Many industries have experienced consolidation in the last few years and music streaming has been no exception.

The strong emergence of a few companies running the show has resulted in these same companies wielding extraordinary pricing power.

Spotify (SPOT) has been one of the leading music streaming platforms for years, and when companies harness pricing power, they can raise prices to compensate for higher expenses.

That is exactly what Spotify did recently as their stock sold off on a wider-than-expected loss for the second quarter, even though subscribers surged.

The streaming service posted a net loss of 302 million euros.

Monthly active users (MUAs) beat estimates of 530 million to hit 551 million — a 27% improvement compared to the year-ago period. Net additions of 36 million represented Spotify's largest quarterly net addition performance in its history.

Premium subscribers also surpassed expectations of 217 million, jumping another 17% year over year to hit 220 million.

In its first-quarter report, the company said it expected to add 15 million new monthly active users in Q2, bringing its total to 530 million. It also expected revenue of 3.2 billion euros and to report 217 million paid subscribers in the quarter.

Spotify is continuing to invest in advertising, and its ad-supported revenue grew 12% year over year. The company said podcast advertising revenue growth reaccelerated to more than 30% year over year.

Spotify will increase the price of its Premium subscription offerings by as much as $2, which translates to a 20% rise for some plans.

In the U.S., Spotify’s Premium Individual offering now costs $10.99, up from $9.99, and the price of its Premium Duo plan changed to $14.99, up from $12.99. The company’s Premium Family plan is now priced at $16.99, up from $15.99, and the Student offering costs $5.99, up from $4.99.

Spotify doesn’t expect a drawdown in product demand from the price increase, and let’s face it, most people can handle paying an extra 2 bucks for something they use every day.

Music streaming is definitely close to becoming an industry participated in by just a few for as long as it’s a viable business.

That means Spotify will also have the opportunity to raise subscription prices again in the future.

The licensing issues alone are too much of a hurdle for most companies to get to launch so to really compete takes a high amount of upfront funds and in the world of high interest rates, tech firms can’t fund this type of retread business again.

Spotify isn’t a pure monopoly.

The others involved are Apple Music, Amazon, Tidal, Deezer, and Pandora.

SPOT’s stock has increased by over 85% after the earnings pullback, and at one point they were up over 100%.

Growing subscriptions at 27% is still considered something that a growth company does at a time when growth companies are hard to find.

It doesn’t matter that they aren’t profitable yet, as long as they add more subscribers, which they have strongly indicated they will.

The stock has pulled back from $175 and once the negative shakeout fades away, traders should get into SPOT while they still can.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-08-02 14:02:142023-08-18 00:36:53Spot On With Spotify

Is it worth it to invest in the “next Tesla” or is it way too optimistic there could even be a next Tesla?

This upstart challenger to Tesla, Lucid (LCID) is more or less what I thought about Tesla a few years ago – buy the car and not the stock.

Like many businesses in the world – it comes down to time and place.

Tesla benefited from generous federal subsidies, first mover advantage and LCID is just a little late to the action.

Why does that matter?

Tesla had its knife and fork at the table by itself when nobody else wanted to join them.

The problem with legacy automakers is that it took them too long to realize that EVs were a tsunami instead of a splash in a pond.

I know with conviction that EV makers like LCID are slogging through because of the numbers that materialize in their earnings reports.

The numbers are a manifestation of the time and place phenomenon that I just mentioned.

LCID continues to face major cash flow issues and will be lucky to exist in a few years.

A high burn rate is a hallmark of smaller EV companies and even Tesla had to be saved at the last second it its early days.

LCID simply doesn’t have the expertise and economies of scale to bring down the unit economics where it delivers a profit.

This achievement is also pushed out far into the future.

We are also seeing a widening gap in its production and deliveries, with approximately 4.76K units undelivered, with a growing inventory value of $1.01B.

LCID's resale value appears to be drastically impacted, with one recently auctioned for $85K, compared to the base model of $110,000.

The intense capital burn has forced LCID management to issue more common stock which dilutes current shareholders and suppresses the stock price.

While LCID may have won the battery competition through its longest driving range and market-leading design, the management's choice to go premium has clearly undermined the mass market.

