Global Market Comments

November 10, 2022

Fiat Lux

Featured Trade:

(TEN MORE TRENDS TO BET THE RANCH ON),

(AAPL), (AMZN), (GOOGL), (TSLA), (CRSP), (EDIT), (NTLA)

Global Market Comments

November 10, 2022

Fiat Lux

Featured Trade:

(TEN MORE TRENDS TO BET THE RANCH ON),

(AAPL), (AMZN), (GOOGL), (TSLA), (CRSP), (EDIT), (NTLA)

Global Market Comments

November 7, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE FED GIVETH AND THE FED TAKETH AWAY)

(SPY), (TLT), (JNK), (AAPL), (MSFT), (AMZN), (GOOGL), (META)

Now you see it, now you don’t.

The rip-roaring rally that started in October, with which we made so much money on, vaporized in a heartbeat. Traders lulled into a false sense of security with happy talk among themselves were suddenly throwing up on their shoes.

Fed governor Powell clearly indicated that interest rates will remain higher for longer, and therefore, stock prices lower. Powell promised us pain last summer and is delivering big time. Powell’s job is NOT to defend the stock market.

Personally, I’m looking for another 75 basis points on December 14, followed by 50 basis points on February 1 and another 25 basis points on March 22. This will bring us 4.75%-5.00% range for overnight Fed funds. After that, rates will fall for years as the Fed rushes to repair the damage it inflicted on the economy. Stocks will deliver the 800% return I have been promising.

I went into the Fed meeting short and used the ensuing meltdown to take profits.

As a result, my November month-to-date performance went off to the races, already achieving a hot +2.20%.

That leaves me with a very rare 100% cash position. With midterm election results out on Wednesday and the next report on the Consumer Price Index on Thursday, that sounds like a prudent place to be.

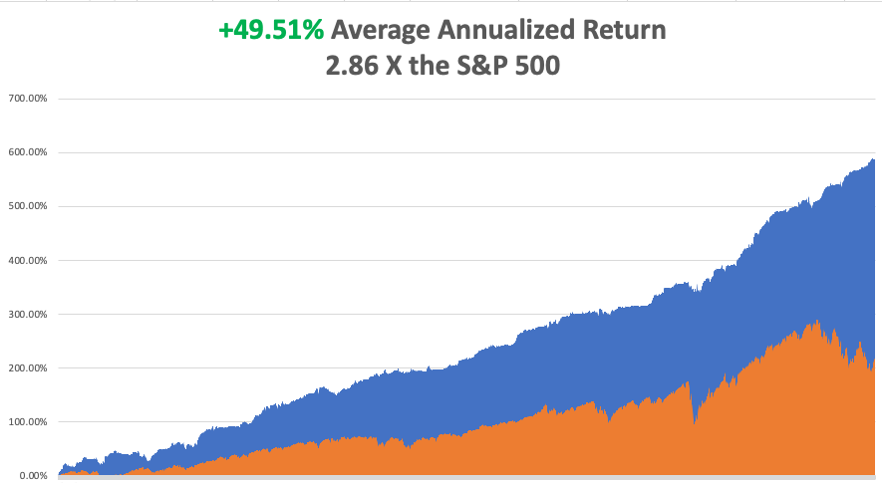

My 2022 year-to-date performance ballooned to +77.57%, a new high. The Dow Average is down -11.85% so far in 2022.

It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high +49.51%.

That brings my 14-year total return to +590.13%, some 2.86 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to +49.51%, easily the highest in the industry.

There is no doubt that the greatest buying opportunity of the century is setting up. Those who bought the Dotcom Crash bottom in 2003 snapped up Apple (AAPL) at 20 cents on its way to $186, split adjusted. During the 2009 Financial Crisis bottom, the savvy snapped up Microsoft (MSFT) at $11. Its top tick last year was $23.

A similar golden opportunity is setting up in the next year and will create immense wealth. Just remember that things always go down more than you think, and then rise far more than you believe possible.

However, one of the greatest questions of all time has finally been resolved. Can stock markets rise without big tech? The answer has been an overwhelming “YES.” Financial, where we have been very heavily involved, rose up to 25% while tech was falling 20%. Healthcare has been on fire as well. It all gives us a place to earn our crust of bread until the long-term trend up in tech resumes, however long that may take.

