Mad Hedge Biotech and Healthcare Letter

October 3, 2023

Fiat Lux

Featured Trade:

(REDEFINING RESILIENCE)

(VRTX), (ABBV), (AMGN), (JNJ)

Mad Hedge Biotech and Healthcare Letter

October 3, 2023

Fiat Lux

Featured Trade:

(REDEFINING RESILIENCE)

(VRTX), (ABBV), (AMGN), (JNJ)

It’s not surprising that a number of investors might be hesitant to purchase stocks this month. A few might remember that a number of the most significant stock market downturns in history took place in October. Numerous stocks continue to be high-priced despite the stock market shedding a considerable portion of its earlier momentum from this year.

However, October has often proven to be a favorable month for the stock market — if you know how to choose. Moreover, while a multitude of stocks carry a high price tag, there are those that do not.

Now, imagine a pharmaceutical giant, a singular entity reigning supreme in a market valued in the billions, poised to unveil three revolutionary products by 2025, each potentially generating sales eclipsing $1 billion. Picture this company at the forefront, pioneering a cure for type 1 diabetes (T1D).

The fascinating part? This isn’t a fragment of imagination—it’s the reality of Vertex Pharmaceuticals (VRTX).

With its towering presence in the biotech sector, Vertex has a market cap surpassing $90 billion, establishing itself as the largest entity among U.S.-headquartered firms. Unlike its contemporaries—AbbVie (ABBV), Amgen (AMGN), and Johnson & Johnson (JNJ)—Vertex doesn’t distribute dividends.

Still, it remains one of the most consistent companies thanks to its remarkable trajectory starting from its inception in 1989. Since the advent of the SPDR S&P Biotech ETF (XBI) in 2006, Vertex has soared, achieving over 900% return, overshadowing the ETF’s 380% return.

The journey of Vertex is not just a tale of numbers and percentages; it’s a narrative of resilience and innovation. The company distinguishes itself with its innovative approach to addressing serious diseases, particularly focusing on cystic fibrosis (CF), and its continuous expansion in the CF treatment market.

As expected, the question of whether Vertex is a one-dimensional entity, solely reliant on CF therapies arises. Far from it.

CF isn't anticipated to be the sole catalyst for Vertex's expansion for much longer. The firm, alongside its partner CRISPR Therapeutics (CRSP), is aspiring to secure approval from U.S. regulatory bodies for exa-cel to treat uncommon hematological conditions such as sickle cell anemia and transfusion-reliant beta-thalassemia in the upcoming months. Additionally, the company envisions an imminent market introduction for VX-548, a potent, non-opioid pain medication.

Looking ahead, the future seems even more promising for this major biotech entity. Vertex is conducting a crucial clinical trial on inaxaplin, focusing on APOL1-mediated renal disease, affecting a broader patient demographic compared to CF.

Meanwhile, the financial prowess of Vertex is another facet of its diverse identity. The company has been a consistent beacon of positive free cash flow since 2016, and its financial robustness was highlighted by a 14% revenue growth in the second quarter, driven by robust international sales.

The company’s strategic investments in R&D and commercial capabilities are pivotal to leveraging the multibillion-dollar market opportunities looming on the horizon. These investments are not mere allocations of resources; they are the building blocks of Vertex’s future, the seeds sown today to reap innovations tomorrow.

An excellent example of this is Vertex’s ambitious stride into the type 1 diabetes market, marked by its acquisition of ViaCyte in a $315 million deal. Ultimately, the goal is to deliver innovative stem cell-derived cell replacement therapies as a functional cure for type 1 diabetes.

While the diabetes products are still navigating through phase 2, the anticipation is palpable regarding their role in fueling Vertex’s future growth. The company’s resilience against elevated rates and its propensity to bounce back make it a fascinating stock to consider during market corrections. It’s not just about the numbers on a balance sheet or the ticks on a stock chart; it’s about the relentless pursuit of innovation, and the unwavering commitment to making a difference in the lives of patients around the globe.

