Mad Hedge Biotech and Healthcare Letter

August 1, 2024

Fiat Lux

Featured Trade:

(THE PLAYBOOK FOR A BIOTECH TRIPLE CROWN)

(ABBV), (TEVA), (PFE), (AMGN), (AZN), (BGNE), (LLY), (CERE)

Mad Hedge Biotech and Healthcare Letter

August 1, 2024

Fiat Lux

Featured Trade:

(THE PLAYBOOK FOR A BIOTECH TRIPLE CROWN)

(ABBV), (TEVA), (PFE), (AMGN), (AZN), (BGNE), (LLY), (CERE)

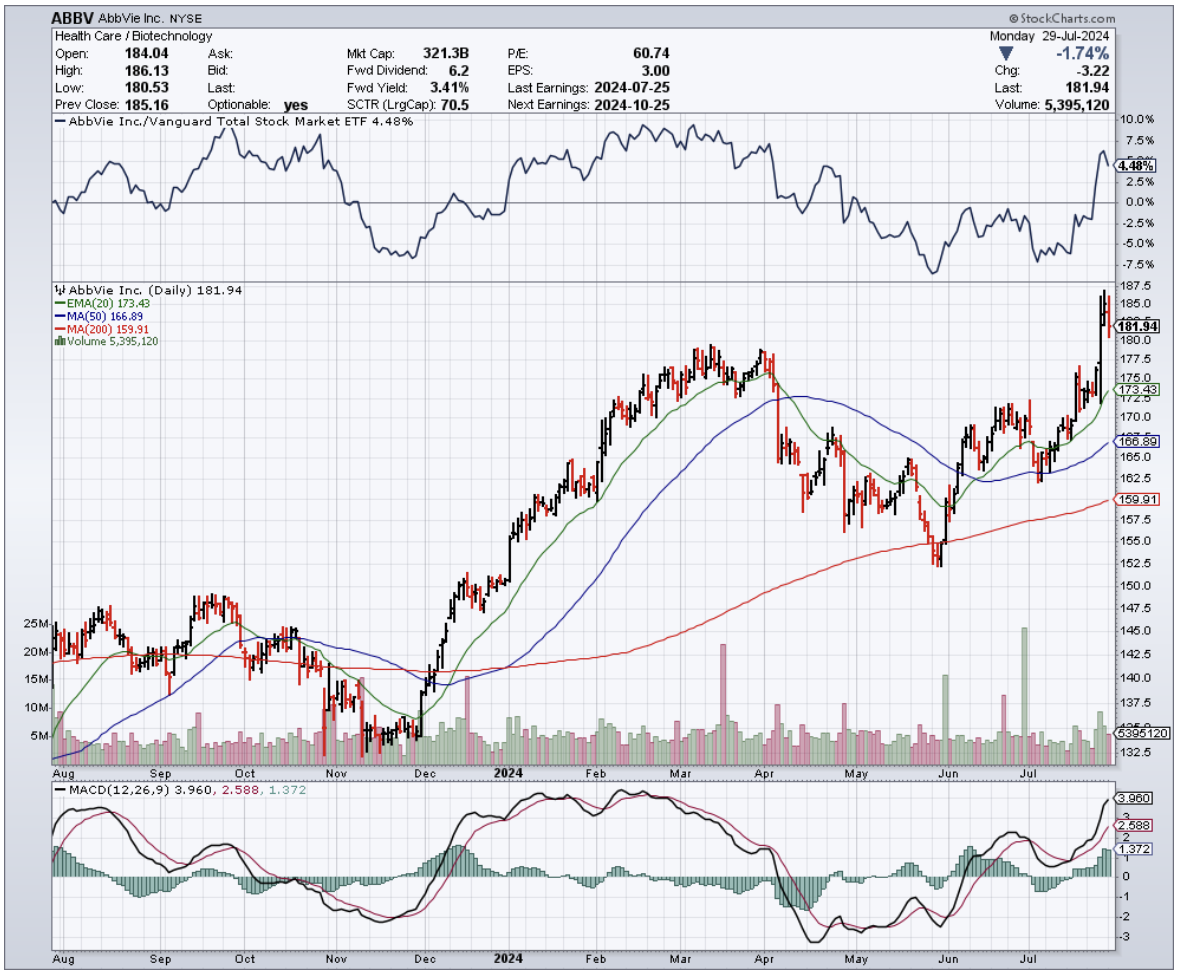

AbbVie (ABBV): A biotech stock that's been on my radar longer than most. If I could travel back to my UCLA biochem days, I'd tell young John to ditch the petri dishes and buy shares in this pharma giant. Why?

