(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE GOLDEN AGE OF BIG BANKING HAS JUST BEGUN) (JPM), (FRC), (BAC), (C), (WFC), (AAPL), (GOOGL), (META), (AMZN), (TSLA), (NVDA), (CRM), ($VIX), (USO), (TLT), (QQQ)

The United States is about to change beyond all recognition.

Most investors have missed the true meaning of the JP Morgan takeover of First Republic Bank for sofa change, some $10.6 billion. It in fact heralds the golden age of big banking. The US is about to move from 4,000 banks to four, with all of the profits accruing at the top.

Look at the details of the (JPM)/(FRC) deal and you will become utterly convinced.

(JPM) bought a $90 billion loan portfolio for 87 cents on the dollar, despite the fact that the actual default rate was under 1%. The FDIC agreed to split losses for five years on residential losses and seven years on commercial ones. The deal is accretive to (JPM) book value and earnings. (JPM) gets an entire wealth management business, lock, stock, and barrel. Indeed, CEO Jamie Diamond was almost embarrassed by what a great deal he got.

It was the deal of the century, a true gift for the ages. If this is the model going forward, you want to load the boat with every big bank share out there.

And the amazing thing was that (JPM) made the highest bid among a half dozen contenders.

Along with Health Care, banking is the last unconsolidated US industry. We have five railroads, four airlines, three trucking companies, three telephone companies, two cell phone providers….and 4,000 banks?

Other countries get by with much less. England has five major banks, Australia four, and Germany two, one of which goes bankrupt every decade (I’m not naming names). America’s financial system is an anachronism of its federal system where each of the 50 states is treated like a mini country.

The net net of this will be a massive capital drain from the entire country to New York where the big banks are concentrated. Local economies in the Midwest and the South will collapse for lack of funding. The West Coast will be OK with behemoth technology companies spinning off gigantic cash flows.

The other big story here is the dramatic change in the administration’s antitrust policy. Until now, it has opposed every large merger as an undue concentration of economic power. Then suddenly, the second largest bank merger in history took place on a weekend, and there will be more to come.

All it takes is a Twitter run by depositors. Every weekend has become a waiting game for the foreseeable future.

Needless to say, this makes all the big banks a screaming buy. Hoover up every one of the coming dip, including (JPM), (BAC), (C), and (WFC).

Big is beautiful.

To prove I am not perfect, my position in First Republic Bank (FRC) still sits on my broker statement a week after it filed for bankruptcy, dead, moribund, and worthless as if it is some form of punishment. It’s a very small position but it stings nonetheless.

It’s like they want to punish me for leading them astray. They have been copying my trades for ages without paying for them and I hope they took a big one in (FRC).

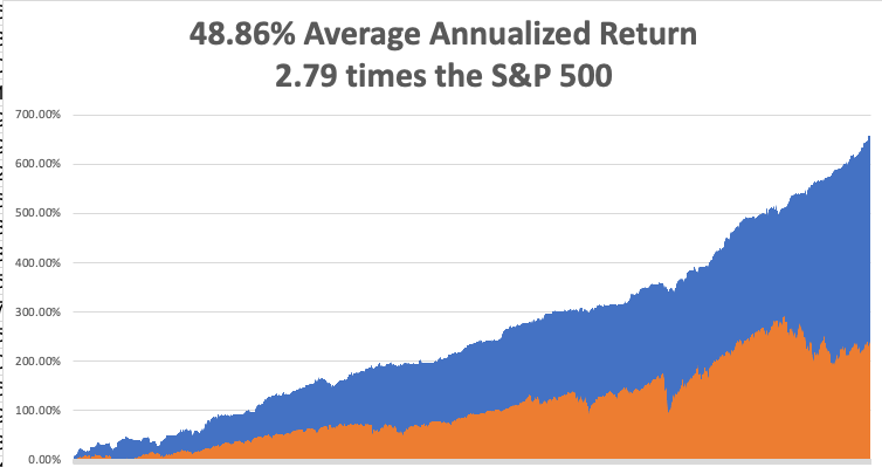

So far in May, I have managed a modest +0.55% profit. My 2023 year-to-date performance is now at an eye-popping +62.30%. The S&P 500 (SPY) is up only a miniscule +8.40% so far in 2023. My trailing one-year return reached a 15-year high at +120.45% versus -3.67% for the S&P 500.