The turn will be called by the prospect of Fed interest rate CUTS sometime in 2023, and good luck calling that.

Further complicating matters near term is that this could be the greatest tax loss selling year of all time, with some stocks down up to 80% sold to offset gains elsewhere, such as in energy. But the mutual funds are already done, their tax year already ended. Whatever is left must be wound up by December 31.

Nonfarm Payroll Comes in at a Hot 261,000 in October, higher than hoped. The Headline Unemployment Rate crawled up to 3.7%, the highest since February. Average hourly earnings are up 4.7% YOY, far below the inflation rate. The U-6 “Discourage worker” rate rose from 6.7% to 6.8%. Anyone who thinks these numbers will lead to an earlier end to the Fed interest rate rises has a hole in their head.

JOLTS Beats Bigtime, with 10.7 million jobs opening, a million more than expected. No cooling of labor demand here.

ADP Rises 239,000, more than expected, nailing the coffin shut on the 75-basis point rate hike. The strong industries, like Airlines and Leisure & Hospitality, are still hiring like crazy.

Is Big Tech Dead Money? It may be for months, or even years, but Big Tech always comes back. It’s just a matter of how long it takes big double-digit earnings to return with the onset of the next robust economic recovery. Until then, expect a lot of differentiation. Apple (AAPL) will hold up best, followed by Amazon (AMZN) and Google (GOOGL). As for Meta (META), the old Facebook, it may never come back.

Tech Austerity Accelerates, with Apple (AAPL) announcing an unheard-of hiring freeze. The rest of big tech is following suit. The knees are about to be cut from under the market’s safest stock.

Fed Raises Interest Rates by 75 Basis Points but changed their language to be slightly more accommodative. Stocks rallied 500 points on the news. If this is bullish, it’s a stretch. They are still targeting a 2% inflation rate and will take into account cumulative tightening to date. Acknowledging they have already raised rates a lot is something. That is more dovish than expected.

Chicago PMI is Still Falling, from 47 estimated to 45.2 in October. Under 50 indicates a recessionary economy.

Morgan Stanley Says Rising Rates to End Soon, according to strategist Mike Wilson. The big pivot will happen sooner than later. I agree.

Twitter Hate Speech Spikes 500%, since Elon Musk took over the company, as racists and conspiracy theorists test his looser limits. The entire senior staff has been fired as they are still subject to fraud accusations from Musk. Musk thinks he can resell the company for a big premium in five years. Is this the end of democracy, or just Twitter (TWTR) whose stock no longer trades? More advertisers will bail after Musk paraded conspiracy theories in the wake of the Pelosi assassination attempt.

US Treasury to Borrow $550 Billion in Q4. It means the bond short (TLT) and (TBT) may have one more gasp to go.

Japan Spends $42 Billion to Support the Yen in October to no avail, as it threatens new lows. The yen will remain weak as long as interest rates remain near zero.

First Starship to Launch in December, the largest rock ever launched. The super heavy booster will return to earth while the capsule will land off the coast of Hawaii. Space X has a $3 billion contract from NASA to return to the moon by 2025.

US Banks Processed $1.2 Billion in Ransomware Payments this Year, triple the previous year’s level. Russia is the source of many of the attacks. And you wonder why we are supporting Ukraine?

Russian Economy Shrinks by 5% YOY in September as the sanctions take their toll. Only 45% to go. The call-up of 300,000 reservists has yet to hit the economy.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With the economy decarbonizing and technology hyper-accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side will be far more efficient and profitable than the old. Dow 240,000 here we come!

On Monday, November 7 at 12:00 PM, the Consumer Credit for September is released.

On Tuesday, November 8, the US Midterm elections take place with 532 House and 34 Senate seats up for grabs.

On Wednesday, November 9 the entire day will be spent analyzing election results and tracking the ties.

On Thursday, November 10 at 8:30 AM, Weekly Jobless Claims are announced. We also get the US Core Inflation Rate for October.

On Friday, November 11 at 8:30 AM the University of Michigan Consumer Sentiment for November is printed. At 2:00 PM, the Baker Hughes Oil Rig Count is out.

As for me, I was recently in Los Angeles visiting old friends, and I am reminded of one of the weirdest chapters of my life.

There were not a lot of jobs in the summer of 1971, but Thomas Noguchi, the LA County Coroner, was hiring. The famed USC student jobs board had delivered! Better yet, the job included hours at night and free housing at the coroner's department.