Because AbbVie isn't just another pharma play – it's a masterclass in diversification, innovation, and market-beating performance.

This is the stock that could turn a bright-eyed student into a savvy investor faster than you can say "immunology franchise."

In fact, if you've been paying attention to the market, you might have noticed that AbbVie's stock has been outperforming the broader U.S. market since mid-April, and for good reason.

This is a company that's been running at full throttle, posting some seriously impressive numbers in Q2 2024. We're talking $14.46 billion in revenue, a whopping 17.5% increase from the previous quarter and beating consensus estimates by a cool $430 million.

Earnings per share may have fallen just short of analysts' expectations, but they still climbed by a respectable 34 cents to $2.65.

But here's the thing: AbbVie's success isn't just a flash in the pan. This is a company with a diversified portfolio that's driving growth across multiple fronts.

I'm talking about their immunology, oncology, and neuroscience franchises, which together account for a staggering 75% of the company's total revenue.

Let's start with immunology. Now, I know what you're thinking - isn't that just Humira, AbbVie's blockbuster drug for Crohn's disease and ulcerative colitis? Well, yes and no.

While Humira has been facing some generic competition from the likes of Teva Pharmaceutical (TEVA), Pfizer (PFE), and Amgen (AMGN), resulting in a 30% year-over-year decline in global sales, AbbVie's got a couple of other tricks up its sleeve.

Enter Skyrizi and Rinvoq, two immunology drugs that are picking up the slack in a big way. Sales of these bad boys climbed 45% and 56%, respectively, in Q2 2024.

Skyrizi, in particular, has been an absolute beast, raking in $2.73 billion and growing 44.8% year-over-year. And with the FDA giving it the green light for moderate-to-severe ulcerative colitis in June 2024, the sky's the limit for this game-changer.

But AbbVie's not content to rest on its laurels. They're pushing the envelope with Rinvoq, a JAK inhibitor that's been approved for a wide range of indications and is showing some serious promise.

In Q2 2024, Rinvoq brought in $1.43 billion, a 30.8% quarter-over-quarter increase, thanks to strong demand in the U.S., excellent clinical trial results, and FDA approval for treating children with psoriatic arthritis and juvenile idiopathic arthritis.

And let's not forget about giant cell arteritis, a condition that AbbVie's been targeting with Rinvoq.

Recent trials have shown some impressive results, with 46% of adult patients taking Rinvoq 15 mg experiencing sustained remission, compared to just 29% of those on placebo.

No wonder AbbVie's been submitting applications left and right to get this drug approved for even more indications.

But it's not just immunology where AbbVie's making waves. Their oncology portfolio, bolstered by the acquisition of ImmunoGen in mid-February 2024, is also delivering the goods.

Sure, demand for Imbruvica may be declining due to newer BTK inhibitors from AstraZeneca (AZN), BeiGene (BGNE), and Eli Lilly (LLY), but Elahere, an antibody-drug conjugate for ovarian cancer, is quickly becoming a rising star.

In Q2 2024, Elahere sales jumped 65.4% quarter-over-quarter to $128 million, driven by increased marketing, growing awareness among physicians, and promising data from clinical trials.

Finally, let's not overlook AbbVie's neuroscience franchise, which generated a cool $2.16 billion in Q2 2024, a 14.7% year-over-year increase.

Headlining this portfolio are Qulipta and Ubrelvy for migraine treatment, and Vraylar for a range of psychiatric conditions.

Qulipta, specifically, has been a standout, with sales surging 56.3% year-over-year to $150 million, thanks to its convenient oral administration and long-term efficacy data.

