Mad Hedge Technology Letter

December 18, 2020

Fiat Lux

Featured Trade:

(TECH IN 2021)

(ZM), (WORK), (NVDA), (AMD), (QCOM), (SQ), (PYPL), (INTU), (PANW), (OKTA), (CRWD), (SHOP), (MELI), (ETSY), (NOW), (AKAM), (TWLO)

Mad Hedge Technology Letter

December 18, 2020

Fiat Lux

Featured Trade:

(TECH IN 2021)

(ZM), (WORK), (NVDA), (AMD), (QCOM), (SQ), (PYPL), (INTU), (PANW), (OKTA), (CRWD), (SHOP), (MELI), (ETSY), (NOW), (AKAM), (TWLO)

The tech sector has been through a whirlwind in 2020, and if investors didn’t lose their shirt in March and sell at the bottom, many of them should have ended the year in the green.

My prediction at the end of 2019 that cybersecurity and health cloud companies would outperform came true.

What I didn’t get right was that almost every other tech company would double as well.

Saying that video conferencing Zoom (ZM) is the Tech Company of 2020 is not a revelation at this point, but it shows how quickly a hot software tool can come to the forefront of the tech ecosystem.

M&A was as hot as can be as many cash-heavy cloud firms try to keep pace with the Apples and Googles of the tech world like Salesforce’s purchase of workforce collaboration app Slack (WORK).

Not only has the cloud felt the huge tailwinds from the pandemic, but hardware companies like HP and Dell have been helped by the massive demand for devices since the whole world moved online in March.

What can we expect in 2021?

Although I don’t foresee many tech firms making 100% returns like in 2020, they are still the star QB on the team and are carrying the rest of the market on their back.

That won’t change and in fact, tech will need smaller companies to do more heavy lifting come 2021.

The only other sector to get through completely unscathed from the pandemic is housing, and unsurprisingly, it goes hand in hand with converted remote offices that wield the software that I talk about.

The world has essentially become silos of remote offices and we plug into the central system to do business with each other with this thing called the internet.

In 2021, this concept accelerates, and cloud companies could easily check in with 20%-30% return by 2022. The true “growth” cloud firms will see 40% returns if external factors stay favorable.

This year was the beginning of the end for many non-tech businesses and just because vaccines are rolling out across the U.S. doesn’t mean that everyone will ditch the masks and congregate in tight, indoor places.

There is nothing stopping tech from snatching more turf from the other sectors and the coast couldn’t be clearer minus the few dealing with anti-trust issues.

I can tell you with conviction that Facebook, Google, Apple, and Amazon have run out of time and meaningful regulation will rear its ugly head in 2021.

We are already seeing the EU try to ratchet up the tax coffers and lawsuits up the wazoo on Facebook are starting to mount.

Eventually, they will all be broken up which will spawn even more shareholder value.

Even Fed Chair Jerome Powell told us that he thinks stocks aren’t expensive based on how low rates have become.

That is the green light to throw new money at growth stocks unless the Fed signal otherwise.

As we head into the 5G world, I would not bet against the semiconductor trade and the likes of Nvidia (NVDA), AMD (AMD), Qualcomm (QCOM) should overperform in 2021.

Communication is the glue of society and communications-as-a-platform app Twilio (TWLO) will improve on its 2020 form along with cloud apps that make the internet more efficient and robust like Akamai (AKAM).

Workflow cloud app ServiceNow (NOW) is another one that will continue its success.

The uninterrupted shift to the cloud will not stop in 2021 and will be a strong growth driver for numerous tech companies next year.

I will not say this is a digital revolution, but as corporate executives realize they haven’t spent enough on the cloud in the lead-up to the pandemic and must now play catch-up in order to satisfy new demands in the business.

The most recent CIO survey was the thesis that cloud and digital adoption at 10% of enterprise and 15% of consumer spend entering 2020 would continue to accelerate post-pandemic and into 2021-2022.

A key dynamic playing out in the tech world over the next 12 to 18 months is the secular growth areas around cloud and cybersecurity that are seeing eye-popping demand trends.

Consumers will still be stuck at home, meaning e-commerce will still be big winners in 2021 such as Shopify (SHOP), Etsy (ETSY), and MercadoLibre (MELI).

The reliance on e-commerce will open the door for more tech companies to participate in the digital flow of transactions and the U.S. will finally catch up to the Chinese idea of paying through contactless instruments and not cards.

