing will fuel a new surge in demand.

Semiconductor equipment companies have been hurt by weak demand from memory chip makers, which are enduring an industry glut.

Luckily, the savior is AI and its insatiable demand for high-end processors.

China has been one of the fastest-growing markets for chip equipment. But the US restrictions have put a wet towel on the business relationship.

Uncertainty is the keyword here, but if AMAT keeps producing world-class equipment, it will accrue value in almost any financial market.

I am comfortable recommending AMAT now and the discount certainly makes it look more attractive.

Once AMAT acquires a license to sell to the Chinese, this will be forgotten.

The demand for conventional chips and AI chips is leading the charge and even though there is a glut of non-AI chips, AI chips will lead the charge in the short term before consumer demand comes back.

This is the forefront of technology and readers should grab a piece of it.

When Elon Musk personally invited me to tour his Gigafactory in Sparks, Nevada, I thought, “How could I pass on this?” He had read my recent report on Tesla and thought the more I know about Tesla the better.

I couldn’t agree more.

As I approached the remote facility 20 miles east of Reno, I spotted a herd of wild Mustangs on the red volcanic hills above. I thought it was a great metaphor for our rapidly evolving transportation system, from horse to all-electric in 100 years.

There are no signs to the Gigafactory until you approach the main gate. I had to find it with my GPS after inputting longitude and latitude. When you upset the apple cart for the global energy system, you make a lot of enemies. Once in, no cameras are allowed.

What I found inside what much what I saw at the original Fremont, CA factory 15 years ago: an army of robots building machines. The factory is in effect a machine that makes machines….by the millions. Occasionally, a worker would swan past with an oil can in his hand and squirt some lubricant into an important joint, then swan away.

If you want a view of the future, this is it.

Elon does nothing small.

The present factory occupies about 2 million square feet, or about 33 football fields. Some 60% of the world’s lithium-ion batteries come out of this one place right now, which are devoted to Tesla Model 3’s and Powerwalls, of which I own six. Japan’s Panasonic, which has the contract to supply the batteries, occupies a substantial part of the factory space.

When completed, it will occupy 6 million square feet, making it the world’s largest building. The planet’s greatest solar array sits on top, making the entire facility energy neutral when combined with local windmills. The plant is fully automated and runs 24/7. There are still a few of those pesky humans around to perform complex tasks which robots can’t do….yet.

The State of Nevada just granted Tesla a ten-year tax holiday to start the second phase, which will employ another 5,000. Whole cities are being carved out of the virgin desert to accommodate them, so the entire city of Reno is rapidly marching east. Burger Kings, Taco Bells, Subways, and Chinese and Mexican restaurants are popping up in the middle of nowhere.

It's all coming into place to assure that Tesla meets its 1.8 million vehicle target for 2023, up 40% from 2022. The last time someone had a technology lead this great was in 1913 when Henry Ford launched assembly lines that mass-produced Model T’s for the first time. He offered them for $400 each and doubled his workers’ pay to $5 a day to buy them. This gave Ford a 75% share of the US car market for two decades.

Elon Musk will achieve the same.

Which all raises a much larger issue.

The future is happening far faster than anyone realizes.

Tesla is just the tip of the iceberg in an AI/automation trend that is rapidly taking over the world. The net effect will be to double or triple the value of the companies that embrace these trends and wipe out those that don’t. ALL companies are AI plays. This is a large part of my Dow 240,000 in a decade prediction.

Microsoft brought out its office in 1990 and it instantly made ALL companies more valuable as they adopted it. The Dow Average soared by 20 times from $600 to $12,000. The same thing is going on now with AI.

If it worked before it will work again. A 20-fold return from here takes the Dow Average from $34,000 to $680,000, except it will happen much more quickly as technology is hyper-accelerating. Dow 240,000 looks like a chipshot.

If you think this is some kind of George Lucas THX 1138 prediction, think again. These are headlines I saw in the last week.

FedEx (FDX) is firing 86,000 drivers, to be replaced by robots. Uber (UBER) is replacing its 5 million drivers with autonomous drivers to increase reliability and cut costs. Dentists adopting AI to read X-rays are catching the 12% of cavities they miss, increasing fillings and increasing profits.

I often get asked for great AI plays in the market and there are no direct ones. But in five years, companies like Microsoft’s (MSFT) ChatGPT and Alphabet’s (GOOGL) DeepMind Technologies will be spun off and sold at enormous multiples to the public, creating a frenzy.

I’ve seen it all before.

What does doubling or tripling the value of surviving companies do to the economy? It reliquefies the financial system with immense corporate cash flows. All asset classes will rocket in value, including stocks, bonds, commodities, precious metals, energy, and real estate.

While the 2010s had endless quantitative easing and zero interest rates, the 2020s will have AI and robots. Except that this time we won’t have to rely on government handouts to get there.

Suddenly, Dow 240,000 looks cheap.

I just thought you’d like to know.

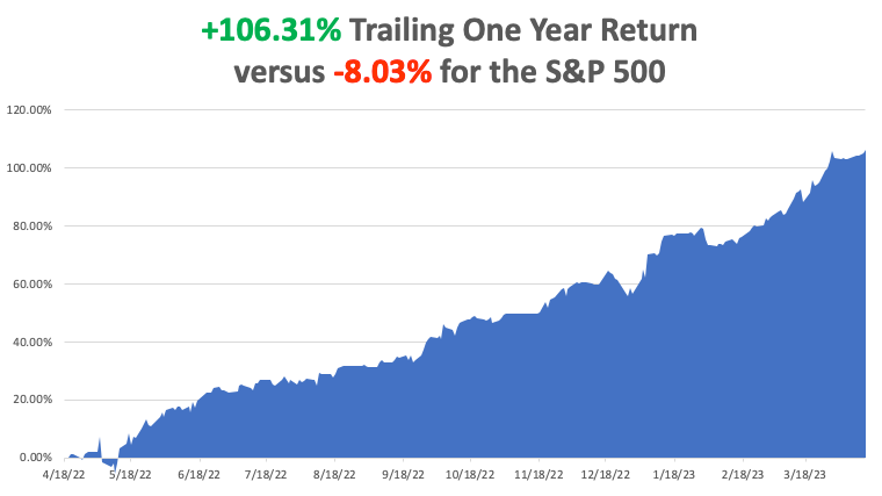

My big bet-the-ranch long in banks and brokers paid off huge. My 2023 year-to-date performance is now at an incredible +49.57%. The S&P 500 (SPY) is up only a miniscule +8.42% so far in 2023. My trailing one-year return maintains a sky-high +106.31% versus -8.03% for the S&P 500.

