Global Market Comments

August 8, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE BOTTOM IS IN),

(AAPL), (AMZN), (GOOGL), (MSFT), (TSLA)

Global Market Comments

August 8, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE BOTTOM IS IN),

(AAPL), (AMZN), (GOOGL), (MSFT), (TSLA)

When the train conductor says “Run”, it’s generally not a good sign.

That’s what happened to me when I had to make a crucial transfer in Visp, Switzerland last month. I’m fine with running. With 200 pounds of luggage? Not so much.

A lot of fund managers started running from their cash positions last week. Tesla (TSLA) shorts ran even faster.

There is a rising sense of panic among money managers today.

The stock market just brought in a blockbuster 7.9% return in July, and they are underweight stocks and loaded with cash. What they DO own are in all the wrong defensive sectors.

A panic is imminent.

A soft landing for the economy is in the cards. There are still plenty of risks out there, as there always are. But bond yields have collapsed, commodity and energy prices are in free fall, and the futures markets are indicating that interest rate hikes ahead will be modest at best.

The Fed is also getting an assist in its tightening efforts from a strong dollar, which pares U.S. multinational earnings, and a recessionary China and Europe. Those two alone are the equivalent of another 100 basis points in rate rises.

The Fed’s work has already been done for it.

The Fed’s Quantitative Tightening is also sucking $120 million a month out of the economy.

The bond vigilantes who were riding hard in the first half have gone to sleep, or at least gone on vacation. That has dropped ten-year US Treasury yields by an amazing 100 basis points in seven weeks. That doesn’t seem to warrant an over-aggressive Fed to me.

Remember also that interest rates no longer have the impact on the economy they once had. The stock of every company I buy has no net debt and are in fact huge net creditors, like Apple (AAPL), Amazon (AMZN), Alphabet (GOOGL), and Microsoft (MSFT).

Those that have refinanced their debts at 150-year lows over the last three years, including myself (30-year fixed rate mortgage at 2.75%, some 6.35% under the current inflation rate!).

No credit crunch here, or distressed financial institutions, the fodder of past recessions.

Sure, earnings have come down. But they are being shaved, not decimated. Again, the companies I buy aren’t growing at a modest 5%-10%, but more like 40%-50%, like Tesla (TSLA). Slow growing companies are other peoples’ problems, not mine.

Better yet, they are likely to bounce back hard next year, which is what the market is discounting now.

I’m buying next year’s market, while everyone else is still selling this year’s.

The bottom line is that the U.S. has the strongest economy and currency in the world, making its stocks deserving of a serious premium. Add up rate rises, QT, a strong greenback, a recessionary world, the largest deficit reduction in history, war, and stocks STILL can’t go down.

It's an old trader’s nostrum that if you dump bad news on a market and it fails to go down, you buy the heck out of it. This is one of those times.

That makes my yearend forecast of an S&P 500 of 4,800 by year-end not only possible but likely. Buy every substantial dip in every one of your favorite stocks from here on out. You might be risking 10%-20% over the short term but gain 100% on a three-year view.

The risk/reward is overwhelmingly in your favor.

I hope this helps.

July Nonfarm Payroll Hits a Blockbuster 528,000, double expectations, the best since February. The Headline Unemployment rate fell to 3.5%, a new post pandemic low. No recession here. Average hourly earnings popped 0.5%. The Dow dropped $250 as possible scenarios were already discounted in the market in a classic “Buy the rumor, sell the news” move. Bond yields soared. The difficulty in finding workers is overwhelming recession fears. Hotels and restaurants created enormous numbers of jobs. The Fed now has a license to maintain aggressive interest rate rises. My bond short in the (TLT) is looking good.

Weekly Jobless Claims hit 260,000, an 8-month high, as recession fears fan the flames. That beats the 1 million figure we saw at the pandemic high two years ago. Layoffs are falling. That makes tomorrows July Nonfarm Payroll Report more important than usual.

Fed Says More Rate Hikes Coming but No Recession, says St Louis Fed president James Bullard. I couldn’t agree more. If inflation dips look for only a 50-basis point rate hike in September. Stocks will soar.

