Mad Hedge Technology Letter

November 6, 2018

Fiat Lux

Featured Trade:

(THE GREAT TECH COMPANY YOU’VE NEVER HEARD OF)

(TWLO), (ROKU), (MSFT), (SQ), (AMD), (CRM), (SEND)

Mad Hedge Technology Letter

November 6, 2018

Fiat Lux

Featured Trade:

(THE GREAT TECH COMPANY YOU’VE NEVER HEARD OF)

(TWLO), (ROKU), (MSFT), (SQ), (AMD), (CRM), (SEND)

As volatility rears its hideous head, it’s not necessarily the best time to catch a falling knife as tech companies have been scrutinized harshly lately.

But the market is always right, and waiting for them to drop into your lap will serve you in good stead, even more so for the higher beta tech names that can behave more petulant than a little child.

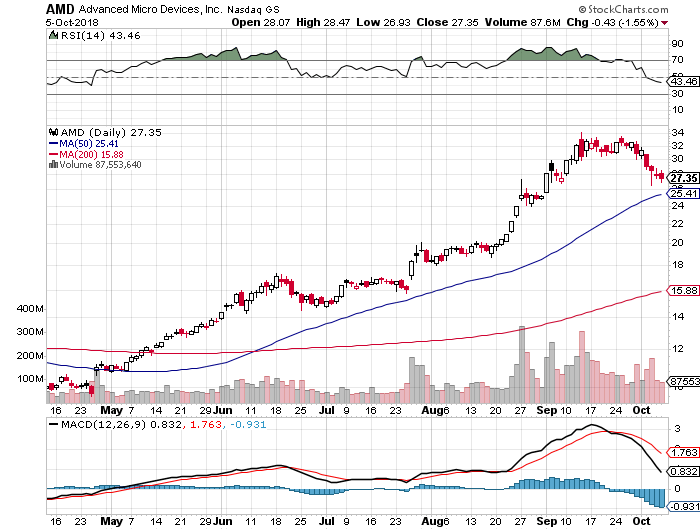

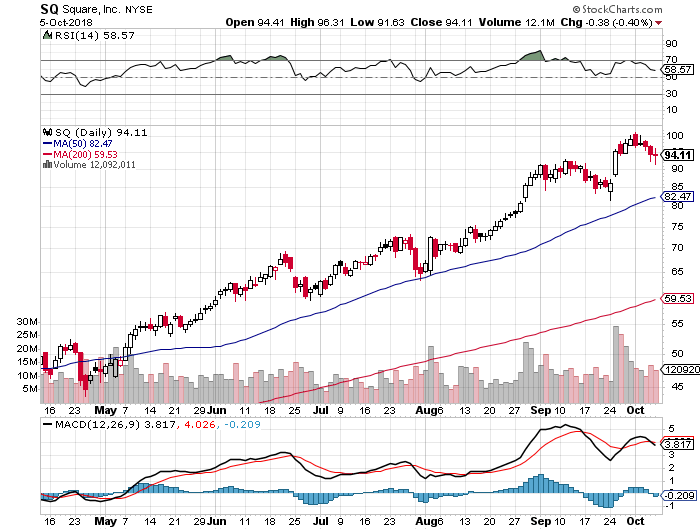

Roku (ROKU), AMD (AMD), and Square (SQ) are a few of these smaller names with prodigious growth stories backed by secular tailwinds.

These up-and-comers regularly experience 5-7% setbacks, while sturdier names such as Microsoft (MSFT) pull back 1-2% allowing you to sleep soundly at night.

Another influential company taking the liberty to infiltrate the backend of every global and local company is no other than communications software company Twilio (TWLO).

Many of you might not have heard of them, and it doesn’t sound like such a sexy company right off the bat but I am sure you have heard of companies such as Uber, Lyft, and Airbnb.

Why do I mention these three private tech companies that are on the verge of going public next year?

Because this trio of unicorns are all powered by Twilio’s communication technology that is best of breed in their genre of cloud software.

More specifically, Twilio is a platform as a service (PaaS) firm offering programmatic phone call functions, can automate sending and receiving text messages, and performs other communication functions using its web service APIs.

When your Uber driver calls asking you to reveal yourself out of a concrete apartment block or your lavish gated community, this is all facilitated by Twilio’s technology.