That brings my 15-year total return to +646.76%, some 2.73 times the S&P 500 (SPY) over the same period. My average annualized return has blasted up to +48.51%, another new high.

I executed four trades last week. I used the spectacular earnings beat at (JPM) to take profits and rolled that money into Boeing (BA), which had just been trashed. I also took profits on my expiring April bond long (TLT) and rolled it into a May bond long. I will run my remaining expiring April long positions in (TSLA), (BAC), (C), (IBKR), (MS), (and FCX) into the Friday, April 21 expiration.

Inflation Takes a Dive, dropping to a 5.6% YOY rate, the ninth consecutive month of decline. I think we will fall to 3%-4% by yearend, prompting the Fed to lower interest rates. That will spark a new bull market and another leg up for residential real estate. It all more fodder for the bull case. Given what the Fed has been facing, a mild recession would be a huge win.

Fed Minutes Fear Banking Crisis May Lead to a Mild Recession, killing off today’s nascent rally. It will also hobble job growth and lead to sharp declines in interest rates in 2024. Markets now see a 75% probability of a 25-basis point rate hike on May 3.

FedEx Looking to Fire All Drivers, moving to autonomously driven delivery vehicles. It may take 20 years but it’s in the works. (FDX) has already cut 12,000 jobs since June in an effort to maintain profitability and surpass rival (UPS). In 2022, (FDX) took in $93.5 billion in revenues delivering 3 billion packages, 9 for each American. I received more than my share.

PC Sales Drop 29% YOY, in Q1, adding more ammunition to the recession camp. Apple Macs led the charge to the downside with a heart-thumping 40% decline. The news slugged (AAPL). Only 56.9 million PCs we sold during the last quarter. Even with heavy discounting inventories remain high. Amazing, isn’t it?

Tesla Cuts Prices Again, knocking $3,000 off the Model 3 and $5,000 for the Model X. That sets the cat among the pigeons with traditional car companies desperately trying to catch up. Tesla is simply passing on the 50% drop in lithium prices this year. If they flush competitors out of business in the meantime so much the better. Ford has ordered designers to cut the number of parts by 80%, which Tesla did 14 years ago. (F) and (GM) are just too slow to react, even when the writing is on the wall.

$1.5 Trillion in Commercial Real Estate Debt coming due is a Threat to all asset classes. Refi’s are coming due that will double or triple interest rates from the zero-rate era and many won’t qualify. The sector is already being hammered by the “stay-at-home” work trend, with big tech firms virtually vacating whole office building in San Francisco. Regional banks may no longer have the capital to roll over at any prices given recent massive deposit withdrawals. Avoid commercial real estate REITS.

Banks Shares Explode to the Upside. JP Morgan announced blockbuster earnings, taking the stock up a ballistic $11, or 8.6%. Revenues came in at $39.34 billion versus an expected $36.19 billion. Adjusted EPS was $4.32 a share versus an expected $3.41. It is the biggest gap up in share prices on an earnings announcement in 20 years. As a result, we are just short of the maximum profit in our long (JPM), with the shares up an eye-popping 21% from the nearest strike price.

PPI Gives Another Deflation Hint, dropping a shocking 0.5% in March to only a 2.7% YOY rate. That’s a big drop from 4.9% in February. It’s the lowest inflation indicator in two years. Stocks loved the news, jumping $383. Low inflation, and therefore sharp interest rate cuts are coming within reach.

Boeing Goes Back in the Penalty Box, with a recurring bulkhead problem halting 737 MAX production. The stock dumped 8%. Buy (BA) on the dip. They’ll fix it. The company has a massive order backlog of 4,000 planes and will crush it on the earnings. The 737 MAX will shortly be flying again, the company’s largest selling product. With the airline business booming a global aircraft shortage has emerged. The end of the trade wars with China will bring a resurgence of orders there. And Boeing just surpassed Airbus in aircraft deliveries in Q1

Weekly Jobless Claims Jump 11,000 to 239,000, showing that the Fed’s harsh medicine is starting to work. It’s all consistent with a stock market that may start to roll over soon.

Private Sector Payrolls Slow to 145,000, according to ADP, a substantial drop from the previous month. Financials took the big hit with a loss of 51,000 jobs, followed by Business Services at 46,000. Leisure & Hospitality leads again with a 98,000 gain. It is more evidence of the economic slowdown the FED has been attempting to engineer for the past year.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, April 17 at 7:30 AM EST, the New York State Manufacturing Index is out.

On Tuesday, April 18 at 6:00 AM, the US Building Permits are announced.

On Wednesday, April 19 at 11:00 AM, the Fed Beige Book is printed.

On Thursday, April 20 at 8:30 AM, the Weekly Jobless Claims are announced. Existing Home Sales are out.

On Friday, April 21 at 8:30 AM, the Global Composite Flash PMI is released. We also get the April options expiration at the 4:00 PM stock market close.

As for me, I don’t get invited to help design new nuclear weapons systems very often. So when the order came from Washington to report to Los Alamos, New Mexico, I was on the next plane.

When the Cold War ended in 1992, the United States judiciously stepped in and bought the collapsing Soviet Union’s entire uranium and plutonium supply.

