Mad Hedge Technology Letter

May 26, 2023

Fiat Lux

Featured Trade:

(RIDE THE ELEVATOR UP WITH GENERATIVE AI)

(NVIDA), (FOMO), (APPL), (MSFT), (META), (GOOGL), (AMZN)

Mad Hedge Technology Letter

May 26, 2023

Fiat Lux

Featured Trade:

(RIDE THE ELEVATOR UP WITH GENERATIVE AI)

(NVIDA), (FOMO), (APPL), (MSFT), (META), (GOOGL), (AMZN)

Part of these artificial intelligence executives going on record to sound out the problems with AI is mostly to protect themselves if this weird digital experiment goes disastrously wrong.

They have mostly said that AI going rogue is a real possibility and could end mankind.

Obviously, we hope that doesn’t happen.

Much of the tech market gains this year have been because of the technology surrounding AI.

Strip that out and the gains will look paltry.

A good example is Nvidia (NVDA) offering legendary guidance to the demand of their chips because of the need to install them in AI-based technology.

The AI narrative truly has legs – it will be the theme that defines 2023 in technology stocks.

The Big 7 tech stocks will possess explosive qualities to their stock precisely because of this thesis.

Then there is the fear of missing out (FOMO).

Every financial advisor is pitching AI as an investment of a lifetime – something that cannot be missed by their clients.

Therefore, I do expect meteoric legs up in shares of Nvidia, Apple, Microsoft, Tesla, Amazon, Facebook, and Google in 2023.

These 7 stocks dominate the tech market and the generative AI gains will mostly manifest themselves in these 7 tech firms.

Yet there are dangerous concerns that AI could also destroy these companies and the internet which we interface with, because the changes could erode the trust in platforms by populating fake photos like deep fakes.

In Washington speech, Brad Smith calls for steps to ensure people know when a photo or video is generated by AI.

Brad Smith, the president of Microsoft, has said that his biggest concern around artificial intelligence was deep fakes, realistic-looking but false content.

Smith called for steps to ensure that people know when a photo or video is real and when it is generated by AI, potentially for harmful purposes.

For weeks, lawmakers in Washington have struggled with what laws to pass to control AI even as companies large and small have raced to bring increasingly versatile AI to market.

Last week, Sam Altman, CEO of OpenAI, the startup behind ChatGPT, told a Senate panel in his first appearance before Congress that the use of AI interferes with election integrity is a “significant area of concern,” adding that it needs regulation.

Lawmakers need to ensure that safety brakes be put on AI used to control the electric grid, water supply and other critical infrastructure so that humans remain in control.

It’s hard to know what is fake and real these days. Fake photos of politicians getting attacked or fake videos of tigers roaming around freely in Times Square New York look weirdly authentic.

AI is getting so good that nobody knows what is real anymore.

