Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, OR IS THIS A 1999 REPLAY?),

(AAPL), (FB), (NFLX), (AMZN), (GE), (WBT),

(JOIN ME ON THE QUEEN MARY 2 FOR MY JULY 11, 2018 SEMINAR AT SEA),

(JUNE 20 BIWEEKLY STRATEGY WEBINAR Q&A),

(SQ), (PANW), (FEYE), (FB), (LRCX), (BABA), (MOMO), (IQ), (BIDU), (AMD), (MSFT), (EDIT), (NTLA), Bitcoin, (FXE), (SPY), (SPX)

Below please find subscribers' Q&A for the Mad Hedge Fund Trader June 20 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader.

As usual, every asset class long and short was covered. You are certainly an inquisitive lot, and keep those questions coming!

Q: What are your thoughts on Square (SQ) as a credit spread or buyout proposition?

A: I love Square long term, and I think there's another double in it. They were a takeover target, but now the stock's getting so expensive it may not be worth it. So, Square is a buy. However, look for a summer sell-off to get into a new position.

Q: The FANGs feel a little bubbly here; will they pull back on a market dip?

A: Yes, my entire portfolio of FANG options is designed to expire on the July 20th expiration. In fact, I may even come out before then as we reach the maximum profit point on these option call spreads. Then look for a summer meltdown to get back in. The FANGs could double from here. If I am wrong they will just continue to go straight up.

Q: Palo Alto Networks (PANW) has a new CEO; are you concerned?

A: Absolutely not, I love Palo Alto networks, as well as the (FEYE) FireEye. It's just a question of getting in at the right price. It's one of the many ballistic stocks in Tech this year that we've been recommending for a long time. Hacking an online theft is never going to go out of style.

Q: Is it time to sell Facebook (FB)?

A: Yes, if you're a trader. No, if you're a long-term investor. There's another double in it. You're going to have natural profit taking on all of these Techs for the short-term, and possibly for the summer, because they've just had enormous runs. If you aren't in the FANGs this year, you basically don't have any performance because almost all of the rest of the market has gone down.

Q: What are your thoughts on Lam Research (LRCX)?

A: The whole chip sector has had two big sell-offs this year because of their China exposure and the trade wars. Expect more to come. China gets 80% of their chips from the U.S. This is normal at the end of a 10-year bull market. It's also normal when a sector transitions from highly cyclical to secular, which is what's happening in the chip sector. Twice the volatility gets you twice the returns.

Q: Would you stay away from Chinese stocks like Alibaba (BABA), Momo Inc.(MOMO), IQ (IQ), and Baidu (BIDU)?

A: I have stayed away because of the trade war fears, and it was the completely wrong thing to do, because they've gone up as much as our Tech stocks, except for the last week. So yes, I would be buying dips on these big Chinese Tech stocks, because they are drinking the same Kool Aid as our Techs, and it's working.

Q: I hear that short selling of volatility is coming back; is that a good thing?

A: Actually, it is a good thing, because it creates buyers on these dips when you had no short sellers left. The entire industry got wiped out in February creating $8 billion in losses. There was no one left to cover those shorts and support the market. Of course, the result was we got a lower low down here because of that. It's always better to have a two-way market to get a real price. Now professionals are sneaking back in on the short side, which is as it should be. This should never have been a retail product.

Q: Why are international markets so disconnected from the U.S.? Many Asian markets are down heavily while the U.S. are up.

A: The U.S. stock market benefits from a rising dollar and rising interest rates, whereas international markets suffer. When you have weak currencies in the emerging markets, people sell their stocks to avoid the currency hit, and that takes the emerging markets down massively. A lot of emerging market companies have their debts denominated in U.S. dollars, so they get killed by a strong greenback. Also, the emerging markets make a lot of money selling goods into China, so when the Chinese economy gets attacked by the U.S. and growth slows, it has the byproduct of attacking all our other allies in Southeast Asia.

Q: Is it a good idea to sell everything for the summer and just de-risk for my portfolio?

A: That's what I'm doing. Summer trading is usually horrible, and now we're going into the summer at close to a high for the year, with a terrible political backdrop and possible economic growth peaking right here. So, yes, it's a good time to sit back, count your money, and maybe even spend some of it on a European vacation.

Q: When do you think the yield curve will invert?

A: In a year, and that is typically when you get a peaking of economic growth and the stock market.

Q: Is the Fed's faster-than-expected desire to raise rates good for equities, or will investors likely sell this news as quantitative tightening continues?