For good measure, my client George Soros provided a $50 million grant to hire every Soviet nuclear engineer. The fear then was that starving scientists would go to work for Libya, North Korea, or Pakistan, which all had active nuclear programs. There ended up here instead.

That provided the fuel to run all US nuclear power plants and warships for 20 years. That fuel has now run out and chances of a resupply from Russia are zero. The Department of Defense attempted to reopen our last plutonium factory in Amarillo, Texas, a legacy of the Johnson administration.

But the facilities were deemed too old and out of date, and it is cheaper to build a new factory from scratch anyway. What better place to do so than Los Alamos, which has the greatest concentration of nuclear expertise in the world.

Before they started, they launched a nationwide search for those who were still alive and had nuclear expertise the last time we made our own plutonium, and they came up with….me?

Los Alamos is a funny sort of place. It sits at 7,320 feet on a mesa on the edge of an ancient volcano so if things go wrong, they won’t blow up the rest of the state. The homes are mid-century modern built when defense budgets were essentially unlimited. As a prime target in a nuclear war, there are said to be miles of secret underground tunnels hacked out of solid rock.

You need to bring a Geiger counter to garage sales because sometimes interesting items are work castaways. A friend almost bought a cool coffee table which turned out to be part of an old cyclotron. And for a town designing the instruments to bring on the possible end of the world, it seems to have an abnormal number of churches. They’re everywhere.

I have hundreds of stories from the old nuclear days passed down from those who worked for J. Robert Oppenheimer and General Leslie Groves, who ran the Manhattan Project in the early 1940s. They were young mathematicians, physicists, and engineers at the time, in their 20’s and 30’s, who later became my university professors. The A-bomb was the most important event of their lives.

Unfortunately, I couldn’t relay this precious unwritten history to anyone without a security clearance. So, it stayed buried with me for a half century, until now. Suddenly, I had an entire room of young scientists who were fair game, and it was fun relaying stories, they hung on my every word. It was like being a Revolutionary War buff and out of the blue you meet someone who knew George Washington.

Some 1,200 engineers will be hired for the first phase of the new plutonium plant, which I got a chance to see. That will create challenges for a town of 13,000 where existing housing shortages already force interns and graduate students to live in tents. It gets cold at night and dropped to 13 degrees F when I was there.

As a reward for my efforts, I was allowed to visit the Trinity site at the White Sands Missile Test Range, the first visitor to do so in many years. This is where the first atomic bomb was exploded on July 16, 1945. The 20-kiloton explosion set off burglar alarms for 200 miles and was double to ten times the expected yield.

Enormous targets hundreds of yards away were thrown about like toys (they are still there). Half the scientists thought the bomb might ignite the atmosphere and destroy the world but they went ahead anyway because so much money had been spent, 3% of the US GDP for four years. Of the original 100-foot tower, only a tiny stump of concrete is left (picture below).

With the other visitors, there was a carnival atmosphere as people worked so hard to get there. My Army escort never left me out of their sight. Some 78 years after the explosion, the background radiation was ten times normal, so I couldn’t stay more than an hour.

Needless to say, that makes uranium plays like Cameco (CCJ), NextGen Energy (NXE), Uranium Energy (UEC), and Energy Fuels (UUUU) great long-term plays, as prices will almost certainly rise and all of which look cheap. US government demand for uranium and yellow cake, its commercial byproduct, is going to be huge. Uranium is also being touted as a carbon-free energy source needed to replace oil.

I know the numbers, but I can’t tell you as they are classified. Otherwise, I’d have to kill you and you might not renew your subscription to Mad Hedge Fund Trader.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

At Ground Zero in 1945

What’s Left of a Trinity Target 200 Yards Out

Playing With My Geiger Counter

Atomic Bomb No.3 Which was Never Used

What’s Left from the Original Test

Global Market Comments

April 10, 2023

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD,

or MAD HEDGE CLOCKS 46.38% PROFIT IN Q1)

(TSLA), (USO), (WMT), (AAPL), (GLD), (GOLD), (SLV),

(UUP), (TLT), (UBI), (NVDA), (MU), (AMAT), (CCJ)

CLICK HERE to download today's position sheet.

How much pain to take?

That is the question plaguing traders and portfolio managers alike around the world. For the average bear market is only 9.7 months long and we are already 16 months into the present one.

Even the longest postwar bear market was only 2.5 years, or 30 months, the 2000-2002 Dotcom Bust, and we are nowhere near that level of economic hardship. Back then, companies posted losses for several quarters in a row, and many ceased to exist (Webvan, Alta Vista, Pets.com).

That means we only have a few more months of pain to take before another decade-long bull market resumes, or 8 months if the bear stretches to a full two years.

That is unless the new bull was actually born last October, which is entirely possible. Certainly, the stock market thinks so, with its refusal to drop on even the worst of news.

Inflation at 6%? Who cares.

A Fed that hates the stock market? Couldn’t give a damn.

Pathetic earnings growth? Call me when it’s over.

This indifference chalked up the deadest trading week I can remember, putting the Volatility Index (VIX) firmly back into “Do Nothing Land” under 20%.

So investors are cautiously putting cash into stocks on every dip, even minor ones, confident that they will be higher by yearend. If a black swan arrives in the meantime, or a political crisis boils out of control, tough luck if you can’t take a joke.

All of which is focusing a lot more attention on gold (GLD), which moved within 2% of a new all-time high last week. I am always looking for cross-asset class confirmations of current trends and the barbarous relic has certainly been one of those.

I have been bullish on gold since I put out LEAPS on Barrick Gold (GOLD) and silver (SLV) last October. They have since performed spectacularly well. The move into precious metals confirms the following. That the Fed tightening cycle will end imminently. Interest rates will fall, and the US dollar (UUP) will weaken. Everything else flows from there.