That brings my 15-year total return to +659.49%. My average annualized return has blasted up to +48.86%, another new high, some 2.79 times the S&P 500 over the same period.

Some 40 of my 43 trades this year have been profitable. My last 20 consecutive trade alerts have been profitable.

I initiated no new trades last week, content to run off existing profitable ones. With the Volatility Index at a two-year low at 15.78%, opportunities are few and far between. Those include both longs and shorts in Tesla (TSLA), a long in the bond market (TLT), and a short in the (QQQ).

That leaves me with only one remaining position, a short-dated long in the bond market. I now have a very rare 90% cash position due to the lack of high-return, low-risk trades.

The Fed Raises Rates 0.25%, likely the last such move in this cycle. Futures markets are now discounting a 25-basis point CUT by September, the beginning of a new decade-long falling rate cycle. The problem is that AI is creating more jobs than it is destroying, keeping the Fed fixated on the wrong data.

Nonfarm Payroll Jumps by 253,000, another hot number. The headline Unemployment Rate dropped to a half-century low of 3.4%. These figures suggest for rate hikes to come.

The JP Morgan Buys First Republic Bank from the FDIC, for $10.6 billion, thus wiping out the shareholders. It’s a huge win for (JPM), which picked up 87 branches and $90 billion in loans in the wealthiest part of the country, taking the share up $5. What you lost on (FRC) you made pack on (JPM) LEAPS. Live and learn. On to the next trade! The FDIC got out for nearly free, a big win for the government.

Government DefaultDate Moved Up to June 1, by US Treasury Secretary Janet Yellen, smacking the bond market for three points. The House remains an albatross around the bond market’s debt.

Europe Ekes Out 0.1% Growth in Q1, versus a 1.1% rate for the US. This is despite the drag of the Ukraine War, energy shortages, high inflation, and Brexit. What’s the difference between the US and Europe? We allow immigrants who become customers, while the continent doesn’t.

You Only Need to Buy Seven Stocks This Year, as the rest are going nowhere. That include (AAPL), (GOOGL), (META), (AMZN), (TSLA), (NVDA), (CRM). Watch out when the next rotation broadens out to the rest of the market.

Is Volatility Bottoming Now? The Fed announcement of a 25 basis point hike on Wednesday could end the move up in stocks. After that, shares will only have an imminent debt default and US government downgrade to focus on. ($VIX) seven-week fade will end that revisit the old highs in the high $20’s. Great shorting opportunities are setting up.

Oil (USO) Crashes 5% on US debt default fears in the biggest drop since January. This is the worst asset class to own going into a recession. EV competition is also starting to take a bite. No gas needed here. $66 a barrel here we come.

More Tesla Price Cuts to Come, with swelling inventories forcing Musk’s hand. The only consolation is that Detroit will suffer more. Musk is cutting profits while the big three are accelerating losses. Tesla has excess inventory for the first time in its 20-year history.

Apple (AAPL) Earnings Beat, led by stronger than expected Q1 iPhone sales at $53.1 billion. EPS came in at $1.53 versus $1.42 expected, revenues at $94.84 billion versus $92.96. Mac and iPad sales are down YOY. Services rose 5.3%. Apple bought back a stunning $90 billion of its own shares and paid dividends. The shares popped $3. The long-term growth play here is low prices phone in India where second hand phone sales have been burgeoning. That's why Apple is now offering to buy your old phone. Next stop: New Delhi.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper-accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, May 8 at 7:30 AM EST, the Consumer Inflation Expectations are out.

On Tuesday, May 9 at 6:00 AM, the NFIB Business Optimism Index is announced. On Wednesday, May 10 at 11:00 AM, the US Inflation rate is printed. On Thursday, May 11 at 8:30 AM, the Weekly Jobless Claims are announced. We also get the Producer Price Index.

On Friday, May 12 at 8:30, the University of Michigan Consumer Sentiment Index for April is released.

As for me, I have been going down memory lane looking at my old travel photos looking for new story ideas and I hit the jackpot.

Most people collect postcards from their foreign travels. I collect lifetime bans from whole countries.

