Mad Hedge Technology Letter

September 24, 2018

Fiat Lux

Featured Trade:

(BAD NEWS FROM MICRON TECHNOLOGY (MU),

(MU), (BABA), (KLAC), (LRCX), (INTC), (AMD), (NVDA), (HPQ)

Mad Hedge Technology Letter

September 24, 2018

Fiat Lux

Featured Trade:

(BAD NEWS FROM MICRON TECHNOLOGY (MU),

(MU), (BABA), (KLAC), (LRCX), (INTC), (AMD), (NVDA), (HPQ)

If your stomach was on edge before, then you must feel quite queasy now.

That’s only if you didn’t get rid of your chip stocks when I told you to.

The chip sector has been rife with issues for quite some time now, and I’ve been firing off bearish chip stories the past few months.

Intel (INTC) was one of the last chip companies I told you to avoid like the plague, please click here to review that story.

The contagion has spread wider.

Micron (MU), the Boise, Idaho-based chip giant, delivered poor guidance from its latest earnings report, adding more carnage to this trouble sector.

It’s been rough sailing for many American-based chip companies lately that are not named Advanced Micro Devices (AMD) and Nvidia (NVDA).

The protracted ongoing trade war between America and China that sees no end in sight is the fundamental reason to stay away from these chip companies that are the meat and potatoes inside of all electronic devices.

Cofounder of Alibaba (BABA) Jack Ma, who recently stepped down from his position as chairman, told news outlets that this trade war could last “20 years” and is “going to be a mess.”

Micron is affected by this trade war more than any other American company, with half of its annual revenue derived from the Middle Kingdom.

Out of the $20.32 billion in annual revenue last year, more than $10 billion was from China alone.

Micron is a leader in selling DRAM chips, which are placed in most portable electronic devices such as smartphones, video game consoles, and laptop computers.

The commentary coming out from chip executives has been overly negative and spells doom and gloom - supporting my view to be cautious on chips through the end of the year.

At the Citi 2018 Global Technology Conference in New York, KLA-Tencor (KLAC) chief financial officer Bren Higgins characterized the winter season DRAM market as “little less than what we thought,” describing margins as “modestly weaker.”

Lam Research (LRCX), once one of my favorite chip plays, offered bearish rhetoric about the state of chip investments, saying on its earnings call that is expected “lower spending on new equipment by some of its memory customers.”

It doesn’t take a rocket scientist to know that “memory customer” is Intel, which is in the throes of a CPU chip shortage rocking the overall personal computer market.

Personal computers face a steep 7% drop in sales volume for the rest of the year, and the knock-on effect is rippling throughout the industry.

The lower volume of produced computers means less memory needed, adding up to less sales for Micron.

This rationale forced Micron to guide down its revenue growth from 22% to 16% for the last quarter of 2018.

Intel’s monumental lapse has offered a golden opportunity for competitor Advanced Micro Devices (AMD) to steal market share from Intel in broad daylight.

This was the exact thesis that provoked me to urge readers to pile into AMD shares like a Tokyo rush-hour subway car.

Shares have gone ballistic to say the least.

(AMD) is poised to seize and reposition itself in the global CPU market with a 70/30 market share, up from the paltry 90/10 market share before Intel’s debacle.

To make matters worse for Intel, widespread reports indicate its shortage problems are “worsening.”

Such is a dog-eat-dog world out there when a company can triple market share in a blink of an eye.

The rotation is real with HP (HPQ) planning to integrate AMD chips into 30% of its consumer PCs, and Dell already mentioning it will use AMD chips to make up for the shortages.

The resilience in chip demand remains the silver lining for this industry as price weakness and production shortages will be finite.

Server demand remains particularly robust.

Google, Amazon, Facebook, and Microsoft coughed up $34.7 billion on data centers to serve cloud-based operation in the first half of the year in 2018, a sharp increase of 59% YOY.