Looking ahead, AbbVie's got even more irons in the fire. Their $8.7 billion acquisition of Cerevel Therapeutics (CERE) is set to close soon, bringing promising neuroscience candidates like emraclidine for schizophrenia and davapidon for Parkinson's into the fold.

With all these positive developments, it's no wonder AbbVie's feeling confident enough to raise its full-year adjusted EPS guidance to $10.71-$10.91, up from the previous range of $10.61-$10.81. Talk about a biochemistry experiment gone right!

So, there you have it. AbbVie: a healthcare powerhouse that's firing on all cylinders and poised for even greater success in the years to come. If only I could've shown this to my younger self back in those UCLA labs – he might've traded his test tubes for trading terminals a lot sooner.

Now, if you're ready to take a ride on this rocket ship, I suggest you buckle up and hang on tight. Because let me tell you, dissecting AbbVie's financial DNA has been more thrilling than any fracking adventure or hedge fund rodeo I've ever been on.

And if there's one thing I've learned in my years hopscotching from biochem labs to Wall Street, it's that the view from the top of a well-diversified, innovative pharma giant is always worth the climb. I suggest you buy the dip.

Mad Hedge Biotech and Healthcare Letter

June 20, 2024

Fiat Lux

Featured Trade:

(VAX TO THE FUTURE)

(AMGN), (RHHBY), (BNTX), (MRNA), (GNCA), (IOVA)

Let's have a heart-to-heart, you and me – about cancer, jabbers, and snake oil. If you think vaccines have been around for a while, you're on the money, my friend.

Over centuries, they've done a bang-up job wrestling down deadly infectious diseases and picking our collective life expectancy off the floor.

But what if I told you there's a different kind of magic we're still waiting for in the world of vaccines?

God's truth, I kid you not, science has been hammering away at this for years: creating vaccines to kick cancer square in the posterior. Yet, like an ardent investor waiting for the grand payoff, we've seen more flops than a fish outta water.

You can count on your one hand the number of cancer vaccines approved by the FDA since that first green-lit in 1990.

Let's not stammer about the bush, it's three – Provenge by Dendreon Pharmaceuticals, Imlygic by Amgen (AMGN), and Tecentriq by Roche (RHHBY).

Meanwhile, our old reliables – chemo, radiation, and the surgeon's knife – have, like battle-weary soldiers, been holding the fort for decades. But even they face formidable foes: nasty side effects, a bill that'll make a Rockefeller blanch and a diminishing punch against advanced cancer.

And the stats tell a story, but it ain't a happy one. Barely 59% of cancer patients treated with standard chemo make it through the five-year mark.

Until now.

Looking back, it's clear we've been a few beans short of a chili in our understanding of how the immune system and tumors get along — or rather, don't.

Now we know these devious cancers have been hoodwinking us with a starter kit of escape tools, literally tricking the immune system into playing “hide and seek.”

That’s where the likes of BioNTech (BNTX), Moderna (MRNA), Genocea (GNCA), and Iovance (IOVA) come in. To date, there are over 350 clinical trials focused on this field.

And if these new kids on the block deliver, we'll be singing hallelujahs with 83% five-year survival odds instead of the grim 59% chemo gives us.

As for those already in late-stage battles, where chemo only offers a bleak 4% five-year survival, immunotherapy could boost that to 23%.

So, what's the game-changer? Immune-modulating cancer vaccines.

Unlike traditional treatments that attack cancer cells directly, these vaccines train your immune system to recognize and destroy cancer cells like a well-trained bouncer booting out unruly party crashers.

Contrasted to the old brute force methods like chemo, and trust me, I’ve had some friends go through that ordeal, these vaccines are more like a sniper - taking precise aim only at cancer cells.

Plus, side effects? Minimal, my friends. But the cherry on top? These vaccines could potentially be your long-term bodyguards against cancer.

Now, I'm sure you love crunching numbers as much as I do, so here's some food for thought - the global cancer vaccine market was worth a cool $4.06 billion in 2019 and is projected to triple to $12.85 billion by 2027.