During the 1970s, The Economist magazine of London sent me to investigate the remote country of Nauru, one half degree south of the equator in the middle of the Pacific Ocean.

At the time, they had the world’s highest per capita income due to the fact that the island was entirely composed of valuable bird guano essential for agriculture. Before the Haber-Bosch Process to convert nitrogen into ammonia was discovered, guano was the world’s sole source of high grade fertilizer.

So I packed my camera, extra sunglasses, and a couple of pairs of shorts and headed for the most obscure part of the world. That involved catching Japan Airlines from Tokyo to Hawaii, Air Micronesia to Majuro in the Marshall Islands, and Air Nauru to the island nation in question.

There was a problem in Nauru. Calculating the market value of the bird crap leaving the island, I realized it in no way matched the national budget. It should have since the government owned the guano mines.

Whenever numbers don’t match up, I get interested.

I managed to wrangle an interview with the president of the country in the capital city of Demigomodu. It turns out that was no big deal as visitors were so rare in the least visited country in the world that he met with everyone!

When the president ducked out to take a call, I managed to steal a top-secret copy of the national budget. I took it back to my hotel and read it with great interest.

I discovered that the president’s wife had been commandeering Boeing 727s from Air Nauru to go on lavish shopping expeditions to Sydney, Australia where she was blowing $200,000 a day on jewelry, designer clothes, and purses, all at government expense. Just when I finished reading, there was a heavy knock on the door. The police had come to arrest me.

It didn’t take long for missing budget to be found. I was put on trial, sentenced to death for espionage, and locked up to await my fate. The trial took 20 minutes.

Then one morning I was awoken by the rattling of keys. My editor at The Economist, the late Peter Martin, had made a call and threatened the intervention of the British government. Visions of Her Majesty’s Navy loomed on the horizon.

I was put in handcuffs and placed on the next plane out of the country, a non-stop for Brisbane Australia. When I was seated next to an Australian passenger, he asked “Jees, what did you do mate, kill someone?” On arrival, I sent the story to the Australian papers.

I dined out on that story for years.

Alas, things have not gone well for Nauru in the intervening 50 years. The guano is all gone, mined to exhaustion. It is often cited as an environmental disaster. The population has rocketed from 4,000 to 10,000. Per capita incomes have plunged from $60,000 a year to $10,000. The country is now a ward of the Australian government to keep the Chinese from taking it over.

If you want to learn more about Nauru, which many believe to be a fictitious country, please click here.

As for me, I think I’ll pass. I don’t ever plan to visit Nauru again. Once lucky, twice forewarned.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2023/05/oceana-may2023.png6861024Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-05-08 09:02:522023-05-08 12:00:34The Market Outlook for the Week Ahead, or The Golden Age of Big Banking has Just Begun!

The one sound bite that really jumped out at me on Amazon’s earnings calls that sums up the zeitgeist right now in the tech sector is when CEO Andy Jassy said “customers are looking for ways to save money however they can right now.”

Savings money is foreign to growth tech, but investors should get used to the new Silicon Valley.

When the success of a tech firm is utterly reliant on mass volume of sales, this isn’t the type of trend that will drive earnings higher in the future.

I am not blaming Amazon for customers pinching pennies.

It has more to do with the generally macro malaise that US consumers are facing with the explosive price rises of the last few years.

There is no point to rehash about inflation, but the net effect is that there is less opportunity for these ecommerce companies to flog products.

The US consumer is even more reliant on debt to finance purchases than before and smart companies like Apple (APPL) have rolled out savings accounts because they are aware that the fight for deposits is up for grabs after the banking contagion.

Even though AMZN delivered us a great quarter in terms of profitability and top line growth, the larger takeaway was the uncertain path going forward.

Amazon CFO Brian Olsavsky told investors on the company's earnings call AWS customers are continuing "optimizations" in their spending.

The CFO described the first quarter as “tough economic conditions.

Revenue in Amazon's AWS unit grew 16% during the first quarter, down from an annual growth rate of 37% seen in the same quarter last year.

Disclosure that sales growth at AWS had slowed further in April sets the stage for AWS’s weakest growth rate since Amazon began breaking out the unit’s sales.

Amazon’s advertising business continues to deliver robust growth, largely due to ongoing machine learning investments that help customers see relevant information when they engage.