Investors have been paranoid of the boom-bust nature of the chip industry for decades.

Each cycle sees spending and chip pricing rocket, only for inventories to build up and demand to evaporate in an instant.

The beginning of the end always starts with lower guidance, followed up with missed earnings the next quarter.

This playbook has repeated itself over and over.

Micron guided first quarter revenue of 2019 in a range between $7.9 billion to $8.3 billion, lower than the consensus of $8.45 billion.

And, if all of this horrid chip news wasn’t reason to rip your hair out - here is the bombshell.

To wean itself off the reliance of American chips, Alibaba has created a subsidiary to produce its own chips called Pingtouge Semiconductor Company.

Pingtouge refers to honey badger in the Chinese language, symbolic for its tenacity in the face of adversity – perhaps a thinly-veiled dig at the American political system.

Former Chairman Ma pocketed this chip company Hangzhou C-SKY Microsystems last year. It will will be given ample leeway and resources to team up with Alibaba to roll out its first commercial chip next year.

Alibaba has rapidly grown into the third-largest cloud player in the world, and require an abundant source of chips moving forward.

Chips tricked out with artificial intelligence will be adopted by not only its data centers, but integrated with its autonomous driving technology and IoT products, which are markets that Alibaba is proud to be part.

You can find Alibaba’s cloud products present in more than 20 countries. And the company that Jack Ma built forecasts to generate more than 50% of its revenue from overseas markets soon.

It could be Jack Ma laughing all the way to the bank.

Ultimately, Micron produced fair results last quarter, but like Facebook found out, if investors believe the company is about to fall off a cliff, it offers little resistance to the share price on a short-term basis.

Could the cyclicality demons start to awake to drag this company down?

Partially, yes, but there are still many positives to take away from this leading chip company.

China will need years to remedy its addiction of American chips.

It will not be able to produce the scope of quality or quantity to just stop buying from American companies for the foreseeable future.

The authorized $10 billion share buyback gave Micron shares a nice lift earlier this year, but the industry dynamics are now deteriorating rapidly.

Chip sentiment is at its lowest ebb for some time, and I reaffirm my call to avoid this sector completely unless it’s the two cornerstone chip companies showing systematic resiliency - (AMD) or Nvidia (NVDA).

The administration initially slapped on a tariff rate of 10% on $200 billion worth of goods with intentions to scale it up.

If nothing is solved, the increase to 25% will cause another 5% to 10% drop in Micron and Intel.

Then if the administration plans to go after the rest of the $250 billion of Chinese imports, expect another dive in chip shares.

Either way, each jawboning tweet as we head deeper into this trade conflict will damage Micron’s shares.

This sector is getting squeezed from many sides now, and if you don’t go outright short chip companies, then stay away until the storm clouds pass over and you can reassess the situation.

Mad Hedge Technology Letter

September 19, 2018

Fiat Lux

Featured Trade:

(IBM’S SELF DESTRUCT),

(IBM), (BIDU), (BABA), (AAPL), (INTC), (AMD), (AMZN), (MSFT), (ORCL)

International Business Machines Corporation (IBM) shares do not need the squeeze of a contentious trade war to dent its share price.

It is doing it all by itself.

Stories have been rife over the past few years of shrinking revenue in China.

And that was during the golden years of China when American tech ran riot on the mainland before the dynamic rise of Baidu (BIDU), Alibaba (BABA), and Tencent, otherwise known as the BATs.

Then the Oracle of Omaha Warren Buffett drove a stake through the heart of IBM shares earlier this year by announcing he was fed up with the company’s direction and dumped a 35-year position.

Buffett unloaded all of his shares in favor of putting down an additional 75 million shares in Apple (AAPL) in the first quarter of 2018.

Topping off his Apple position now sees Buffett owning a mammoth 165.3 million total shares in the resurgent tech company.

Buffett’s shrewd decision has been rewarded, and Apple’s stock has rocketed more than 20% since he jovially declared his purchase in May.