So, do these make Vertex the unstoppable stock poised to rule the next two decades? The signs are pointing to a resounding yes.

Global Market Comments

September 5, 2023

Fiat Lux

Featured Trades:

(The Mad Hedge September Traders & Investors Summit is ON!)

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE NEW GOLDEN AGE IS ABOUT TO BEGIN!)

(TLT), (TSLA), (AAPL), (AMGN)

CLICK HERE to download today's position sheet.

If any of you ever had concerns about the long-term future of the United States of America you can put them to rest.

Escaping from Silicon Valley to the cooling majestic heights of the High Sierras ahead of the Labor Day weekend, Google Maps directed to a series of back roads to avoid the traffic Armageddon taking place on the freeways.

Known as the “Delta Highway,” I had to cross three ancient rickety 100-year-old bridges just to get to Stockton.

And you know what I saw?

The proverbial “majestic waves of grain.”

I passed square mile after square mile of ripening corn “as high as an elephant’s eye”. Next came square miles of fields in fallow planted with clover capturing nitrogen. That was followed by miles of the darkest and richest earth you ever saw ready for new planting.

The fields were intermittently spaced with You-Pick cherry and peach orchards crowded with Asian customers. To them, the fact you can just drive out into the countryside and pick fresh fruit for $5 a bucket was utterly amazing.

One of the questions I get asked most often from the top down is whether China will invade Taiwan. My answer is always the same: Not a chance. They’ll never do more than bluff as they have done for the last 70 years.

That is because modern China exists only because of America’s good graces. If they invaded, we would cut of their food supply the next day. There are no alternative food supplies for 1.2 billion people anywhere in the world.

Over time, they might develop some supplies in South America or Africa but by the time those had any meaningful impact, half the population would starve to death. Everything in agriculture happens slowly.

I’ve been in China during famines and let me tell you it’s no fun. There is no substitute for food, not at any price.

We know this, the Chinese know this, everybody knows this.

The power of nations used to be measured in food production, bushels of wheat in the West and baskets of rice in Asia. To some extent it still is. Who are the largest producers of food in the world? China, India, the US, and Brazil. But the first two consume their entire output and then some, while the last two are the world’s largest food exporters by miles.

Of course, China will take Taiwan if we give it to them. That’s why it’s useful to keep our Seventh Fleet in the neighborhood just to remind them that we’re still watching. It’s also not a bad idea to bring some of our semiconductor production home as well just as a hedge, a risk control measure.

So you can stop asking me if China will invade Taiwan.

In the meantime, regarding your personal investment strategy, there is only one number you need to know: $5.6 trillion. That is the amount of cash, cash equivalents, money, market funds, and 90-day T-bills sitting on the sidelines waiting to go into risk assets.

And by risk assets, I mean stocks, bonds, commodities, precious metals, energy, and real estate.

Incredible as it may seem, the majority of investors still don’t believe that the greatest bull market of the ages started on October 15, 2022. They think we are in a bear market and are waiting for better buying opportunities much lower down.

Partly this is happening because they are being told by their political leaders that the US has the worst economy in the world. When they come to the harsh reality that the opposite is true, that the US has the best economy in the world by far, money will come pouring off the sidelines and take stocks up at least until 2030.

This will take place no later than October by my reckoning.

That’s when a New Golden Age kicks off that will last a decade or more, driven by AI, quantum computers, graphene, carbon fiber, free energy, superconductivity, solid state batteries, and 100 other hyper-accelerating technologies.

Make concentration of the wealth at the top work for you and get involved in the market. Become one of the 1%. I’ve done it starting from a very low base. Keep those 90-day T-bills at your peril, no matter how attractive those 5.35% guaranteed yields may be.

Which leads us to a quandary.

Stocks never got cheap during the summer selloff, they just dropped from very expensive to expensive. The Mad Hedge AI Market Timing Index didn’t get lower than 45 compared to the usual low of 20, or even 3 (the pandemic low).