This is a segment that fellow automakers such as Tesla (TSLA) and BYD (OTCPK:BYDDF) have invested great efforts while improving their supply chain and pricing strategies.

This alone suggests LCID's highly niche market segment based on the hefty price tag of $150K per unit, compared to TSLA at $40K and BYD between $20K to $30K (in China), effectively will stoke higher cash burn levels.

For now, LCID has not achieved break-even, selling every EV at a loss.

This signals weak consumer demand for LCID.

This automaker's expanded annualized production capacity of up to 90K vehicles in the AMP-1 facility and up to 155K in the Saudi Arabia facility.

Production is still miles behind Tesla at a time when supply chains and material costs are squeezing EV makers even more.

When we consider that the stock was trading at $20 per share just 1 year ago, the stock languishing at $7.50 today represents quite a pitiful performance.

I do acknowledge they make quite a nice EV.

However, it’s still highly debatable whether its business model is sustainable.

I do believe that around $4 per share is a good entry point for this EV maker.

Any pop from $4 should be sold.

There is no reason to overpay for LCID right now in a market that values accelerating and positive free cash flow.

Better the stock come to you than to go fishing for it.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-07-17 14:02:562023-08-01 14:43:13Is Lucid The Next Tesla?

There are many so-called “experts” and “economists” dumping on the upcoming tech earnings season.

I got it – they won’t be the best ever.

No need to beat a dead horse when it’s down.

They say that the optimism of a soft landing for the economy is dissipating as stubbornly high inflation keeps central banks hawkish.

It’s hard to believe that tech stocks have been on a tear in 2023 during a period of hawkishness.

Higher for longer luckily has not affected tech stocks yet, yet many are saying this earnings season could be the straw that breaks the camel’s back.

I must admit, at the intro level such as venture capitalism and start-ups, the rate environment has been nothing short of catastrophic.

Investors aren't giving money for just ideas anymore.

The good news is that at the incubator level, nobody cares because these paltry numbers don’t move the stock market and are decades away from going public.

It doesn’t matter to the tech market that the next Amazon or Facebook has a tough time borrowing with these sky-high rates.

Nobody cares because most people hold Apple and Tesla stock.

I am also willing to call B.S. on the negativity for the upcoming tech earnings season and will say it should be just fine.

I am not diminishing the belt-tightening going on inside the offices, it certainly is happening.

Tech companies are hunkering down, which is true because the low-lying fruit has been plucked off the branch.

42% of respondents from a recent survey said the biggest negative for the earnings season will be the impact of further tightening of financial conditions.

I would say that if that is the biggest risk out there to respondents, then tech shares will certainly end the year higher from today.

There’s also a widespread belief that earnings per share (EPS) will fall off a cliff and then rebound to growth in the final three months of the year, according to data by Bloomberg Intelligence.

This seems like the perfect setup for tech executives to lower the bar.

While the tech rally was boosted by the hype around artificial intelligence, over 70% of survey participants say the impact of AI on tech earnings is overblown.

Amid the gloom, the biggest positive drivers for equities will be any signs of easing inflation and cost cutting, according to the majority of those surveyed.

Ultimately, it has already been baked into the pie that margins will come under pressure as companies lose the ability to keep raising prices when inflation cools and as growth slows.

That doesn’t mean there will be anything more than a technical and orderly pullback which I have been championing for.

A result like that would be healthy for tech stocks.

Tech shares simply cannot go up in a straight line forever, but they keep defying gravity in the first 7 months of the year.

Even if the big 7 tech stocks signal some downshifting revenue trajectories, it won’t be more than a few days' drop in shares signifying a marvelous opportunity to finally get into some of these premium names that rarely offer optimal entry points.

Expect nothing special from this earnings season and buy any garden variety dip from premium tech stocks.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-07-14 16:02:072023-08-01 14:38:24Bad Tech Earnings Are Priced In

Silicon Valley has gone from the least regulated industry to trending the other way. On a global scale, draconian regulations are rearing their ugly head to really stymy places like China and artificial intelligence.

The European Union just rolled out a slew of proposed regulations on AI that could hamper its ability to embed itself in many tech companies.