US customers are moderating spending on discretionary categories as well as shifts to lower-priced items and healthy demand in everyday essentials, such as consumables and beauty.

A little bit of a mixed bag, but disappointing guidance in AWS really sticks out like a sore thumb.

As we exit the bulk of big tech earnings, it is clear there is quite a bit of runway left for big tech shares to go higher.

I can’t say the same for every tech stock, because growth stocks have a different set of challenges that they haven’t been able to overcome.

Amazon still posted great earnings and investors should absolutely look to buy shares on the dip.

Even at less than 100%, AMZN is still worth owning over a lot of SPACs, growth tech, or emerging tech.

What we are seeing now are these behemoth tech companies leveraging their balance sheet in an interest rate matters world which is why small companies can’t compete anymore.

Although not technically monopolies, some of these tech firms are getting darn close with their closed “ecosystems.”

Buy AMZN on the next dip.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-04-28 14:02:142023-05-02 00:49:49Buy Amazon on the Dip

Below please find subscribers’ Q&A for the April 26 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Las Vegas, NV.

Q: Would you start adding to The Russell 2000 (IWM) around here?

A: No, the Russell 2000 is the most sensitive to market action and the most sensitive to an economic downturn, which it seems we have already entered. And you don’t add positions one week into the downturn, you do it like 3-6 months into the downturn. So, I would not touch (IWM) right around here.

Q: Are you buying more First Republic Bank (FRC) down here?

A: No, at this point the stock is a no-go. It is a ripe takeover target for someone, and the risk is, the takeover price is lower than your cost. I don’t understand why First Republic is down this far—like 97% — and when I don't understand things, I stay away. I had never seen a bank go under before that didn’t have bad loans, nor has anyone else. A lot of people were asking if they should double up, we went from $16 to $6 in a day, and the firm answer is that I just don’t know. The fundamentals of the company by no means justify that discount, it must be discounting something terrible that we haven’t heard yet. So I’m going to stay away and look for better trades to do.

Q: I missed the Tesla (TSLA) trade on Friday, should I be looking to buy the dips down here?

A: Yes, I would. I put out a May $110-$120 vertical bull call debit spread on Tesla, which is now only 3 weeks to expiration. Remember, at Tesla’s growth rate, the company is now 12% larger than it was when it hit the $104 bottom in January. I should point out that once our trade alert went out, it literally triggered billions of dollars worth of market action and crushed volatility. It took the implied volatility on Tesla options down 10% on that one day. So, with implied volatility this low, I’m not sure you can get Tesla done at any price that makes sense—but if you can, I’m all for it. As for the short, we’re almost in max profit on our Tesla short position. It’s cratered about $35 since we put it on, so I wouldn’t be chasing that one.

Q: Is there a reason why Freeport McMoRan (FCX) is not progressing upwards?

A: Recession fears—the long-term case for copper is spectacular— I’m looking for $100 in (FCX) a couple years down the road. With the short term, all they see is recession and US government debt default, and as long as those two things are overhanging the market, all of the economically sensitive plays are going to go down. You’re not going to get gains, you’re going to get losses. If you want to know how the debt default is working out, you can write a letter to Kevin McCarthy in Washington DC and ask him what he’s going to do. The stock market doesn’t like it for sure, so I’m inclined to go back to 100% cash and duck that whole cluster.

Q: Can China survive without foreign investment?

A: Yes, with a much lower standard of living, and technology that is greatly lagging behind the US. The Chinese use all the foreign investment going on to upgrade their own technology—it's very common for a Chinese worker to work for an American company for a year and then walk across the street and work for their main Chinese competitor. That is a major means of technology transfer. Without that, they fall way behind, and they know it. You can’t copy your way to leadership, as Japan found out to their great expense in the 1990s. You can add that to the long list of reasons why China will never invade Taiwan. Not only have they cut off their food and energy supply, but also their technology supply.

Q: Would it be safe to deposit my money with Apple (APPL) who’s offering a 4.15% interest rate?

A: Yes, Apple has about $150 billion in cash on the balance sheet to back up any deposit runs. I imagine Apple financially is probably far safer than any small regional bank in the US. But, there are better things to do than Apple, and that’s the good old 90-day US T-bill. That bill never defaults; it’s offering 5.2% — it may even be a little bit higher after May 3 when the Federal Reserve raises interest rates by 25 basis points.