That means we are going to have to invest on the basis of stocks going from expensive to extremely expensive. It’s not the game we are used to playing. But stocks have done this before.

The (QQQ) traded at a price-earnings multiple of 100 times earnings at the Dotcom Bubble top in 2000 compared to only 30.79 times now and that was only with a fraction of the emerging technologies currently under development.

You can wait for The Mad Hedge AI Market Timing Index to get to 20, or even 3, but it might never happen.

I just thought you’d like to know.

So far in September, we are unchanged with a +0.00% return. My 2023 year-to-date performance is still at an eye-popping +60.80%. The S&P 500 (SPY) is up +17.10% so far in 2023. My trailing one-year return reached +92.45% versus +8.45% for the S&P 500.

That brings my 15-year total return to +657.99%. My average annualized return has fallen back to +48.15%, another new high, some 2.50 times the S&P 500 over the same period.

Some 41 of my 46 trades this year have been profitable.

Nonfarm Payroll Comes in Weak, at 187,000, in August. The Headline Unemployment rate posted at near a 50-year low at 3.8%.

It’s the third month in a row under 200,000. The U-6 “discouraged worker” rate popped from 6.7% to 7.1%. Strikes are becoming a factor. The news took the ten-year US Treasury bond yield (TLT) under 4.0% for the first time in months.

Weekly Jobless Claims Decline to 228,000 as the economy heats up. 235,000 was expected. Continuing Claims are at 1.9 million.

Jolts Disappoints, with new job openings coming in at only 8.83 million, a 2 ½ year low. The labor shortage is getting worse, suggesting that the headline Unemployment Rate could rise on Friday and that inflation will continue falling. The drop in openings reflected declines in professional and business services, health care, and government. Hold on to your hat!

Apple (AAPL) to Launch New iPhone 15 on September 15. The highlight of the event will be the iPhone 15 lineup, which will include two entry-level models and two high-end models. The lower-end devices, likely to be called the iPhone 15 and 15 Plus, will get some capabilities of last year’s Pro models — the A16 chip, Dynamic Island interface, and a 48-megapixel rear camera — but retain the current design.

Bank Earnings Forecasts Cut, by Wells Fargo’s Mike Mayo, a noted bank analyst. New regulations are raising costs across the board. Capital requirements are rising. You can count on share buybacks to be paid back. More business is being pushed outside the banking system. Stand back from bank shares until we learn the new paradigm.

India Attempts to Win the Next Tesla Factory (TSLA), buy offering to cut import duties. Elon Musk would certainly love the non-union labor costs there. The world’s third largest car market has only an EV penetration of 2% because of the high duties, which currently range from 60%-100%.

Hedge Fund Exposure to “Magnificent Seven” at All-Time High, says Goldman Sachs. It amounts to 20% of all hedge fund holdings. Megacap tech and AI still rule. It’s momentum on steroids.

Crypto Trading Volume Hits Four-Year Low. With the SEC cracking down on all intermediaries this asset class will eventually shrink down to “hot wallets” only. No helping is a hangover of massive fraud and theft. Avoid all crypto like the plague.

Case Shiller Rises 0.7% in June, launching the shares on its usual preannouncement uptrend. High mortgage interest rates seem to no longer be having an effect. Chicago, Cleveland, and New York again reported the highest year-over-year gains among the 20 cities in June at 4.2%, 4.1%, and 3.4%, respectively.

Bigfoot Sightings are Rising, in the form of Tesla Cybertruck whose widespread release in imminent. It will be one of the greatest automotive events in history, with several generational upgrades for the general Tesla platform in store. The waiting list is 2 million long, including myself. Buy (TSLA) on dips or sell short out-of-the-money puts.

Amgen Gets FTC Go Ahead on $27.8 billion Horizon Deal and holds on to monster August gains. (AMGN) is a long-term Mad Hedge Biotech & Health Care favorite. The Stock has popped an impressive 27% since June. You can’t keep a good stock down!