The net result is highly bullish for Silicon Valley companies minus the chip companies that are experiencing revenue cuts.

When rules tighten, the entrenched benefit disproportionately and this could trigger a continuation of the tech rally that has been blistering hot this year.

Inversely, it will become even more difficult for start-ups to become unicorns, because they suffer more at smaller sizes to digest the higher amount of regulation that mature tech companies never faced.

Much of this is occurring at the highest level as the White House is considering new restrictions on exports of artificial intelligence chips to China, potentially adding to a list of banned semiconductor technology from Nvidia, Advanced Micro Devices, and other US companies.

The U.S. Department of Commerce could prohibit shipments of chips from Nvidia and others to customers in China as soon as early next month.

Nvidia, which produces graphics chips that drive the technology behind OpenAI Inc’s ChatGPT and Alphabet Inc’s Bard chatbots, is one of those chip companies that could see a slide in revenue in the short term.

Across the pond where governments are specialists at regulation, the European Parliament has approved draft legislation to regulate AI-powered technology.

The Act applies to anyone who creates and disseminates AI systems in the EU, including foreign companies such as Microsoft, Google, and OpenAI.

As outlined in the Act, EU lawmakers seek to limit or prohibit AI technology they classify as unacceptable or high risk.

It’s a little vague who will be deemed high risk but in the crosshairs are technologies such as predictive policing systems and real-time, and remote biometric identification systems.

Silicon Valley cash cows can function without these intrusive elements.

The AI Act would give the European government the authority to levy heavy fines on AI companies that do not abide by its rules.

Financial penalties may be steeper than GDPR penalties, amounting to €40 million or an amount equal to up to 7% of a company’s worldwide annual turnover, whichever is higher.

Beyond the government’s power to enforce the Act, European citizens would have the power to file complaints against AI providers they believe are in breach of the Act.

European officials expect to reach a final agreement on the rules by the end of 2023 after spending years developing the legislation. Such swift and consistent momentum to regulate technology in Europe stands in stark contrast to the United States, where lawmakers are still grappling with initial regulatory steps.

If passed, the Act is expected to become law by 2025 at the earliest.

It’s a lot easier for tech firms to operate in the Wild West when there are no rules, but if there are rules, it’s better than American tech has already built cash cows to keep the party moving right along.

It’s true there won’t be much competition and possibly an oligarchy, but it will translate into much higher share prices for the likes of Apple, Tesla, Meta, Microsoft, Google, and Amazon.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-06-28 15:02:592023-07-12 00:39:50Regulation Heats Up

Keeping up with the Joneses – that’s what Amazon is doing with its foray into generative artificial intelligence.

Its cloud division AWS is building a $100 million AI center to go toe to toe with increasing competition in cloud infrastructure services

The upcoming AWS Generative AI Innovation Center will become the heart and soul of Amazon experts in AI and machine learning.

This is a seismic strategic move for Amazon whom we have heard very little about in the generative AI sphere so far.

However, most people in the know understand that Amazon wouldn’t let this get away from them and use time wisely to concoct something worthy enough to show they have some skin in the game.

Unsurprisingly, AMZN shares were up relative to other big tech companies in a down week last week on the Nasdaq.

AMZN shares haven’t had quite the mojo that stocks like Tesla or Microsoft have had this year and this call to action is an aggressive step towards the vanguard of technological development.

I highly applaud the management at AMZN for this chess move.

In generative AI, algorithms are used to create new content, such as audio, code, images, texts, simulations, and videos.

Amazon said Highspot, Twilio, Ryanair, and Lonely Planet will be among the first users of the innovation center. With the new center, the company expects to hijack additional cloud services amidst increasing competition in the cloud infrastructure market.

Enterprise spending on cloud solutions reached $63 billion worldwide in the first quarter of 2023, up 20% from the same quarter last year.

Microsoft and Google had the strongest year-over-year growth rates, gaining 23% and 10% in worldwide market share, respectively. Amazon, the leader in cloud infrastructure, kept its 32% market share in Q1.

Amazon recently debuted Bedrock, an AI solution that allows customers to build out their own ChatGPT-like models.