I mean, come on, that's a compound annual growth rate of 17.4%. It’s like watching your favorite sports team go on a championship run, season after season.

And the broader cancer immunotherapy market, sitting pretty at $75 billion in 2022, is on track to hit $120 billion by 2030, boasting a 14% CAGR.

These are not just empty promises either. We're seeing real progress - BioNTech and Moderna are developing personalized cancer vaccines that target unique tumor antigens.

Then there’s Genocea and Iovance, busy rolling out “off-the-shelf” cancer vaccines like fresh donuts off a conveyor belt.

This is a critical development, as around 70% of cancer patients develop resistance to chemotherapy.

These new immunotherapy contenders, with an overall survival rate of 50% compared to just 22% for those resistant to chemo, with every single patient potentially scoring against the dreaded C, and not fretting about chemoresistance. Talk about a fighting chance.

Overall, I think the cancer vaccine field is the Wild West of biotech – exciting, unpredictable, and potentially very rewarding. With companies pouring money into R&D, fueled by rising cancer rates and expedited FDA approvals, the race is on.

Immune-modulating cancer vaccines might just be the sheriff that this Wild West of cancer treatment needs, flipping the script on what used to be a death sentence into something we can manage.

Now, I'm not saying you should throw all your eggs in one basket, but keep a close eye on those mavericks like BioNTech, Moderna, Genocea, and Iovance. They could be the dark horses in this race.

Add them to your watchlist, and when the market hiccups and those share prices dip, that could be your chance to get a piece of the action.

Mad Hedge Biotech and Healthcare Letter

June 13, 2024

Fiat Lux

Featured Trade:

(THE TORTOISE IN THE BIOTECH RACE THAT’S ABOUT TO CROSS THE FINISH LINE)

(AMGN), (LLY), (NVO), (IMVT), (ARGX)

You know how every golfer dreams of donning the green jacket at the Masters, every chess player longs for the title of Grandmaster, and every football player fantasizes about hoisting the Lombardi Trophy?

Well, healthcare and biotech companies have their own version of the ultimate dream: launching a product that's as successful as the latest weight loss drugs from Eli Lilly (LLY) and Novo Nordisk (NVO).

These two pharma heavyweights have been on an absolute tear, with their shares skyrocketing 611% and 471% respectively over the past five years. It's the kind of rally that'll make your head spin and your wallet sing.

And guess what? The good news just keeps on coming. Analysts have cranked up their forecast for the obesity market. They're now predicting it'll hit a jaw-dropping $130 billion by 2030, up from their previous estimate of $100 billion.

That's an extra $30 billion. I don't know about you, but I call that a pretty sweet cherry on top.

Thanks to this obesity drug frenzy, Lilly has become the world's biggest healthcare company, and Novo Nordisk is now the most valuable company in Europe. It's like watching a couple of underdogs become the kings of the castle overnight.

Now, don't get me wrong, I love a good growth story as much as the next guy, and I wouldn't bet against Lilly or Novo Nordisk. But you know what I like even more? Biotech companies that are flying under the radar. The ones that are quietly innovating and positioning themselves for big things down the road.

That's where Amgen (AMGN) comes in.

I've been singing this company's praises in almost every piece I write, and for good reason. Amgen is one of the most innovative healthcare companies out there, with a massive product portfolio, a robust pipeline, and a balance sheet that's healthier than a triathlete on a kale smoothie diet.

Let me break it down for you. Established biotech companies with strong product portfolios are like fortresses in the business world.

They've got wide moats that are harder to cross than the Strait of Gibraltar. Why? Because bringing a new drug to market costs an arm and a leg.

We're talking anywhere from $314 million to $2.8 billion, depending on who you ask. That's not exactly chump change.

But Amgen? They've got it all figured out. Their portfolio spans a variety of therapeutic areas, including general medicine, oncology, inflammation, and rare diseases.

And in the first quarter of this year, these products helped Amgen rake in a whopping $7.4 billion in revenue, a 22% increase from the same period last year.

Key drugs like Repatha, Evenity, Blincyto, and Tezpire are leading the charge, with growth rates that'll make your head spin.