This highly benefits U.S. fintech companies like Square (SQ) and PayPal (PYPL). Intuit (INTU) and its accounting software is another niche player that will dominate.

Intuit most recently bought Credit Karma for $8.1 billion signaling deeper penetration into fintech.

Since we are all splurging online, we need cybersecurity to protect us and the likes of Palo Alto Networks (PANW), Okta (OKTA), and CrowdStrike Holdings, Inc. (CRWD).

The side effect of the accelerating shift to digital and cloud are troves of data that need to be stored, thus anything related to big data will also outperform.

Most of the information created (97%) has historically been stored, processed, or archived.

As new mountains of digital gold are created, we expect AI will have an increasingly critical role.

I believe that 2021 will finally see the integration of 5G technology ushering in another wave of digital migration and data generation that the world has never seen before and above are some of the tech companies that will make out well.

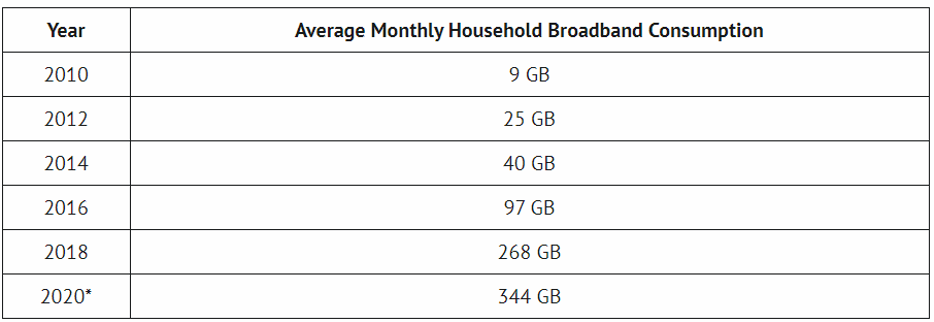

The average household is using 38x the amount of internet data they were using ten years ago and this is just the beginning.

Mad Hedge Technology Letter

December 14, 2020

Fiat Lux

Featured Trade:

(NVIDIA’S SHOW OF FORCE)

(NVDA), (AMD), (APPL), (OTC:SFTBF), (INTC), (QCOM)

One of the best buy and hold tech stock has to be Nvidia (NVDA).

They are positioned at the vanguard of every major cutting-edge technology in the world such as self-driving technology, data center, and artificial intelligence.

Their cash cow business of manufacturing GPUs (graphics processing unit) which are essential to video gaming has been bolstered by the shelter-at-home movement.

Video games as an activity or something to just pass the time has never been so popular and Nvidia is the best of breed in this department.

The key takeaway from Nvidia’s asset portfolio is the diversity.

They aren’t beholden to any one division and I wouldn’t bet anytime soon that video games are going to go out of fashion because of the generational tailwind occurring.

In fact, the underlying Nvidia stock has risen more than 120% in 2020 and semiconductors have proven to be an astute place to put your money in during the pandemic.

The same goes for competitive rivals such as Advanced Micro Devices (AMD), Intel (INTC), and Qualcomm (QCOM) who explore some of those same markets.

Nvidia counts Amazon (AMZN) Web Services as a customer for data-center chips. It is partnering with VMware (VMW) and Amazon on an AI-driven cloud platform for big businesses.

Be mindful that semiconductor stocks are volatile because of the boom-bust nature of their business cycle.

Global chip sales cratered in late 2018 and fell 12% in 2019.

They rallied early this year on signs of an industry recovery and on a U.S.-China trade deal, then sold off on coronavirus fears.

The trade war has also thrown a spanner in the works of global chip production.

Production was first halted in China and then put global economies under strain.

Despite the pandemic, the semiconductor industry will return to growth in 2020.

Chip sales will rise by 5.1% to $433 billion this year and accelerate to 8.4% in 2021.

The spread of 5G wireless networks is a key catalyst.

Moving forward, it’s highly likely that U.S. lawmakers maintain an anti-China doctrine, and Nvidia and AMD derive only 1% to 2% of revenue from Huawei.

In fact, other companies are more exposed like Cisco and Intel.

How well is Nvidia doing?

They increased revenue by 57% year over year in the third quarter predominately due to its data center business, which grew revenue by 162% over the same period.

In Q3, the data center division accounted for $1.9 billion of the company's $4.7 billion of revenue.

