Mad Hedge Technology Letter

May 23, 2022

Fiat Lux

Featured Trade:

(ONSHORING GETS CLOSER)

(AAPL), (AMZN)

Mad Hedge Technology Letter

May 23, 2022

Fiat Lux

Featured Trade:

(ONSHORING GETS CLOSER)

(AAPL), (AMZN)

The end of globalization is accelerating as the iPhone company, Apple (AAPL), has indicated to close sources that they no longer wish to manufacture products in mainland China.

If many might remember, it was Apple CEO Tim Cook who often visited China for a victory lap while simultaneously keeping his mouth shut about the atrocities occurring in the Muslim region of China.

Not only that, zero covid policy in China has served as a political stage for something that appears much more insidious brewing in the Middle Kingdom.

Cook and many other multinational CEOs, selling out their own country, might have finally realized that doing business in totalitarian countries is a bad idea.

Starbucks even shut down in Russia.

There are network costs and brand damage that are hard to recover from.

Truth be told, Apple laughed all the way to the bank with this China arrangement, and their stock price is an indication the strategy worked like clockwork.

Well, it works until it doesn’t.

China was also a great place to live, until it’s not.

Also, China was a great place to manufacture cheap products, until it’s not.

That’s what happens in a country that presides over arbitrary laws which in fact means that the country has no laws.

Now Chinese residents are locked up with robot police dogs barking out orders to stay inside from the street.

What does this mean for Apple’s stock?

Short-term lower if interest rates continue to rise, but very positive long term.

Also, Apple’s equipment might not secure a proper “exit visa.” We also left our military equipment in Afghanistan too.

At least Tim Cook wasn’t locked inside an Apple factory in China like some American CEOs in the past.

At a product level, Apple phones will become more expensive because Apple won’t be able to ignore worker rights and pay them peanuts in producing these shiny gadgets.

Materials will also be harder to source in large quantities.

Remember, China has access to nickel and cobalt.

If they are able to produce in a poorer country like Cambodia, there are transitional costs along with slippage costs.

China’s Foxconn and Pegatron facilities will suffer the fate of many other trade war pawns and I believe this is the end of offshoring for America inc.

Here's another idea, get Foxconn to build an Apple factory in Phoenix and deliver work visas to the best Chinese workers.

Tell them they don’t even need to sleep on the factory floor and don’t need to work 14-hour shifts too. They would take the next plane to the desert.

Apple production partners like Foxconn have already established facilities in India to help produce iPhones for the domestic market there. A further expansion would see iPhones made in India and then exported for global sale.

However, is India sustainable as well? They banned wheat exports to the chagrin of the American government and even worse, they refused to ban Russian energy.

India’s behavior suggests they are working for themselves and not for Ukraine which can be perceived in many coastal American cities as undemocratic.

Either way, Apple’s stock is around 22% from its highs and that’s a victory when we consider stocks like Amazon (AMZN) are down around 45%.

Even if Apple’s stock sustains 30% losses at the time the US Fed starts to lower rates, possibly in 2023, then I would also consider that a resounding success.

Long term, manufacturing in America makes sense not only politically, but economically.

Automation is getting that good too which will soften the blow.

Apple does $365 billion in sales and the natural growth rates suggest it will break half a trillion in sales in 3 years.

However, if Apple wants to do $1 trillion of annual sales, they are going to have to produce the literal iPad on wheels, the Apple EV.

If Apple can pull off an Apple EV while maintaining the high level of quality they are known for, they are guaranteed to clock $1 trillion per year in sales no questions asked meaning the stock should go to $300 per share.

Global Market Comments

May 20, 2022

Fiat Lux

Featured Trade:

(MAY 18 BIWEEKLY STRATEGY WEBINAR Q&A),

(C), (FXI), (BABA), (TSLA), (AAPL), (AMZN), (TGT), (FLR), (QQQ),

(FB), (ARKK), (TSLA), (WYNN), (UAL), (ALK), (DAL)

Below please find subscribers’ Q&A for the May 18 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley.

Q: When do you see the banks returning to glory?

A: When recession fears go away, which should happen this summer. A recession will either have come and gone, or we will have confirmation by the end of summer that there is no recession in sight for the next few years at least. This will likely trigger a monster rally in the banks, which could all jump 50% from here. Obviously, Warren Buffet is putting his money where his mouth is by loading up on Citibank (C) yesterday. This would take us to new all-time highs by the end of the year. So, again, use these down-1000-point days to go cherry-picking among the generals who have been executed. If that’s not mixing metaphors, I don’t know what is!

Q: Should I listen to CNBC?

A: No, do not listen to the talking heads on TV. They are on TV because they don’t know how to make money. If they did know how to make money, they’d be locked up in a dark basement somewhere like me, grinding out millions for their firms. In fact, watching TV is the perfect money destruction machine because on down days, they bring out the uber bears, and on up days they bring up the hyper bulls. They are trying to egg you to get you to do the exact opposite of what you should be doing. They’re not interested in you making money; they’re interested in getting traffic on their websites and making money for themselves. CNBC can be highly dangerous to your financial health.

Q: Will we get stagflation?