A: Short-term they will buy the market on rising rates, they always do at the early part of an interest rate rising cycle. They sell stocks when you get to the middle or the end of a rate rising cycle.

Q: Do you think large Tech stocks are expensive here?

A: No, I think the Large-Cap Tech stocks can potentially double here. It can take another year to year and a half to do it, and if they don't do it in this cycle they will certainly do it in the next one, after the next recession in the 2020s. So, long term you want to think FANG, FANG, FANG, TECH, TECH, TECH. You really shouldn't have anything else in the long term, except for maybe Biotech, where you can now get in at a multiyear low.

Q: Can I buy a chip company like Advanced Micro Devices (AMD), or should I buy a cloud company, like Microsoft (MSFT)?

A: I would go with the Cloud company. The innovation there is incredible. Cloud is growing like the Internet itself was growing on its own in 1995, and with chip stocks like (AMD), you're going to get much higher volatility, but more gain. So, pick your poison. But I would go with the Cloud plays.

Q: Can we watch the recorded version of this webinar later?

A: Yes, we post the webinar on our website a couple hours later, if you're a paid subscriber.

Q: What about the CRISPR stocks?

A: They are a screaming buy right now, buy Editas Medicine (EDIT) and Intellia Therapeutics (NTLA) on the dip. The paper that triggered the sell-off saying that CRISPR causes cancer is complete BS.

Q: Only 30 million in Bitcoin was stolen in South Korea so will that still have an impact?

A: Yes, but there have been countless other hacks this year and the total loss is well over $500 million. In addition, Bitcoin is now down 70% from its December top so not all is well in cryptocurrency land.

Q: Should we expect any Trade Alerts before August 8?

A: Yes, some of my best trades have been done while only vacation. I once sold short the Euro (FXE) from the back of a camel in Morocco. Another time, I bought the S&P 500 (SPY) while hanging from a cliff face on the Matterhorn. Both of those made good money.

Q: Will the S&P 500 reach new highs before the end of the year?

A: Yes, once you get the election out of the way, that removes a huge amount of uncertainty from the market. If we could end our trade war before then, I think you're looking at another 10-15% in gains from this level by the end of the year. That takes you to an (SPX) of 3,100 by the end of 2018, which was my January 1 prediction.

Q: What does all the heavy mergers and acquisition activity mean for the market?

A: It means fewer stocks are left to trade. Stock shortages leads to higher prices, always, so it is a big market positive this year

Good Luck and Good Trading.

John Thomas

CEO and Publisher

The Diary of a Mad Hedge Fund Trader

The Chinese BATs (Baidu, Alibaba, and Tencent) are China's response to the American FANG group.

It's one of few sectors outperforming the vigorous American tech sector, and valuations have soared in the past year.

Former English teacher Jack Ma founded the Amazon (AMZN) of China named Alibaba in April 1999, which has grown to become one of the biggest websites on the Internet.

This company even has a massive cloud division that acts in the same way as Amazon Web Services (AWS).

Alibaba also has Alipay on its roster, the fintech and digital payments subsidiary of Alibaba.

Baidu, led by Robin Li, is the de-facto Google search of China and is entirely tailored for the Chinese market without English language support.

Tencent, created by Ma Huateng, has an assortment of businesses from social media, instant messaging, online gaming, and digital payments.

Tencent's WeChat platform is the lynchpin acting as the gateway to the robust Tencent eco-system.

The BATs have heavily invested in autonomous vehicle technology set to roll out in the coming years.

These companies are some of the biggest venture capitalists in the world throwing around capital like Masayoshi Son's SoftBank.

Alibaba has seen its share price rocket from $135 in June 2017 to $206.

Baidu has also seen huge gyrations in its share price elevating from $174 in June 2017 to $270.

Tencent, public on the Hong Kong Hang Seng Index, has gone from $273 HKD (Hong Kong dollars) to $412 HKD.

And this is all just the beginning!

An economy growing a stable 6.5% per year with companies able to scale to a mind-boggling 1.3 billion people is something of which to take notice.

China hopes to wean itself from its industrial heritage betting the ranch on a rapidly expanding tech sector.

Does this put China on a collision course steamrolling toward the American FANGs?

Highly possible but not yet.

Even though the BATs modus operandi has been to follow in the footsteps of the FANG's business model, they do not directly compete.

