Below please find subscribers’ Q&A for the October 18 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from London England.

Q: Is Nvidia (NVDA) a buy at the current price?

A: Absolutely, if your view is more than, say, a month. This stock will easily be $1,000 in the next year or two. They have such a huge moat on their business, and the high-end chips that are banned in China are only a tiny fraction of their overall business—they’re still allowed to sell small and medium-sized chips.

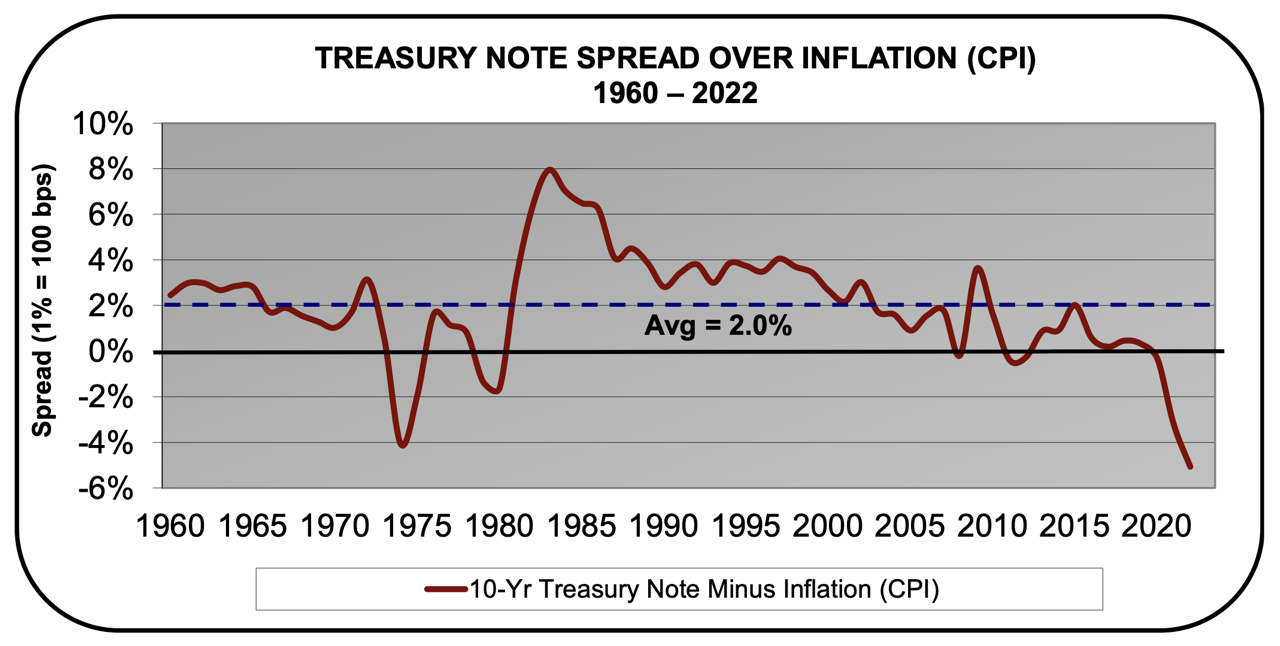

Q: Where do you see bond yields peaking out?

A: My pet target is 5.2% on a spike. We may get there in a few weeks or months. The position we have breaks even at 5.15% in 21 trading days. So any kind of rally on that position becomes profitable—even a one-day rally.

Q: Are you hitting Israel next?

A: No, I covered the Middle Eastern wars for 10 years starting with the ‘73 Yom Kippur wars, and I got sick of it. They’re using the same arguments to justify their positions that they were 50 years ago. In fact, the disputes have been going on for hundreds of years. So, I moved on to other more interesting wars like Ukraine. There are plenty of newbies cutting their teeth as war correspondents in Gaza now—I'll leave it to them.