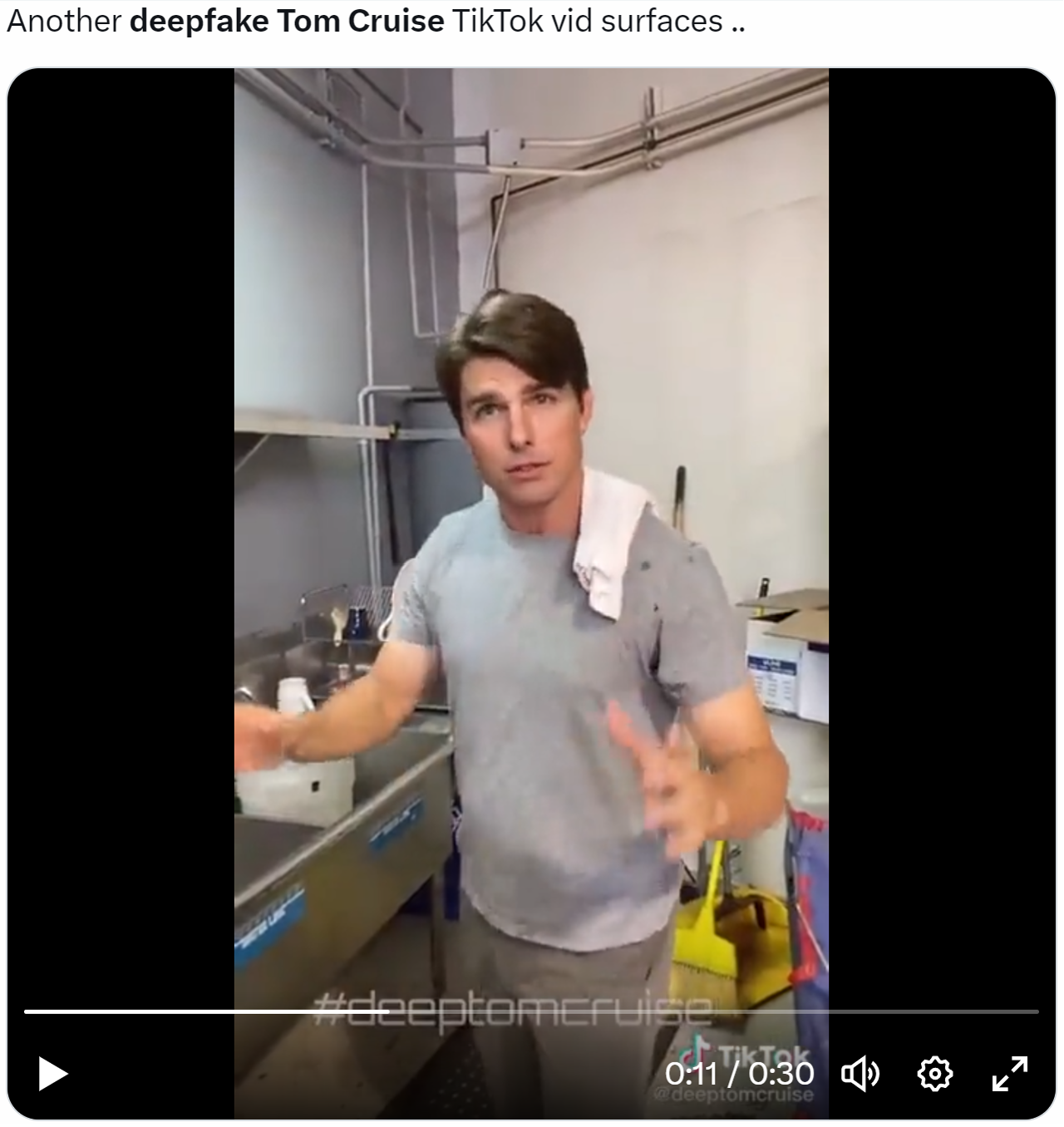

I’m sure some of you saw the recent Tom Cruise deep fake where the fake Tom Cruise is telling the audience that he does a lot of “industrial clean up” along with his own stunts. Honestly, I could not tell it was fake, and most people wouldn’t. It caught me – hook, line, and sinker.

As it stands, ride this generative AI to riches in the short-term, but be aware that this technology could blow up the internet or make the internet unusable because of security and trust reasons.

DEEPFAKES LOOK AND SOUND TOTALLY REAL IN 2023

Global Market Comments

May 26, 2023

Fiat Lux

Featured Trades:

(MAY 24 BIWEEKLY STRATEGY WEBINAR Q&A),

(FCX), ($INDU), (NVDA), (TSLA), (AMZN), (TLT), ($VIX), (CCI), (BABA)

CLICK HERE to download today's position sheet.

Below please find subscribers’ Q&A for the May 24 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Silicon Valley, CA.

Q: Should I roll over my $55-$60 Freeport-McMoRan (FCX) 2024 LEAPS?

A: Yes, move it from the January 2024 expiration to January 2025—that gives you a full 18 months for the stock to recover from a recession (which it’s now discounting) and then double, which is where you make the really big money on our LEAPS.

Q: What's your year-end price prediction for Freeport-McMoRan (FCX)?

A: $50, this year’s high.

Q: If there’s a default, do members of Congress get paid?

A: No, they don’t, no money is no money, the cupboard is bare. Nothing gets paid. And the Treasury will have to choose who gets paid last because when they run out of money there's no money to pay anybody, which then leads to a default and a 50% stock market correction.

Q: Why do you buy in-the-money bull call spreads instead of selling credit spreads?

A: They’re easier to understand for beginners. It’s easier for people to understand that if you buy something and it goes up, you make money. It’s harder for people to understand that if you sell short something and it goes down, you make money. And it’s basically six of one and half a dozen of the other in terms of profit. I get that question constantly and that is always going to be the answer.

Q: What do you think about artificial intelligence; how will it affect stock prices?

A: It’ll be what takes the Dow average ($INDU) from $32,000 to $240,000 over the next 10 years. What AI does is it automatically triples the value of any company using it, even though now it may take years for the stock market to catch up. On top of that, companies will have their regular earnings growth from their traditional businesses.

Q: How far will Nvidia (NVDA) stock go up?

A: Well the consensus between fund managers is it goes up 7 times from here, to well over 1,000. It's at 300 today, so it sounds like 2,100 is the final target, assuming we don't have any more recessions. And by the way, we did recommend NVDA on a split adjusted basis around $2, so NVDA has gone up 175 times already from our initial recommendation 7 years ago when it was just a gaming play. The (NVDA) January 2025 LEAPS I recommended on September 29 at 50 cents is now worth $6.25 and expires worth $10, up 20-fold!

Q: How can companies be selling AI prediction services for traders, as no one can predict the future?

A: Well that is accurate, no one person can predict the future. However, algorithms can take patterns in the past, project them in the future, and they're often accurate as long as a black swan doesn’t happen. AI is getting so sophisticated now—not only do we have index predictions which we’ve been using now for almost 10 years to great success, but Mad Hedge is now services with single stock recommendations. They will say in 30 days (AMZN) will be at $X, and they’re right 90% of the time. This is getting very advanced very quickly, and we are at the absolute cutting edge of this (and have been for a long time), and that’s why we’re getting such spectacular results—it's me plus my algorithm.