Ant Financial, the fintech arm of Alibaba, was blocked from purchasing MoneyGram International (MGI), effectively, closing any doors leading to the lucrative American digital payments industry.

This also meant curtains for WeChat, the multi-functional app that half of the Chinese use as a digital wallet, in the digital payments space.

The Committee on Foreign Investment in the United States (CFIUS) has made it crystal clear that BAT's capital will be scrutinized more than ever before because of China's open policy of transferring Western technology expertise to the mainland for the purpose of leading the world in technology.

China cannot have its cake and eat it.

The first stumbling block is that the American market does not suit the BAT's FANG business model with Chinese characteristics.

For example, the only other market Baidu search operates in is Brazil.

It has leveraged itself to the Chinese consumer whose purchasing power has spiked from its burgeoning middle class.

Another headwind is the lack of innovation caused by a rigid education system punishing freedom of thought in favor of rote memorization.

Innovation is American tech's bread and butter and investors pay up for this ingenuity that cannot be found elsewhere in the world.

This is also the reason why the BATs need to buy American technology and not the other way around.

Original concepts such as Uber and Airbnb were made in America first and Didi Chuxing and Tujia are rip-offs of these American companies.

The list is endless.

The BATs understand they cannot go head to head with American talent, but that does not mean they won't win out in the end.

To make matters worse, global tech talents do not want to work in China if they are reliant on America to develop something and copy it.

Why not just go work in Silicon Valley for a higher salary?

This was highlighted when the only tech talent to cross over to the other side quit in a blaze of glory.

Hugo Barra was poached from Alphabet in 2013, where he worked as vice present for the Android mobile operating system.

He was installed as the vice president of international development for smartphone maker Xiaomi, the Apple (AAPL) of China.

Barra suddenly threw in the towel at Xiaomi in 2017, offering a harsh critique stating, "What I've realized is that the last few years of living in such a singular environment have taken a huge toll on my life and started affecting my health."

Not exactly the stamp of approval the Mandarins were looking for.

In turn, China has focused its effort on recruiting Chinese-Americans who understand the working environment better and have roots or even family on the mainland.

The dire tech talent shortage is worse in China than Silicon Valley because Chinese tech companies have zero access to non-Chinese talent.

Even with a reverse in immigration policies by the administration, America continues to be the holy grail of tech jobs.

That is why you see hoards of Chinese, Indians, Russians, and every other country's best and brightest waiting in line to make the move.

Taiwanese American CEOs lead some of Silicon Valley's best companies such as the CEO for Nvidia (NVDA), Jensen Huang, and the CEO of Advanced Micro Devices (AMD), Dr. Lisa Su.

Only 1% of Baidu's revenues is extracted from American soil underscoring the BAT's China-first business model. Tencent isn't much better at 5%, and Alibaba heads the list at 11%.

Compare these statistics with Alphabet (GOOGL) making 53% and Facebook (FB) earning 56% of revenue from international sales.

Amazon is still very much an American business but 32% of revenue comes from international sales.

The bulk of this revenue is mainly from Europe where American large-cap tech companies are staunch mainstays.

China has focused on building out its business in Southeast Asia instead.

Those governments are cozy with Beijing and are willing to relinquish some sovereign influence to develop its poor digital infrastructure.

The nail in the coffin for potential BAT companies doing business in America is the total lack of data protection in China.

If you think what Facebook is doing doesn't make you sleep at night, the BATs are running riot with personal data in China.

Expect multiple attempts of hackers breaking into your email while your phone number is constantly harassed by spam messages and robo-calls galore.

This is a normal day in the life of a Chinese national and they are used to it.

China understands they are not ready to eclipse the juggernaut that is Silicon Valley.

The BATs are biding their time organically growing by investing into American tech firms helping their overall products and services.

The past five years have seen a gorge of American investment amounting to 95 deals totaling $27.6 billion.

However, this smash-and-grab investment party is effectively over because CFIUS has clamped down on exporting local technology.

Consequently, the BATs will continue to focus on what they know best - the Chinese market.

Southeast Asia is also ripe to become the next stomping ground for the BATs. Expect them to dominate in this region for years to come.

The runway is long in domestic China. The 6.5% annual growth is entirely biased toward these three companies to prolong their hearty growth trajectories.

The communist party even has a seat on the board at each of these companies highlighting another area of conflict if these companies dive head into the American market.

Let's just say corporate governance in China is a shell of what it is in America.

One day there could be an all-out battle for tech supremacy, but these Chinese companies would need some assurances they would likely come out on top.