England Predicts Major Recession after hiking interest rates by 0.50% to 1.75%. The Bank of England expects inflation to peak at 13.3%. Europe economy is in the toilet and China is weak. It all highlights how America now has the strongest economy in the world and is therefore the first choice for equity investors.

Weak Chinese Data Torpedoes Oil, down 34% from its February peak. Oil is now lower than when the Ukraine War started. Manufacturing PMI dropped from 51.7 to 50.4, barely outside recessionary data. New Chinese Covid shutdowns are the cause. Could this recession go global?

Home Prices fall at a Record Pace, down from a 19.3% annual gain to 17.3% in June, according to Black Knight, a mortgage analytics firm. Some 25% of major U.S. markets saw growth slow by three percentage points in June. It’s all about interest rates.

Mortgage Rates Drop Below 5%, for the 30-year fixed, a four-month low. It’s putting a floor under the housing market. Refi’s are still near zero. The collapse in bond yields is feeding through.

Half of U.S. Homes are Equity Rich, indicating homeowner equity is more than 50% of market value. That makes available trillions of dollars in potential second mortgages to support the economy. Americans are richer than they think.

Tesla Voted to Split Shares. The 3:1 split will make the shares more affordable for lower-end (poorer) investors who want to make the millions we have for the past decade. Watch for a spike in the price as share splits always attract a hoard of short-term meme investors. The last 5:1 split in 2020 brought an eye-popping near doubling of the shares in six months

ISM Non-Manufacturing Gains 2%, in June where tech lives. It shows that our “recessionary” economy may be stronger than you think, especially in the right sectors. No wonder stocks are going up every day.

Carried Interest Lives Again, with Arizona’s Kristin Sinema stopping the abolishment of tax-free treatment of hedge funds and private equity funds as her pound of flesh for backing Biden’s stimulus bill. People have been trying to end carried interest since President Carter pushed it through in 1979 to jump-start venture capital and Silicon Valley. It truly demonstrates the power of lobbying and will lead to more concentration of wealth at the top. Look for a vote next week.

My Ten-Year View

When we come out the other side of pandemic and the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With oil peaking out soon, and technology hyper accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side will be far more efficient and profitable than the old. Dow 240,000 here we come!

With some of the greatest market volatility in market history, my August month-to-date performance reached +0.46%.

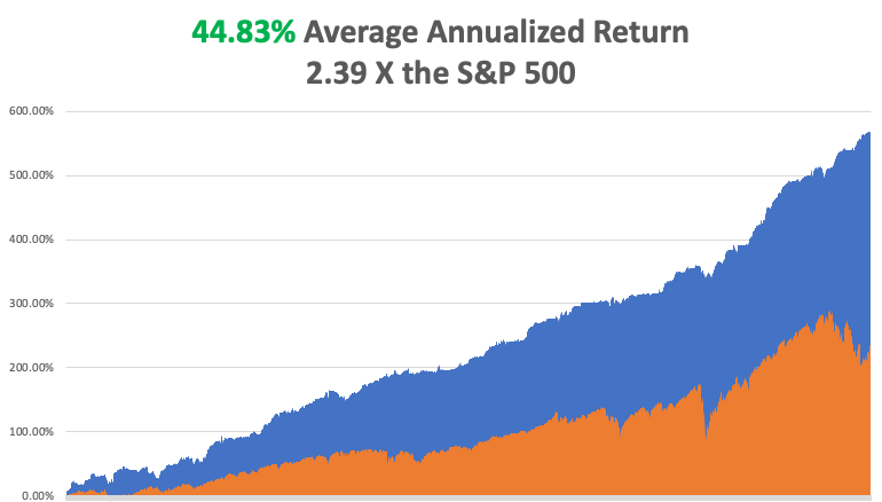

My 2022 year-to-date performance expanded to 55.29%, a new high. The Dow Average is down -9.64% so far in 2022. It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high 74.73%.

That brings my 14-year total return to 567.85%, some 2.39 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to 44.83%, easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 91 million, up 300,000 in a week, and deaths topping 1,033,000 and have only increased by 2,000 in the past week. You can find the data here at https://coronavirus.jhu.edu.