IBM has been a rare misstep for Buffett, who took a moderate loss on his IBM position disclosing an average cost basis of $170 on 64 million shares that Berkshire bought in 2011.

IBM has flatlined since that Buffett interview, and slid around 25% since its peak in mid-2014.

IBM is grappling with the same conundrum most legacy companies deal with – top line contraction.

In 2014, IBM registered a tad under $93 billion in annual revenue, and followed up the next three years with even lower revenue.

A horrible recipe for success to say the least.

In an era of turbo-charged tech companies whose value now comprise over a quarter of the S&P, IBM has really fluffed its lines.

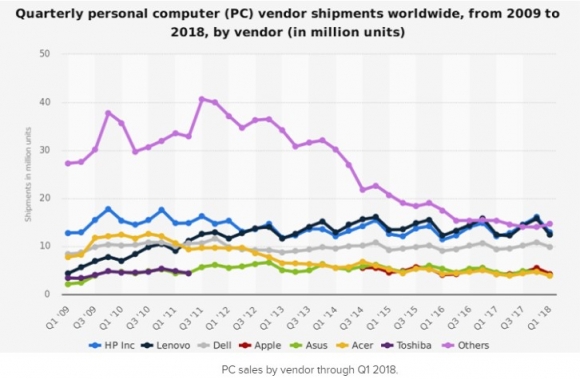

IBM’s prospects have been stapled to the PC market for years.

A recent JP Morgan note revealed the PC market could contract by 5% to 7% in the fourth quarter because of CPU shortages from Intel (INTC).

The report’s timing couldn’t have been worse for IBM.

The PC industry has been tanking for the past six consecutive years unable to shirk shrinking volume.

Intel is another company I have been lukewarm on lately because it is being outmaneuvered by chip competitor Advanced Micro Devices (AMD).

Even worse, this year has been a bad one for Intel’s management, which saw former CEO Brian Krzanich resign for sleeping with a coworker.

The poor management has had a spillover effect with Intel needing to delay new product launches as well.

To read more about my timely recommendation to pile into AMD in mid-August at $19, please click here.

Meanwhile, AMD shares have gone parabolic and surpassed an intraday price of $34 recently.

Investors should ask themselves, why invest in IBM when there are so many other tech companies that are growing, and growing revenue by 20% or more per year?

If IBM does manage to eke out top line growth in 2018, it will be by 1% to 2%, similar to Oracle’s recent performance.

Unsurprisingly, the price action of Oracle (ORCL) for the past year has been flatter than a bicycle ride around Beijing.

Live by the sword and die by the sword.

Thus, the Mad Hedge Technology Letter has been ushering readers into high-performance stocks that will bring technological and societal changes.

If you put a gun to my head and forced me to give sage investment advice, then the answer would be straightforward.

Buy Amazon (AMZN) and Microsoft (MSFT) on the dip and every dip.

This is a way to print money as if you had a rich uncle writing you checks every month.

Legacy tech is another story.

The IBMs and the Oracles of the world are bringing up the tech sector’s rear.

To add insult to injury, the lion’s share of IBM’s revenue is carved out from abroad, and the recent surge in the dollar is not doing IBM any favors.

IBM’s Watson initiative was billed as the savior for Big Blue.

The artificial intelligence initiative would integrate health care data into an actionable app.

The expectations were high hoping this division would drag up IBM from its long period of malaise.

IBM bet big on this division ploughing more than $15 billion into it from 2010-2015, predicting this would be the beginning of a new renaissance for the historic American company.

This game changing move fell on deaf ears and has been a massive bust.

IBM swallowed up three companies to ramp up this shift into the AI world - Phytel, Explorys, and Truven.

The treasure trove of health care data and proprietary analytics systems these companies came with were what this division needed to turn the corner.

These three companies were strong before the buy out and engineers were upbeat hoping Watson would elevate these companies to another level.