That is hardly the case yet and they make way too much money by copying Silicon Valley.

"The leader of the market today may not necessarily be the leader tomorrow," - said Tencent founder and CEO Ma Huateng.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-06-18 01:05:272018-06-18 01:05:27Don't Worry About the BATs

How would you like to be part of the biggest business development in the history of mankind?

This revolution will increase business functionality up to 10 times while flattening costs by up to 90%.

Still interested?

Enter the Internet of Things (IoT).

The Internet of Things (IoT) can be boiled down to Internet connectivity with things.

Your luxury juice maker, hair removal kit, and multi-colored Post-its will soon be online.

No, you won't be able to have Tinder chats with the new connectivity, but embedded sensors, tracking technology, and data mining software will aggregate a digital dossier on how products are performing.

The data will be fed back to the manufacturing company offering a comprehensive and accurate review without ever asking a human.

The magic glue making IoT ubiquitous and stickier than a hornet's nest is the emergence and application of 5G.

4G is simply not fast enough to facilitate the astronomical surge in data these devices must process.

5G is the lubricant that makes IoT products a reality.

Verizon Communications (VZ) and AT&T (T) have been assiduously rolling out tests to select American cities as they lay the groundwork for the 5G revolution.

The aim is for these companies to deliver customers a velocious 1 Gbps (gigabits per second) wireless connection speed.

Delivering more than 10 times the average speed today will be a game changer.

America isn't the only one with skin in the game and some would say we are not even leading the pack.

China Mobile (CHL) is carrying out a bigger test in select Chinese cities, and Chinese telecom company Huawei can lay claim to 10% of the 5G patents.

Americans should start to notice broad-based adoption of 5G networks around 2020.

Once widespread usage materializes, watch out!

It will go down in history books as a transformational headline.

The IoT revolution will follow right after.

Until the 5G rollout is done and dusted, tech companies are licking their chops and preparing for one of the biggest shifts in the tech ecosphere affecting every product, service, and industry.

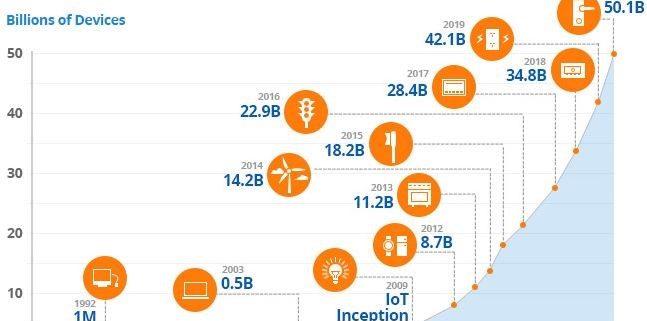

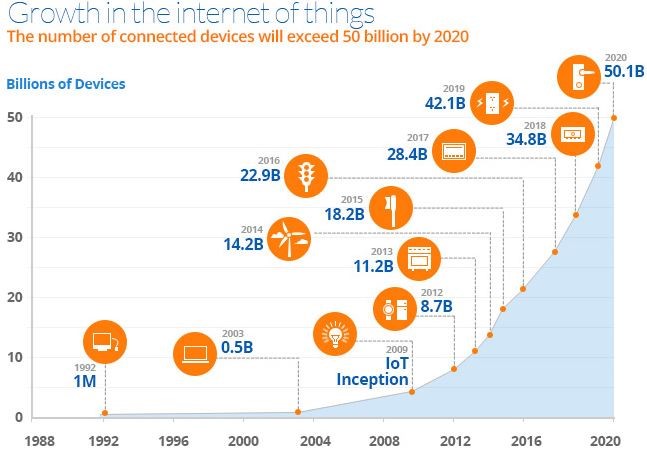

The worldwide IoT market is poised to mushroom into a $934 billion market by 2025 on the back of cloud computing, big data, autonomous transport technology, and a host of other rapidly emerging technology.

The arrival of 5G will have an astronomical network effect. Companies will be able to enhance product specs faster than before because of the feedback of data accumulated by the tracking technology and sensors.

The appearance of this flashy new technology will spawn yet another immeasurable migration to technological devices by 2020.

In just two years, the world will play host to more than 50 billion connected devices all pumping out data as well as consuming data.

What a frightful thought!

IoT's synergies with new 5G technology will have an unassailable influence on the business environment.

For instance, industrial products in the form of robots and equipment will be a huge winner with 5G and IoT technology.