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, September 4, US markets are closed for Labor Day.

On Tuesday, September 5 at 7:00 AM EST, US Factory Orders are released.

On Wednesday, September 6 at 7:00 AM, the ISM Services PMI is published.

On Thursday, September 7 at 8:30 AM, the Weekly Jobless Claims are announced.

On Friday, September 8 at 12:00 PM, the Used Car Prices for August are published. At 2:00 PM, the Baker Hughes Rig Count is printed.

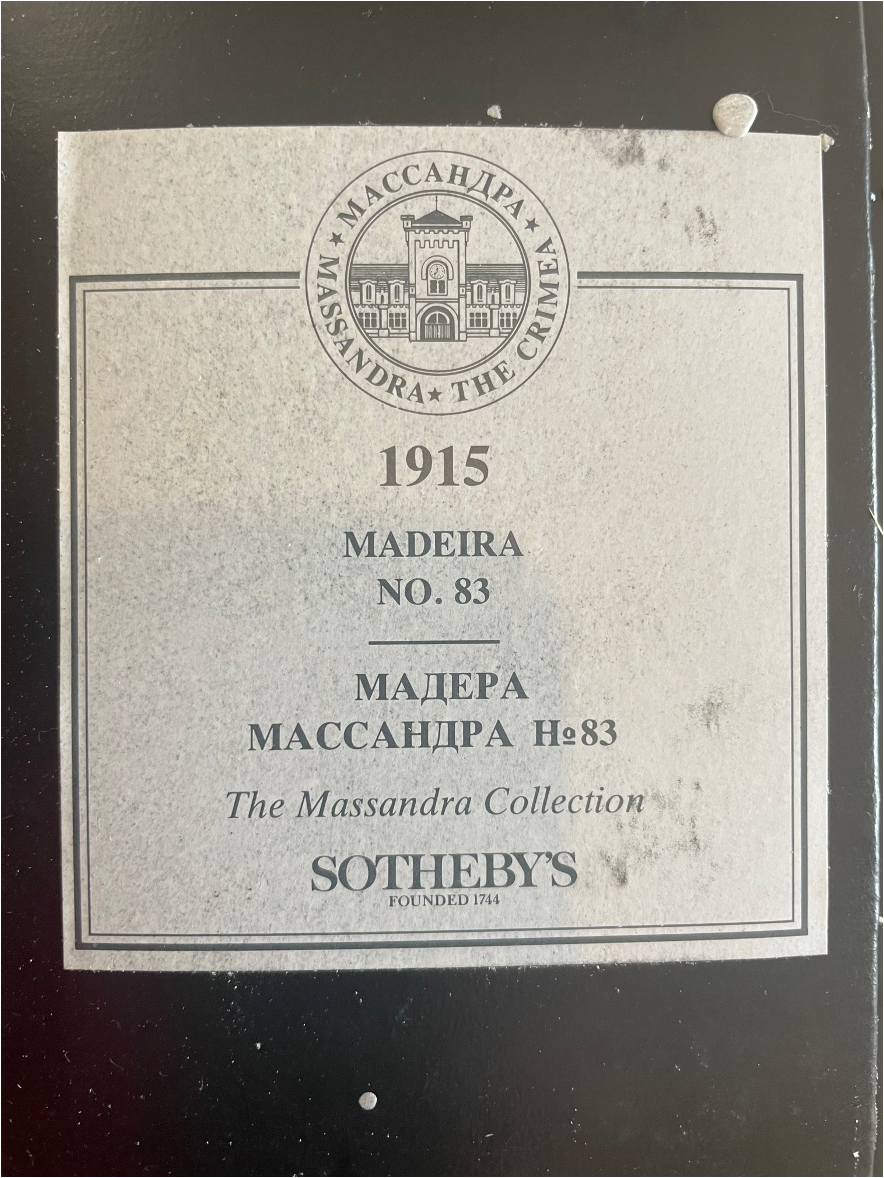

As for me, as a lifetime oenophile, or wine lover, I long searched for the Holy Grail of the perfect bottle. I finally found my quarry in 1989.