The company also announced the upcoming Titan, which includes two new foundational models developed by Amazon Machine Learning.

Tech is largely downsizing staff and firing diversity officers and other woke positions, but the one area that is pushing for greater numbers is artificial intelligence data scientists and a bevy of LinkedIn posts show they are on the lookout to poach talent.

Amazon, who crushed Microsoft and Google in the business of renting out servers and data storage to companies and other organizations, enjoys a commanding lead in the cloud infrastructure market.

However, those rivals are early into generative AI, even though Amazon has drawn broadly on AI for years to show shopping recommendations and operate its Alexa voice assistant.

Amazon also failed to create the first popular large language model that can enable a chatbot or a tool for summarizing documents.

One challenge Amazon currently faces is in meeting the demand for AI chips. The company chose to start building chips to supplement graphics processing units from Nvidia (NVDA), the leader in the space. Both companies are racing to get more supply on the market.

At a technical level, Amazon shares and the rest of tech shares are quite overbought in the short term.

Last week was a modest pullback between 1-2% in the Nasdaq and I view that as highly bullish because of its orderly nature and lack of volume.

No panic selling is what we want for the markets to optimize the next bullish entry point.

After the modest price action digests fully, I do expect another dip-buying shopping spree for tech shares.

Stay patient and stay hungry.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-06-26 14:02:032023-06-27 00:48:19Amazon Joins the Party

I just received a call from the Marine Corps to go on emergency standby. This is not something the Corps does lightly.

The word is that there may be a coup d'etat underway in Russia and the entire US military has gone to a heightened alert status.

The Wagner group is Marching on Moscow with the intent of overthrowing the government, or at least the military. Putin took off in a plane which then disappeared radar, meaning he has either been shot down, or is flying low level to keep his destination secret.

This thing could go nuclear very easily, but only in Russia. It also could mean the end of the Ukraine War. There is nothing to do here as intelligence pours in over the weekend. We have ample satellites overhead and human intel on the ground.

Expect market volatility today. The markets are ripe for a black swan-inducted selloff, which a Mad Hedge Market Timing Index at 82 was screaming at us.

I will be monitoring the situation closely.

My view that the markets were topping was vindicated last week. The “Magnificent Seven” which gained a record 25% in market capitalization in only eight weeks led the downturn, as they always do. But the AI surge that prompted the fastest equity creation in history is only just getting started.

This is against a backdrop of savage cost-cutting by Big Tech, which has had the effect of boosting earnings by an impressive 7% in only three months. My cleaning lady, gardener, dry cleaner, and shoe shine boy have started giving me stock tips yet, as they did in 2000, 2008, and 2020….but they are thinking about it.

While attention is focused elsewhere, one should not underestimate the importance of India Prime Minister Modi’s meeting with Joe Biden in Washington.

It signifies a major geopolitical shift out of the Russian orbit into the US one. Decades ago, India obtained all its weapon systems and nuclear power plants from Russia and was a major trading partner.

Now partnering up with Apple (AAPL), Google (GOOGL), Microsoft (MSFT), and General Electric (GE) is a much more attractive option. It is gaining a $2.7 billion factory from Micron Technology (MU) and presents a major market for its products. Amazon (AMZN) is investing $13 billion in cloud infrastructure there. The subcontinent graduates some 2.5 million STEM graduates a year and they need to be put to work in the global economy. It shows how limited Russia’s future really is. It’s a major win for the US.