Q: Are money market funds at risk if the US defaults?

A: If the US defaults and stays defaulted, then yes. Nothing anywhere is safe except gold bricks under the bed. If the US does default, they’ll get defaulted probably in days. And that's what happened last time, 12 years ago. So, I don't expect the world to end.

Q: What is the best strategy for a long-term retirement account?

A: If you're already retired like over 70, I would go 100% into fixed income, and spread out your fixed income exposure to 10-year treasuries which is now yielding 3.75%, to junk which is yielding 8.5%. And you might throw in a couple high dividend stocks like (CCI). Over age 70 you basically are looking for a 100% income portfolio, because you’re too old to go back to work at Taco Bell if you lose all your money. And believe me, I’ve been to Taco Bell and seen the 70-year-olds working there who did lose all their money, so you don’t want to do that. Equities are for younger kids like me, who are going to live forever.

Q: What about iShares 20 Plus Year Treasury Bond ETF (TLT)?

A: We’re watching very closely. We will do LEAPS, but I’m waiting for a capitulation selloff triggered by inaction in Washington to get there. Also, when they do reach a deal, it unleashes a bunch of bond selling by the government. The US Treasury is going to have to sell 700 billion dollars’ worth of bonds immediately, because they’re behind on their bills, how about that? They’re not paying military contractors. So yes, the initial move of a debt deal could be down for bonds—that's the move I'm waiting for.

Q: Are you buying at the money’s or out of the moneys on LEAPS?

A: At the money if you’re a conservative old fogie like me, and out of the money like 20% or 30% where you get like a 400% return for younger people so they still will live long enough to earn back all the money if they lose it.

Q: What do you think the next move on CBOE Volatility Index ($VIX) is?

A: Up, and I think we could see VIX at $30 sometime in June or July when our 10% selloff happens.

Q: Would you buy the ProShares UltraShort S&P 500 (SDS) now for protection?

A: Yes, I’d be buying some as a hedge against your long-term positions.

Q: Do you prefer one or two year LEAPS?

A: Two years is the more conservative maturity because it gives you two years to go into recession and get back out. If you think there isn’t going to be a recession and we reaccelerate from here, then you only want to do one year. With Treasuries bonds, I’m inclined to do one year because I think once the rise in prices happens it’ll happen very quickly. If you’re not happy with a 100% return in a year maybe you should consider another line of business.

Q: Is the housing market going to crash because of 7% mortgage rates?

A: No, one third of all the buyers now are cash buyers, who are spending their savings and will refinance when mortgages get back to 3% or 4%. Until then, housing prices go sideways because there is a severe shortage of housing nationwide, which is getting worse.

Q: How do I get my wife used to regenerative braking in Tesla (TSLA)?

A: Just take your foot off the acceleration pedal; as the car slows down, each of the four wheels perform as generators and recharge the battery. That means when you drive from Lake Tahoe at 7,000 ft down to the Central Valley at sea level, your power consumption is zero. You’re getting a free ride because you’re gravity powered, the wheels are recharging the battery the whole time. All you have to do is take your foot off the acceleration and the regenerative braking kicks in instantly. Teslas only use actual use brake shoes when they slowdown from five miles an hour down to zero.

Q: Which level is more likely this year in oil: $50 a barrel or $100?

A: Well, if we do get the recession or something close to it, we’ll see the $50 first, and then we’ll see the $100 on the recovery. That is what’s going to happen.

Q: When is the economic recovery going to be this year?

A: In the 4th quarter, starting in October, and the stock market will start discounting that in July or August. That is my view.

Q: What’s a better investment: stocks or real estate?

A: It depends on the person. At this level, stocks will probably deliver bigger returns than real estate. But real estate allows you 5-1 leverage. If you have an 80% mortgage, and that’s more leverage than most people can get in the stock market. The other thing about homes is that you don’t get to see the price every day in the newspaper and then panic and sell at the bottom. That's the other great thing about houses.

Q: Will this recording be available?

A: Yes we post it in about two hours on the website. You can look at all the charts and the commentary then.

Q: How would you hedge a 100% equity portfolio?

A: I would buy deep out of the money puts on the S&P 500, maybe 10% out of the money on puts—something like a 360 put on the SPY with a 2 month maturity. That gets you through the summer, gets you through any debt crisis, and certainly will reduce the volatility of your portfolio.

Q: Would you be buying Alibaba (BABA) down here?

A: No, I don’t want to get involved in China in anything—too much political risk.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH or TECHNOLOGY LETTER, then WEBINARS, and all the webinars from the last 12 years are there in all their glory

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

A Senior Citizen Teach Me the Computer at Taco Bell

Global Market Comments

May 22, 2023

Fiat Lux

Featured Trades:

(MARKET OUTLOOK FOR THE WEEK AHEAD,

or CONCENTRATION OF WEALTH AT THE TOP)

(AAPL), (GOOGL), (AMZN), (MSFT), (NVDA), (TSLA), ($VIX), (JPM), (BAC), (C)

CLICK HERE to download today's position sheet.