Nvidia is also growing through acquisitions with its blockbuster pending $40 billion acquisition of chip design licensor ARM Holdings from Softbank (OTC:SFTBF).

ARM’s acquisition will help NVIDIA maintain the best of breed quality through 2021 and beyond.

That is important because the semiconductor industry is becoming more cutthroat with many big players sourcing chips in-house after deeply investing in this technology.

Apple (AAPL) recently unveiled its own stable of Mac processors, the M1, making its debut in late 2020. Manufacturing chips is historically a capital-intensive activity, and new chips don’t roll out that fast. In any case, cash-rich companies the size of Google and Apple have the firepower to pull this off.

ARM holds many unique patents forcing many companies to license from them, Apple can customize those designs, and the actual fabrication is outsourced to Taiwan Semiconductor (TSM), the largest and most technologically advanced semiconductor fabricator in the world.

In this specific case, Intel is the direct loser from the production of Apple M1 chips and at this point, this is becoming an existential crisis for Intel.

The acquisition of ARM is a gamechanger, and not just because NVIDIA would gain access to new markets like CPUs for mobile as early as 2021.

Integrating with ARM signals NVIDIA's future shift toward licensing of technology - a far more stable business model than the traditionally cyclical nature of semiconductor industry sales driven by upgrade cycles.

It all comes down to the quality of NVIDIA's chips which remain highly competitive in secular growth areas of tech, such as data centers and artificial intelligence. This alone should keep NVIDIA high up investors' list for years to come.

Demand for the new Nvidia GeForce RTX GPU has been “overwhelming” and the company completed its Mellanox acquisition, a tech firm that sells adapters, switches, software, cables, and silicon for markets including high-performance computing, data centers, cloud computing, computer data storage, and financial services, in April, helping it to double down on their revenue drivers.

Sales for Nvidia's chips remain robust across some of the most desirable end markets and there is nothing meaningful out there to suggest that Nvidia won’t continue its overperformance next year even if the shelter-at-home economy stops.

I am highly bullish on Nvidia stock into 2021 and beyond.

Mad Hedge Technology Letter

October 30, 2020

Fiat Lux

Featured Trade:

(THE TWO CAN'T-MISS CHIP COMPANIES)

(NVDA), (AMD), (XLNX), (ARM)

I want to talk about two companies that are the “no-brainers” of the semiconductor space that would give you a call option on the data center space.

Let’s take a quick look back at some of their latest moves and what it would mean for your tech portfolio.

A few months ago, Nvidia said it would buy British chip company Arm from SoftBank for $40 billion in a stock and cash deal.

CEO Jensen Huang admitted that while the company's acquisition of the rival British chipmaker was a little on the expensive side, it would make sense in the long-term.

“I had to pay you an arm and a leg for it,” the Nvidia CEO said, and “I told you I was going to be the last and highest bidder.”

Overpaying for high quality companies is something that is only possible from a position of strength.

Huang justified Arm’s price tag saying that the chipmaker’s network of customers made it worthwhile and that he wants to expose those customers to Nvidia’s artificial intelligence technology.

Cross-selling the products and services is where the synergies between the companies can be exploited.

AMD is the other player that is really crushing it along with Nvidia and they recently made a deal to acquire Xilinx.

The deal is a direct response to Nvidia’s attempts to become the leader in high performance computing.

Obviously, the acquisitions are made possible because of years of refining their balance sheets and buying into more growth is a time-honored strategy that tech companies focus on.

AMD will give Nvidia a run for their company with a combined additional 13,000 talented engineers and over $2.7 billion in annual R&D investments.

This is very much a talent grab as well as a revenue grab.

Xilinx offers AMD access to adaptive platforms in critical areas such as 5G and automotive.

The tie-up is a transformational opportunity to tap into a total addressable market of $110 billion, up from previous AMD standalone estimates of $79 billion for 2022.

Xilinx adds about $31 billion to the total addressable market and on the operational side, AMD will see gross margins spike from 45% to 51%.

Even more impressive, operating income margins will surge to 21%, up from 16%.

It’s not like AMD needed much help, as they smashed expectations by growing 55.6% and beating estimates by $240 million in the latest earnings report.

EPS beat analyst estimates by $0.06 providing the highest level of earnings in years at $0.41 per share.

The Computing and Graphics division beats estimates with revenues of $1.67 billion.

The ramp-up of new consoles and data center sales led to a mindboggling 101% sequential revenue increase.