At the recent Twilio Signal Conference in San Francisco, Twilio indicated that its latest “call center in a box” product called Flex was up and running after announcing it this past March.

Prior to Twilio’s roll-out, this type of call center functionality was only reserved for the Fortune 500 companies that could afford expensive software to serve its minions of customers.

The small guy was left out in the cold as usual.

Twilio has reshaped the call center and, at $1 per hour or $150 per month, has made itself a gamechanger for SMEs who don’t have the manpower or capital to fund exorbitant back-end operations.

Twilio is really going after anyone with a light or bulky-shaped wallet as you see from their all-star lineup of customers. U-Haul, real estate website Trulia, and data analytic firms Scorpion and Centerfield are just a few of their customers proving the incredible flexibility of the software.

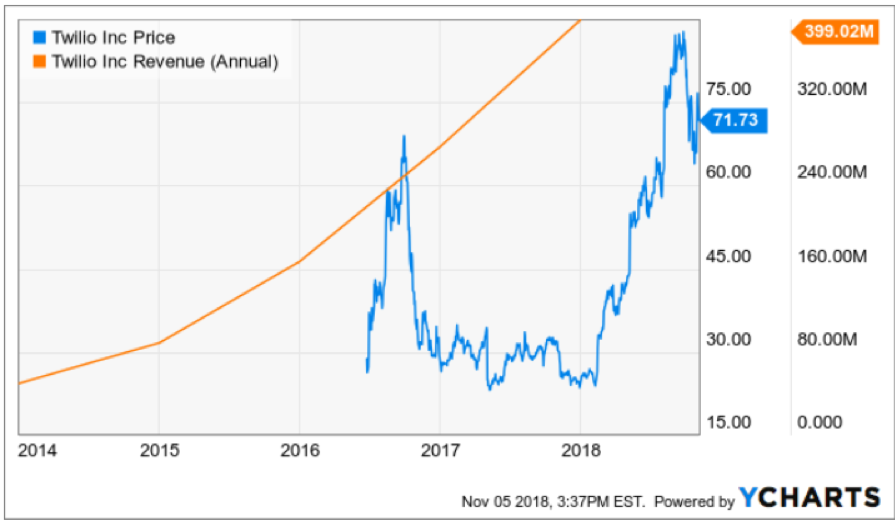

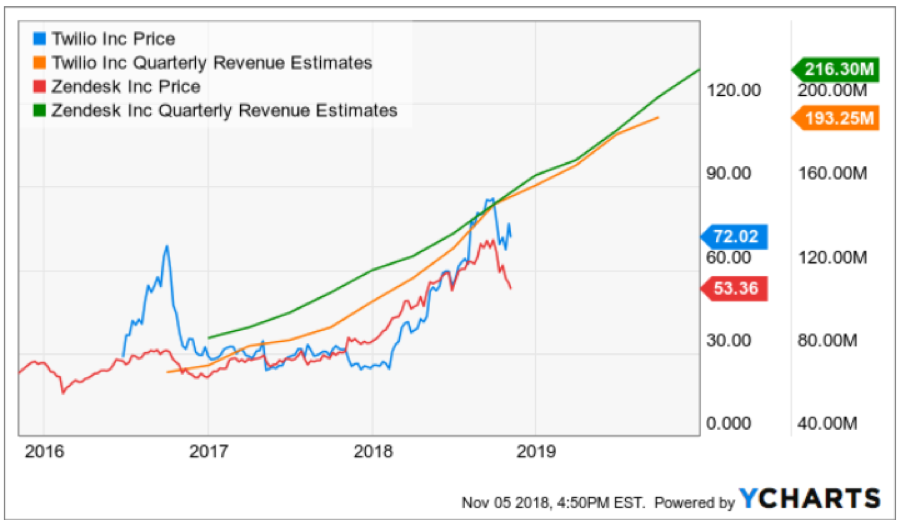

It’s not a shock that this stock has gone ballistic in 2018 surging over 200% and I must admit, investors need to wait for this molten hot stock to cool down.

But how can you blame a company that habitually tears apart any expectation of them devouring expectations because of its super growth model and rapid broad-based adoption?

From the fourth quarter of last year, revenue accelerated to 48% YOY and Twilio followed that up with a blistering 54% YOY quarter.