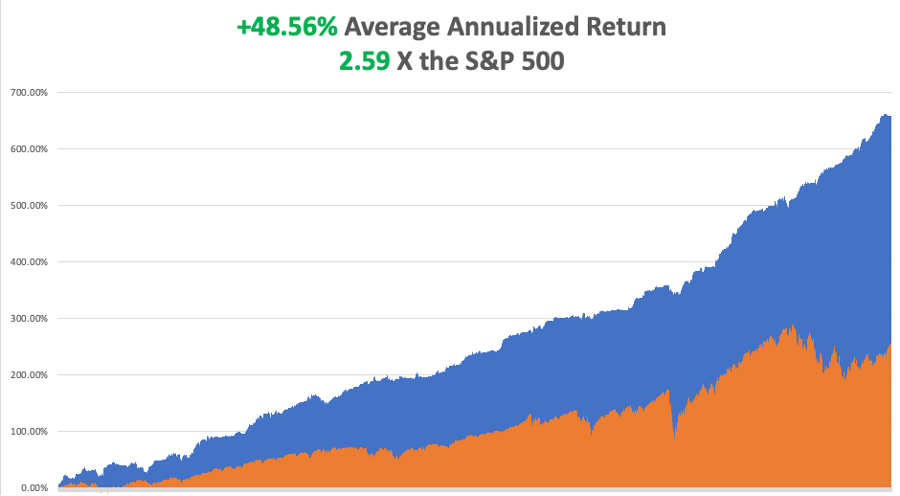

So far in June, we are up +0.47%. My 2023 year-to-date performance is still at an eye-popping +62.52%. The S&P 500 (SPY) is up only a respectable +14.00% so far in 2023. My trailing one-year return reached +96.63% versus +21.52% for the S&P 500.

That brings my 15-year total return to +659.71%. My average annualized return has blasted up to +48.56%, another new high, some 2.59 times the S&P 500 over the same period.

Some 42 of my 46 trades this year have been profitable. Only 23 of my last 24 consecutive trade alerts have been profitable.

The Mad Hedge December 6-8 Summit Replays are Up. Listen to all 28 speakers opine on the best strategies, tactics, and instruments to use in these volatile markets. It is a true smorgasbord of investment strategies. Find the best one to suit your own goals. The product discounts offered last week are still valid. Start, stop, and pause the videos at your leisure. Best of all, access to the videos is FREE. Access them all by clicking here and then choosing the speaker of your choice. We look forward to working with you.The next summit is scheduled for September 12-14.

$2 Billion Fled Stock Market Last Week, according to a Bank of America survey, in what it calls a “Baby Bubble.” The markets are showing all the signs of an interim top, with either a 10% correction or a three-month flat line ahead of us. Time to strap on those Buy Writes for long-term shareholders.

Short Bets on US stocks Hit $1 trillion, the highest since April 2022. Shorts have so far lost $101 billion in 2023, with much of this hedged. The market is way overdue for a correction so these guys may finally be right. Even a broken clock is right twice a day.

Germany Signs Massive US Natural Gas Contract, in a major move to end reliance on Russian natural gas. Venture Global LNG will supply EnBW with 1.5 million tons a year of LNG starting in 2026. The 20-year sales and purchase agreement is Germany’s first binding deal with a US developer since the government announced ambitious plans to begin importing the super-chilled fuel. The move does a lot to eliminate the glut of gas in the US currently plaguing producers. Buy (UNG) LEAPS on dips. When China comes back on line, watch out!

Volatility Index ($VIX) Hits the $12 Handle, in a new multiyear low. At the high for the year in the S&P 500, complacency is running rampant. Time to add some downside hedges.

Copper Should be a “Critical Metal”, says billionaire Robert Friedland. A looming structural shortage is the reason, with the world going to an all-electric auto fleet and doubling of the electrical grid to accommodate it. Buy more (FCX) LEAPS on dips.

Leading Economic Indicators Down 0.7% for the 15th consecutive negative month. We are approaching the bottom of the trough in this cycle. I’ll focus on the half of the economy that is growing.

Distressed Commercial Property Debt is Exploding, up 10% to Q1 to $64 billion. Another $155 billion is waiting in the wings. This will go away when interest rates start to drop in six months.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper-accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, June 26 at 8:30 AM EST, the Dallas Fed Manufacturing Index is out.

On Tuesday, June 27 at 6:00 PM, S&P Case-Shiller National Home Price Index is published.

On Wednesday, June 28 at 7:30 AM, the Fed Governor Jay Powell speaks.

On Thursday, June 29 at 8:30 AM, the Weekly Jobless Claims are announced. The Final Report for Q1 US GDP is printed.

On Friday, June 30 at 8:30 AM, Personal Income and Spending is announced.