You are even seeing this in US Treasury Bond yields, with the ten-year plunging to 3.30%, a one-year low. The (TLT) hit $109 last week. Aren’t bonds supposed to be held back by the looming default by the US government?

I’m starting to wonder if the debt ceiling crisis is this generation’s Y2K. At worst, your toaster may show the wrong year but nothing further. Or maybe the pent-up demand for bonds and high yields is so great that it overwhelms all other considerations?

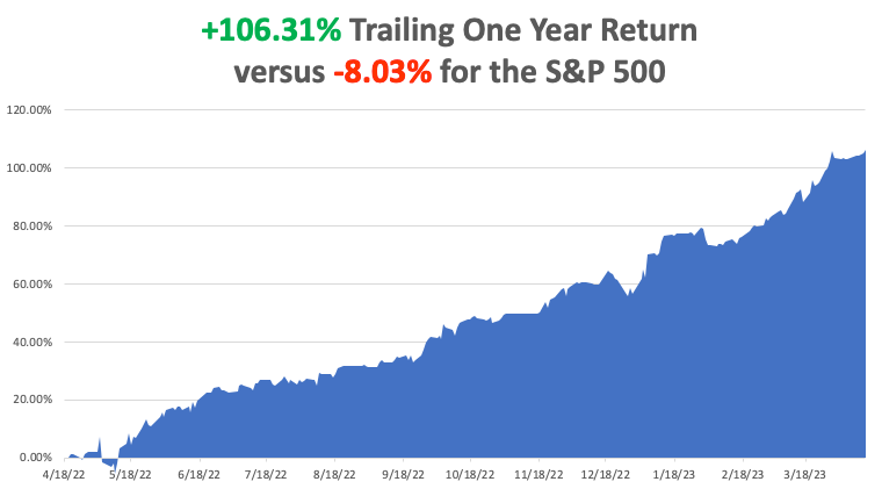

My 2023 year-to-date performance is now at an incredible +46.38%. The S&P 500 (SPY) is up only a miniscule +7.0% so far in 2023. My trailing one-year return maintains a sky-high +103.2% versus +7.0% for the S&P 500.

That brings my 15-year total return to +643.57%, some 2.71 times the S&P 500 (SPY) over the same period. My average annualized return has blasted up to +48.26%, another new high.

I executed no trades during the holiday-shortened week, content to run my ten profitable positions into the April 21 options expiration. If a strategy ain’t broke, don’t fix it. If I see something I like, I’ll take profits on an existing position and replace it with a new one.

Nonfarm Payroll Report Holds Up, at 236,000 in March, the lowest since December 2020. It shows that high interest rates still have not impacted the jobs market. February was revised up to 326,000. The headline Unemployment Rate dropped back to a 50-year low at 3.5%. Average Hourly Earnings dropped to 4.2% YOY, a two-year low, showing that inflation is in retreat. Leisure & Hospitality led at 74,000 followed by Government at 47,000.

Weekly Jobless Claims Drop, to 228,000, down 18,000 as recession fears rise. High interest rates are finally taking their toll, with a banking crisis thrown in for good measure.

Open Jobs Tighten, The June JOLTS survey of job openings fell to 10.698 million, down from 11.3 million last month and well below expectations of 11 million. Is this the calm before the storm when job openings disappear? This report is highly negative for the US dollar.

Tesla (TSLA) Posts Record EV Deliveries, Deliveries grew 36% from a year ago, below the 50% growth Elon Musk promised for the year on the last earnings call, but Musk has a habit of overpromising. The expansion is still a healthy sign that consumers are spending. Any pullback in Tesla is a gift for shareholders.

Oil (USO) Production Cut Sends Price Soaring, with OPEC+ including Russia has pledged a total of 3.66-million-barrel oil output cut which is nearly 3.7% of global demand. The jump in oil price will only accelerate global inflation and force the Fed into a tougher predicament. The Saudi – US cooperation is at its lowest ebb.

Walmart’s (WMT) Automation Effort Goes Into Overdrive, Walmart said it expects around 65% of its stores to be serviced by automation by 2026. The company said around 55% of packages that it processes through its fulfillment centers will be moved to automated facilities and unit cost average could improve by around 20%. This is the first step to getting rid of human employees. Eventually, the government will need to deliver universal basic income (UBI).

Gold and Miners Threaten New All-Time Highs, suggesting that a collapse in interest rates is imminent. So is an economic recovery and a resurgence of monetary expansion. Russian and China continue to be major buyers to evade sanctions. Keep buying (GLD) and (GOLD) on dips.

Apple (AAPL) Cash Hoard Soars to $165 Billion, as the cash flow king of all time goes from strength to strength. This will be one of the top targets in any tech rebound, which may be imminent. But you’re have to compete with apple to buy the shares, which is a huge buyer of its own stock.

Chip Stocks are On Fire, clocking the best sector of any in Q1. Too far, too fast, say I, but I’ll be in there buying with both hands on any serious dips. This is no future without (NVDA), (MU), and (AMAT) playing a major role.

Stock Dividends Hit New All-Time Highs, at $146.8 billion, up 7% YOY. As interest rates rose, companies had to raise dividends to keep up. The economy is also far stronger those most realize, with many analysts believing we should have entered a recession a long time ago. A high dividend also gives downside protection in bear markets.

Uranium Demand is Surging with the Nuclear Renaissance. And now the US is restarting plutonium production for the first time in 20 years, a uranium derivative. The 20-year supply we bought from the old Soviet Union has run out with a scant chance of renewal. The Los Alamos Labs in New Mexico is seeking to hire 1,200 engineers to build a brand-new factory from scratch. Buy (CCJ) on dips. And buy Los Alamos real estate if you can get a security clearance.