Repatha alone saw record sales of $517 million, thanks to a 44% increase in volume. And get this: expanded coverage and the removal of prior authorization requirements made the drug more accessible to patients.

It's like Amgen waved a magic wand and made all the red tape disappear.

Still, Amgen isn't just content with dominating the US market. They're taking their show on the road and expanding their international footprint.

Evenity, for example, has become the segment leader in Japan, capturing a staggering 46% of the bone builder market. And Uplinza, Amgen's fastest-growing biologic for a rare neurological disorder called neuromyelitis optica spectrum disorder (NMOSD), has been launched in multiple markets, including Canada.

Speaking of Uplinza, this little powerhouse came to Amgen via their $27.8 billion acquisition of Horizon last year. And let me tell you, it's paying off in spades.

In the first quarter of 2023, sales of Uplinza shot up by roughly 60%. And its smaller sibling, Tavneos, which targets a rare blood vessel disorder, saw a mind-boggling 122% growth.

The good news doesn't stop there. Amgen just released some hot-off-the-press Phase 3 data for Uplinza in another autoimmune condition, bringing it one step closer to yet another FDA approval.

This could put some serious pressure on competitors like Immunovant (IMVT) and argenx (ARGX), who have hit a few speed bumps lately.

Now, I know what you're thinking. "But John, what about the obesity market? Isn't that where the real action is?" Well, let me tell you, Amgen's got its fingers in that pie too.

They've got a unique obesity drug candidate called MariTide, which I talked about in detail last month, and the early clinical trial data suggests that it could blow Eli Lilly and Novo Nordisk's drugs out of the water.

But Amgen isn't just about cutting-edge drugs and international expansion. They're also rewarding their shareholders with cold, hard cash.

Last December, they hiked their dividend by 5.6%, and they're now paying out $2.25 per share every quarter.

That translates to a juicy 3% yield, and it's backed by a payout ratio that's lower than a limbo stick at a beach party.

Plus, Amgen's been raising its dividend like clockwork, with a five-year compound annual growth rate of 9.6% and 12 consecutive annual hikes. That's the kind of consistency that'll make any investor smile.

Overall, it’s clear that Amgen is a standout in the biotech world, plain and simple.

Besides, this company isn’t some Johnny-come-lately to the biotech game. They've been in this fight since the beginning, and their very name is proof of their founding principles. In fact, “Amgen” is a fancy-pants word for "applied molecular genetics."

That's right, when they picked that name back in 1980, they were already knee-deep in the groundbreaking science of genetic engineering, cooking up new therapies that would change the face of medicine as we know it.

So here’s my advice. When the chips are down and the stakes are high, you can never go wrong to bet on the OG of applied molecular genetics. Buy the dip on Amgen.

Mad Hedge Biotech and Healthcare Letter

May 21, 2024

Fiat Lux

Featured Trade:

(THE FAT’S IN THE FIRE)

(RHHBY), (LLY), (NVO), (AMGN), (VKTX), (PFE), (MRK), (SNY), (ABT)

Well, well, well, look who's decided to crash the obesity-drug party. Roche (RHHBY), the Swiss pharmaceutical giant, has just unveiled some pretty impressive early-stage results for its weight-loss drug, CT-388. And let me tell you, this could be the start of something big.

Now, I know what you're thinking: "Another weight-loss drug? Yawn." But trust me, this is no ordinary contender.

In a small trial, patients who received CT-388 saw an average placebo-adjusted weight loss of 18.8% after just 24 weeks. That's right, 18.8%.

While it's hard to compare trials, experts are saying these numbers might even give Eli Lilly's (LLY) Zepbound, the current king of the market, a run for its money.

Let's take a step back and look at the bigger picture. The obesity drug market has been on fire lately, with everyone going gaga over these miracle pills.

Lilly and Novo Nordisk (NVO) have been dominating the scene with their drugs, Zepbound and Wegovy, but that hasn't stopped a whole host of other companies from trying to get a piece of the pie.