The industrial IoT market is expected to sprout to $233 billion by 2023.

Robots will pervade deeply into economic provenance acting as the mule for brute strength heavy labor plus more advanced tasks as they become more sophisticated.

Total global spending related to IoT products will surpass 1.4 trillion dollars by 2021, according to the International Data Corporation (IDC).

IoT growth will become most robust in the thriving Asian markets fueled by a bonus tailwind of the fastest growing region in the world.

The advanced automation abilities of Germany and the U.K. will also give them a seat at the table.

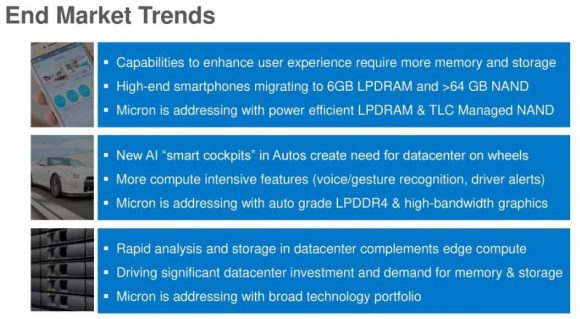

Micron CEO Sanjay Mehrotra gushed about the future at Micron's investor day celebrating IoT and data as the way forward. Mehrotra explained that the explosion of IoT products will create a new tidal wave of "growing demand for storage and memory."

Chips are a great investment to grab exposure to the 5G, IoT, and big data movement.

Up until today, the last generation of technological innovation brought consumers computers and smartphones.

That world has moved on.

Open up your eyes and you will notice that literally everything will become a "data center on wheels or on feet."

To arrive at this stage, products will need chips.

As many high-grade chips as they can find.

Data centers are one segment in dire need of chips. This market will more than double from $29 billion in 2017 to $62 billion in 2021.

The general-purpose chip market for servers is cornered by Intel.

Industry insiders estimate Intel's market share at 98% to 99% of data center chips. Clientele are heavy hitters such as Amazon Web Services, Google, and Microsoft Azure along with other industry peers.

The only other players with data server chips out there are Qualcomm (QCOM) and Advanced Micro Devices Inc. (AMD).

However, there have been whispers of Qualcomm shutting down the 48-core Centriq 2400 chip for data centers that was launched only last November after head of Qualcomm's data center division, Anand Chandrasekher, was demoted via reassignment.

AMD's new data center chip, Epyc, has already claimed a few scalps with Baidu (BIDU) and Microsoft Azure promising to deploy the new design.

IoT integration is the path the world will take to adopting full-scale digitization.

Microsoft just announced at its own Build 2018 conference its plans to invest $5 billion into IoT in the next four years.

The Redmond, Washington-based company noted operational savings and productivity gains as two positive momentum drivers that will benefit IoT production.

Consulting firm A.T. Kearny identified IoT as the catalyst fueling a $1.9 trillion in productivity increases while shaving $177 billion off of expenses by 2020.

These cloud platforms give tech companies the optimal stage to win over the hearts and dollars of non-tech and tech companies that want to digitize services.

Many of these companies will have IoT products percolating in their portfolio.

Examples are rampant.

Schneider Electric in collaboration with Microsoft's IoT Azure platform brought solar energy to Nigeria by the bucket full.

The company successfully installed solar panels harnessing its performance using IoT technology through the Microsoft cloud.

Kohler rolled out a new lineup of smart kitchen appliances and bathroom fixtures coined "Kohler Konnect" with the help of Microsoft's Azure IoT platform.

Consumers will be able to remotely fill up the bathtub to a personalized temperature.

Real-time data analytics will be available to the consumer by using the bathroom mirror as a visual interface with touch screen functionality giving users the option to adjust settings to optimal levels on the fly.

Kohler's tie-up with Microsoft IoT technology has proved fruitful with product development time slashed in half.

To watch a video of Kohler's new budding relationship with Microsoft's Azure IoT platform, please click here.

It is safe to say operations will cut out the wastefulness using these new tools.

Look no further than legacy American stocks such as oil and gas producer Chevron (CVX), which wants a piece of the IoT pie.

Chevron announced a lengthy seven-year partnership with Microsoft's Azure platform.

The fiber optic cables inside oil production facilities generate more than 1 terabyte of data per day.

In the Houston, Texas, offices, sensors installed six miles below the surface shoot back data to engineers who monitor human safety and system operations on four continents from the Lone Star State.