Keep Buying 90-Day T-Bills, now pushing a 5% risk-free yield. The regional banking crisis highlights another reason. If your bank or broker goes under, your cash deposits can be tied up in bankruptcy for three years. If you own US government securities, they can be ordered and transferred out in days to another institution. You can also buy them directly from the US government free of fee. Just thought you’d like to know.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, April 10 at 7:30 AM EST, the Consumer Inflation Expectations are out.

On Tuesday, April 11 at 6:00 AM, the NFIB Business Optimism Index is announced.

On Wednesday, April 12 at 7:00 AM, the US Core Inflation Rate and Consumer Price Index are printed.

On Thursday, April 13 at 8:30 AM, the Weekly Jobless Claims are announced. The Producer Price Index is also released.

On Friday, April 14 at 8:30 AM, the US Retail Sales are released.

As for me, I covered the Persian Gulf for Morgan Stanley for ten years during the 1980s when medieval sheikdoms still living in the 14th century were suddenly showered with untold wealth. Needless to say, the firm, which we called Morgan Stallion, had a few ideas on what they should do about it.

I was picked as the emissary to the region because I had already been visiting the Middle East for 20 years and had been doing business there for 15 years. My press visa to cover the Iran-Iraq War was still valid.

In addition, I had already developed a reputation for being wild, reckless, and up for anything to enjoy a thrill or make a buck. In addition, with all the wars, terrorist attacks, and revolutions underway, everyone but me was scared to death to go near the place.

In other words, I was perfect for the job.

Being a veteran combat pilot proved particularly useful. I used to fly down on Kuwait Airlines and I still have a nice collection of the cute little Arabic artifacts they used to hand out in first class. Once in Abu Dhabi, I rented a local plane and hopped from one sheikdom to the next drumming up business. Once, I landed on a par five fairway at a private golf course just to give a presentation to a nation’s ruler.

My last stop was always Kuwait, where I turned the plane back in and met the CIA station chief for lunch to fill him in on what I had learned. It was all considered part of the job. When Iraq invaded Kuwait in 1991, I was their first call.

Of course, flying across vast expanses of the Arabian desert is not without its risks. Whenever you fly a single-engine plane you are betting your life on an internal combustion engine, never a great idea. I always carried an extra gallon bottle of water in case of a forced landing. The survival time without water is only three days.

Whenever I refueled, I filtered the 100LL aviation gas through a chamois cloth to keep out water and sand. Still, I was pretty good at desert survival, growing up near Indio California in the Lower Colorado Desert and endlessly digging my grandfather’s pickup truck out of the sand.

Once my boss tried to ban me from a trip to the Middle East because the US Navy had bombed Libya. I assured him that something as minor as that didn’t even move the needle on the risk front, at least in my lifetime.

The problem with the Persian Gulf was that they had all the money in the world and no way to spend it. An extreme Wahabis religion was strictly adhered to, and alcohol was banned. But you could have four wives and I enjoyed some of the best fruit juice in my life.

So my clients came to rely on me for diversions. The Iran-Iraq War was taking place then. I took them up in my plane to 10,000 feet and we watched the aerial war underway 50 miles to the north. The nighttime display of rockets, machine gun fire, and explosions was spectacular.

During one such foray, the wind shifted dramatically as a sandstorm rolled in. Suddenly I was landing in a 50-knot crosswind instead of a 10-knot headwind. A quick referral to the aircraft manual confirmed that the maximum crosswind component for the plane was 27 knots.

Oops!

Then I got a bright idea. I radioed the tower and asked for permission to land on the taxiway at a 90-degree angle to the main runway. After some hesitation, they responded, “If you’re willing to try it”. They knew my only alternative was to ditch at sea with two high-ranking gentlemen who couldn’t swim.

The tower very kindly talked me down with radar vectors and at the last possible second, with the altimeter reading 20 feet, the taxiway popped into view. With such a stiff wind I was able to pancake the plane down in yards, slam it on the runway, and then immediately shut the engine down. I asked for a tow, not wanting to risk the windstorm flipping the plane over.

My passengers thanked me profusely.

When Iraq invaded Kuwait in 1991, I lost most of my friends there. They were either killed, kidnapped and held for ransom, or volunteered as translators for US forces. I never saw them again.

I didn’t return to the Middle East until 2019 when I took two teenage girls to Egypt to introduce them to that part of the world. They wore hijabs, rode camels, and opened their eyes. I even set up some meetings with an educated Arab woman.

I will probably go back someday. I still haven’t seen the ruins at Petra in Jordan, nor ridden the Hijaz Railway, which Lawrence of Arabia blew up in 1918. But I have an open invitation from the king there.

I knew his dad.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

February 24, 2023

Fiat Lux

Featured Trade:

(PART 2: THE BEST OF THE REST IN QUANTUM COMPUTING)

(GOOGL), (QUBT), (IBM), (MSFT), (AMAT)

Alphabet (GOOGL)

In 2019, Google claimed that it had achieved what it called quantum supremacy. The company claimed to have built a computer with capabilities far beyond those of traditional computers.

In a report published in Nature, Google said its quantum computer managed to calculate something that would take a normal machine 10,000 years.

What practical applications Google's performance will have in the real world is still unclear. The initial computation was a demonstration of capability rather than a product that will have a significant commercial impact any time soon.

Having a horse in the race will also mean they can turn it up a notch once they receive more direction on where this might lead.

Like so many of its other companies, Alphabet invests heavily in the latest computer technology.

Many of these ventures probably won't bring in much money; others, on the other hand, will likely recoup the company's entire research budget and then some. And the good thing about Alphabet is that it's so busy that a single project, such as B. quantum computing, will not decide on the entire investment.

I am not going to sit here and say that Google is a quantum computing company because it’s not, but they are ready to pounce if the opportunity presents itself.

Quantum Computing (QUBT)

Quantum Computing is an innovative company focused on its namesake. It sees a market opportunity in the ability to create a service that coordinates computing needs.

There are providers of quantum computers, such as IonQ or Rigetti. Then there are customers in large companies, universities, or research laboratories. Quantum Computing sits in the middle, making software to help customers manage their quantum computing needs.