Then they pulled a shocker guiding down only expecting 35% to 37% growth but dismantled any whiff of jangling investors' nerves by posting another quarterly growth rate of 54%.

If you average out the three-year sales growth rate, few can topple the 57% Twilio has registered.

Performance has been fantastic, to say the least, and Flex could be the product that cements their industry lead and widens the moat around them.

Airbnb, Uber, and Lyft will avoid tinkering with the back end of their operations before their 2019 IPOs boding well for Twilio who are on a hot streak scoring a series of big contracts.

Twilio has been embroiled in further recent stock weakness as they gobbled up SendGrid (SEND), a mass-email marketing software service, for $2 billion.

SendGrid is growing sales at a lower rate in the mid-30%, and this move will add to top line growth.

Synergies from this acquisition are numerous and Twilio will be able to cross-sell to SendGrid’s customers who can apply other communication tools to use.

Telecommunication product in the past was truly unaffordable for the bulk of companies and now that Twilio can bring in all the smaller companies, the SME landscape is poised to change.

Software is becoming powerful to the point where one person living in a basement will have the access to a software that could convince customers a 100-man team is putting this product altogether.

Flex allows customers to personalize this contact-center-in-a-box software for each specification.

It can even quickly integrate into CRM platforms like Salesforce (CRM) which is a wildly popular interface for companies around the world.

Twilio Autopilot, Twilio’s oral conversational AI tool, offers machine learning bots who deliver automated voice-activated functions to customers.

Companies can easily type what they want bots to orate to customers and simply paste it into the code with ease and minimal hassle.

Twilio’s updated payment capabilities offer a new API for building payment experiences by contacting center agents who can now securely accept credit card payments from customers over the phone without the agents ever getting a whiff of the actual numbers.

Effectively, this allows any business in the world to professionalize their communications and backend department to a point they could have never imagined a few years ago.

The saying rings true when industry experts note that it’s the best time to become a billionaire and worst time to become a millionaire because the power of leveraging these robust software programs could potentially fuel the rapid rise of anyone in the world who will eat everybody else’s lunch.

If you break down the numbers, most companies are still holding on to their legacy systems of yore.

Being saddled with outdated hardware and software will doom companies going forward as the explosion of brilliant software modernizes companies in a few clicks of the mouse.

Twilio has added another 15,000 developers to the 35,000 already on the books and the purchase of SendGrid can no doubt be attributed partially to a talent grab of developers who have deep experience building communication-based products.

These types of developers don’t grow on trees.

Last year saw Twilio bring in about $400 million in sales and I am modeling for around $1 billion in sales by 2021.

This $7 billion market cap tech darling has a long runway ahead of itself and investors looking for high-volatility, high-reward stocks can tuck this one away in their sheath.

With earnings coming up and an already 200% plus pop this year, there will be better entry points into this ebullient company if investors are patient.

Wait for a dip to get in on the best communication-based cloud company on the market.

Global Market Comments

November 2, 2018

Fiat Lux

Featured Trade:

(OCTOBER 31 BIWEEKLY STRATEGY WEBINAR Q&A),

(EDIT), (TMO), (OVAS), (GE), (GLD), (AMZN), (SQ), (VIX), (VXX), (GS), (MSFT), (PIN), (UUP), (XRT), (AMD), (TLT)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader October 31 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader.

As usual, every asset class long and short was covered. You are certainly an inquisitive lot, and keep those questions coming!

Q: I would like to keep CRISPR stocks as a one or two-year-old, or even longer if it is prudent. What do you think?

A: Yes, there is a CRISPR revolution going on in biotech—I’m extremely bullish on all these stocks, like Editas Medicine (EDIT), Thermo Fisher Scientific (TMO), and Ovascience Inc. (OVAS). If any of these individual companies don’t move forward with their own technology, they will get taken over. The principal asset of these companies is not the patents or the products, it’s the staff, and there is an extreme shortage in CRISPR specialists (and anybody who knows anything about monoclonal antibodies).

Q: Could you explain how to manage LEAPs? For example, the Gold (GLD) and the General Electric (GE) LEAPs. Sit and leave them or trade them short term?