Q: Aren’t earnings coming in better than expected?

A: Yes they are, however, the earnings season was frontloaded with the best-performing sector in the market—i.e. the banks—which you were 100% long of until last week, and the weaker performers are next. That seems to be what the stock market is telling us with the selloff, and of course, the weaker performers are technology stocks. So that's why I piled on the shorts (especially in the Invesco QQQ Trust), that’s why I cut back position sizes, it’s time to take the money and run.

Q: How much longer do you plan to do this?

A: Well Warren Buffet is 92 and he seems to be doing just fine. Joe Biden plans to be President of the United States until he is 86. Work for these men is their lives and they will never quit. The same is true for me. If they can do that, I can certainly run Mad Hedge Fund Trader until I am 92, or for 21 more years. Besides, what else would I do? I’m terrible at golf, I hate pickleball, Bingo is boring and is usually rigged, and all the other stuff that people my age do doesn’t appeal in the least.

Q: Are there ETFs that mirror the rates of 90-day T-bills, or is it better just to buy direct through my broker?

A: It’s always better to buy T-bills directly because your ETF does not work for free. They’re taking out fees somewhere, even if you can’t see them, even if they’re not in the marketing material—nobody works for free; except the US government, it would seem. So buy directly from the US government. If you own the T-bills and your institution goes bankrupt, you can always get your T-bills back in a couple of days. If you own their ETF that mirrors the T-bill, that can become a complete loss and you’ll get tied up in bankruptcy proceedings that last three years (and you may or may not get your money back.) So T-bills directly are the gold standard, I would buy those if you’re looking for a cash alternative.

Q: What about Rivian (RIVN)?

A: It’s red meat in this kind of market—don’t touch it. If the entire car industry is rolling over, including Tesla, don’t expect Rivian to outperform in that situation. As for Amazon (AMZN), like all tech stocks, I’m going to wait for the current selloff to work its way for its system, but then it’s probably a great long term buy and a two-year LEAPS.

Q: What’s your estimate for S&P earnings?

A: I’m at $220 a share which today gives us a multiple of 18.73, which is the middle of the recent range. We may drop a point or two from there, but that’s close enough for the cigar.

Q: Won’t wider credit spreads hurt iShares iBoxx $ High Yield Corporate Bond ETF (HYG)?

A: Yes, for the short term, but you’re being compensated for that by the 8% yield; and you’re buying junk bonds not for where they are for the next month or two, but where they are for the end of the year, which would be at least 10$-15% higher than they are now, so your total “all in” return might be as much as 25%. Not bad.

Q: What’s your thought on the Salesforce (CRM) drop?

A: I’ll buy it in about 3 months, once the next tech washout is finished and they’re throwing these things out with the bathwater.

Q: Do you think iShares 20 Plus Year Treasury Bond ETF (TLT) will trade higher if the market collapses?

A: Yes it will; that is your classic flight to safety out of stocks into bonds. We haven’t seen it in quite a while because both of them have been moving up and down together.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH or TECHNOLOGY LETTER, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Playing the Penny Slots in Las Vegas is Definitely NOT my Retirement

https://www.madhedgefundtrader.com/wp-content/uploads/2023/04/john-thomas-penny-slots.jpg212260Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-04-28 13:02:442023-04-28 14:27:44April 26 Biweekly Strategy Webinar Q&A

This is a seven-stock tech market and there is no point to getting exotic and buying something aside from these 7.

That is what the price action is telling us.

Four of the seven are no other than tech overlords Alphabet (GOOGL), Amazon, (AMZN), Microsoft (MSFT), and Meta Platforms (META). These four Big Tech stocks alone account for 41% of the S&P 500's 2023 gain.

The other three are Apple (AAPL), which reports next week, Nvidia (NVDA), and Tesla (TSLA) stock.

These seven account for 86% of the S&P 500's 2023 gain.

These seven Big Tech stocks have essentially made the market this year and everybody else is dragging behind kicking and screaming.

Part of the great performance has to do with the market's oversold nature in 2022.

Rarely does a market operate at the extremes for so long.

These seven have done more than bounce back.