As I write this to you, I am flying at 30,000 feet over the red clay of Georgia. The azure blue of the Gulf of Mexico is on the left and the Golden State of California lies straight ahead.

I am returning from a five-day whirlwind tour of Florida, which saw me speak at three Strategy Luncheons and countless private meetings.

It was a blast!

Not only did I learn the local lay of the land, I often pick up some great trading ideas.

I first hitchhiked across the Sunshine State in 1967. Except for a few small towns on the coasts, there was nobody there. The entire inland of the state was covered with small cattle ranches and the odd tourist trap (mermaids, alligator wrestling, snake shows etc).

People thought the extensive freeway system was only built because the state was just 90 miles away from Cuba, then a Cold War flash point (it is officially called the “Dwight D. Eisenhower National System of Interstate and Defense”). Suddenly, somebody secretly started buying up land around Orlando. The locals thought General Motors (GM) was going to build a car plant there.

Then Walt Disney Corp (DIS) swept in and announced they were building a second Disneyland to cater to the east coast, creating an astonishing 70,000 jobs and the freeways started to fill up (click here for the video).

Today, driving around the state is a dystopian nightmare. The US population has doubled since the first Interstates were built in the 1950s, and the US GDP has increased by ten times, a byproduct of the Interstates. That means ten times more heavy truck traffic which has been mercilessly beating the life out of the roads. In Florida, the population has risen by more than fourfold as well, from 5 million to 22.2 million so you get the picture.

You lurch from one traffic jam to the next, even in the middle of the night. Whatever time Google Maps says it will take to get somewhere, triple it. The only consolation is that the traffic is worse in California.

I loved Key West where a very happy Concierge member made available an 1859 mansion close to the waterfront, restored and modernized down to the studs. By this time of the year, anyone with money has decamped for New England leaving only the retirees and beach bums.

I made the pilgrimage to Earnest Hemmingway’s home where he produced 70% of his published writings in only seven years. Another two boxes of manuscripts were discovered in the basement of his favorite bar last year.

It’s ironic that this state is now known for banning books that include sex and violence. Steinbeck’s work has already hit the dustbin, so old Earnest can’t be far behind.

What’s next? The Bible? It has lots of sex and violence.

As for me, Hemingway’s granddaughter, Mariel, stands out as the only Playboy cover girl I ever dated (April, 1982, I think). She is now happily married with three grown kids.

And yes, I did prove that it is possible to eat Key Lime Pie four days in a row.

As for the stock market last week, there really isn’t much to say. The concentration of wealth at the top continues unabated, as it is in the rest of the country. Stocks are still discounting a soft landing, while commodities, energy, and bonds expect a recession.

Go figure.

The top five stocks continues to suck all the money out of the rest of the market, (AAPL), (GOOGL), (AMZN), (MSFT), and (NVIDIA), the early beneficiaries of AI, accounting for 80% of this year’s market gains. Of the other 495 stocks, 250 are below their 200-day moving averages, meaning they are still in bear markets.

This is what has crushed volatility, taking the ($VIX) from $34 down to $15. The last time volatility was this low was just before the Long Term Capital Management fiasco where it languished around $9 (read Liar’s Poker by my friend Michael Lewis). When LTCB went bust, volatility rocketed to $40 overnight and stayed there for two years.

Options traders made fortunes.

Mad Hedge has nailed every trend this year. We bought tech and Tesla (TSLA) in January when we should have. We shorted ($VIX) every time it approached $30. Then we bought the banking bottom in March (JPM), (BAC), (C) and carried those positions into April.

We’ve been shorting Tesla strangles every month. And now we are 80% in cash waiting for the world to end one more time in Washington DC so we can load the boat with LEAPS and replay the movie one more time.

By the way, Mad Hedge has issued 25 LEAPS over the past year and 24 made money with an average profit of about 300%. Our sole loser has been with Rivian (RIVN), but even it still has 18 months to run. Never own an EV stock during a price war.