A: You make a lot of money trading long-term LEAPs. Just because you own a year and a half LEAP doesn’t mean that you keep it for a year and a half. You sell it on the first big profit, and I happen to know that on both the Gold (GLD) and the (GE) LEAPs we sent out, people made a 50% profit in the first week. So, I told them: sell it, take the profit. The market always gives you another chance to get in and buy them cheap. You make the money on the turnover, on the volume—not hanging out trying to hit a home run.

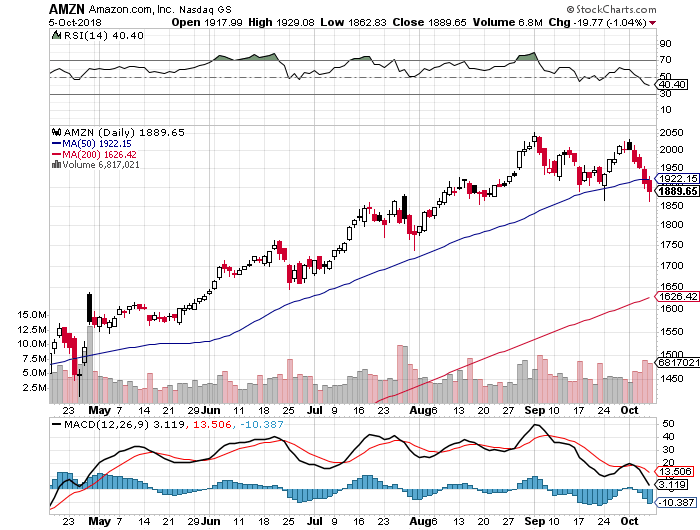

Q: Why did you only close the Amazon (AMZN) November $1,550-$1,600 vertical bull call spread and not roll the strike prices down and out?

A: Well I actually did do the down and out strike roll out first, which is the super aggressive approach. By adding the November $1,350-$1,400 vertical bull call spread position on Monday at the market lows and doubling the size—we took a huge 30% position in Amazon and that position alone should bring in about $3600 in profits in two weeks, at expiration. And when I put on that second position I told myself that on the next big rally I would get out of the high-risk trouble making position, which was the November $1,550-$1,600 vertical bull call spread. So that’s how you trade your way out of a 30% drop in three weeks in one of the best tech stocks in the market.

Q: Is AT&T (T) no longer a good buy at these prices?

A: All of the telephone companies have legacy technology, meaning they are all dying. Basically, AT&T is about owning a bunch of rusting copper wire spread around the country. They haven’t been able to innovate new technologies fast enough to keep up with others who have. The only reason to own this is for the very high 6.56% dividend. That said, dividends can be cut. Look at General Electric which cut its dividend earlier this year. Whatever you make of the dividend can get lost in the principal.

Q: Do you think Square (SQ) is a good buy at this level?

A: Absolutely, it’s a screaming buy. It’s one of the favorite companies of the Mad Hedge Technology Letter and one of the preeminent disruptors of the banks. We think there’s another 400% gain in Square from here. It’s dominating FinTech now.

Q: When do you expect to close the short position in the iPath S&P 500 VIX Short-Term Futures ETN (VXX)?

A: If we can get the Volatility Index (VIX) down to $15, the (VXX) should crater. We’ll take a hit on the time decay and that’s why I say we may be able to sell it for 20 cents in the future when this happens. We’ll still take a 50% hit on the position, but half is better than none.

Q: What happened to Microsoft (MSFT) last week?

A: People sold their winners. They had a great earnings report and great long-term earnings prospects, but everyone in the world owned it. Buy the long-term LEAP on this one.

Q: If we want to double up on the iPath S&P 500 VIX Short-Term Futures ETN (VXX), how do you plan to do it?

A: Go out to further with your expiration date. When you go long the (VXX) you only buy the most distant expiration date. I would buy the February 15 expiration as soon as it becomes available.

Q: How do you see Goldman Sachs (GS) from here to the end of the year?

A: It may go up a little bit as we get some index money coming into play for year-end, but not much; I expect banks to continue to underperform. They are no longer a rising interest rate play. They are a destruction by FinTech play.

Q: Is it too soon for emerging markets in India (PIN)?

A: As long as the dollar (UUP) is strong, which is going to be at least another year, you want to avoid emerging markets like the plague. As long as the Federal Reserve keeps raising interest rates, increasing the yield differential with other currencies, the buck keeps going up.

Q: What are your thoughts on retail ETFs like the SPDR S&P Retail ETF (XRT)?