The company’s server processor revenue almost doubled compared with the year earlier, and AMD is on track to begin shipping its next-generation server processors later this year.

The current and future status of gaming is very much tied to the fortunes of Nvidia and AMD and the pandemic has fueled massive migration to time spent playing video games.

Who would have thought if people can’t go outside, more video games would be played?

The new generation of consoles is set to launch in November from Microsoft (MSFT) and Sony (SNE) which has helped boost AMD’s gaming chip business.

Typically, this gaming chip segment drops in the fourth quarter, but this year it will mushroom because of the new console launches and ramp-up in production and sales.

Ultimately, in terms of the Xilinx (XNLX) deal, it is complimentary to AMD’s business – an appetizer to the main dish.

It will help improve the company’s ability to support data center customers and adds exposure to sectors such as automotive, aerospace, defense, and industrials.

Through Xilinx’s field-programmable gate array (FPGA) chips—or semiconductors that can be reprogrammed after production, unlike most semiconductors—AMD could benefit from the tail end of the 5G upgrade cycle, too.

That’s because with many emerging technologies, it’s too expensive to experiment with chips with instructions that are set in stone, and build emerging infrastructure such as 5G.

Xilinx’s businesses also tend to retain customers for longer because its strong designs can lead to longer product cycles.

Together, Xilinx and AMD will also operate at a significantly larger scale, which should improve margins and cash flow.

These deals will create a leading supplier of chips for edge-network base stations.

Unlike in the data center market where general-purpose chips win, edge networks require chips that are good at specific things: low-latency, custom-built, specific units.

Those are all things AMD and Xilinx are good at making. Edge computing is a concept that refers to moving processing power and data storage closer to where it’s needed, thus improving performance on local machines.

In short, Nvidia and AMD are the leading lights of the semi-chip industry involved in all the growth industries from artificial intelligence, data centers, video gaming, and self-driving technologies.

I am highly bullish both.

Global Market Comments

October 15, 2020

Fiat Lux

Featured Trade:

(OCTOBER 14 BIWEEKLY STRATEGY WEBINAR Q&A),

(VXX), (INDU), (TLT), (GLD), (IB), (XPEV),

(TSLA), (MRNA), (AMD), (SDS), (ITB)

Below please find subscribers’ Q&A for the October 14 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: Do you think Interactive Brokers (IB) will give better executions?

A: No, these executions are all done by identical computers with identical programs now, across eleven differences of electronic exchanges. It’s like trying to decide whether to buy Exxon or Mobile gas. It’s all the same stuff. The only real difference in brokers these days is in customer service; and you really have to shop around there and find what you like. Even on customer service, most brokers have cut back staff to a minimum. In the end, the only difference among brokers may be “hold” times.

Q: What are your thoughts on Xpeng, Inc. (XPEV), the Chinese electric car manufacturer?

A: The Chinese have actually had electric cars longer than Tesla (TSLA) has and I have visited their factories in China, like BYD Auto (https://en.wikipedia.org/wiki/BYD_Auto). The problem has always been quality—the batteries tend to catch on fire, the cars fall apart—and that’s why they have never exported an electric car to the U.S. I don't expect that to change. What’s more likely is Tesla building more factories in China, where they overwhelmingly have the technology, brand, and quality lead. I don't think any electric car company can threaten Tesla now that they’re so far ahead.

Q: Is it a good time to buy the iPath S&P 500 VIX Short Term Futures ETN (VXX)?

A: No, because you only make money on the (VXX) when you get a volatility increase almost immediately after you buy it. So, if you have some great insight on the next volatility explosion, try it; otherwise, the time decay will kill you. By the way, everyone knows there is going to be a presidential election in three weeks so it’s already in the price.

Q: What is the likelihood of a financial transaction tax, and how would it affect our trading?

A: It wouldn't hurt our trading, because we’re mostly small fry. It would wipe out high-frequency trading where they’re trading for a penny with no transaction costs. And that, in fact, would be the goal: to wipe out high-frequency trading. Unfortunately, they’re about 80% of the market now, so I’m not sure who would step in and fill in that space. But there’s always someone.

Q: What about Moderna (MRNA)?

A: Yes, I like it for the long term. I think next year will be another golden age for biotech, and they have had a great rally so I’d be looking to buy on dips. MRNA is certainly going to participate. After Corona, there are 100 other diseases they could be working on. It’s not a COVID-19-only story, which is what some of the short sellers got wrong.