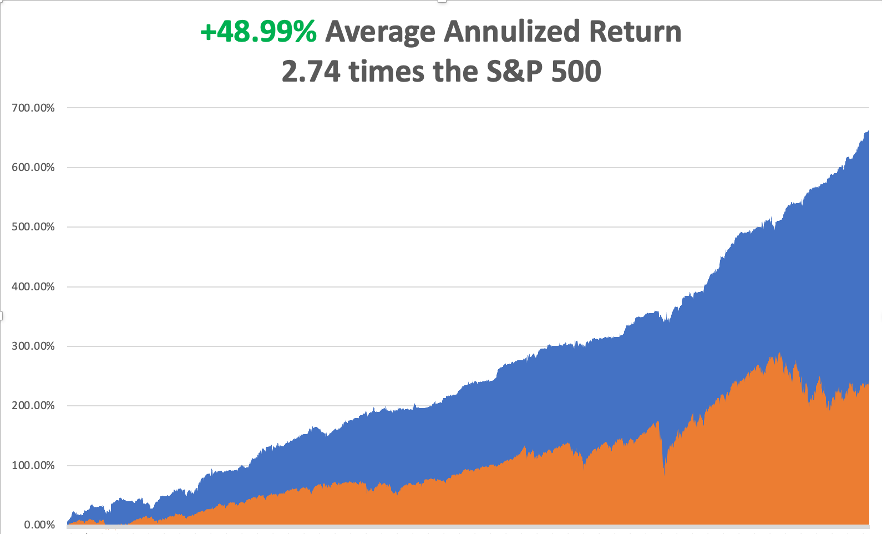

So far in May I have managed a modest 2.43% profit. My 2023 year-to-date performance is now at an eye-popping +64.18%. The S&P 500 (SPY) is up only a miniscule +9.00% so far in 2023. My trailing one-year return reached a 15-year high at +113.84% versus +10.87% for the S&P 500.

That brings my 15-year total return to +661.37%. My average annualized return has blasted up to +48.99%, another new high, some 2.74 times the S&P 500 over the same period.

Some 41 of my 44 trades this year have been profitable. My last 22 consecutive trade alerts have been profitable.

I closed out only one trade last week, a long in the (TLT) just short of max profit a day before expiration. That just leaves me with a long in Tesla and a short in Tesla, the “short strangle”. I now have a very rare 80% cash position due to the lack of high return, low risk trades.

There’s a 1,000 Point Drop in the Market Begging to Happen. That’s what happens when the market rallies on a Biden McCarthy debt ceiling deal, which McCarthy’s own party then votes down. After all, it took McCarthy 15 votes to get his job. Just watch volatility, it’s a coming.

Weekly Jobless Claims Fall to 242,000, down from 264,000. It’s a surprise slowdown. The rumor is that last week’s highpoint was the result of a surge in fraudulent online claims in Massachusetts.

NVIDIA Could Rise Fivefold in Ten years, say fund managers. I think that’s a low number. The Silicon Valley company makes the top performing GPU’s in the industry selling up to $60,000 each. (NVDA) is seeing a perfect storm of demand from the convergence of AI and Internet growth. The shares have already tripled off of the October low.

Tesla is Considering an India Factory, as part of its eventual build out to 10 plants worldwide. The country’s 100% import duty on cars has been a major roadblock. India is now pushing a “Made in India” initiative. Good luck getting anything done in India.

Homebuilder Sentiment Up for 10th Straight Month, as it will be for the next decade. There is no easy escape from a demographic wave. New homebuilders have figured out the new model.

India’s Tata to Build iPhones for Apple, in an accelerating diversification away from China. Apple has had too many of its eggs in one basket, especially given the recent political tensions between the US and the Middle Kingdom.

US Dollar Soars to Three Month High, as investors flee to safe haven short term investments. Rapidly worsening economic data is sparking recession fears. Ten consecutive months of falling inflation is another indicator of a slowdown.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper-accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, May 22 there is nothing of note to report.

On Tuesday, May 23 at 4:00 PM EST, the inaugural launch of Mad Hedge Jacquie’s Post takes place. Please click here to attend this strategy webinar. The Federal Reserve Open Market Committee minutes are out at 2:00 PM.

On Wednesday, May 24 at 2:00 PM, the Federal Reserve Open Market Committee minutes are out.

On Thursday, May 25 at 8:30 AM, the Weekly Jobless Claims are announced. The US GDP Q2 second estimate is also published.

On Friday, May 26 at 2:00 PM, the University of Personal Income & Spending and Durable Goods are released.

As for me, I am reminded of my own summer of 1967, back when I was 15, which may be the subject of a future book and movie.

My family summer vacation that year was on the slopes of Mount Rainier in Washington State. Since it was raining every day, the other kids wanted to go home early.

So my parents left me and my younger brother in the firm hands of Mount Everest veteran Jim Whitaker to summit the 14,411 peak (click here for this story ). The deal was for us to hitchhike back to Los Angeles as soon as we got off the mountain.

In those days, it wasn’t such an unreasonable plan. The Vietnam War was on, and a lot of soldiers were thumbing their way to report to duty. My parents figured that since I was an Eagle Scout, I could take care of myself anywhere.

When we got off the mountain, I looked at the map and saw there was this fascinating-sounding country called “Canada” just to the north. So, it was off to Vancouver. Once there I learned there was a world’s fair going on in Montreal some 2,843 away, so we hit the TransCanada Highway going east.