Currently, quantum computing has almost no revenue. Management acknowledges that the company is still in the early stages of market development and understanding customer use cases.

QUBT stock is highly speculative, as are most other companies in the sector. However, as the market for quantum computing vendors and customers grows, a brokerage service that connects the two could represent a fairly profitable niche.

IBM (IBM)

Tech analysts like to compare IBM to companies like Radio Shack and Eastman Kodak (KODK) as a dinosaur inevitably heading towards the dustbin of history.

However, the truth is much more nuanced.

IBM still achieves $60 billion a year in total revenue, and that number is actually on the rise again. They also have a PE ratio of 21 as its ongoing operations in consulting, services, and cloud, among others, are very profitable. And IBM continues to invest heavily in research and development, including quantum computing.

IBM's quantum computing division promises to unlock information beyond the reach of even the world's fastest supercomputers. The IBM partnership for quantum computing already involves 160 Fortune 500 companies as well as national laboratories and academic institutions. These partners work in areas such as finance, chemistry, and logistics.

Microsoft (MSFT)

Like IBM, Microsoft wants to take the lead in the emerging field of quantum computing. Microsoft has an inbuilt advantage, as its Azure cloud platform already has a massive installed base with a variety of Fortune 500 customers.

Now Microsoft is building its quantum computing capabilities directly into Azure. Microsoft describes this as “the world’s first full-featured, open cloud ecosystem for quantum computing.”

It makes a lot of sense that this would be offered as part of a cloud package. After all, most customers probably don't need their own supercomputer. Rather, they want the ability to buy that computing power only when they need it.

If Microsoft can seamlessly integrate this experience into its native Azure platform, it could be a major win, both for this product and for securing greater market share in cloud computing.

Applied Materials (AMAT)

Another approach to betting on quantum computing stocks is to be long on suppliers. Given that the technology is still very new, it can be difficult to determine which companies will ultimately be among the winners in this space. What is certain, however, is that if quantum computing catches on, we will need faster and more powerful semiconductors.

Applied Materials is one of the industry leaders in terms of patents and industry know-how when it comes to manufacturing chips that will be used in quantum computing hardware. During a gold rush, you want to be the one selling the shovels. Applied Materials should be the shovel dealer for the quantum computing industry.

In the meantime, Applied Materials' existing business is extremely profitable.

Global Market Comments

October 17, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or BLUNDER 3.0)

(RIVN), (TSLA), (V), (JPM), (AMAT), (HPE), (DELL), (KBH), (LEN)

There is no doubt whatsoever that the stock market tried to break down last week and failed. At worst, the Dow Average double bottomed at $29,600, the same level it reached on September 28.

And even that low was a mere 800 points lower than the one we set on June 14.

And that’s how it’s going to go.

Incremental new lows, followed by violent “rip your face off” rallies on enormous volume.

Until it ends.

That happens when markets start speculating about coming interest rate cuts sometime in 2023. And remember, you’re buying stocks for not what the economy is doing today, but for how well it will be performing in six to nine months.

You’re buying the future, not the present, or heaven forbid, the past.

That means you should use these throw-up-on-your-shoes days to scale into your favorite long-term companies. When markets inevitably rally, you can either sell for a short-term profit and rewind the video once again or keep it as part of a long-term holding.

It's a nice choice to have. I’ve been doing it all year.

With some of the greatest market volatility in market history, my October month-to-date performance ballooned to +5.00%.

I used last week’s extreme volatility to roll down strike prices for Tesla (TSLA) and JP Morgan (JPM) option spreads to manage my risk. I was still able to hang on to a 40% long position and threw out a new short in the S&P 500 at the end of Thursday.

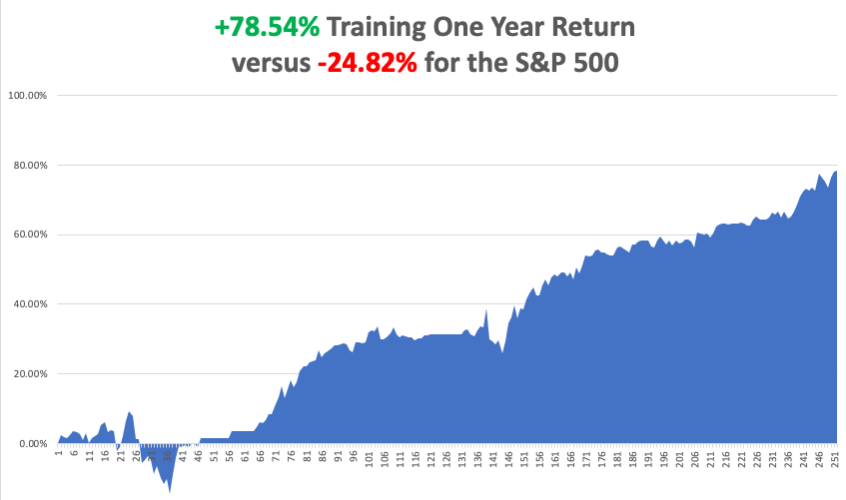

My 2022 year-to-date performance ballooned to +75.06%, a new high. The Dow Average is down -18.48% so far in 2022. With the coming Friday options expiration, I will be up +76.49%.

It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high +78.54%.