Merck (MRK), Sanofi (SNY), Abbott Labs (ABT), and Eisai have all tried their hand at weight-loss drugs and ultimately thrown in the towel.

More recently, Pfizer's (PFE) daily oral pill, danuglipron, has faced hurdles due to side effects. Amgen's (AMGN) drug, MariTide, is in Phase 2 studies and showing promise. And let's not forget Viking Therapeutics' (VKTX) VK2735, which has earned the nickname "twincretin" for its dual targeting of GLP-1 and GIP receptors.

So, what makes Roche's CT-388 so special?

Well, for starters, it's a GLP-1/GIP receptor agonist, which is similar to Lilly's Zepbound. In the Phase 1 trial, all participants achieved more than 5% weight loss, with 85% losing more than 10%, 70% shedding more than 15%, and a whopping 45% dropping more than 20% of their body weight. That's some serious weight loss.

Of course, there were some side effects, mainly mild to moderate gastrointestinal issues, but hey, that's the price you pay for looking fabulous, right? Roche is also testing CT-388 in patients with Type 2 diabetes, so stay tuned for updates on that front.

Now, I know you're all dying to know how CT-388 stacks up against the competition.

Notably, the drug's data looks strong compared to earlier studies of Zepbound. In fact, CT-388's efficacy results appeared "numerically higher" than Zepbound's.

But let's not get ahead of ourselves. Lilly still has a multi-year lead on Roche, so CT-388 isn't an immediate threat. However, it does suggest that the future of this rapidly growing market is up for grabs.

Now, let's talk about Roche. It’s the world's seventh-largest pharma company by market cap, sitting at around $205 billion. They pulled in $65 billion in revenue in 2023, second only to Johnson & Johnson (JNJ).

But here's the kicker—they've been struggling with growth, and their share price has taken a hit, down more than 25% over the past three years.

Contrast that with Eli Lilly and Novo Nordisk. Lilly's share price shot up 290% in three years, and Novo's climbed 226%.

Even though their revenues were less than half of Roche's in 2023, their market caps are sky-high. Why? Because of their blockbuster GLP-1 agonist drugs, Zepbound and Wegovy, which have shown jaw-dropping weight-loss results.

But could CT-388 be the underdog story Roche needs?

With the obesity market estimated to reach a staggering $100 billion by 2030, and over 1 billion people worldwide suffering from obesity, the potential is enormous.

Of course, there's still a long way to go for CT-388. Cross-trial comparisons can be tricky, and Roche's Phase 1 trial was much smaller than Lilly's pivotal study of Zepbound.

Plus, we don't have all the juicy details on patient characteristics, dose titration, and long-term weight loss just yet.

But here's the thing: Roche has scale and infrastructure on its side. It could potentially outmuscle smaller players like Viking and Boehringer Ingelheim.

And if CT-388 can match or even surpass the performance of current and future GLP-1 agonists? Well, let's just say those peak revenue forecasts might be in for a surprise.

So, is Roche the dark horse you should bet on in the obesity-drug race? If you're looking to get in on the action without paying the premium commanded by Lilly and Novo, or taking on the higher risk of smaller players, Roche might just be the ticket.

With promising mid-single-digit revenue growth on the horizon and a strong position in other areas like oncology and autoimmune disorders, Roche could be a smart play for anyone keen on the obesity drug market.

As for me? Well, you know I love an underdog story. And CT-388 might just be the Cinderella story of the year. I suggest you buy the dip.

Mad Hedge Biotech and Healthcare Letter

May 7, 2024

Fiat Lux

Featured Trade:

(PACKING A HEAVIER PUNCH)

(AMGN), (NVO), (LLY), (REGN)

Amgen (AMGN) is having a moment. Early results for their injectable drug MariTide sound pretty darn promising.

But it’s not all roses and sunshine at Amgen. The company also dropped the curtain on AMG786, an experimental oral weight-loss pill that just wasn't cutting it.

It’s tough in the pharmaceutical arena, especially since this whole weight-loss drug market is a gold rush right now. Eli Lilly (LLY) and Novo Nordisk (NVO) are cleaning up, and even Pfizer (PFE), despite their hiccup, isn't going to roll over that quickly.