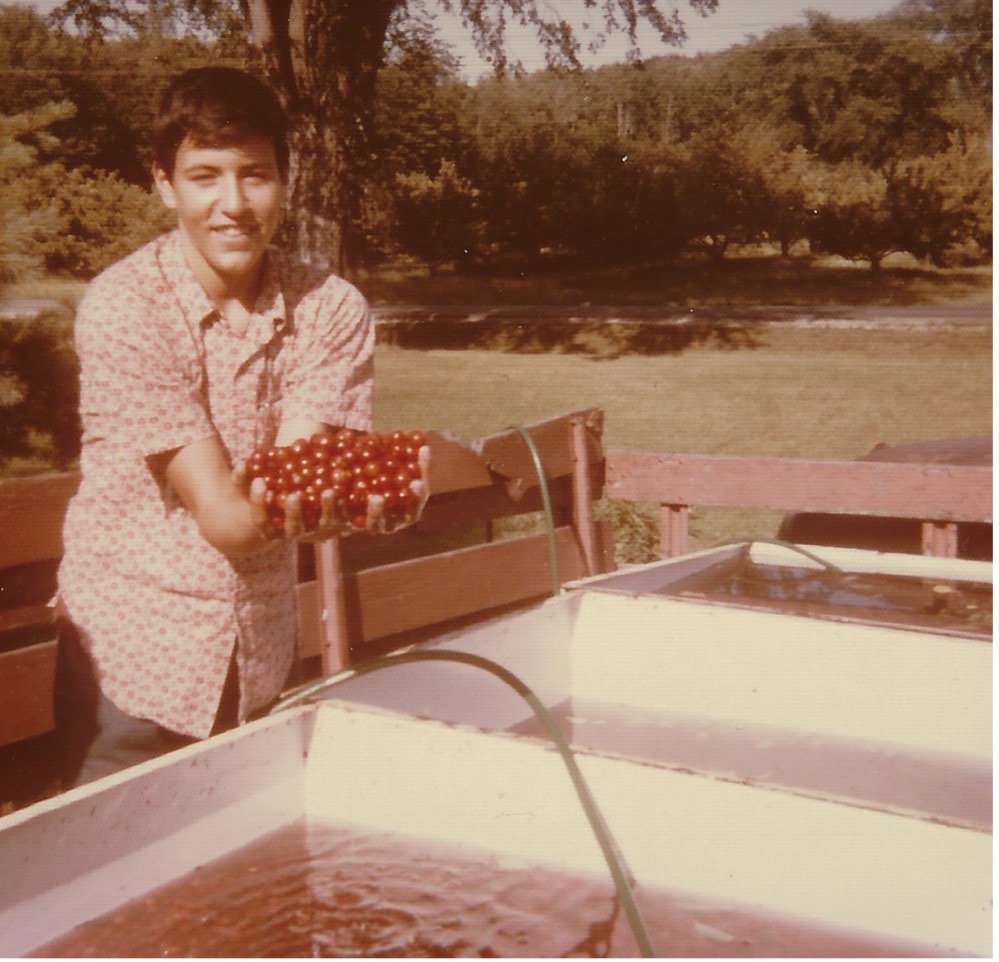

We ran out of money in Alberta, so we took jobs as ranch hands. There we learned the joys of running down lost cattle on horseback, working all day at a buzz saw, artificially inseminating cows, and eating steak three times a day.

I made friends with the cowboys by reading them their mail, which they were unable to do since they were all illiterate. There were lots of bills due, child support owed, and alimony demands.

In Saskatchewan, the roads ran out of cars, so we hopped a freight train in Manitoba, narrowly missing getting mugged in the rail yard. We camped out in a box car occupied by other rough sorts for three days. There’s nothing like opening the doors and watching the scenery go by with no billboards and the wind blowing through your hair!

When the engineer spotted us on a curve, he stopped the train and invited us to up the engine. There, we slept on the floor, and he even let us take turns driving! That’s how we made it to Ontario, the most mosquito-infested place on the face of the earth.

Our last ride into Montreal offered to let us stay in his boat house as long as we wanted so there we stayed. Thank you, WWII RAF Bomber Command pilot Group Captain John Chenier!

Broke again, we landed jobs at a hamburger stand at Expo 67 in front of the imposing Russian pavilion with the ski jump roof. The pay was $1 an hour and all we could eat.

At the end of the month, Madame Desjardin couldn’t balance her inventory, so she asked how many burgers I was eating a day. I answer 20, and my brother answered 21. “Well, there’s my inventory problem” she replied.

And then there was Suzanne Baribeau, the love of my life. I wonder whatever happened to her?

I had to allow two weeks to hitchhike home in time for school. When we crossed the border at Niagara Falls, we were arrested as draft dodgers as we were too young to have driver’s licenses. It took a long conversation between US Immigration and my dad to convince them we weren’t. It wasn’t the last time my dad had to talk me out of jail.

We developed a system where my parents could keep track of us across the continent. Long-distance calls were then enormously expensive. So, I called home collect and when my dad answered, he asked what city the call was coming from.

When the operator gave him the answer, he said he would NOT accept the call. I remember lots of surprised operators. But the calls were free, and Dad always knew where we were. At least he had a starting point to look for the bodies.

We had to divert around Detroit to avoid the race riots there. We got robbed in North Dakota, where we were in the only car for 50 miles. We made it as far as Seattle with only three days left until high school started.