As for me, when I first met Andrew Knight, the editor of The Economist magazine in London 45 years ago, he almost fell off his feet. Andrew was well known in the financial community because his father was a famous WWII Battle of Britain Spitfire pilot from New Zealand.

At 34, he had just been appointed the second youngest editor in the magazine’s 150-year history. I had been reporting from Tokyo for years, filing two stories a week about Japanese banking, finance, and politics.

The Economist shared an office in Tokyo with the Financial Times, and to pay the rent I had to file an additional two stories a week for them as well. That’s where I saw my first fax machine, which then was as large as a washing machine even though the actual electronics would fit in a notebook. It cost $5,000.

The Economist was the greatest calling card to the establishment one could ever have. Any president, prime minister, CEO, central banker, or war criminal was suddenly available for a one-hour chart about the important affairs of the world.

Some of my biggest catches? Presidents Gerald Ford, Jimmy Carter, Ronald Reagan, George Bush, and Bill Clinton, China’s Zhou Enlai and Deng Xiaoping, Japan’s Emperor Hirohito, terrorist Yasir Arafat, and Teddy Roosevelt’s oldest daughter, Alice Roosevelt Longworth, the first woman to smoke cigarettes in the White House in 1905.

Andrew thought that the quality of my posts was so good that I had to be a retired banker at least 55 years old. We didn’t meet in person until I was invited to work the summer out of the magazine’s St. James Street office tower, just down the street from the palace of then Prince Charles.

When he was introduced to a gangly 25-year-old instead, he thought it was a practical joke, which The Economist was famous for. As for me, I was impressed with Andrew’s ironed and creased blue jeans, an unheard-of concept in the Wild West where I came from.

The first unusual thing I noticed working in the office was that we were each handed a bottle of whisky, gin, and wine every Friday. That was to keep us in the office working and out of the pub next door, the former embassy of the Republic of Texas from pre-1845. There is still a big white star on the front door.

Andrew told me I had just saved the magazine.

After the first oil shock in 1973, a global recession ensued, and all magazine advertising was cancelled. But because of the shock, it was assumed that heavily oil-dependent Japan would go bankrupt. As a result, the country’s banks were forced to pay a ruinous 2% premium on all international borrowing. These were known as “Japan rates.”

To restore Japan’s reputation and credit rating, the government and the banks launched an advertising campaign unprecedented in modern times. At one point, Japan accounted for 80% of all business advertising worldwide. To attract these ads the global media was screaming for more Japanese banking stories, and I was the only person in the world writing them.

Not only did I bail out The Economist, I ended up writing for over 50 business and finance publications around the world in every English-speaking country. I was knocking out 60 stories a month, or about two a day. By 26, I became the highest paid journalist in the Foreign Correspondents’ Club of Japan and a familiar figure in every bank head office in Tokyo.

The Economist was notorious for running practical jokes as real news every April Fool’s Day. In the late 1970s, an April 1 issue once did a full-page survey on a country off the west coast of India called San Serif.

It warned that if the West coast kept eroding, and the East coast continued silting up, the country would eventually run into India, creating serious geopolitical problems.

It wasn’t until someone figured out that the country, the prime minister, and every town on the map were named after a type font that the hoax was uncovered.

This was way back, in the pre-Microsoft Word era, when no one outside the London Typesetter’s Union knew what Times Roman, Calibri, or Mangal meant.

Andrew is now 84 and I haven’t seen him in yonks. My business editor, the brilliant Peter Martin, died of cancer in 2002 at a very young 54, and the magazine still awards an annual journalism scholarship in his name.

My boss at The Economist Intelligence Unit, which was modeled on Britain’s MI5 spy service, was Marjorie Deane, who was one of the first women to work in business journalism. She passed away in 2008 at 94. Today, her foundation awards an annual internship at the magazine.

When I stopped by the London office a few years ago I asked if they still handed out the free alcohol on Fridays. A young writer ruefully told me, “No, they don’t do that anymore.”

Sometimes, change is for the worse, not the better.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2021/09/john-thomas-economist-e1664802946349.png285500Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-06-26 09:02:572023-06-26 12:08:01The Market Outlook for the Week Ahead, or Is there a Coup Underway in Russia?

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.