Q: How far does Gold (GLD) go down before it goes up?

A: Probably not much more; we have had a decent 10% correction. I was actually thinking about buying gold today, but I also hate leaning into a downtrend. So, any downtrends are temporary, we're looking at new highs in gold next year. This is a QE (quantitative easing) trade, not a risk-off trade like it used to be. So, the continuation of QE for years means that gold goes higher.

Q: When is it time to trade bonds (TLT) again?

A: Bonds just had their narrowest trading range in years in the last month. We only want to play on the short side; it broke down last week so we don't want to do anything here.

Q: Is a 1% drop in Advanced Micro Devices (AMD) a dip?

A: No, a 10% drop in AMD is a dip. Buying a 1% drop is a chase, which is an invitation to a lot of pain.

Q: Have SPACs (Special Purpose Acquisition Corporation) replaced IPOs?

A: I think SPACs are one of the greatest scams of all time. Everybody will get ripped off after paying enormous fees, and once these things go illiquid, no one will be able to get out, so I would not chase the SPAC game. They are only created to dodge the investor protections in the IPO process, I've seen too many of these fads happen over the last 50 years. They always end in tears.

Q: I think there will be another surprise Trump win similar to 2016. How would the market react to a Trump win?

A: It would crash because the market has built in a Biden win and chased up Biden sectors. So, if that doesn’t happen, the market has to give up all those gains and reorient itself. Trump had a 2-3-point polling deficit last time, and now he has to overcome a 17-point deficit or whatever the number is depending on the poll you look at. So, I don’t think so. Remember, Trump only won the election by 78,000 votes in three states. The 220,000 who have died from the pandemic are definitely NOT voting for Trump, nor are their 10X family members. That’s 2.2 million votes lost. Remember, the Corona death rate in red states is far higher than in blue states.

Q: Do you think a Bollinger Band squeeze is forming in Tesla right now?

A: Yes, even though this stock has had a prolific run, it looks like it wants to go higher. I wouldn’t go short.

Q: What about over issuance of US debt?

A: Any concerns about over issuance of debt won’t hit for a while because the Fed is going to keep the short-term rates at zero, which will anchor everything else at low levels. The initial heat will be felt in the ten- and 30-year bonds where you should be permanently short.

Q: Reminder that 4 years ago, you said a Trump win would crash the market.

A: Yes, I did say that, and it did crash the market—it dropped 1,000 points overnight and made it all back the next morning. I spent that entire night rebuilding portfolios which then had a massive run, so I remember that very well. That is the only election I was wrong on in 50 years. So, the lesson is don’t bet against the guy who's only wrong once in 50 years and count on him being wrong again. There are hundreds of data points now which show that Trump has no chance of winning and he’s acting in a way that backs that up.

Q: Is there a second COVID wave priced in yet?

A: No, the way these things work is scientists predict waves, traders say no it will never happen, then it happens and the traders puke out. And if that happens, we will know that is the buying opportunity of the century because that is exactly what we got on the last puke out in March. And yes, I was wrong; I said the stocks would double in two years and instead they doubled in three months.

Q: Do you think a real estate bubble is forming?

A: Yes, but it may not pop for another 10 years because we have 85 million millennials trying to buy housing right now, with interest rates near zero. I just refinanced my home at 2.75%. And only 65 million Gen Xers have homes to sell them, which is being expressed in higher home prices. That’s why I love the homebuilders (ITB).

Q: What about ProShares Ultra Short S&P 500 2X bear ETF (SDS)?

A: I would bail on that because the long-term trend is still up. Dow 120,000 here we come! You only want to use the (SDS) on short term dips, and then come out at the bottom.

Good Luck and Stay Healthy

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

October 9, 2020

Fiat Lux

Featured Trade:

(THE NEW AI BOOK THAT INVESTORS ARE SCRAMBLING FOR),

(GOOG), (FB), (AMZN), MSFT), (BABA), (BIDU),

(TENCENT), (TSLA), (NVDA), (AMD), (MU), (LRCX)

Global Market Comments

October 2, 2020

Fiat Lux

Featured Trade:

(SEPTEMBER 30 BIWEEKLY STRATEGY WEBINAR Q&A),

(NVDA), (AMD), (JPM), (DIS), (GM), (TSLA), (NKLA),

(TLT), (NFLX), (PLTR), (VIX), (PHM), (LEN), (KBH), (FXA), (GLD)