The newest facility in Kazakhstan, using state-of-the-art technology, will produce more data than all the refineries in North America combined.

Using the aid of artificial intelligence (A.I.), computers will analyze seismic surveys. This pre-emptive technology customizes solutions before problems can germinate.

The new smart-work environment will multiply worker productivity that has been at best stagnant for the past generation.

To get in on the IoT action, buy shares of companies with solid IoT cloud platforms such as Microsoft and Amazon.

Buy best-of-breed chip companies such as Nvidia (NVDA), Intel (INTC), Advanced Micro Devices (AMD) and Micron (MU).

And buy tech companies that produce wafer fab equipment such as Applied Materials (AMAT) and Lam Research (LRCX).

"Don't be afraid to change the model." - said cofounder and CEO of Netflix Reed Hastings.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/05/Growth-in-the-IOT-image-4.jpg449647MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-05-29 01:05:272018-05-29 01:05:27Here Are Some Early 5G Wireless Plays

The Amazon (AMZN) and Netflix (NFLX) model is not the only technology business model out there.

Micron (MU) has amply proved that.

Bulls were dancing in the streets when Micron announced a blockbuster share buyback of $10 billion starting in September.

This is all from a company that lost $276 million in 2016.

The buyback is an overwhelmingly bullish premonition for the chip sector that should be the lynchpin to any serious portfolio.

The news keeps getting better.

Micron struck a deal with Intel to produce chips used in flash drives and cameras. Every additional contract is a feather in its cap.

The share repurchase adds up to about 16% of its market value and meshes nicely with its choreographed road map to return 50% of free cash flow to shareholders.

Tech's weighting in the S&P has increased 3X in the past 10 years.

To put tech's strength into perspective, I will roll off a few numbers for you.

The whole American technology sector is worth $7.3 trillion, and emerging markets and European stocks are worth $5 trillion each.

Tech is not going away anytime soon and will command a higher percentage of the S&P moving forward and a higher multiple.

The $5 billion in profit Micron earned in 2017 was just the start and sequential earnings beats are part of their secret sauce and a big reason why this name has been one of the cornerstones of the Mad Hedge Technology Letter portfolio since its inception as well as the first recommendation at $41 on February 1.

Did I mention the stock is dirt cheap at a forward PE multiple of just 6 and that is after a 35% rise in the share price so far this year?

What's more, putting ZTE back into business is a de-facto green light for chip companies to continue sales to Chinese tech companies.

China consumed 38% of semiconductor chips in 2017 and is building 19 new semiconductor fabrication plants (FAB) in an attempt to become self-sufficient.

This is part of its 2025 plan to jack up chip production from less than 20% of global share in 2015 to 70% in 2025.

This is unlikely to happen.

If it was up to them, China would dump cheap chips to every corner of the globe, but the problem is the lack of innovation.

This is hugely bullish for Micron, which extracts half of its revenue from China. It is on cruise control as long as China's nascent chip industry trails miles behind them.

At Micron's investor day, CFO David Zinsner elaborated that the mammoth buyback was because the stock price is "attractive" now and further appreciation is imminent.

Apparently, management was in two camps on the capital allocation program.

The two choices were offering shareholders a dividend or buying back shares.

Management chose share repurchases but continued to say dividends will be "phased in."

This is a company that is not short on cash.

The free cash flow generation capabilities will result in a meaningful dividend sooner than later for Micron, which is executing at optimal levels while its end markets are extrapolating by the day.

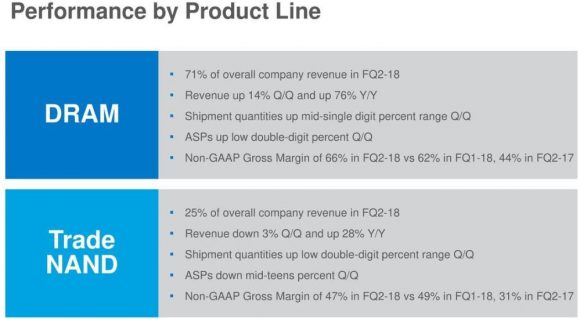

As it stands today, Micron is in the midst of taking its 2017 total revenue of about $20 billion and turning it into a $30 billion business by the end of 2018.

The overall chips market is as healthy as ever and data from IDC shows total revenues should grow 7.7% in 2018 after a torrid 2017, which saw a 24% bump in revenues.