Finally, my parents had a nervous breakdown. They bought us our first air tickets ever to get back to LA, then quite an investment.

I haven’t stopped traveling since, my tally now tops all 50 states and 135 countries.

And I learned an amazing thing about the United States. Almost everyone in the country is honest, kind, and generous. Virtually every night, our last ride of the day took us home and provided us with an extra bedroom, garage, barn or tool shed to sleep in. The next morning, they fed us a big breakfast and dropped us off at a good spot to catch the next ride.

It was the adventure of a lifetime and I profited enormously from it. As a result, I am a better man.

As for my brother Chris, he died of covid in early 2020 at the age of 65, right at the onset of the pandemic. Unfortunately, he lived very close to the initial Washington State hot spot.

People often ask me what makes me so different from others. I answer, “My parents taught me I could do anything with my life, and I proved them right.”

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Summit of Mt. Rainier 1967

McKinnon Ranch Bassano Alberta 1967

American Pavilion Expo 67

Hamburger Stand at Expo 67

Picking Cherries in Michigan 1967

Mad Hedge Technology Letter

May 19, 2023

Fiat Lux

Featured Trade:

(DON’T COUNT OUT THE TECH SECTOR)

(GOOGL), (MSFT), (AMZN), ($COMPQ)

It’s no surprise that the technology industry led other sectors to the number of job cuts in 2022.

It found more than 150,000 tech workers received pink slips in the year, a 900% increase from 2021.

In 2023, tech layoffs continue throughout various firms, and let’s go through some of the prominent ones.

Microsoft (MSFT) announced cuts to 10,000 workers, representing approximately 5% of the company's workforce.

Amazon (AMZN) announced 18,000 layoffs across many of the company's business areas, including Amazon Web Services, its healthcare businesses, the robotics unit, and many others.

Google announced 12,000 job cuts in January.

Tech hiring took off during the pandemic as the societal shift toward digital services meant technology firms needed to iterate and boost efficiency.

Many companies became too bold in hiring and in some cases, didn’t have enough work for the new workers.

Growth cratered as the pandemic eased, interest rates rose, and inflation cut into personal spending and increased many business expenses. Tech companies also need capital to invest in artificial intelligence (AI) or other innovations, and reducing staffing is one way to generate cash.

Amid these private company layoffs are reports of current and recently laid off employees dumping private shares, as they need capital in the face of falling valuations.

Another driver for private share selling is the low number of initial public offerings (IPOs), which reached the lowest point in 20 years in 2022.

The lack of potential windfalls from an IPO pushed more employees to sell some of their private shares, which then drops their companies' valuations. Lower valuations impact a company's ability to raise additional capital and strain the available venture capital funds.

The broad-based decimation of high-paying Silicon Valley jobs might be the trigger that plants the seeds for the new era of technology.

One of many unintended consequences of the “great resignation” of 2022 that bled into 2023 is that it refuels the pool of talent across the tech sector.

Many of these workers will find employment with other tech firms for a lot higher pay, but others will take the opportunity to launch their own startups.

A survey of 1,000 laid-off tech workers found 63% of the respondents started their own company after their layoff. And tech workers reported they made more money after starting a company.

Obviously, the new talent won’t be able to produce innovative products right away because of the lag involved.

However, put that many great minds in one room, something genius is bound to sprout up.

And I’m not talking about something marginal like buy now, pay later which is just another variation of a payment service.

I do believe we are on the cusp of another technological renaissance that could boost tech revenues 10-fold.

The pandemic reinforced the trend that many of the Silicon Valley headliners were burnt out. Many took the chance to move to Texas or the beaches in Florida.

I do believe that the next innovative wave is on the way and this time it won’t come from California because so much of the talent left.

In the short-term, these big job cuts from established tech royalty will contribute to higher stock prices but it will send the fired on a mission to reimagine themselves in the form of generation-changing innovation and productivity.

Generative A.I. is just one example of that.

Until then, expect big tech shares to grind up. I hear how bearish everyone is, but point me to someone that is actually selling.

Take for instance the supposed activist genius Carl Icahn, who recently reported of gargantuan multi-billion dollar losses over the past few years because he bet on a tech crash.

As long as there are investors, expect tech shares ($COMPQ) to march higher.

Global Market Comments

May 10, 2023

Fiat Lux

Featured Trades:

(FRIDAY MAY 19, 2023 BOCA RATON, FLORIDA GLOBAL STRATEGY LUNCHEON)

(WHY THE ROBOTICS INDUSTRY IS RAINING GOLD)

(GM), (ISRG), (ABB), (TER), (YASKY), (FANUY), (AMZN), (BMWYY), (KUKAF)

CLICK HERE to download today's position sheet.

We need to look back to the ancient world to discover the origins of robots. During the industrial revolution, humans developed the structural engineering capability to control electricity so that machines could be powered with small motors.