During the 19th century, Russia was still an emerging country that sought to import advanced European technology. So, they sent agents to the top wine-growing regions of the continent to bring back cuttings from the finest first-growth Bordeaux vineyards to create a domestic wine industry. They succeeded beyond all expectations building a major wine industry in Crimea on the Black Sea.

Then the Russian Revolution broke out in 1918.

Czar Nicholas II and his family were executed in Yekaterinburg, and eventually, the wine industry was taken over by the Soviet state. They kept it going because wine exports brought in valuable foreign exchange which the government could use to import expensive foreign equipment and industrialize the country.

Then the Germans invaded in 1941.

Not wanting the enemy to capture a 100-year stockpile of fine wine, the managers of the Massandra winery dug a 100-yard-deep cave, moved their bottles in, bricked up the entrance, and hid it with shrubs. Then everyone involved in hiding the wine was killed in the war.

Some 45 years later, looking to expand the facility some Massandra workers stumbled across the entrance to the cave. Inside, they found a million bottles dating back to the 1850s kept in perfect storage conditions. It was a sensation in the wine-collecting world.

To cash in they hired Sotheby’s in London to repackage and auction off the wine one case at a time. It was the auction event of the year. For years afterwards, you could buy glasses of 100-year-old ports and sherries from the Czar’s own private stock at your local neighborhood restaurant in London for $5, the deal of the century. The market was flooded.

I attended the auction at Sotheby’s packed Bond Street showroom. The superstars of the wine-collecting world were there with open checkbooks, including one of the Koch brothers from Texas. I sat there with my paddle number 138 but was outbid repeatedly and wondered if I would get anything. In the end, I managed to pick up three of the less popular cases, an 1894 Lividia port, a 1938 sherry, and a 1940 port for about $25 a bottle each.

For years, these were my special occasion wines. I opened one when I was appointed a director of Morgan Stanley. Others went to favored hedge fund clients at Christmas. My 50th, 60th, and 70th birthdays ate into the inventory. So did the birth of children numbers four and five. Several high school fundraisers saw bottles earn $1,000 each.

One of the 1894s met its end when I came home from the Gulf War in 1992. Hey, the last Czar didn’t drink it and look at what happened to him! Another one bit the dust when I sold my hedge fund at the absolute Dotcom Bubble market top in 2000. So did capturing 6,000 new subscribers for the Mad Hedge Fund Trader in 2010, leaving me with 2,000 checks to cash.

It turns out that the empties were quite nice too, 130-year-old hand-blown green glass, each one is a sculpture in its own right.

I am now reaching the end of the road and only have a half dozen bottles left. I could always sell them on eBay where they now fetch up to $6,000 per bottle.

But you know what? I’d rather have six more celebrations than take in a few grand.

Any suggestions?

My Massandra 1894 Lividia Port

Mad Hedge Biotech and Healthcare Letter

August 29, 2023

Fiat Lux

Featured Trade:

(WEIGHTY RETURNS)

(NVO), (LLY), (SNY), (AMGN), (PFE), (AZN)

These days, the narrative around transformative weight-loss drugs just got a little juicier. Here's the lowdown: Heart-failure patients are now giving a nod to Novo Nordisk’s (NVO) Wegovy. But, why?

The intel shows that the overweight community, grappling with heart woes, noticed a stamina uptick and weight drop when on Wegovy. The buzz was so compelling that it got its spotlight moment at the European Society of Cardiology Congress in Amsterdam. Plus, the New England Journal of Medicine gave it some ink.

Dive into the numbers, and you'll find that out of about 530 individuals with hearts not really pulling their weight (pun intended), the Wegovy brigade shed 13% of their body weight. That’s in stark contrast to the 3% that the placebo group managed.