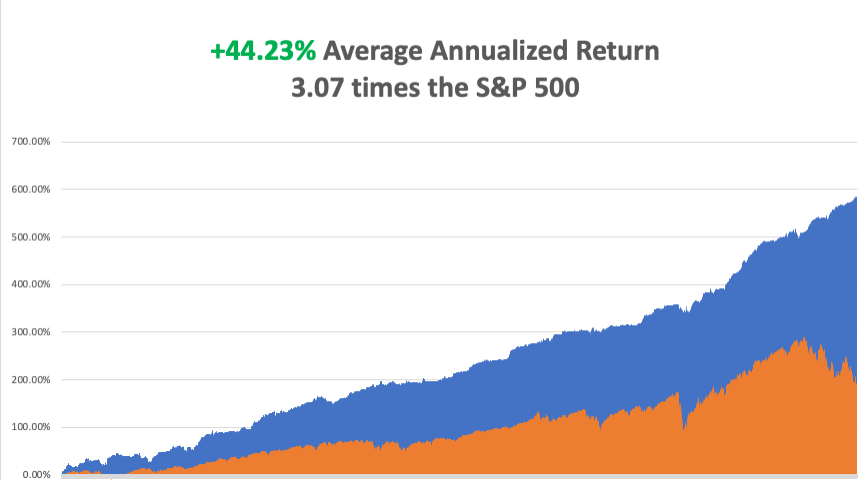

That brings my 14-year total return to +587.62%, some 3.03 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to +44.23%, easily the highest in the industry.

Remember that old 60/40 equity/bond investment strategy? The idea was that whenever stocks went down, the losses would be offset by the profits from rising bonds.

This year, it delivered the worst performance in 100 years, down 34.4% year-to-date. That is the inevitable end result of a decade of zero interest rates and free money that took everything up.

So what is the best strategy you could probably employ right now? A 60/40 strategy. Even I find myself checking out bond yields these days, where I got my start in life as a trader 50 years ago. Yes, before there were stocks, there were bonds. Junk is now yielding 10%. Remember, that means a holding doubles in value every six years.

The market is clearly in a mood to throw out the babies with the bathwater. I would be remiss not to mention the recent decline of Tesla posing one of its periodic tests of the faithful, now approaching a once unheard-of price earnings multiple of 30X.

Up until September 20, Elon Musk’s creation was almost immune to the bear market.

Then Twitter (TWTR) happened.

Musk agreed to take majority control of a $44 billion company, of which Elon himself is only contributing $16 billion. He sold Tesla shares last July to fund this. But the market wiped $333 billion, or 34.6%, off the market capitalization of the company. It is a wild overreaction to the move.

This has nothing to do with Tesla itself, as the richest man in the world is buying Twitter with his own pocket change. But it is undeniable that it will be a distraction of management time.

And here is all you need to know about Tesla. Tesla is the fastest growing large company in the world. Profit margins are increasing, thanks to the recent collapse of commodity prices. Unit sales will rise by 40% this year. Every time Tesla opens a new factory at a cost of $7 billion, it generates $15 billion of profit per year, forever!

Remember also, that the stock market gets an 800-pound gorilla off its back with the end of the midterm elections on November 8. It makes no difference who wins, a major uncertainty will be gone. That much IS certain.

And what happens when the Fed keeps interest rates too low for long, then raises them too much? It lowers them again too much, igniting a monster bull market in stocks. That’s also what you’re buying down here. That's what you get when you appoint a central bank governor with a political science major rather than PhDs and Nobel Prizes in Economics like the last ones.

Call it blunder 3.0.

Consumer Price Index Rockets Up to 8.6%, up 0.4% on the month and a new 40-year high. Stocks, bonds, crypto, and currencies were crushed and the US Dollar Soared. Look for new lows in stocks. Growth really took it on the nose. Expect another month of volatility until the next CPI report comes out.

Stocks Mount Historic Rally, gaining $1,420 points, or 5% of the intraday low. Stocks were down 500 in the wake of the CPI report, then up $1,420. It was mostly hedge short covering, as most institutions are too slow to react. Still, we now have a low to trade against.

The Fed Minutes are Out, and our central bank is clearly worried about doing too little than too much, when they are doing too much. At least they did six weeks, or 4,000 Dow points ago. The inflation goal is still 2.0%. Interest rates will go higher before they go lower.

Equity Inflows Hit a Record Last Week, the third highest week since 2008. Long term investors are willing to bottom fish here, even if the final bottom isn’t found for months.

Bond Liquidity Issues Haunting the Fed, and bids dry up in an endlessly falling market. The matter has been greatly exacerbated by a Fed that is now selling $95 billion a month as part of its quantitative tightening policy. It’s becoming increasingly difficult to move big blocks of bonds in a zero-bid market. Spreads are widening and size is shrinking. The bad news is that the worst is yet to come.

You Just Got an 8.7% Raise, if you are older than 61 and collecting Social Security. That is the payment increase that kicks in from January. Fortunately, some thoughtful person eons ago tied payments to the CPI, which is now going through the roof. I’m going to Hawaii with my money, even if the increase means that Social Security goes bankrupt by 2034, when I’m 82.

PC Sales Dive 19.5% in Q3, reaching only 68 million units. It’s the steepest decline since PC data collection began 30 years ago. And you wonder why they are selling the chip stocks so aggressively. High inventories are also a big problem. Lenovo was the top seller in the world at 20.2 million units, followed by Hewlett Packard’s (HPE) 17.6 million, and Dell (DELL) at 15.2 million.

Applied Materials Cuts Estimates, in line with everyone else in the industry. The new government export restrictions will cost it $250-$500 million in the current quarter. But how much is already in the price? Buy (AMAT) on dips.

Home Financing Pours into 5/1 ARMS, which can be had for a doable 5.56%. That compares to over 7.0% for the 30-year fixed, the highest since 2006. It will be low enough to keep homebuilders on life support for a couple of years Avoid (LEN) and (KBH).

REITS are Still Getting Slaughtered, with the plunge in the bond market today to multidecade lows. The REIT Index is down 30% this year, while the (SPY) is off only 21%. Real Estate Investment Trusts do best when interest rates are low. Too many investors piled into REITS in a desperate reach for yield. There’s a great trade here someday, but not yet.

My Ten-Year View

When we come out the other side of pandemic and the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With oil in a sharp decline and technology hyper-accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side will be far more efficient and profitable than the old. Dow 240,000 here we come!