Wistfully, IBM Management led by CEO Ginni Rometty grossly mishandled Watson’s execution.

Phytel boasted 160 engineers at the time of IBM’s purchase and confusingly slashed half the workforce earlier this year.

Engineers at the firm even lamented that now, even smaller firms were “eating them alive.”

Unimpressed with the direction of the artificial intelligence division at IBM, many of these three companies’ best and brightest engineers jumped ship.

The inability for IBM to integrate Watson reared its ugly head in plain daylight when MD Anderson Cancer Center in Texas halted its Watson project after draining $62 million.

This was one of many errors that Watson AI accrued.

The failure to quicken clinical decision-making to match patients to clinical trials was an example of how futile IBM had become.

In short, a spectacular breakdown in execution mixed with an abrupt brain drain of AI engineers quickly imploded the prospect of Watson ever succeeding.

In 2013, IBM confidently boasted that Watson would be its “first killer app” in health care.

Internal leaks shined a brighter light on IBM’s subpar management skills.

One engineer described IBM’s management as having “no idea” what they were doing.

Another engineer said they were uncertain of a “road map” and “pivoted many times.”

Phytel, an industry leader at the time focusing on population health management, was bleeding money.

The engineers explained further, chiming in that IBM’s management had zero technical experience that led management wanting to create products that were “simply impossible.”

Not only were these products impossible, but they in no way took advantage of the resources these three companies had at their disposal.

Do you still want to invest in IBM?

Fast forward to today.

IBM is being sued in federal court with the plaintiff’s, former employees at the firm, claiming the company unfairly discriminated against elderly employees, firing them because of their age.

The documents submitted by the plaintiff’s state that “IBM has laid off 20,000 employees who were over the age of 40” since 2012.

This prototypical legacy company has more problems than the eye can see in every nook and cranny of the company.

If you have IBM shares now, dump them as soon as you can and run for cover.

It’s a miracle that IBM shares have eked out a paltry gain this year. And this thesis is constant with one of my overarching themes – stay away from all legacy tech firms with no cutting-edge proprietary technologies and stagnating growth.

________________________________________________________________________________________________

Quote of the Day

“Some say Google is God. Others say Google is Satan. But if they think Google is too powerful, remember that with search engines unlike other companies, all it takes is a single click to go to another search engine,” said Alphabet cofounder Sergey Brin.

Global Market Comments

September 12, 2018

Fiat Lux

THE FUTURE OF AI ISSUE

Featured Trade:

(THE NEW AI BOOK THAT INVESTORS ARE SCRAMBLING FOR),

(GOOG), (FB), (AMZN), MSFT), (BABA), (BIDU),

(TENCENT), (TSLA), (NVDA), (AMD), (MU), (LRCX)

Mad Hedge Technology Letter

September 4, 2018

Fiat Lux

Featured Trade:

(READY PLAYER ONE’S INSIGHT INTO THE FUTURE OF TECHNOLOGY),

(MSFT), (SQ), (TTWO), (AMD), (NVDA), (EA), (ATVI), (PYPL), (GOOGL), (FB)

The technology-laced film Ready Player One gives viewers a snapshot into the future where technology, income inequality, and society have run their course, and the year 2045 looks vastly different from the world of 2018.

Set in a semi-dystopian backdrop, the movie offers us a deeper insight into how certain technology trends will permeate into everyday life.

The first and most obvious future trend is the copious use of avatars.

Avatars will become the new normal. The first place that humans will find them is through the use of social media and entertainment, as children eventually becoming a part of us like our social media profiles today.

The Mad Hedge Technology Letter has incessantly hammered home about the phenomenon of gaming, and this will incorporate virtual reality allowing gamers access to a new digital world.

This was the on show in the film where the likes of protagonist Wade Watts, played by Tye Sheridan spent most of his life playing in the virtual world of Oasis using his character Parzival.

This could be your child in the future.