A: You may get lucky and catch a rally on that but the medium term move for retail anything is down. They are all getting Amazoned.

Q: Is it better to increase long exposure the day before the election?

A: No, what we saw starting on Tuesday was the pre-election move. That said, I expect it to continue after the election and into yearend.

Q: Any opinions on Advanced Micro Devices (AMD)?

A: Yes, this is a great level. It was extremely overbought two months ago but has now dropped 50%. It is a great long-term LEAP candidate.

Q: What about the W bottom in the stock market that everyone thinks will happen?

A: I’m one of those people. So far, the bottom for the move in the S&P 500 is looking pretty convincing, but we will test the faith sometime in the next week I’m sure. We got close enough to the February $252 low to make this a very convincing move. It sets up range trading for the market for the next year.

Q: How do you figure the inflation rate is 3.1%?

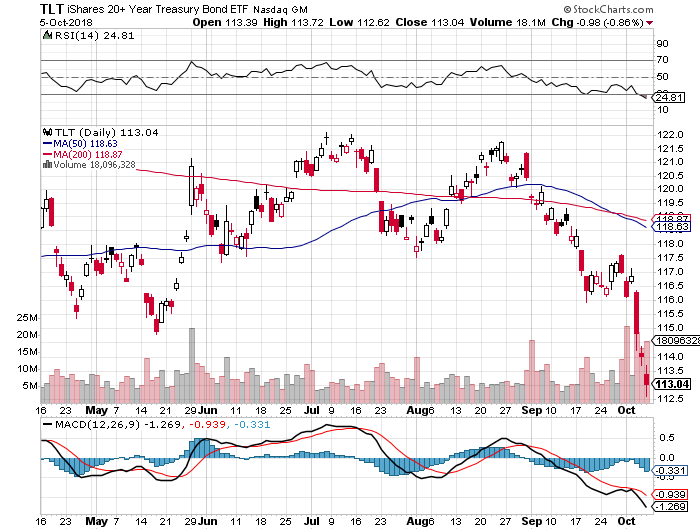

A: The year-on-year Consumer Price Index for September printed at 2.3%, and the most recent months have been running at an annualized 2.9% rate. Given that this data is months old we are probably seeing 3.1% on a monthly annualized basis now given all the anecdotal evidence of rising prices and wages that are out there. That is certainly what the bond market believes with its recent sharp selloff and why I will continue to be a fantastic short. Sell every United States US Treasury Bond Fund ETF (TLT) rally. Like hockey great Wayne Gretzky said, you have to aim not where the hockey puck is, but where it's going to be.

Q: Will rising interest rates kill the housing market?

A: It already has. A 5% 30-year mortgage rate shuts a lot of first time Millennial buyers out of the market. We are seeing real estate slowing all over the country. Los Angeles is getting the worst hit.

Q: How do you see the Christmas selling season going?

A: It’s going to be great, but this may be the last good one for a while. And Amazon is getting half the business.

Q: October was terrible. How do you see November playing out?

A: It could well be a mirror image of October to the upside. We are already $1,000 Dow points off the bottom. So far, so good. Throw fundamentals out the window and buy whatever has fallen the most….like Amazon.

Did I mention you should buy Amazon?

Good luck and good trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

November 1, 2018

Fiat Lux

Featured Trade:

(THE TERRIFYING CHART FORMATION THAT IS SETTING UP),

(SPY), (AMD), (MU), (AMZN), (NFLX),

(THE TECHNOLOGY NIGHTMARE COMING TO YOUR CITY)

The Mad Hedge Fund Trader is seeing its biggest one-day gains since the inception of our Trade Alert Service 11 years ago. By the time you read this, we will have picked up an astounding 11% profit for the entire portfolio in 24 hours.

However, this being Halloween, I don’t want to sound like I’m whistling by the graveyard. But what I am about to say will scare the daylights out of you.

I hate to say I told you so but my prediction a year ago that the bull market would end on May 10, 2019 at 4:00 PM is starting to look pretty good.

If I am right, the charts for the S&P 500 (SPY) are setting up a classic head and shoulders top. The left shoulder was created by the January 2018 rally to $282.

We just saw the head created at the beginning of October at $293. All that remains is to build the right shoulder back up to $282 by the spring. What will then follow is the crying.