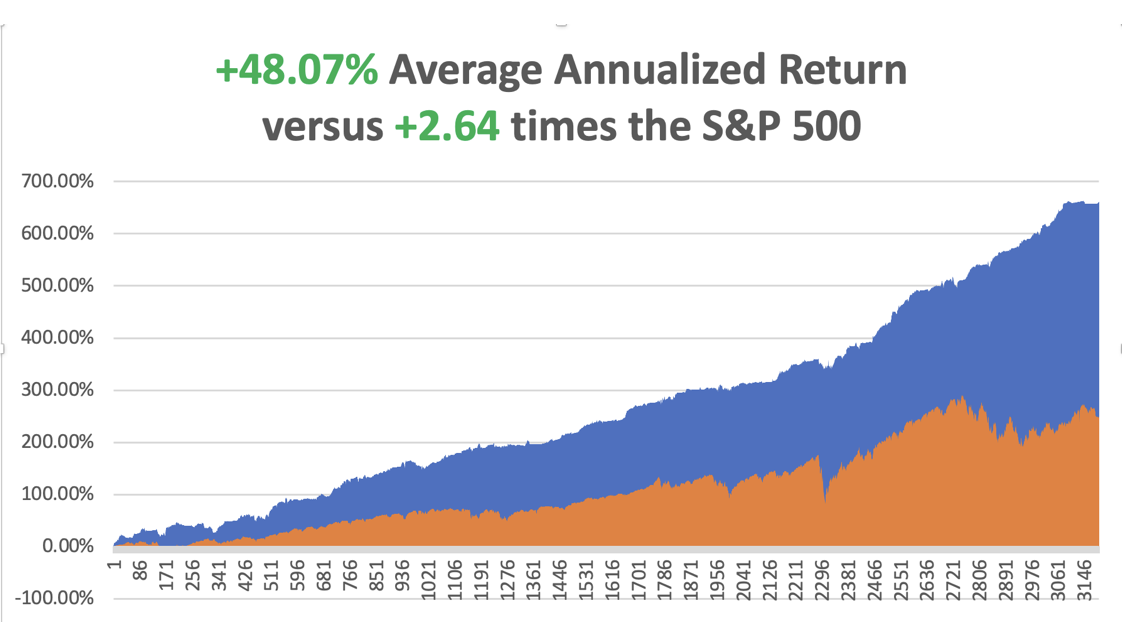

Q: Are the results for all of the newsletters or just for one?

A: Those alerts that I send out personally are the results for the Mad Hedge Global Trading Dispatch. All of the other services (we have six now) have their own trade histories which we don’t publish, as it’s too much of an account job effort to update six independent track records. People know whether they’re making money or not—that's good enough for me. That’s how we’re set up; we’re a staff-light operation so that we can keep the prices low.

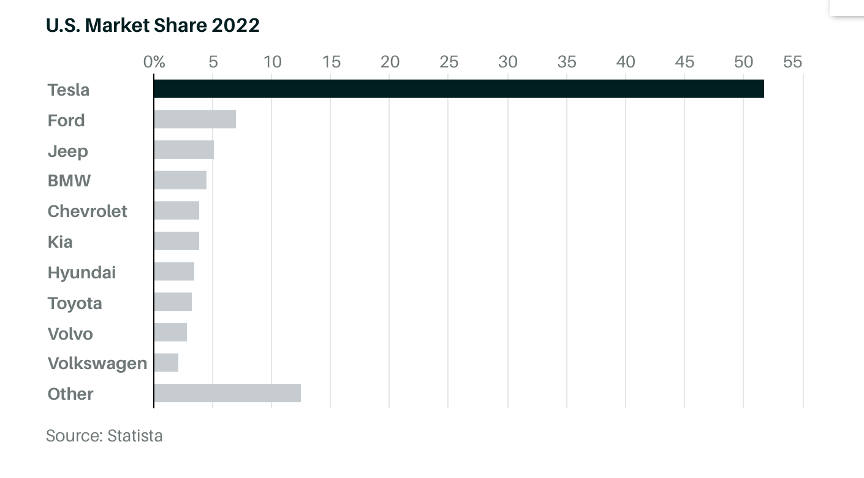

Q: What do you expect for Tesla (TSLA) earnings today?

A: I never make same-day earnings calls, but I would expect they’d be good. They would be less than they were in the past because the price wars are cutting into margins, but they’re gaining market shares at everybody else’s expense, which makes (TSLA) a “BUY”. In fact, if you look at the charts, it seems to be moving sideways into an upside breakout.

Q: Is it too late to buy military?

A: No, I’d be buying any of the big military stocks like Lockheed Martin (LMT), because the increase in demand for weapons is not a short-term thing—it is a more or less permanent thing which will go out decades. Also, they all already have massive government contracts to rebuild our own weapons. Most people don't realize that almost every weapons system in the United States is more than 50 years old. The reason is we quit investing in conventional weapons because we all thought the next war would be cyber. Well, Russia got absolutely nowhere on cyber—they made a few weak attempts to shut down Ukraine and couldn't even break into Elon Musk’s Skylink system, which all of Ukraine is running on.

Q: Why is Morgan Stanley (MS) doing so poorly?

A: All the financials are getting hit because of the collapsing bond market. Once the bond market finds a bottom you want to be buying financials with both hands.

Q: When the market recovers, which sector will lead?