More walking, less heart huffing-puffing - Wegovy users clocked in 17 times more steps on the treadmill and showcased fewer heart hiccups. Oh, and fewer side effects? Check.

Rewinding the tape, GLP-1 drugs initially stepped into the arena as the remedy for Type-2 diabetes. But then, surprise! Novo’s Ozempic and Eli Lilly’s (LLY) Mounjaro became the talk of the town. Not just because they were treating diabetes, but because those popping them shed an eye-catching 15% to 20% of their body weight. That's blockbuster material right there.

Eventually, Novo bagged the FDA's green light first for weight loss with Wegovy, and its demand skyrocketed so much so that medical maestros started prescribing Ozempic and Mounjaro to folks with weight woes. Now, all eyes are on the FDA's next move concerning Lilly’s weight-loss contender.

Now, here’s the kicker. This isn’t Wegovy’s first rodeo in the spotlight. Earlier this month, eyebrows were raised when it was revealed that these new kids on the block, known as GLP-1 agonists, might be the next superhero squad against a gamut of diseases.

Yet, GLP-1 might not just stop at obesity and heart diseases. It can also combat a spectrum of illnesses, including Alzheimer's. As expected, Novo and Lilly are doubling down on this potential, exploring these drugs' impact on liver and kidney diseases. As the benefits of GLP-1s unfold, insurers will probably be queuing up to offer coverage.

Let’s paint a clearer picture in terms of market potential.

Nearly 42% of U.S. adults grapple with obesity. The World Obesity Atlas dropped a bombshell—by 2035, over 4 billion global citizens might be tipping the scales, adding an astronomical $4 trillion in health costs.

The repercussions? Beyond the obvious heart diseases, strokes, and type 2 diabetes, they are also prone to mental health challenges, like depression and anxiety.

The economic ripples? Staggering. A drug that can be the silver bullet for such a widespread health epidemic could be the next Wall Street darling.

The next 10 years will likely see the GLP-1 agonists market touching an annual $86 billion. Yet, these figures might be leaning heavily on diabetes and off-label prescriptions.

With the World Health Organization cautioning about a billion obese and 2 billion overweight individuals by 2030, it's clear—this market is about to get a whole lot bigger.

With promises like these, it's no shocker that investors are tossing their coins into the ring. Both Novo and Lilly have seen their valuations triple, and Lilly's net worth now towers over its peers at a staggering $500 billion, crowning it the globe's pharmaceutical kingpin.

However, it’s wise to remember that it's one thing to climb the mountain and another to stay on the summit. Even in this early stage, competitors have started to emerge, including Amgen (AMGN), Sanofi (SNY), AstraZeneca (AZN), and Pfizer (PFE).

By 2025, the biopharma giants could potentially unveil their very own GLP-1-based wonder drugs for obesity, chipping away a quarter of Novo and Lilly's market dominance by 2032.

In the ever-evolving theater of biopharma, GLP-1 agonists, led by stalwarts like Wegovy, are emerging as the new front-runners. While the rewards seem tantalizingly vast, savvy investors know the pharmaceutical landscape is punctuated with highs and inevitable lows.

And here's a golden nugget: in the dynamic world of stock trading, every dip is an opportunity disguised as a setback. So, if you're seeking a stock market mantra for this burgeoning sector, remember to buy on the ebb, not the crest. It's in these valleys that fortunes are made, setting the stage for robust returns. Dive in wisely.

Mad Hedge Biotech and Healthcare Letter

August 1, 2023

Fiat Lux

Featured Trade:

(CHASING THE TRILLION-DOLLAR DREAM)

(LLY), (NVO), (AMGN), (PFE)

Mark my words. The healthcare sector is on the cusp of a seismic shift. By 2033, I expect to see the dawn of a trillion-dollar enterprise. Now, you might think I've lost my marbles, but hear me out.

The prime contender for this prestigious title? Eli Lilly (LLY).