I got the graveyard shift, from midnight to 8:00 AM. All I had to do was buy a black suit from Robert Halls, for $25.

Noguchi was known as the “coroner to the stars” having famously done the autopsies on Marilyn Monroe and Jane Mansfield. He did not disappoint.

For three months, whenever there was a death from unnatural causes, I was there to pick up the bodies. If there was a suicide, gangland shooting, or horrific car accident, I was your man.

Charles Manson had recently been arrested and I was tasked with digging up the victims. One, cowboy stuntman Shorty Shay, had his head cut off and neatly placed in between his ankles.

The first time I ever saw a full set of women’s underclothing, a girdle, and pantyhose, was when I excavated a desert roadside grave that the coyotes had dug up. She was pretty far gone.

Once, I and another driver were sent to pick up a teenage boy who had committed suicide in Beverly Hills. The father came out and asked us to take the mattress as well. I regretted that we were not allowed to do favors on city time. He then said, “can you take it for $200”, then an astronomical sum.

A few minutes later found a hearse driving down the Santa Monica Freeway on the way to the dump with a double mattress expertly tied on the roof with Boy Scout knots with a giant blood spot in the middle.

Once, I was sent to a cheap motel where a drug deal gone wrong had produced several shootings. I found $10,000 in a brown paper bag under the bed. The other driver found another ten grand and a bag of drugs and kept them. He went to jail. I didn’t.

The worst pick-up of the summer was also the most disgusting and even made the old veterans sick. A 300-pound man had died of a heart attack and was not discovered for a month. We decided to each grab an arm or leg and all tug on the count of three. One, two, three, and all four limbs came off!

Eventually, I figured out that handling dead bodies could be hazardous to your health, so I asked for rubber gloves. I was fired.

Still, I ended up with some of the best summer job stories ever.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

November 4, 2022

Fiat Lux

Featured Trade:

(THE SILICON RESET)

(LYFT), (AMZN), (STRIPE)

This is the new Silicon Valley, where layoffs are the talk of the town!

That’s not always a good thing if you’re an employee, but at least health service jobs are still available for the newly unemployed tech workers.

Better get a move on before they run out.

The recent data backs up my biggest fears that many tech firms are getting out the machete and slicing and dicing the fat off the bone.

Staff cuts are on the menu and it’s the main dish, unfortunately.

This will be a roller-coaster ride for the ages where employees suddenly face a predicament in which they must finally prove their value to their bosses, and do it fast.

Gone are the times when Twitter workers could waltz into the front entrance 2 hours late and sit in the cafeteria all day with a cup of joe and an ice cream sandwich.

Not going to happen anymore!

Gone are the cheerleading warriors who were whole “marketing” departments acting like they market products but really doing no work at all.

Three-hour bathroom breaks are now caput.

You know who you are!

It’s finally time to get fingers out of noses.

If companies haven’t announced heart-palpitating layoffs, then they have instituted hiring, promotion, and wage hike freezes.

One company I know well from the inside is Amazon, which announced it will no longer fill certain corporate positions, while Apple said it would stop hiring in most departments.

Meanwhile, younger tech companies including payment provider Stripe and ride-hailing business Lyft (LYFT) are also slashing workforce.

They both said the decelerating economy was becoming increasingly unfavorable for tech.

Last week, Amazon released dismal third-quarter earnings showing revenue growth of 15% which was down from 37% growth a year ago.

AMZN’s stock plummeted 20% overnight, sending the company’s market value below $1 trillion for the first time since 2020.

With aggregate demand for its services falling, Amazon is looking to shrink its risk exposure.

Last week, after the poor earnings report, the company laid off around 150 people from its live radio division, and on Thursday shared with employees that it was implementing a hiring freeze for corporate retail jobs.

All eyes are on Twitter’s Musk now, who is really dishing out the new playbook for how to cut down while being most efficient and productive.

He’s even looking at cutting Twitter cloud costs by $1 billion per year at Twitter.

Musk’s management style is distinguishing him from the charlatans, and I see that as a highly positive development in corporate America long term.

Rumors of workers required to work 84 hours in a sink-or-swim scenario could be true; Musk is testing workers to see who he wants to keep.

I’ve also seen photos of workers who have resorted to taking naps on the ground in sleeping bags in Twitter’s San Francisco headquarters.