Wade Watts character is the new cool for Generation Z, as they are largely unconcerned about underage drinking and partying like the generations before them.

Gaming and hanging out on their preferred social media platforms are the new cool.

The companies dictating the current video game industry will have the first crack at it to realize profits and develop new businesses such as Microsoft (MSFT), Nvidia (NVDA), Advanced Micro Devices (AMD), Electronic Arts Inc. (EA), Take-Two Interactive Software, Inc. (TTWO), and Activision Blizzard, Inc. (ATVI).

Children just aren’t going outside like they used to and per most studies, they are addicted to the smartphone you bought them at age 10.

Most studies have found that once a child becomes hooked on technology, it is hard to reverse the habit, as once they enter into adult life and start their career, they become even more reliant on the technologies that got them to that point in the first place.

If your kid is already staring at tech devices three to four hours per day now for activities other than school work, expect that to grow to a minimum of six to seven hours per day once he hits puberty and smartphone time limits begin to fade away.

This all means that VR and gaming could be the handsome winner in all this, and the use of social media platforms will reap the benefits as well.

Generation Z just surpassed Millennials in terms of population comprising 25% of the American populace.

Neither of these generations have grown up with VR in their daily lives because the technology wasn’t advanced enough to really make a dent in their lives.

More than 75% of Generation Z has access to a smartphone, and they can truly be called the first generation of digital natives.

Avatars will push deeper into everyday life because the facial tracking technology has advanced by leaps and bounds.

Instead of cartoon-like avatars, lifelike avatars have replaced the less refined versions. It will be a tough time going forward distinguishing what is real and what is fake.

If you think fake news is a problem now, imagine how fake it will become in the future.

This could devastate the news industry as news organizations run the risk of melting down at any point, or just being completely taken over by tech companies and their algorithms, which is already happening now with Alphabet (GOOGL).

The future looks bleak for all newspaper assets, and the ones with the most advanced digital strategies will survive.

Newspapers only have so much time they can hang on with digital ad revenue, the reason they are still in business.

Viewers don’t want to see ads – period. And at some point, they will be disrupted as well.

Swashbuckling youth already have downloaded ad-blockers to completely remove ads from their lives, and refuse to open any website that forces them to white list a website.

There are children in Generation Z who might never have seen an ad before because their digital native capability allows them to navigate around ads with adept skill.

Or the easy solution for many Millennials is just watch Netflix because the platform is ad-less. The aversion to ads is so strong that traditional media giants such as Fox are experimenting with six-second ads because that is all a viewer can tolerate these days.

The traditional media giants were forced to adopt this new format after Alphabet’s YouTube rolled out micro-ads.

Popular browser Mozilla announced it will block all tracking scripts by default beginning in 2019, thwarting unregulated data collection and relentless ad pop-ups.

The reason why digital ads will have an existential crisis is because companies will be able to monetize the pure data, forcing companies with huge digital ad businesses such as Facebook (FB) to battle with the new competition that only wants your data and not hawk ads.

This is already happening in the e-brokerage space with disruptors such as Robinhood, which charges no commission and is more interested in collecting data and getting by with interest payment revenue.

Let’s face it, digital ads are not a high-quality business even though they are a high-margin business. As tech moves forward, the quality of tech will rise eliminating all low-grade tech that is still profiting in 2018.

On the business side of things, automation is replacing humans faster than humans realize, and the replacement will be an avatar representing the face of a company.

For lower-end services, an avatar chosen by the customer will populate to often give better service than a human can provide.

If this type of service is scaled, it would offer a massive cut in costs for American corporations saving on employee costs.

It will have the same effect that self-checkout kiosks have at supermarkets, wiping out another position at the low-end.

The front-end avatar that will service you is all possible because of the rapid advancement of artificial intelligence.

Every possible situation will be programmed in the software and executed briskly.

If customers desire the human touch, they will have to pay up.

Human interaction will command a premium price because human interaction cannot be automated.