A: Technology. The Magnificent Seven will lead. There’s safety in size. Google/Alphabet (GOOG), Nvidia (NVDA), Tesla (TSLA), Microsoft (MSFT), Amazon (AMZN), Apple (APPL), Facebook/Meta (META). They’re already leading now, so if you have those positions, I’d keep them. If you don’t, you should start picking them up.

Q: Is Rivian (RIVN) a buy at this level?

A: Absolutely. Amazon, which owns 25% of the company, just hit 10,000 Rivian delivery vans. I’ve seen them in California, they’re completely silent—very interesting cars. It’s just a question of how quickly they can produce them.

Q: Why is there a market drop today?

A: It’s the bond market. The first thing you look at every day is the bond market—if it's doing crappy, everything sells off.

Q: Do you still suggest 90-day T-bills at this point?

A: We may end up getting a stock buying opportunity into the year-end. Even if we have to wait for a yearend rally, you get paid every day for 90-day T-bills, and you can sell them at any time and get interest up to the day you sell them because they’re discount bonds that appreciate every day to reflect the yield. It’s a great way to park money, and most brokers will let you buy stocks against your 90-day T-bill position. So say you want to go fully invested in stocks—you could do that while selling your 90-day T-bills the same day. Most brokers will let you do that, worst case charging you one day of margin.

Q: Do you think China is using the Hamas attack on Israel to distract the US?

A: No, China wouldn’t want to get involved in this. Iran has its fingerprints all over it. Iran supplied all the missiles used to attack Israel, and if the Israelis turn around and attack Iran by destroying all of their nuclear and missile-making facilities, I would not be surprised one bit. That may be what Biden is really doing over there—trying to convince the Israelis not to escalate the war.

Q: What are the chances of a US default on November 17 (TLT)?

A: So far on all of these government shutdowns, the US Treasury has been able to come up with magic tricks to keep from defaulting; but if the default is long enough, even they will have to stop paying interest to bondholders, which will increase the debt burden of the US government because a lower credit rating will cause it to pay higher interest rates. Why people think this is a great strategy is beyond me.

Q: Gasoline is down and oil is up—what’s going on?

A: That’s usually driven by the crack spread—the availability of gasoline from refineries in the US, so I wouldn’t use that as any kind of indicator.

Q: Do you think China (FXI) is shifting priorities away from economic growth to military strength?

A: No I don’t, they would love to have economic growth if they could, and in fact, their central bank has been stimulating their economy, and it's working; that’s how this morning’s report got back up to 5%. At the end of the day, they just want peace. All this military stuff—they’re just bluffing and posturing, which is really all they’ve ever done, at least since the Korean War. They weren’t even big participants in the Vietnam War, so China doesn’t worry me at all; there are bigger things to worry about. But they definitely have hit a wall in economic growth, and a big part of that is Covid, and a big part of that is a shrinking population—a shortage of workers, and a shortage of workers who can support older parents.

Q: Will there be an oil embargo against Israel? The US and Europe by OPEC countries?

A: No. The Middle Eastern governments know what's really going on here, even though what they may say in public is completely different. The fact is that Hamas started this war, and none of these other countries want Hamas in their countries because they know that the first thing they'll do is overthrow the local government. Effectively, Hamas doesn’t exist anymore either—they've really all been killed, so you just have to give some time for things to cool down out there, and of course, the US is working overtime to keep the situation from escalating, but we can only try—we can’t enforce this thing. One question I've been getting from a lot of people lately is: will the US send troops to Israel or to Gaza? The answer is no—we were in Iraq and Afghanistan for 20 years! We’re in no hurry to get back into a new war, especially a new 20-year war, and that would not be in our own interest. By the way, Israel can amply defend itself; they have the best military in the Middle East by far, largely supported by the United States. For me, the big mystery is how intelligence in Israel missed this attack. They were just completely asleep at the switch, and some day in the future there will be an investigation about this, but don’t expect it from the current government.

Q: Why won’t Egypt and Jordan take the Palestinian refugees?

A: They are both poor countries. Neither of them is oil-rich, and Egypt especially has a horrendous population problem—they are in fact the world's second largest food importer after China. They have 110 million people to feed and not enough production locally to do that, so it isn’t easy to take in 2 million Palestinians. If you don't believe me, go to Cairo—it's just incredibly crowded. With a population of 10 million you can't go anywhere, so where are they going to put 2 million more people? So this is a difficult problem, there's no easy fix depending on what side you’re on.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, select your subscription (GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or Jacquie's Post), then click on WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Good Trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

2021 Mount Rose Summit Nevada