The road map for 2019 is murkier with signs of a slowdown because of the nature of semi-conductor production cycles. However, these marginal prognostications have proved to be red herrings time and time again.

Each red herring has offered a glorious buying opportunity and there will be more to come.

Consolidation has been rampant in the chip industry and shows no signs of abating.

Almost two-thirds of total chip revenue comes from the largest 10 chip companies.

This trend has been inching up from 2015 when the top 10 comprised 53% in 2016 and 56% in 2017.

If your gut can't tell you what to buy, go with the bigger chip company with a diversified revenue stream.

The smaller players simply do not have the cash to splurge on cutting-edge R&D to keep up with the jump in innovation.

The leading innovator in the tech space is Nvidia, which has traded back up to the $250 resistance level and has fierce support at $200.

Nvidia is head and shoulders the most innovative chip company in the world.

The innovation is occurring amid a big push into autonomous vehicle technology.

Some of the new generation products from Nvidia have been worked on diligently for the past 10 years, and billions and billions of dollars have been thrown at it.

Chips used for this technology are forecasted to grow 9.6% per year from 2017-2022.

Another death knell for the legacy computer industry sees chips for computers declining 4% during 2017-2022, which is why investors need to avoid legacy companies like the plague, such as IBM and Oracle because the secular declines will result in nasty headlines down the road.

Half way into 2018, and there is still a dire shortage of DRAM chips.

Micron's DRAM segments make up 71% of its total revenue, and the 76% YOY increase in sales underscores the relentless fascination for DRAM chips.

Another superstar, Advanced Micro Devices (AMD), has been drinking the innovation Kool-Aid with Nvidia (NVDA).

Reviews of its next-generation Epyc and Ryzen technology have been positive; the Epyc processors have been found to outperform Intel's chips.

The enhanced products on offer at AMD are some of the reasons revenue is growing 40% per year.

AMD and Nvidia have happily cornered the GPU market and are led by two game-changing CEOs.

It is smart for investors to focus on the highest quality chip names with the best innovation because this setup is most conducive to winning the most lucrative chip contracts.

Smaller players are more reliant on just a few contracts. Therefore, the threat of losing half of revenue on one announcement exposes smaller chip companies to brutal sell-offs.

The smaller chip companies that supply chips to Apple (AAPL) accept this as a time-honored tradition.

Avoid these companies whose share prices suffer most from poor analyst downgrades of the end product.

Cirrus Logic (CRUS), Skyworks Solutions (SWKS), and Qorvo Inc. (QRVO) are small cap chip companies entirely reliant on Apple come hell or high water.

Let the next guy buy them.

Stick with the tried and tested likes of Nvidia, AMD, and Micron because John Thomas told you so.

"Bitcoin will do to banks what email did to the postal industry." - said Swedish IT entrepreneur and founder of the Swedish Pirate Party Rick Falkvinge.

Fetch a measuring stick from the cupboard, gauge the levels of innovation around Silicon Valley, and Nvidia's name floats straight to the top of the list.

Nvidia has it all and more.

Not many firms can brandish one of the best CEOs in all of tech.

Nvidia CEO Jensen Huang is a true visionary.

When he hops on earnings calls, investors and analysts rejoice about the breadth of innovation percolating through the corridors in Santa Clara, CA.

Nvidia was able to increase quarterly revenue by an eye-popping 61% YOY. And this company is one of the quintessential growth companies in tech.

Huang is one of the few CEOs confident enough to talk all the way through the earnings call like he is talking about the back of his hand.

Most CEOs delegate to the CFO after a carefully choreographed introductory statement.

He knows everything about the company and is not afraid to go into detail.

The past few weeks have been hell for chip companies.

The cascade of downgrades undercut momentum with chip shares prices falling across the board.

Every nonsensical downgrade has proved unjustified with chip earnings displaying the robust potency that only FANGs can replicate.

Delve into Nvidia's latest performance and two parts of the business have gone into overdrive.

Gaming has burst to the forefront providing a sturdy pillar to Nvidia's income stream.

Fortunately, crypto mining and e-gamers are dual drivers fueling a rapidly expanding market.

In Q1, crypto miners and e-gamers faced a hysterical "scarcity" of high grade GPU hardware.

To make matters worse, Apple and Samsung are using the same memory as graphic cards.

These two global giants front ran other companies agreeing pricier per unit contracts to guarantee sufficient supply for their product lineup.

This led to a huge famine or feast environment to secure the necessary components.