The financial industry has a huge target on its back, and swaths of financial advisors could be sacked in favor of avatars with the functional software behind it to produce profits.

In fact, many financial advisors are instructed to refrain from recommendations now and urged to collect input to enter into a proprietary algorithm that will decide the customers’ portfolio.

Big banks have enjoyed their time in the sun, but technology will disrupt them in the near future. This is why you have seen huge run-ups in innovative fintech companies such as Square (SQ) and PayPal (PYPL).

Many forms of outside entertainment are on the chopping block, as well as indoor entertainment such as Hollywood.

Hollywood A-list actors command hefty premiums to contract their services, and that could all crumble if younger audiences prefer avatar-based films with the human roles performed by unknowns.

Johnny Depp earns more than $50 million for one movie, and these insane amounts could deflate rapidly if human participation in films becomes marginalized.

Ready Player One was a test case for how much technology could be infused into a movie, and the audience easily absorbed it.

I could argue that audiences could argue even more in this VR format.

The movie had a budget of $175 million, and returned $582 million at the box office.

The resounding success will encourage more directors to inject technology into their movies, and they will have to, if they hope to tempt younger audiences to the movie theater.

Going to the movie theater is another activity that has struggled to cope against the rise of Netflix and technology.

Theaters have been forced to improve the overall experience of watching a film with prime seating, comfortable seats, and other extras that never existed.

Every industry is going through the same headache of competing with technological disruption.

Stagnation is akin to surrendering in 2018.

And it wasn’t just a fringe director creating Ready Player One, it was visionary director Steven Spielberg, one of the most famous movie directors to ever exist.

This will pave the way for other lesser-known movie directors relying on technology to pump out the profits.

They wouldn’t be the first people or the first industry to go down this road either.

________________________________________________________________________________________________

Quote of the Day

“The worst thing a kid can say about homework is that it is too hard. The worst thing a kid can say about a game is it's too easy,” – said American media scholar Henry Jenkins III.

Mad Hedge Technology Letter

August 30, 2018

Fiat Lux

Featured Trade:

(ON TRUMP’S TECHNOLOGY ATTACK),

(AMZN), (GOOGL), (FB), (AMD), (TWTR)

First Amazon (AMZN), now Alphabet.

In a strategic move to fortify his base ahead of critical midterm elections, the President of the United States Donald J. Trump has denounced tech behemoth Alphabet (GOOGL) describing search results using his name as “rigged.”

If Trump loses the midterm elections, it could open a can of worms and threaten his position.

It is no surprise that he plans to invest 40 days traveling around America campaigning for Republicans in November.

This is a big deal.

Silicon Valley has been a frequent bashing target for the White House.

The data privacy fiasco of 2018 has offered ample ammunition to pretty much anyone who wants to rain on big tech’s parade.

Big tech has experienced a wave of bad press shifting public opinion against them ruining future guidance for social media companies such as Facebook (FB).

How does the administration’s attack against Alphabet affect its stock price going forward?

It won’t even blink.

Alphabet’s stock barely budged after the President used his Twitter (TWTR) feed to sound off against the famous digital search engine company.

The stock closed down 0.83% on the day.

We have seen this story again and again with the administration lashing out at certain sectors or individuals, only for the stock market to shrug off any resemblance of weakness and power higher to new all-time highs.

Resiliency would be the best way to characterize this market.

Ironically, Trump found time yesterday to tweet that the Nasdaq had just surpassed 8,000 for the first time, showing off the tech strength underpinning the nine-year bull market.

The FANGs are front and center the stars of the show. Grumbling about a prominent member of this cohort will do nothing to stop the profit engines that tech companies have constructed.

Stellar corporate earnings are the secret sauce in this recipe and investors would be crazy to veer away from that.

Investors have no reason to panic because the tech narrative will not go away anytime soon, and the market knows that.

Political turbulence has been baked into the pie, and it would be eerie if the airwaves went silent.