This is not a matter of throwing a dart at a calendar or reciting a chant taught to me by a long-dead Yaqui Indian. It is a simple matter of math. Here’s how it goes:

*The Fed Raises funds rate 25 basis points per quarter for the next four quarters to 3.25%

*The Yields Curve Inverts, taking short rates higher than long rates now at 3.15%

*Bond yield spread trades increase massively going into the inversion as traders ramp up the size to make up for shrinking spreads.

*When the spread turns negative, they dump everything, creating an interest rate spike to 4% or 5%.

*Inverted yield curves last an average of 14 months or until February 2020 in this cycle when a recession begins.

*Stock markets peak on average seven months before recessions, and you arrive at Friday, May 10, 2019 at 4:00 PM EST as the date for the demise of the bull market. At that point, it will be ten years and two months old, the longest such move in history.

A lot of people asked why I sent out so few trade alerts during the summer and going into the fall.

In fact, the list of negatives has reached laughable proportions:

*Longest bull market in history

*In the face of rising interest rates

*In the face of rising oil prices

*Rising inflation

*Nothing else to buy

*Only bull market in the world

*Valuations approaching two-decade highs

*Overwhelmingly concentration in big cap tech

*Double top in the market on an Equal Weight S&P 500 chart

*Record retail inflows into ETFs

*Recession has already started in the auto industry

*Recession has already started in the housing industry

*Rotation to value defensive stocks underway

*Massive unicorn IPOs planned in 2019- $215 billion

*Slowing GDP Growth 4.2% to 3.5%

*Large amount of economic growth sucked forward from 2019 as businesses accelerate Chinese imports to beat the tariffs

*The same is going on in China to buy our exports

Should you throw up your hands, dump all your stocks, and hide out in cash?

Absolute not! In fact, the last six months of a bull market are often the most profitable. Many tech stocks like Micron Technology (MU) and Advanced Micro Devices (AMD) have dropped by half in recent months. That means they have to double to get back to their old highs.

Other big quality stocks such as Amazon (AMZN) and Netflix (NFLX) have plunged by 30% and only have to appreciate by 43% to hit highs. It is, in fact, the best entry point for large-cap tech stocks since 2015 with valuations at a three-year low.

If I am wrong, the trade war with China plunges us into recession and ends the bull market sooner. Almost all the “worry” items on the list above are getting worse by the day.

Mad Hedge Technology Letter

October 8, 2018

Fiat Lux

Featured Trade:

(A LONG-AWAITED BREATHER IN TECHNOLOGY),

(AMZN), (TGT), (NVDA), (SQ), (AMD), (TLT)

Taking profits - it was finally time.

The Nasdaq has been hit in the mouth the last few days and rightly so.

It was the best quarter in equities for five years, and a quarter that saw tech comprise up to a quarter of the S&P demonstrating searing strength.

It would be an understatement to say that tech did its part to drive stocks higher.

Tech shares have pretty much gone up in a straight line this year aside from the February meltdown.

Even that blip only caused Amazon (AMZN) to slide around 10%.

After all the terrible macro news thrown on the market in spades – tech stocks held their own.

Not even a global trade war with the second biggest economy in the world which is critical to exporting products to America was able to knock tech shares off their perch.

At some point, 26% earnings growth cannot sustain itself, and even though the tech narrative is still intact, investors need to breathe.

Let’s get this straight – tech companies are doing great.

They benefit from a secular tailwind with every business pivoting to mobile and software services.

All that new business has infused and invigorated total revenue.

The negative reaction by technology stocks was based on two pieces of news.

Interest rates (TLT) surging to over 3.2% was the first piece of news.

The increase in rates reinforces that the economy is humming along at a breakneck speed.

Yields are going up for the right reasons and this economy is not a sick one indeed.

As rates rise, other asset classes become more attractive such as CD’s and bonds.

The whole world is looking at the pace of rate rises because this will affect the ability for tech behemoths to borrow money to invest in their expensive well-oiled machines.

Three things are certain - the economy is hot, the smart money is buying on the dip now, and Amazon will still take over your home.

Even in a rising rate environment, Amazon is fully positioned to outperform.

The second catalyst to this correction was Amazon’s decision to hike its minimum wage to $15 per hour.

This could lay the path for workers around the country to demand higher pay.