On Monday, August 8, there is no data of note.

On Tuesday, August 9 at 8:30 AM, the NFIB Business Optimism Index for July is out.

On Wednesday, August 10 at 8:30 AM, the CPI Index for July is published.

On Thursday, August 11 at 8:30 AM, Weekly Jobless Claims are announced. The Producer Price Index for August is printed.

On Friday, August 12 at 7:00 AM, the University of Michigan Consumer Sentiment Index is disclosed. At 2:00 the Baker Hughes Oil Rig Count is out.

As for me, I had the good fortune to live with a Nazi family in West Berlin during the 1960s. While working at the Sarotti chocolate factory in Templehof, my boss took pity on me and invited me to move in with his family. I jumped at the chance of free rent and all the German food I could eat.

What I learned was amazing.

Even though the Germans had lost WWII 20 years earlier, they still believed in the core Nazi beliefs. However, they loved Americans as we had saved them from the Bolsheviks, especially in Berlin. President Kennedy had delivered his famous “Ich bin ein Berliner” speech only seven years earlier.

There have been thousands of books written about wartime Germany, but almost none about what happened afterwards. I absorbed dozens of stories from my adopted German family, and I’ll tell you one of the most unbelievable ones.

In the weeks after the German surrender on May 7, 1945, Berlin was shattered. The city had been the subject of countless 1,000 bomber raids and the population had shrunk from 5 million to only 1.5 million. Most of the military-aged men were absent. Survivors were living under the rubble.

What’s worse, everyone knew that the allies would soon declare the German currency, the Reichsmark, worthless and replace it with a new one, wiping out everyone’s life savings. So, they had to spend as fast as they could. But with the economy in ruins, there was nothing to buy. In any case, the only thing they really wanted was food, which they could get on a thriving black market.

It turned out that there was only one thing they could buy in unlimited quantities:

Movie tickets.

When Hitler came to power in 1933, one of the first things he did was ban American movies. The industry was taken over by propaganda minister Joseph Goebbels who only permitted propaganda films promoting Nazi values for domestic consumption.

The only American film permitted in Germany during the 1930s was Grapes of Wrath because it highlighted U.S. weaknesses. Movie production was shut down completely in 1943 because of the war’s demands on supplies.

When the war ended, suddenly, the iconic movies of the Great Depression became available, such as the works of the Marx Brothers, Shirley Temple, The Wizard of Oz, Gone with the Wind, and King Kong.

Impromptu movie theaters were thrown up against standing walls of destroyed buildings. Within two weeks of the surrender, half of Berlin’s prewar 550 theaters had reopened. Of a population of 1.5 million, 850,000 movie tickets were sold every weekend. The summer of 1945 became one long film festival. The Germans laughed, cried, and were enthralled.

Every weekend was a sellout. The only movie that bombed that summer was a U.S. Army documentary about the concentration camps. But even that one sold 400,000 tickets.

The movies had a therapeutic effect on the German people. It distracted them from their daily privations, starvation, and suffering. It also allowed them to reconnect with western civilization. Ask any Berliner about what they did after the war and all they will talk about are the movies.

The allies finally did withdraw the Reichsmark in 1948. Individuals were only permitted to convert $40 out of the old currency into the new Deutschmark, which was then worth 25 cents. Only those who had title to land maintained their wealth, and most of those were farmers in the new West Germany.

I hope you enjoyed this little fragment of unwritten history, which I find amazing. But then, I find everything amazing.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Berlin in 1945

Berlin in 1968

Mad Hedge Technology Letter

August 3, 2022

Fiat Lux

Featured Trade:

(LOSING ITS MOJO)

(NFLX), (AMZN)

The reversion to the mean crowd who like to do no research and just buy certain shares when they go down anticipating a quick rebound needs to avoid former streaming darling Netflix (NFLX).

The company has gone from bad to worse and like your black sheep little brother who loves to play the victim, avoid at all costs!

NFLX has parlayed deteriorating content with an even worse future game plan that screams subscriber bleeding.