Huang has ensured investors that Nvidia is moving mountains to meet demand and he hopes prices will "normalize" in the upcoming quarter.

Advanced Micro Devices (AMD) is the other player producing GPU chips that is experiencing a demand overload.

On the last sell-off, AMD dropped as low as 9.50 and was the perfect entry point into a great company led by Lisa Su, PhD.

AMD continued to bounce off the $9 handle and is trading at $13 after an outstanding earnings report.

Huang also caveated his hopes of chip prices normalizing by saying the "pent-up demand" could get worse because of the unbelievable gaming options in the market, such as blowout title Fortnite and popular online game Player Unknown's Battlegrounds that have sold more than 40 million copies throughout various platforms.

Nvidia has caught the innovation bug with new products coming off the conveyer belt sooner than expected.

Nvidia has announced NVIDIA RTX, the "holy grail" of graphic performance that will offer gamers Hollywood cinematic production quality lighting, reflections, and shadows.

This product has been in the works for the past 10 years and has gamers and miners drooling over this new technology called ray tracing.

Revenue from crypto miners is not a part of Nvidia's core mission, and the stronger than expected numbers are just the beginning.

If bitcoin takes another stab at $20,000, GPU demand will go through the roof.

As the price of cryptocurrencies rise, the profit-making opportunities to mine are greatly enhanced.

Another division running on all cylinders showing no sign of slowing down is the data center segment.

Initially, this industry was tabbed by Nvidia as a $30 billion opportunity by 2020.

They were completely wrong.

Nvidia moved the goal posts and announced at a recent investors day that it believes data center revenue will be a $50 billion market by 2023.

Data center revenue spiked 71% YOY to $701 million highlighting the innovation leadership Nvidia enjoys.

The data center incorporates Nvidia's Volta architecture and adoption has been broad-based.

Volta offers 500% more deep learning power than its previous edition Pascal.

The stamp of approval is evident with every major cloud player embracing the Volta technology.

At some points during the earnings call, it appeared to be a commercial for data center, gaming and crypto because of the strength of these two segments.

Huang did talk about other businesses such as autonomous driving buttering up its place in Nvidia's lineup.

Autonomous driving will be a $60 billion opportunity by 2035, according to conservative estimates.

Nvidia's DRIVE Constellation continues to be the bread-and-butter platform for automotive companies.

The platform allows car companies to use virtual reality (V.R.) to carry out driving trials.

Two servers have been built to aid in development.

The first server allows simulation in the form of a pseudo video game, and the other server is used to process the simulated data.

In whole, autonomous driving lagged gaming and data center with 4% growth YOY.

This should not alarm investors because Nvidia is in it for the long run.

The software system and infotainment in the first generation of commercial autonomous vehicles will have plenty of Nvidia chips hovering around under the hood.

At some point, every vehicle in the world will require autonomous technology. As Nvidia stays ahead of the innovation curve, buyers will gravitate toward its products.

The architecture of Nvidia chips allows car companies to advance their autonomous vehicle technology.

Nvidia is partnering with other industry leaders such as Tesla and Mercedes Benz, just to name a few.

Going forward developers will harness the power of artificial intelligence (A.I.) to build new software programs for the car.

The new car software will be part and parcel with voice recognition that has quickly come to the forefront of tech development.

Creating a whole autonomous vehicle system to just drag and drop into its business could lead to Nvidia's products becoming the industry standard.

Technical superiority eventually wins out.

Nvidia has diversified into every cutting-edge trend in technology.

Huang understands that to keep buyers salivating over its products, they must be the highest quality.

The reason Alphabet (GOOGL) or Apple partner and synergize with Nvidia so well is because it makes the best of the best and they cannot copy their products.

This is why ZTE, one of the biggest tech companies in China, practically went out of business after Donald Trump cut of its pipeline of critical American components.

Chinese companies have been attempting to buy American chip companies for years because the quality of chips is significantly superior.

Amid a backdrop of a trade war, Nvidia shares have been trading choppily from a strong support level of $200.

It is only a matter of time before Nvidia explodes through the $250 resistance level and climbs higher.

To watch a video demonstration on Nvidia's new RTX ray tracing technology click here.

"The United States must possess unquestioned capacity to launch crippling counter-cyberattacks. This is the warfare of the future ... America's dominance in this arena must be unquestioned and today, it's totally questioned." - said President of the United States Donald J. Trump.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-05-17 01:05:062018-05-17 01:05:06Nvidia Nails it Again

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.