Now, back to MariTide. Calling it a "multi-blockbuster" sounds flashy, but investors want to see if it can crack the hold those big two already have. Amgen's got a decent track record though, so I wouldn't write them off just yet.

The early scoop on MariTide is pretty tantalizing. The last round of Phase 2 trials showed that three monthly shots could significantly trim the waistline, with the heftier doses keeping the pounds off for up to four months post-treatment.

Actually, MariTide’s core strength is that it’s just once-a-month jab — an easier regimen compared to the weekly routine required by current front-runners like semaglutide and tirzepatide.

Speaking of the competition, Novo Nordisk’s semaglutide and Eli Lilly’s tirzepatide have been seeing users pack the pounds back on pretty quickly after stopping treatment.

That’s not ideal, and it’s exactly the kind of opening Amgen is looking to capitalize on with MariTide.

Now, let’s broaden our scope. It's a bit of a misnomer to just call it an “obesity pipeline” because, let me tell you, this technology is dipping its toes into much more than just shedding pounds.

Those GLP-1 agonists like semaglutide and the double-duty “double G” agonists like tirzepatide? They’re not just one-trick ponies.

Aside from battling the bulge, they’re making waves in treating diabetes, slicing through cardiovascular risks, and even exploring new frontiers like osteoarthritis and sleep apnea.

Heck, they’re even peeking into Alzheimer’s prevention — Novo Nordisk is already revving up for a phase 3 trial.

Despite these lucrative offshoots though, obesity remains the arena’s juggernaut.

Novo Nordisk’s latest data, as bleak as it might seem for global health, paints a picture of a market vast enough to entice anyone. Think about it—out of 813 million people wrestling with obesity, only one million are currently on these incretin drugs.

And with projections pointing to numbers ballooning to 1.2 billion by 2030, well, the potential market is jaw-dropping.

If Amgen’s MariTide hits the mark, we could be talking about a whopping $20 billion in annual sales from just this one contender in about 7-8 years, spanning obesity and a few neighboring conditions.

That’s even if they face a dogfight over pricing and if the average price per patient hangs below what the big guns like Novo Nordisk and Eli Lilly are currently pulling.

Now, think about this — current estimates peg Amgen’s growth from $33 billion this year to a modest $35.1 billion by 2033. My take? That’s wildly conservative.

If you ask me, Amgen's obesity pipeline alone, even with just modest success, could blast those numbers out of the water.

But let's not kid ourselves – MariTide alone won't make Amgen king of the obesity market. To truly capitalize on the segment’s potential, Amgen might need to consider teaming up with those emerging stars working on preserving lean body mass, or even big players like Regeneron (REGN).

They could take a couple of routes here. One slick move could be scooping up some smaller biotech firms or cozying up to bigger fish through partnerships or in-licensing deals to beef up their treatment options.

Alternatively, Amgen could play it cool and simply pair MariTide with their own upcoming products once they hit the market. Sure, this might keep things simple, but it kind of feels like leaving money on the table, isn’t it?

Admittedly, it’s still early days when it comes to these weight loss treatments. One thing's for sure: the next few years will be a wild ride for obesity drugs. After all, it’s clear that the GLP-1 craze is doing for pharma what AI hype is doing for tech stocks. It’s like a rising tide lifting all boats.

Looking ahead, the big winners in the next 18 months are looking to be Novo Nordisk and Eli Lilly. These guys are leading the pack, while others might just not make it to the finish line, ending up as flops in the stock market drama.

Yet, through all this, Amgen stands out as a dark horse.

Even if the obesity pipeline doesn't turn out to be their golden ticket, Amgen's strategic positioning could still deliver solid long-term value.

But, and here’s the kicker, if MariTide and its potential combo treatments hit their stride as hoped, Amgen could sprint ahead in this fast-paced market race — not just in obesity but in those juicy, adjacent niches too. This could spark some serious value creation that current forecasts haven't even begun to factor in.

So, while the market’s getting its gears grinding, Amgen might just surprise us all. I say keep this stock on your watchlist.