Now, Lilly is comfortably lounging at a market cap of $425 billion, a massive figure, yes, but still less than half of our $1 trillion target. Lilly's stock would need to scale up by a staggering 135% to breach the trillion-dollar threshold.

Daunting, right?

But if you break it down to an annual growth rate over a 10-year span, we're looking at a relatively modest compound rate of around 8.9%. With Lilly's recent track record and brimming product pipeline, this growth trajectory doesn't seem so far-fetched.

A closer look at Lilly's pharmaceutical lineup reveals a host of innovative treatments. Lilly's recent contributions to diabetes care - Mounjaro, Jardiance, and Trulicity - represent significant strides.

Adding to the fray are Taltz, a cutting-edge psoriasis solution, and Verzenio, a life-saving breast cancer drug. A peek into Lilly's late-stage pipeline reveals potential blockbusters in the making, like lebrikizumab for atopic dermatitis, mirikizumab for immunology, and donanemab for the relentless battle against Alzheimer's.

Then, there's the $1.9 billion acquisition of Versanis Bio, positioning Lilly at the precipice of the weight-loss market.

Lilly stands out with its robust line-up in the race for weight loss solutions. Mounjaro, initially a diabetes drug, has demonstrated potential as a weight-loss aid in clinical trials, with participants on the highest dosage shedding up to 22.5% of their body weight over 72 weeks.

Yet, the sector is intensely competitive, with giants such as Novo Nordisk (NVO), Amgen (AMGN), and Pfizer (PFE) on the battlefield. While Lilly's recent acquisitions present strong prospects, forecasting revenue growth over the next decade remains an intricate puzzle.

Notably, weight-loss solutions form a crucial part of Lilly's growth plan and could contribute more than 60% of the company's annual revenue by the mid-2030s.

Meanwhile, Lilly is developing potential breakthroughs in Alzheimer's treatment, with donanemab showing promise in clinical trials. This treatment has a mechanism that targets amyloid plaque, often found in the brains of Alzheimer's patients.

If approved, sales could reach a projected $3.9 billion by 2027.

Despite these promising avenues, caution is warranted. Lilly's stock is trading at 51.75 times its forward-looking earnings estimates. While the prospects for Alzheimer's and weight management treatments show promise, their success is far from guaranteed.

Historically successful drugs like Humalog and Alimta have seen their sales decline by 25% and 83%, respectively, as they lose exclusivity and face competition from lower-cost alternatives.

A company's value is often tied to its latest blockbuster in the pharmaceutical sector. Patent protection typically lasts 25 years from the date of discovery, with about half this time spent on testing. This leaves a limited window for profitability.

Investing in Lilly or any other pharma stock based on earnings expectations over 50 times isn’t always a guaranteed win. The firm’s upcoming offerings could indeed be significant earners, but they must offset foreseeable losses from other areas.

For instance, Trulicity, Lilly's top-selling treatment, generated nearly $2 billion in sales during the first quarter of 2023. However, Trulicity's revenue may be cannibalized by Lilly's own Mounjaro, with looming patent expirations set to intensify the pressure from 2027.

With robust profit margins exceeding 20%, the ascent of Eli Lilly to a trillion-dollar valuation is not only a bold prediction but also a captivating journey to monitor.

While this forecast appears to be grounded in solid reasoning and well-articulated facts, the reality of this industry is inherently marked by uncertainty and continuous change. Without the caveat of patent expiration, Lilly would be an unequivocal strong buy.

But given this reality, investors might be wiser to monitor Lilly first, rather than rush into a commitment. I suggest patiently waiting and buying the dip.

Mad Hedge Biotech and Healthcare Letter

July 18, 2023

Fiat Lux

Featured Trade:

(BIG PHARMA, BIGGER OPPORTUNITIES)

(AMGN), (HZNP), (BMY), (GILD), (PFE)

The irresistible charm of pharma companies often boils down to their potential pot of gold at the end of the rainbow: the groundbreaking drugs they're tirelessly laboring to introduce. But let's not be reckless.