The leverage of in-person work is now over for 2023, and we most likely will see another paradigm shift in terms of work environment.

Even more important, the massive .75% rate hike and waving away any possible pauses in interbank interest hikes means that the dollar will get stronger and tech stocks will continue to be a sell-the-rally or buy-the-bear-market-rally type of deal.

Ultimately, this industry needs a reset as the supercharged growth coincided with too much bloat, which is really starting to reveal itself.

In the last few years, effectiveness definitely suffered from diminishing returns, and now that cost of capital is not free; management cannot just sling things at walls to see what sticks.

Responsible management will be the x-factor in choosing who thrives in the next tech bull market.

Global Market Comments

November 3, 2022

Fiat Lux

Featured Trade:

(LONG TERM PORTFOLIO UPDATE)

(BMY), (AMGN), (CRSP), (LLY), (EEM), (BABA),

(GOOGL), (AAPL), (AMZN), (SQ), (TBT), (JNK), (JPM),

(BAC), (MS), (GS), (FXA), (FXC), (SLV)

Mad Hedge Technology Letter

October 28, 2022

Fiat Lux

Featured Trade:

(ENTRY POINT INTO AMAZON)

(AMZN)

The bonanza is over for now at Amazon (AMZN).

“Tightening our belt” are 3 words that I never thought I would hear from a Silicon Valley tech behemoth.

Yet, that is the shocking phrase that Amazon CFO Brian Olsavsky uttered as the man behind Amazon’s numbers spoke about the firm’s immediate future.

His less-than-sanguine outlook dovetails accurately with my prognosis for this earnings season that big tech will show weakness, but far short of the earnings apocalypse many were predicting.

That is why I am executing bullish trades on the dips for the best of class in tech.

Many investors are writing off 2022 as a year to forget, and tech companies are trying to make it over the line so they can pick a new play in the huddle.

The conditions and backdrop in Silicon Valley couldn’t have been worse in 2022.

2023 is poised to be a rebound year as liquidity loosens and supply chain bottlenecks ease.

Amazon used to glide through earnings with 5 stars.

Now they are stuck with quite a few mediocre businesses.

Amazon said it expects to post fourth-quarter revenue between $140 billion and $148 billion, representing year-over-year growth of 2% to 8%. Analysts were expecting sales to come in at $155.15 billion.

Amazon growing at 2%!

Yes, you heard it here first, and how the mighty and powerful have declined.

Under current CEO, Andy Jassy, who took the helm from founder Jeff Bezos in July 2021, Amazon has responded to hyperinflationary costs by aggressively cutting expenses across large segments of the company in recent months.

It shed warehouse resources, froze many experimental projects, shelved its telehealth service, and froze hiring for corporate roles in its retail business.

Amazon CFO Brian Olsavsky said the company cut its capital expenditures budget for this year by a third after it spent heavily over the last two years on things like ramping up its fulfillment and logistics network to deal with a lockdown economy.

When Founder Jeff Bezos resigned as CEO and took a back seat, Bezos knew that Amazon was peaking in the short term. He even sold some stock at the peak to cash in.

Jassy simply has a hard task on his hands to prove that he can reignite the tech company, but to give him the benefit of the doubt, he entered into a company dipping from its peak.

One bright spot that I didn’t mention was the strength of the digital ad business – it should arrive at a $10 billion per year business in a year or 2.

In totality, there is no way I can just throw AMZN onto the scrap heap.

The 10% selloff this morning, although warranted, is a great buy-the-dip entry point in the short term or long term.

That is why I executed a bullish call spread with strike prices of $87-$92 speculating that AMZN will stay above $92 by November 18.

This trade is even more soothing when the probability of the Fed slowing down rate hikes has dramatically improved in the short-term.

Any type of behavior that is perceived as pausing the tightening of liquidity is now equivalent to a “pivot.”

Global Market Comments

September 16, 2022

Fiat Lux

Featured Trade:

(TESTIMONIAL)

(LONG-TERM ECONOMIC EFFECTS OF THE CORONAVIRUS),

(ZM), (LOGM), (AMZN), (PYPL), (SQ), CNK), (AMC), (IMAX),

(CCL), (RCL), (NCLH), (CVS), (RAD), (WMT)

The world will never be the same again.

Not only is the old world rapidly disappearing before our eyes, the new one is kicking down the front door with alarming speed.