The move was a misnomer as it will eliminate stock awards and monthly bonuses lessening the burden that Amazon actually has to dole out.

Call this a push – the rise in expenses won’t be material and realistically, Amazon can afford to push the wage bill by another order of magnitude, even though they will not.

This was also a way for Amazon founder Jeff Bezos to keep Washington off his back for a few months, and his generous decision was praised by government officials.

The wage hike underscores the strength of the ebullient American economy, and the consumer will benefit by recycling their wages back into Amazon and the wider economy.

Amazon makes up 50% of American e-commerce sales, and when workers are buying goods online, a good chance its coming from Amazon.

In an environment of full employment, the natural direction of wages is up, and this was due to happen.

You can also look at wage inflation as employees gaining at the expense of the corporation.

However, the massive deflationary trends of technology will also make this wage hike quite irrelevant over time as Amazon will automate more of their supply chain to make up for any wage hike that could damage revenue.

Amazon’s economies of scale give the Seattle-based company enough levers and buttons to push and pull to dilute expenses to make this a non-issue.

Each earnings call usually involves CFO of Amazon Brian Olsavsky explaining the acceleration of efficiencies in fulfilment centers bolstering the bottom line.

The stellar innovation in operational expertise moves up a level each quarter if not two levels.

Ultimately, though expensive on the surface, this won’t affect Amazon’s numbers at all, but more critically please the lower tier of workers who fight and scratch for their daily crust of bread.

This win-win scenario casts a positive image of Bezos in the public eye at a crucial time when he plans to recruit another legion of Amazon workers, as Amazon will shortly announce the location of their second American-based headquarter.

In fact, this turns the screws on the smaller retailers who must match the $15 per hour wage or confront a potential disaster of an entire workforce walking out and joining Amazon.

The mysterious Amazon-effect works in many shapes and sizes.

Big retailers like Target (TGT) have griped that it’s near impossible to find seasonal workers for the upcoming holiday season.

Moreover, if inflation remains moderate but contained – technology will power on.

And it will take more than a few prints of rising inflation to impress the Fed enough to expedite the raising of rates.

But it is safe to say that investors cannot expect the 100% up moves like in Amazon and Advanced Micro Devices (AMD) in one calendar year moving forward.

Technology has a plate full of challenges facing its share price as we move into the latter part of the fiscal year.

The challenges are two-fold - mid-term elections and navigating a smooth year-end.

Earnings should be good which is already baked into the pie, and the benefits of the tax cut have already worked itself through the system.

The furious pace of share buybacks will eventually subside too.

Management might finally bring out the spin doctors claiming the stronger dollar and worsening trade war is the reason to guide down.

At least tech companies doing business in China might follow this playbook.

Either way, tech shares are demonstrably sensitive right now and while the market needs tech to lead the way, the sector is exhausted from the burden of carrying the bulk of the load.

Freak-outs on rate surges have been a common experience for those old hands presiding over markets for decades.

These are all the staples of a 9th year bull market.

Typical late stage topping action is normal in economic cycles.

After the dust settles, the overreaction will give way to great buying opportunities at great prices, albeit it in the higher quality names.

The chip sector is still one to avoid unless the names are Advanced Micro Devices or Nvidia (NVDA).

Legacy companies have always been a no-go.

If you want hyper-growth, fin-tech name Square (SQ) would be an ideal candidate.

If buy and hold is your cup of tea, any 10% discount would be a great entry point in any of these quality companies.

Global Market Comments

October 5, 2018

Fiat Lux

Featured Trade:

(WEDNESDAY OCTOBER 17 HOUSTON STRATEGY LUNCHEON INVITATION),

(OCTOBER 3 BIWEEKLY STRATEGY WEBINAR Q&A)

(SPY), (VIX), (VXX), (MU), (LRCX), (NVDA), (AAPL), (GOOG), (XLV), (USO), (TLT), (AMD), (LMT), (ACB), (TLRY), (WEED)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader October 3 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader.

As usual, every asset class long and short was covered. You are certainly an inquisitive lot, and keep those questions coming!

Q: Will the market keep increasing for the rest of the year?

A: We haven’t had the pullback yet, so the short answer is yes. My yearend target of and S&P 500 (SPY) for the end of 2018 still stands. You can’t argue with the immediate price action. That said, the market is wildly overbought for the medium term and is approaching valuation levels we haven’t seen since the Dotcom peak in 2000. That why I am running a 70% cash trading book now.