The headwinds are adding up to something that will be insurmountable quite soon and I don’t believe that has been accurately reflected in the stock price yet.

Let’s take the running of their clean brand.

They are damaging the brand by integrating it with a lower-cost, ad-supported tier in early 2023. This comes on the heels of Netflix tapping Microsoft to be its partner on the ad-supported offering.

For many years, NFLX was adamant they would never go this route only to do an about-face.

Already losing subscribers, inserting ads to only muddy the content further won’t move the needle in terms of improving the quickly eroding content quality.

Like on a sinking ship, they are trying to chug as many whiskey bottles as possible before the ship goes underwater.

Netflix had warned investors last quarter that it expected to shed around 2 million subscribers but only lost around 970,000 during the three-month period ending June 30.

This artsy game of claiming a pyrrhic victory because the subscriber loss was only around a million and not 2 is insane.

A million subscribers lost is detrimental to any subscriber-based company in any sphere of business.

And remember, NFLX is supposed to be the preeminent growth company, yes, the one that is losing 1 million subscribers every 3 months.

Let’s rate the business model today.

Will the median consumer bite at a monthly NFLX subscription?

In the current market environment, which is characterized by inflation, consumers alter spending. In concrete terms, this means that consumers are concentrating on fewer streaming services.

Also, an NFLX content archive that is shrinkflating doesn’t help and I am not talking in terms of volume.

They no longer have access to the hit shows of old like Friends or Seinfeld that many Millennial viewers love to watch because other streaming platforms have recalled that content.

Times are lean to the bone for NFLX these days.

What we have today is a streaming service that can’t make in-house blockbusters apart from Stranger Things and after that, the kitchen is barren.

Weirdly enough, NFLX executives have turned to anime as if it’s a broad solution to the content woes.

I’ll give you a hint - it’s not.

Stealing content ideas from their 14-year-old daughter won’t hack it in this climate.

Even worse, they are taking classic anime titles from Japan and Americanizing them.

This type of Frankenstein anime is hard to watch.

The conclusion of Stranger Things Season 4 is peak NFLX for 2022 as pitiful as that sounds.

The search for content has really gone into full drive with Amazon (AMZN) picking up France Ligue 1 soccer league rights for $250 million per year on a 3-year contract.

Things have moved on a lot in the content world with American tech companies scouring the world for quality content while NFLX has been stuck in neutral.

The stock has gone from $700 to $200, and the poor executive decisions today mixed with inferior content means that they will underperform any tech rally that is manufactured to end the year.

Global Market Comments

August 2, 2022

Fiat Lux

Featured Trade:

(AN INSIDER’S GUIDE TO THE NEXT DECADE OF TECH INVESTMENT),

(AMZN), (AAPL), (NFLX), (AMD), (INTC), (TSLA), (GOOG), (META)

Last weekend, I had dinner with one of the oldest and best-performing technology managers in Silicon Valley. We met at a small out-of-the-way restaurant in Oakland near Jack London Square so no one would recognize us. It was blessed with a very wide sidewalk out front and plenty of patio tables.

The service was poor and the food indifferent, as are most dining experiences these days. I ordered via a QR code menu and paid with a touchless Square swipe.

I wanted to glean from my friend the names of the best tech stocks to own for the long term right now, the kind you can pick up and forget about for a decade or more, a “lose behind the radiator” portfolio.

To get this information, I had to promise the utmost confidentiality. If I mentioned his name, you would say “oh my gosh!”

Amazon (AMZN) is now his largest holding, the current leader in cloud computing. Only 5% of the world’s workload is on the cloud presently so we are still in the early innings of a hyper-growth phase there.

By the time you price in all the transportation, labor, and warehousing costs, Amazon breaks even with its online retail business at best. The mistake people make is only focusing on this lowest of margin businesses.

It’s everything else that’s so interesting. While its profitability is quite low compared to the other FANG stocks, Amazon has the best growth outlook. For a start, third-party products hosted on the Amazon site, most of what Amazon sells, offer hefty 30% margins.

Amazon Web Services (AWS) has grown from a money loser to a huge earner in just four years. It’s a productivity improvement machine for the world’s cloud infrastructure where they pass all cost increases on to the customer who, once in, buy more services.