The January Effect is a seasonal increase in stock prices throughout the month of January. The increase in demand for stocks in January is often preceded by a decrease in prices during the month of December, in part due to tax-loss harvesting.

Second, many of these tech companies have been aggressively cutting costs.

I would even say again that Facebook cutting 25% of staff since 2022 is not enough.

Get rid of 80% like Twitter did.

Even more important, the world's most advanced AI models are coming together with the world's most universal user interface - natural language - to create a new era of computing.

Microsoft helped kick off Big Tech's AI obsession with its multi-year, multi-billion dollar investment in ChatGPT developer OpenAI.

MSFT has since implemented versions of OpenAI's technology in its Edge browser, Bing search engine, Microsoft 365 productivity software, and cybersecurity offerings.

Microsoft leading the AI means that rival Alphabet's Google (GOOGL) is playing catch up. Amazon (AMZN), meanwhile, is working to bring generative AI to its services, while Facebook parent Meta (META) is piecing together teams to kick-start its own efforts.

And while Microsoft’s stock has seemingly benefited from both the AI hype and overall market rebound after a rough 2022, the company's main growth driver continues to be its cloud computing efforts in its Azure unit.

But that growth has drastically cratered over the last year. In Q3 2022, Microsoft reported Azure growth of 46% year-over-year. But that's since fallen each quarter, landing at 27% in Q3 2023.

Part of the reason for this decline was large customers pulling back on spending as higher interest rates challenged global growth. Microsoft is also contending with scarce PC sales, as demand from consumers and business customers falls from pandemic-era highs.

It’s easy to say that tech has fared quite well this year.

However, peel back the layers and the lack of participation in this tech rally is highly worrisome.

In a winner take all economy, we have never been reliant on a small group of stocks to save us from collapse.

Interest rates as high as they mean that without a strong balance sheet, it is tough sledding out there for the growth companies.

In the short term, I fully expect tech companies with poor fundamentals to struggle and show minimal price appreciation as recession risks pile up.

These 7 should be a fortress for investors looking to protect their wealth.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-04-26 16:02:142023-05-02 00:40:32The Fortress