Investors have largely avoided pinpointing non-economic issues and focused on the economy and its robust 4% growth rate.

It helps that the unemployment rate has fallen to 3.9%, and the full labor market is a net positive, even though inflation and wage growth has yet to contribute as much as initially hoped.

Of course, politics play a substantial role in influencing the stock market. But looking back at the past crisis, the stock market reacted the same as it will now and go much higher.

The market is still very much a tech story, and last week’s price action confirmed this.

The Mad Hedge Technology Letter is still net negative on chip stocks, but the two chip stocks that circumvent my negative calls are companies I recommended recently and that have seen a breathtaking leg up.

Not all chip companies are made equal and Advanced Micro Devices, Inc. (AMD) proved that by spiking 35% so far in August, 23% in the past week, and more than 140% this year.

The hockey stick move has seen (AMD) short sellers singed to a tune of $3 billion in 2018.

Chip stocks were supposed to get crushed by the weight of the trade war. However, these two stalwarts prove that if you are in the right names, you’ll avoid the carnage, which has beset many smaller chip companies that have the bulk of revenue tied to China.

Tech companies have bought back more than $1 trillion of their own stock since the beginning of 2009 because they have the money to do so.

Silicon Valley companies continue to purchase back their own stocks at a furious pace, putting a floor under many cash cow tech firms to the benefit of share prices.

Whether you want to believe or not, the market is metamorphizing into an all-tech story as every sector migrates to the cloud and the heavy use of big data.

Industrial giants are turning into industrial IoT companies.

Turn over any stone and you would be hard pressed to not find some sort of tech in new products.

Silicon Valley is on the cusp of rolling out its self-autonomous driving technology for commercial operations with Alphabet’s subsidiary Waymo.

If that wasn’t a good reason to buy Alphabet, then let’s review the other positive levers in their portfolio.

Alphabet is one member of a two-man team dominating digital advertising revenues with Facebook.

Global media spend is expanding at 13% YOY as the migration to mobile sees no end.

Google has the best search engine in the world. There are no competitors even close to supplanting its holy grail search engine business, unless you consider bing.com a worthy competitor, which it isn’t.

Data is the new oil, and Alphabet is able to douse itself in data because of the gobs it possesses.

This is the reason Google knows everything about most people in the world outside of China.

Alphabet will be able to leverage this enormous treasure trove of big data and monetize it using artificial intelligence technology.

Add it all up and Alphabet is massively profitable and positioned on the vanguard of every future groundbreaking technology in the world.

Picking on the big boys won’t do much, and the stock price will power on unabated for the foreseeable future.

As the midterm elections draw closer, Trump could also double down on his foreign exploits attempting to consolidate political capital.

That means virulently attacking China’s trade policy, which could go into overdrive as they could give him the source of expansive buffer for which he is looking.

However, it is a double-edge sword as many constituents in red states could be the recipient of higher costs that elevated tariffs would bring.

At the bare minimum, Trump has cast a light on China’s unfair trading policies that has tapped an uneasy nerve for many other countries quietly agreeing with the American president.

This could create a whack-a-mole scenario as China could experience growing problems with numerous undeveloped countries felt wronged, and these headaches could take on different forms such as the Forest City project in Malaysia.

Back in the equity world, the smaller chip companies are baring the brunt of the administration’s scathing rhetoric toward China, but the economy, stock market, and consumer health will hum along as if nothing happened.

The damage is limited, giving Trump sufficient leeway to speak out about side issues as the vital midterm elections roll around.

The bull market is not close to dying and there is still room to run.

________________________________________________________________________________________________

Quote of the Day

“Technology itself is neither good nor bad. People are good or bad,” – said former CEO of InfoSpace, Inc. and cofounder of Moon Express Naveen Jain.

Mad Hedge Technology Letter

August 21, 2018

Fiat Lux

Featured Trade:

(THE CHIP MINI RECESSION IS ON),

(NVDA), (AMD)