Q: Should I be buying the Volatility Index (VIX) here?

A: Look at the bottom where we broke back in August, if we go down there and sit for a couple of days, then go out and buy the March 2019 $40 iPath S&P 500 VIX Short-Term Futures ETN (VXX) calls—way out of the money, way far in the future—and that way if you get any bounce in the (VIX) in the next 6 months, you’ll make a ton of money on that. You can buy them today for 50 cents. Plus, we could get one of these situations where there’s a major selloff once we’re into the new year, so a 6-month (VXX) call option would hedge that.

Q: Given the choice of Apple (AAPL) or Google (GOOG), which would you buy?

A: If you’re a conservative, old lady, widow and orphan type, you’d probably want to buy Apple— it’s almost turned into a utility, it’s so reliably safe, going up and has a nice dividend. If you want to be aggressive, swinging for the fences young stud and are looking for a double, I would go with Google—much higher growth pattern, pays no dividend and has had a 3-month consolidation going sideways. The only thing that could hurt this company would be government regulation, but with the Democrats possibly taking control of Congress in November, the prospect of government regulation of the entire technology sector could rapidly fade away.

Q: When should I get into Health Care (XLV)?

A: I think you have to wait at this point. To me, it’s tremendously overbought at the moment, but is still enjoying a long-term bull move. This is one of my two favorite sectors in the entire market. It has been rising for four months now, even though the Trump threat of price cuts are constantly overhanging the market.

Q: Is oil (USO) going to 100?

A: Because of the disruptions caused by the Iran sanctions and the tearing up of the Iran Nuclear Treaty, Trump has created a short squeeze in oil prices. He is threatening to boycott any country that buys oil from Iran, so Iran is shipping their oil through China, which is already under sanctions itself. However, that is easier said than done. The oil business is much more complicated than people realize. For China to take Iranian oil, they literally have to build new refineries from scratch to process the crude from Iran; no two crudes are alike. When you build a major supply, you have to build refineries to match that, and you have to get it there. This market will eventually stabilize, but in the meantime, there is a big short squeeze going on in Europe.

Q: Do you see the economy going strong into the end of the year?

A: Yes, I do—we still have the tax cuts, global liquidity, and deregulation kicking in, and those things will all work until the end of the year. I think we close at the highs of the year, and after that we’re going to have to start to work hard for our money once again in 2019. The US economy is like a supertanker; it takes a long time to turn it around.

Q: Will the interest rate spike kill the market?

You think? Investors are so used to ultra-low interest rates that a transition to normal rates will be traumatic. Next Friday, we get Core CPI, and if that comes in hot we could see another spike to 3.35% in the ten-year US Treasury bond (TLT). There are now a ton of people desperate to get out of their bond holdings at last week’s prices. This is why I have been selling short the bond market for the past three years and selling as recently as Monday. The next leg down in a 30-year bear market has begun.

Q: Advanced Micro Devices (AMD) has shot over $30—would you sell it?

A: We love the company long term but short term it is just way overdone; take the double and run, and then buy back on the next dip.

Q: Are you still bearish on the chip company?

A: Short term yes, long term no. This sector is now totally driven by the trade war with China. This includes NVIDIA (NVDA), Micron Technology (MU) and LAM Research (LRCX). Lam is particularly exposed because they had ordered to sell ten entire chip factories to China which is now on hold. That said, the day the trade way ends these stocks will all start a 50% run up. If China gets the same free pass and symbolic treaty that Canada did, that could happen sooner than later. If you can’t sleep at night until then, cut your position in half. If you still can’t sleep, cut it again.

Q: Do you think Lockheed Martin (LMT) is a buy Here at $350?

A: No, there is a double top risk for the stock right here. And if the Democrats get control of congress, the whole Trump trade could unwind. That would give the opposition the purse strings and the first thing they’ll do is cut defense spending, which Trump bumped up by $50 billion.

Q: Do you have any views on pot stocks like Aurora Cannabis (ACB), Tilray (TLRY) and (WEED)?

Stay away in droves. They’re this year’s bitcoin stocks. It’s still illegal. That’s why these companies are all based in Canada. And after all it’s a weed. How hard is it to grow? The barriers to entry are zero.