In short: the future is happening fast, very fast.

To a large extent, long-term economic trends already in place have been given a turbocharger. Quite simply, you just take out the people. Human contact of any kind has been minimized.

I’ll tick off some of the more obvious changes.

To say that we are merely fatigued from a nearly three-year quarantine would be a vast understatement. Climbing the walls is more like it.

As I write this, US Covid-19 deaths have topped one million and cases have surpassed 95 million. China peaked at over 5,000 deaths with four times our population. The difference was leadership issue. China welded the doors shut of early Covid carriers.

Here, it said it was a big nothing and would “magically” go away.

The magic didn’t work, nor did bleach injections.

In the meantime, you better get used to your new life. You know that home office of yours you’ve been living in? It is now a permanent affair for many of you, as your employer figured out they can make more money and earn a high stock multiple with you at home.

Besides, they didn’t like you anyway.

Many employees are never coming back, preferring to avoid horrendous commutes, $5.40 a gallon gasoline, mass transit, lower costs, and yes, future pandemic viruses. GoToMeeting (LOGM) and Zoom (ZM) are now a permanent aspect of your life.

Commerce has changed beyond all recognition. Did you do a lot of shopping on Amazon (AMZN) like I do? Now, you’re really going to pour it on.

Amazon hired a staggering one million new distribution and delivery people in 2020 and 2021 to handle the surge in business, the most by any organization since WWII. I can’t believe the stock is only at $122. It is worth double that, especially if they break up the company.

The epidemic really hammered the mall, where a fatal disease is only a sneeze away. Mall REITs have since taken off like a rocket, once it was clear that the virus was coming under control.

And how are you going to pay for that transaction? Guess what one of the most efficient transmitters of disease is? That would be US dollar bills. Something like 50% of all US paper money already test positive for drugs, according to one Fed study. While in Scandinavia last summer, I learned that physical money has almost completely phased out.

Take paper money in change and you are not only getting contact from the sales clerk, but the last dozen people who handled the money. You are crazy now to take change and then not go swimming in Purell afterwards.

Personally, I leave it all as a tip.

Contactless payment deals with this nicely and is now here to stay. Next to come is simply scanning people when they walk in the store, as with some Whole Foods shops owned by Amazon.

Conferences?

They are now a luxury. All of my public speaking events around the world have been cancelled. Webinars now rule. They offer lower conversion rates but include vastly cheaper costs as well. I can reach more viewers for $1,100 a month on Zoom (ZM) than the Money Show could ever attract to the Las Vegas Mandalay Bay for $1 million.

At least I won’t have 18 hours of jet lag to deal with anymore on my Australia trips. I’m sure Qantas will miss those first-class ticket purchases and I’ll miss the free Champaign.

Entertainment is also morphing beyond all recognition. Streaming is now the order of the day. Disney+ (DIS) was probably the best-timed launch in business history, coming out just two months before the pandemic.

They earned enough to cancel out most of the losses from the closure of the theme parks. Again, this has been a long time coming and the other major movie producers will soon follow suit.

Movie theaters, which have been closed for years, may also never see their peak business again (CNK), (AMC), (IMAX). The theaters that survive will do so by only accumulating so much debt that they won’t be attractive investments for a decade.

The same is true for cruise lines (CCL), (RCL), (NCLH). But that won’t forestall dead cat bounces that are worth a double in the meantime, as they are coming off of such low levels. No vaccination, no cruise.

Exercise has changed overnight. All gyms and health clubs closed, and are only just now slowly reopening. Working out will become a solo exercise far away on a high mountain. I have already been doing this for 30 years, so piece of cake here.

Friends with yoga classes are now doing them in the living room, streaming their instructors online. The economics of online yoga classes are so compelling, with hundreds attending online classes at once. The old model may never come back.

If you are having trouble getting your kids to comply with social distancing requirements, have a family movie night and watch Gwyneth Paltrow and Cate Winslet die horrible deaths in Contagion. It has been applauded by scientists as the most accurate presentation of the kind of out-of-control pandemic we have been dealt with.

It is bone-chilling.

I hope you learned from the last pandemic because the next one may be just around the corner, thanks to globalization. In 1918, it took three months for an enhanced mutated flu virus to get from Europe to the US. This time, it took a day to get from China.

Stay healthy.