As appetizing as these stocks may be, they carry a hefty price tag. Moreover, the road to drug development is fraught with unexpected potholes that can leave a nasty dent in the stock's value.

Alternatively, you could pivot to buying a cluster of the more affordable ones.

After all, embracing the tried-and-true philosophy of "a penny saved is a penny earned" can be a winning strategy across diverse sectors, and pharma stocks are no exception.

Here are some options you can explore.

Hovering at $222, Amgen (AMGN) carries a price-to-earnings ratio slightly shy of 12. The firm is grappling with the challenge of a potential few-billion-dollar-a-year dip in sales for some of its drugs while making ambitious strides to enhance its annual revenue of $27 billion.

So far, the most notable beacon of hope for Amgen is its experimental obesity treatments, AMG133 and AMG786, positioned in a market that has the potential to skyrocket beyond a whopping $30 billion annually.

Meanwhile, in a bold move, Amgen has proposed a $27 billion acquisition of Horizon Therapeutics (HZNP).

This strategic takeover could directly bolster Amgen's earnings per share (EPS) by more than $5, significantly enhancing the firm's current annual EPS of $18.

Amgen remains resilient despite facing hurdles from the Federal Trade Commission, which has launched legal proceedings to halt the transaction. The company is not just fixated on Horizon; it has the bandwidth to explore other potential acquisitions or augment its stock buyback program.

Another stock to consider is Bristol Myers Squibb (BMY). Priced at a humble $63, it’s trading at a modest valuation, barely touching eight times its earnings.

The market trembles at the potential stagnation—or worse, reduction—of its annual EPS, currently soaring just above $8. This anxiety is fuelled by the projected multi-billion dollar decline in sales for several drugs as the sands of time run out on their patents. These drugs, after all, form a substantial portion of this year's anticipated revenue of $46.6 billion.

However, it's not all gloom and doom. Bristol Myers Squibb has not one, not two, but a whopping eight new drugs jostling their way through clinical trials. One to keep an eye on is milvexian, a stroke prevention formula that shows immense promise.

These innovative concoctions could eventually inject a stunning $30 billion into the company's annual revenue stream, with the stock potentially reaching an ambitious price target of $85, projecting a handsome upside of 32%.

Gilead Sciences (GILD) is one more stock to take into consideration. Trading at an enticing 11 times earnings, it’s a steal at $76.

Yes, some of its products are on the downhill, but here's the game-changer: Trodelvy, an innovative cancer treatment.

Anticipated to triple revenues, this treatment’s sales is projected to surge from a humble $1 billion this year to a staggering $2.7 billion by 2028.

This suggests an upward trajectory for Gilead's sales, hurtling from just shy of $27 billion this year to well over $30 billion by 2028. The earnings per share (EPS) is poised to see an annual gain of about 6%, potentially reaching nearly $9 by then.

There’s also Pfizer (PFE), priced at a modest $36 and trading just shy of 11 times earnings.

As the dark cloud of Covid-19 gradually disperses, the pharmaceutical titan projects a significant contraction in its annual vaccine sales - halving it down to nearly $14 billion this year, contributing to the overall $67.8 billion income.

But don't be too hasty to dismiss Pfizer's prospects. Its innovation pipeline is teeming with promising solutions like its groundbreaking meningitis therapy. Moreover, it's poised to breathe fresh life into its vaccine division by fusing a flu and Covid vaccine.

Come 2026, the company anticipates its vaccines will arm over 130 million Americans, a notable surge from this year's 79 million recipients of the Covid vaccine alone.

You may find a less treacherous path by adopting a strategic approach of integrating more economically priced pharma stocks into your portfolio.

These stocks may grapple with dwindling sales from established drugs and the relentless onslaught of generic brands.

Nevertheless, they also harbor promising new entrants that, if successful, could spark a significant rally.

All things considered, the companies mentioned above are not mere “cheap” stocks but intriguing opportunities laced with robust potential. I suggest you take advantage of the dip.