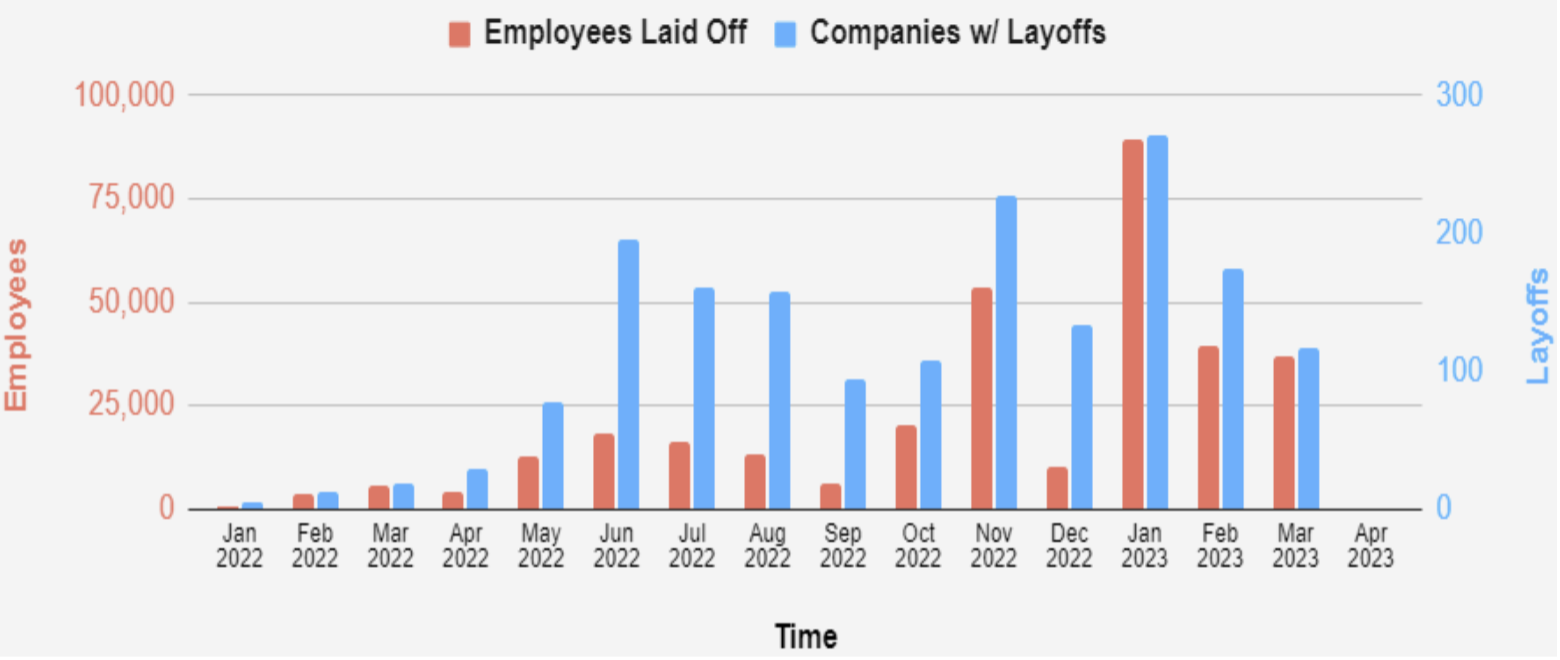

Tech workers are slowly losing their leverage in the job market that has largely been unforgiving to the average tech worker.

Part of that is due to inching closer to the much-awaited recession that everyone has been waiting for so investors can finally take advantage of 0% interest rates again.

The number breakdown shows that around 330,000 tech workers have been fired by 1,600 tech firms.

In the first month of 2023, 167,000 of those cuts occurred representing an acceleration of tech firings lately.

Some of the noteworthy cuts have been 27,000 jobs at Amazon, 12,000 at Google, and 10,000 at Meta.

Sure, the top 10% are untouchable and can work from a nuclear submarine if desired, but the average joe schmoe is living on borrowed time in the tech sector.

News of Google removing free snacks and artisanal brewed coffee from the offices in Mountain View, California struck fear into the hearts of the ultra-pampered tech worker that has never known a staff reduction in their career.

Now many tech workers who gave the middle finger to their middle manager before the lockdowns are now romanticizing how good things were before 2020.

Many tech workers now regret moving on to van life or moving to the beach of Cancun to sell donkey rides to digital nomads.

They want their old job back and specifically, they want their old pay level back.

Empirical evidence suggests that the so-called Great Resignation is now morphing into the Great Regret.

Thousands of workers began quitting their jobs in early 2021 because they didn’t “feel” empowered or appreciated by their boss. Feelings were hurt. Tears were shed.

These workers who felt jilted jumped at the chance to increase their salary during the arbitrary lockdowns because of a tight labor market.

Now, as life returns to normal, many of the perks they signed up for are being rescinded and the cost-of-living crisis is dumping fuel on the bonfire.

A third of office workers said the cost-of-living crisis had changed how they feel about their current job.

Just under a quarter said they were tired of hybrid working, mostly because they have minimal access to the higher ups they need to connect with for specific promotions.

Lack of access equates to lower positions and the obvious knock on of lower pay, lower benefits, and lower team morale.

Many are also moonlighting secretly while working full time jobs which have resulted in a big reduction in efficiency.

The once game changing pay rises now pale in comparison to the rising cost of living.

More than four in five workers admitted to keeping in touch with their former managers, with almost a third stating that this was for the primary purpose of keeping the door open for future job opportunities

Painful rounds of deep lay-offs in the tech sector and warnings of a looming recession appear to have smashed the lingering leverage workers still thought they had to crowbar a nice wage increase.

As much as 330,000 tech layoffs jump out on paper, tech firms need to fire over 1 million employees.

The fat hasn’t been trimmed to the bone yet.

The recession will approach in 2023 and this will be the optimal chance to set the record straight for employers to grab back negotiating leverage from the renegade employees while shrinking down to a leaner operation.

Tech is in great position to weather the recession and will be the first industry to over perform after the recession ends.

https://www.madhedgefundtrader.com/wp-content/uploads/2023/04/layoff.png6601560Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-04-05 17:02:292023-04-26 00:10:48Reverting Back to Normal Staffing Levels

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.