The idea of the humanoid machine was developed in the early 20th century. The first uses of modern robots were in factories as industrial robots. A car company - General Motors - paved the way here first.

General Motors (GM) introduced the first industrial robot, called "The Unimate," back in 1959. It was just a simple hydraulic arm that did some repetitive welding tasks. Seven years later, "The Unimate" made a friendly appearance on The Tonight Show with Johnny Carson, where it played not such a bad imitation of golf.

As technology has improved and become cheaper, robots have become more prevalent. Robot sales in North America have hit record highs for the last three consecutive quarters. We now encounter robots in our daily lives in various forms: they vacuum floors (Zoomba), mow lawns, make coffee, and even provide companionship (see the movie Her).

Additionally, they help combat supply chain disruptions and inflation. Automation allows employees to focus on higher-value tasks and work efficiently. Robots now work successfully alongside humans.

So, the robotics industry looks like a savvy investment.

Why?

The global robotics market is expected to grow at an impressive CAGR of 23% from 2021 to 2026, eventually hitting a cool $186.7 billion by the end of that span.

The range of robotics applications continues to expand at lightning speed and has become evident in everything from manufacturing to healthcare, logistics to agriculture, and beyond. It's all driven by many factors behind the scenes, like advancements in AI and machine learning, growing demand for automation, and improvements in sensor technologies. More and more companies are tapping into robotics R&D, and the stock market is taking notice.

One company that is particularly well-positioned to benefit from the growth of robotics is Intuitive Surgical (ISRG).

Intuitive Surgical is a pioneer in the field of robotic surgery, with its flagship da Vinci Surgical System being used in over 7 million surgeries worldwide. The company has a market cap of $125.6 billion, and its stock has been surging in recent years, growing by over 800% in the last decade.

Presently, about half of all robotic procedures are used in urological and gynecological procedures, but robotic surgery has applications across the medical field. Currently, only 3% of all surgeries are done robotically, so there is a lot of potential for growth in this area.

Another company that benefits from the growth of robotics is ABB (ABB), a Swiss-Swedish multinational corporation specializing in robotics, power, and automation technology.

ABB has a market cap of $67.2 billion and is a leader in industrial robotics, with applications ranging from welding and painting to packaging and palletizing. The company's robotics division has seen double-digit growth in recent years, and it is well-positioned to capitalize on the continued expansion of the global robotics market.

Of course, the growth of the robotics industry isn't limited to these two companies. Other publicly traded firms that are likely to benefit from this trend include Teradyne (TER), Yaskawa Electric (YASKY), and Fanuc (FANUY), among others.

Logistics is also benefiting from robotics. As online shopping and same-day delivery become more popular, companies need help to keep up and must find ways to streamline their supply chains and reduce costs.

Robotics play a major role in solving these problems. Autonomous robots can zip around warehouses, grab products off shelves, and even help load and unload trucks.

A company that is leading the charge in this area is Amazon (AMZN).

Amazon has been investing heavily in robotics for years, and its acquisition of Kiva Systems in 2012 has been instrumental in the company's ability to scale its logistics operations. The company now has over 200,000 robots deployed in its warehouses, and it is constantly experimenting with new ways to use robotics to increase efficiency and reduce costs.

An additional reason that robots are becoming more in demand involves the transportation industry.

People keep coming up with state-of-the-art ways to make cars and trucks, and these new production technologies require lots of robots. Moreover, factories worldwide are getting upgrades, so they need revolutionary robots to help them improve.

In 2020, BMW AG (BMWYY) and industrial robots and systems manufacturer KUKA (KUKAF) signed a deal to provide more than 5,000 robots to new production lines and factories worldwide. KUKA stated that these industrial robots would be utilized globally at the BMW Group's overseas manufacturing facilities to produce present and future vehicle models.

Industrial robot costs have become much more reasonable over the past thirty years. They have dropped by an average of 50%. This decrease makes adopting robotics technology in various industries a feasible option.

Robots are not replacing factory workers. Instead, they're working alongside their human counterparts to free up their time for more critical tasks. The Institute for Operations Research and the Management Sciences backs the idea that investments in robotics technology equaled firm employment.

Science fiction robotic concepts have arrived in our modern-day environments and investors will now be able to profit handsomely from this industry.

In the wise words of Warren Buffett, "Opportunities come infrequently. When it rains gold, put out the bucket, not the thimble."

While the growth of robotics may lead to job displacement in some sectors, it's important to remember that this is a natural evolution of technology. As new jobs are created in various areas, such as robotics engineering and data analysis, we must adapt and embrace these changes.

In the meantime, savvy investors can capitalize on the continued expansion of the robotics market. Companies such as Intuitive Surgical, ABB, and Amazon are just a few examples of publicly traded firms well-positioned to benefit from this trend.

However, let's remember that the robotics industry is still in its early stages, and there are bound to be new players emerging in the coming years.

As with any investment, it's essential to do your due diligence and invest wisely. But the rewards could be massive for those willing to take the risk. So take Buffett’s advice and put out the bucket, to catch some of that golden rain.