Apple (AAPL) is his second holding. The company is in transition now justifying a massive increase in earnings multiples, from 9X to 25X. The iPhone has become an indispensable device for people around the world, and it is the services sold through the phone that are key.

The iPhone is really not a communications device but a selling device, be it for apps, storage, music, or third-party services. The cream on top is that Apple is at the very beginning of an enormous replacement cycle for its installed base of over one billion phones. Moving from upfront sales to a lifetime subscription model will also give it a boost.

Half of these are more than four years old, and positively geriatric in the tech world. More than half of these are outside the US. 5G has added a turbocharger.

Netflix (NFLX) is another favorite. The world is moving to “over the top” content delivery and Netflix is already spending twice as much on content as any other company in this area. This is why the company won an amazing 44 Emmys last year. This will become a much more profitable company as it grows its subscriber base and amortizes its content costs. Their cash flow is growing by leaps and bounds, which they can use to buy back stock or pay a dividend.

Generally speaking, there is no doubt that the pandemic has pulled forward some future technology demand with the stay-at-home trend. But these companies have delivered normal growth in a hard world.

5G has enabled better Internet coverage for everyone and increased the competitiveness of the telecom companies. Factory automation has been another big area for 5G, as it is reliable and secure, and can be integrated with artificial intelligence.

Transportation will benefit greatly. Connected self-driving cars will be a big deal, improving safety and the quality of life.

My friend is not as worried about government-threatened break-ups as regulation. There will be more restraints on what these companies can do going forward. Europe, which has no big tech companies of its own, views big American tech companies simply as a source of revenue through fines. Driving companies out of business through cutthroat competition is simply not something Europeans believe in.

Google (GOOG) is probably more subject to antitrust proceedings both in Europe and the US. The founders have both retired to pursue philanthropic activities, so you no longer have the old passion (“don’t be evil”).

Both Google and Meta (META) control 70% of the advertising market between them, which is inherently a slow-growing market, expanding at 5% a year at best. (META)’s growth has slowed dramatically, while it has reversed at (GOOG).

He is a big fan of (AMD), one of his biggest positions, which is undervalued relative to the other chip companies. They out-executed Intel (INTC) over the last five years and should pass it over the next five years.

He has raised value tech stocks from 15% to 30% of his portfolio. Apple used to be one of these. Semiconductor companies today also fall into this category. Samsung with 40% margins in its memory business is a good example. Selling for 10X earnings is ridiculously cheap. It is just a matter of time before semiconductors get rerated too.

He was an early owner of Tesla (TSLA) back in the nail-biting days when it was constantly running out of cash. Now they have the opposite problem, using their easy access to cash through new share issues as a weapon to fight off the other EV startups. Tesla is doing to Detroit what Apple did to the cell phone companies, redefining the car.

Its stock is overvalued now but will become much more profitable than people realize. They also are starting to extract services revenues from their cars, like Apple has. Tesla will grow revenues by 30%-50% a year for the next two or three years. They should sell several millions of the new small SUV Model Y. Most other companies bringing EVs will fall on their faces.

EVs are a big factor in climate change, even in China, the world’s biggest polluter. In Europe, they are legislating gasoline cars out of existence. If you can make money building cars in Fremont, CA, you can make a fortune building them in China.

Tech valuations are high, there is no doubt about it. But interest rates are much lower by comparison. The Fed is forcing people to buy stocks, enabling these companies to evolve even faster.

Tech stocks have a lot more things going for them than against them. The customers keep coming back for more.

Needless to say, the above stocks should make up your short list for LEAPS to buy at the coming market bottom.

Mad Hedge Bitcoin Letter

July 28, 2022

Fiat Lux

Featured Trade:

(ANOTHER 130 MILLION)

(BTC), (AMZN), (MSFT), (GOOGL)

Mad Hedge Technology Letter

July 27, 2022

Fiat Lux

Featured Trade:

(STITCHED UP BY ITS OWN POOR DECISIONS)

(SFIX), (AMZN)

Mad Hedge Biotech and Healthcare Letter

July 26, 2022

Fiat Lux

Featured Trade:

(ANOTHER TECH AND HEALTHCARE CROSSOVER)

(ONEM), (AMZN), (TDOC), (AMWL), (GOOGL), (AAPL), (MSFT), (CVS), (WBA), (UNH)

The battle for telemedicine dominance might have just ended before it even began.