On Monday, October 17 at 8:30 AM, the New York Empire State Manufacturing Index for September is released.

On Tuesday, October 18 at 7:00 AM, the D for September is out.

On Wednesday, October 19 at 8:30 AM, Housing Starts and Permits for September are published.

On Thursday, October 20 at 8:30 AM, Weekly Jobless Claims are announced. At 10:00 AM, we get Existing Home Sales for September.

On Friday, October 21 at 2:00 PM, the Baker Hughes Oil Rig Count is out.

As for me, it was in 1986 when the call went out at the London office of Morgan Stanley for someone to undertake an unusual task. They needed someone who knew the Middle East well, spoke some Arabic, was comfortable in the desert, and was a good rider.

The higher-ups had obtained an impossible-to-get invitation from the Kuwaiti Royal family to take part in a camel caravan into the Dibdibah Desert. It was the social event of the year.

More importantly, the event was to be attended by the head of the Kuwait Investment Authority, who ran over $100 billion in assets. Kuwait had immense oil revenues, but almost no people, so the bulk of their oil revenues were invested in western stock markets. An investment of goodwill here could pay off big time down the road.

The problem was that the US had just launched air strikes against Libya, destroying the dictator, Muammar Gaddafi’s royal palace, our response to the bombing of a disco in West Berlin frequented by US soldiers. Terrorist attacks were imminently expected throughout Europe.

Of course, I was the only one who volunteered.

My managing director didn’t want me to go, as they couldn’t afford to lose me. I explained that in reviewing the range of risks I had taken in my life, this one didn’t even register. The following week found me in a first-class seat on Kuwait Airways headed for a Middle East in turmoil.

A limo picked me up at the Kuwait Hilton, just across the street from the US embassy, where I occupied the presidential suite. We headed west into the desert.

In an hour, I came across the most amazing sight - a collection of large tents accompanied by about 100 camels. Everyone was wearing traditional Arab dress with a ceremonial dagger. I had been riding horses all my life, camels not so much. So, I asked for the gentlest camel they had.

The camel wranglers gave me a tall female, which was more docile and obedient than the males. Imagine that! Getting on a camel is weird, as you mount them while they are sitting down. My camel had no problem lifting my 180 pounds.

They were beautiful animals, highly groomed, and in the pink of health. Some were worth millions of dollars. A handler asked me if I had ever drunk fresh camel milk, and I answered no, they didn’t offer it at Safeway. He picked up a metal bowl, cleaned it out with his hand, and milked a nearby camel.

He then handed me the bowl with a big smile across his face. There were definitely green flecks of manure floating on the top, but I drank it anyway. I had to lest my host to lose face. At least it was white. It was body temperature warm and much richer than cow’s milk.

The motion of a camel is completely different from a horse. You ride back and forth in a rocking motion. I hoped the trip was short, as this ride had repetitive motion injuries written all over it. I was using muscles I had never used before. Hit your camel with a stick and they take off at 40 miles per hour.

I learned that a camel is a super animal ideally suited for the desert. It can ride 100 miles a day, and 150 miles in emergencies, according to TE Lawrence, who made the epic 600-mile trek to Aquaba in only four weeks in the heat of summer. It can live 15 days without water, converting the fat in its hump.

In ten miles, we reached our destination. The tents went up, clouds of dust rose, the camels were corralled, and the cooking began for an epic feast that night.

It was a sight to behold. Elaborately decorated huge five wide bronze platers were brought overflowing with rice and vegetables, and every part of a sheep you can imagine, none of which was wasted. In the center was a cooked sheep’s head with the top of the skull removed so the brains were easily accessible. We all ate with our right hands.

I learned that I was the first foreigner ever invited to such an event, and the Arabs delighted in feeding me every part of the sheep, the eyes, the brains, the intestines, and gristle. I pretended to love everything, and lied back and thought of England. When they asked how it tasted, I said it was great. I lied.

As the evening progressed, the Johnny Walker Red came out of hiding. Alcohol is illegal in Kuwait, and formal events are marked by copious amounts of elaborate fruit juices. I was told that someone with a royal connection had smuggled in an entire container of whiskey and I could drink all I wanted.

The next morning I was awoken by a bellowing camel and the worst headache in the world. I threw a rock at him to get him to shut up and he sauntered over and peed all over me.

The things I did for Morgan Stanley!

Four years later, Iraq invaded Kuwait. Some of my friends were kidnapped and held for ransom, while others were never heard from again.

The Kuwaiti government said they would pay for the war if we provided the troops, tanks, and planes. So they sold their entire $100 million investment portfolio and gave the money to the US.

Morgan Stanley got the mandate to handle the liquidation, earning the biggest commission in the firm’s history. No doubt, the salesman who got the order was considered a genius, earned a promotion, and was paid a huge bonus.

I spent the year as a Marine Corps captain, flying around assorted American generals and doing the odd special opp. I got shot down and still set off airport metal detectors. No bonus here. But at least I gained insight and an experience into a medieval Bedouin lifestyle that is long gone.

They say success has many fathers. This is a classic example.

You can’t just ride out into the Kuwait desert anymore. It is still filled with mines planted by the Iraqis. There are almost no camels left in the Middle East, long ago replaced by trucks. When I was in Egypt in 2019, I rode a few mangy, pitiful animals held over for the tourists.

When I passed through my London Club last summer, the Naval and Military Club on St. James Square, who’s portrait was right at the front entrance? None other than that of Lawrence of Arabia.

It turns out we were members of the same club in more ways than one.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

John Thomas of Arabia

Checking Out the Local Camel Milk

This One Will Do

Traffic in Arabia

Global Market Comments

May 24, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or IT'S ALL ABOUT THE NUMBERS),

(TLT), (SPY), (FCX), (QQQ), (VIX), (UUP), (AMAT), (CRM), (GOOG), (AMZN), (AAPL), (FB)