Amazon (AMZN) just announced its all-cash plan to acquire One Medical (ONEM) for $3.9 billion, paying $18 per share.

To date, this will be Amazon’s biggest step toward the healthcare world.

With the entry of Amazon into this telehealth segment, companies like Teladoc (TDOC) and Amwell (AMWL) would need to work overtime to match the resources of the e-commerce giant.

However, Amazon’s move isn’t exactly novel considering that other FAANG companies like Google (GOOGL), Apple (AAPL), and Microsoft (MSFT) have already acquired healthcare companies.

What this move simply indicates is that Amazon has finally turned serious in its bid for a bigger piece of the healthcare market.

This isn’t even the first time Amazon decided to go beyond its retail business. It has a pretty diverse portfolio including Amazon Web Services, a cloud infrastructure service, and even Whole Foods.

However, the decision to aggressively pursue the $800 billion healthcare industry might just be what Amazon needs to really move the needle.

In 2018, Amazon shelled out roughly $1 billion to buy an online pharmacy called PillPack which led to the launch of virtual Amazon Care clinics.

On that same year, the e-commerce company also pursued a joint venture, dubbed Haven, with Berkshire Hathaway and JPMorgan Chase. Unfortunately, that plan didn’t pan out and was eventually shut down.

Buying One Medical at a premium of 77%, Amazon beat other interested bidders including CVS (CVS), Walgreens (WBA), and UnitedHealth (UNH).

It’s still unclear what Amazon plans with One Medical. The e-commerce giant might add it to its Amazon Care brand or let it operate independently.

One Medical is a membership-based platform, which is backed by the Carlyle Group (CG) and managed under 1Life Healthcare.

Like most telehealth companies, it offers virtual healthcare services like virtual visits. What makes it different is that it also provides in-person checkups in accredited medical offices within the US.

One Medical’s app enables clients to schedule appointments, talk with their healthcare provider, and ask for prescriptions.

A key selling point is that the company guarantees that all the appointments start on time. Another notable feature is that users can gift a yearlong subscription to someone for $199.

Like Teladoc and Amwell, the company isn’t profitable yet. This case isn’t shocking for a relatively new field.

However, One Medical’s strategy has led to impressive revenue and membership growth.

The company’s revenue has consistently increased since its 2020 IPO. In 2021, its membership count climbed by 34% to reach 736,000.

In the first quarter of 2022, One Medical’s membership grew again by 28% and revenue jumped 109% to record over $254 million. So far, more than 8,000 companies provide One Medical services to their staff.

For 2022, One Medical projects its revenue to be between $831 million and $853 million.

Admittedly, these figures seem inconsequential when you compare them to the other sectors of Amazon’s business. For example, Amazon Web Services raked in $18.4 billion in sales in the first quarter of 2022.

Actually, One Medical’s revenue and membership growth might even look small and unimpressive compared to Teladoc, which recorded $565 million in the first quarter and has more than 54 million members in the US alone.

Undoubtedly, the healthcare market offers a mouthwatering opportunity for the likes of Amazon. It’s a lucrative industry, one of the handful that can truly make a difference in an already thriving business. Moreover, it has been highly profitable over the years.

Nonetheless, the acquisition of One Medical isn’t a foolproof plan for Amazon’s dominance in healthcare. So far, the e-commerce giant’s track record has been mixed. That doesn’t mean that the deal is a bad move. In fact, it indicates Amazon’s seriousness in making a play for the healthcare market.

Either way, the clear winner would be One Medical. Since the announcement, the stock has risen 70%.

Moreover, even if Amazon falls victim to politicization or anti-trust issues involving the deal, One Medical still has a number of suitors lined up.

Basically, it’s a win-win for this emerging telehealth company.