A: No, because I think that once the year-on-year comparisons kick in—literally in a month or two—inflation will drop from the current 8.3% to down maybe 4% by the end of the year. That also is another factor in your monster second-half rally.

Q: Do you think the bounce in the market yesterday is the beginning of an upward trend or a dead cat bounce?

A: Definitely a dead cat bounce. I expect we’ll keep chopping around in the current range for the next 3, 4, and 5 months, and then we catapult into a monster year-end rally. That is a typical bottoming-type process.

Q: Is the wisdom “Go away in May” still alive or is your best bet that this year may prove different and the market goes up in the latter part of the year?

A: Actually, you should have gone away in November. That’s when all tech stocks peaked; only energy went up after that. If you’d gone away in November and said “come back in August” that would have been a good strategy because I think that’s when the year-end rally begins. If anything, May could be the bottom of the entire move.

Q: Is it time for LEAPS (Long Term Equity Anticipation Securities)?

A: Not yet—it’s too soon for LEAPS territory. You only want to do LEAPS when you are on a sustained long-term uptrend in a stock. We are nowhere near sustained anything, we are still in a bottoming phase, and could be there for months. At the end of those months is when we’ll be looking at LEAPS, where you can double your money every 6 months.

Q: Is it time to start nibbling on China stocks (FXI) now that COVID news is marginally better?

A: I’m going to avoid Chinese stocks because the American ones are so much better. You want to buy the quality at the discount, not the marginal, high-risk political footballs at a discount. And China will remain high-risk as long as they are abandoning capitalism. If you have to buy one Chinese stock, I would say Alibaba (BABA); you could get a double on that. But remember it is a high-risk trade—if the Chinese government wants to roll Jack Ma up in a carpet and kidnap him to Western Chinese re-education camp, the stock will get slaughtered. And that’s been happening increasingly with the heads of major companies in the Middle Kingdom.

Q: When this current route comes to an end, should we look to enter the market with 50% margin on stocks like Tesla (TSLA)?

A: It’s never sensible to go to 50% margin because if the stocks drop 50%, you are completely wiped out—you’ve lost everything. Plus, coming back from a loss is one thing; coming back from zero is impossible. So, I would not recommend that. You might do a safe stock like Apple (APPL), with a 2% dividend, and then at least you’re getting a double dividend. You only do the 50% margin on the safest, high dividend stocks.

Q: Amazon (AMZN) is on its way down. What is your expectation for the $3200/$3400 vertical bull call spread in January 2023?

A: I think you could make money on that. It may not be the full amount of the spread, but you’ll definitely get a big increase from current levels, because when we do get a second half rally, it will be tech-led, and Amazon has already had a horrific decline. What you might consider is rolling your strike down, taking the loss on the 3200/3400 and rolling down to like a $2,000/$2,200 in twice the size, and you’ll make your money back that way.

Q: For those of us thinking about LEAPS, how should we start to buy in—20, 30, 50% right now?

A: Well, first of all, you only do them on down days like today, when the market is down 800, and you scale in. 20% now, 20% higher or lower, and 20% again higher or lower. But you really want to be saving cash for days like this because You want to feel smarter than everybody else, and they absolutely will hit any bid on a down day, and that's where your LEAPS fills are really excellent, is on a down day like this.

Q: Can the Fed avoid another policy mistake? Because it seems that not only are they heading for high inflation, but layoffs are coming as well, and even with that I’m sure they will perform a soft landing of sorts.

A: For sure, when you take massive amounts of stimulus out of the economy, as we have in the last year, that is recessionary. In fact, the US government is close to running a balance budget right now because Biden can’t get anything through Congress other than money for Ukraine. Good for Ukraine economy, not for ours. And yes, they can do a soft landing, but has it ever been done before? No. Though this is the Fed that just keeps on surprising, so who knows. In the meantime, I'm willing to trade the ranges, and that may be all you get to do for a while.

Q: Target (TGT) shares are down 25%, as they cited higher costs that will result in rising prices for their customers. Would you buy the dip?

A: No, I generally don’t like retailers anyway. It’s a business that operates on a 2% profit margin. I like 40 or 50% profit margin businesses—those tend to be technology stocks.

Q: Would you buy retailers going into a recession?

A: No, that’s the worst thing in the world to own.

Q: Could Fluor Corp (FLR) be a Ukraine infrastructure stock?

A: Yes, once the war ends there will be a massive effort to rebuild Ukraine. Every company in the world will be involved, and Fluor and Bechtel will be the biggest, though Fluor is the only one where you can buy the stock. We already have the money to do this with all of the money that was seized from Russia. I predict discount sales on mega yachts.

Q: Why do you think all that money is going to Ukraine?

A: Because a weakened Russia is in the national interest of the United States, and it’s better that their soldiers are doing the dying than ours. I’ve done the latter and definitely prefer the former, using the other country's’soldiers as cannon fodder.

Q: On down days like today, should I be putting on one-month trades like the June options?

A: Yes, because the minimizes your risk and cuts the cost of mistakes. Waiting for the second half of the year when we get a prolonged uptrend to look at LEAPS—that is the correct way to do it.

Q: Over the next 12 months, do you think the S&P 500 will outperform Nasdaq?

A: No—for the next 3 months the S&P 500 will outperform NASDAQ. After that, NASDAQ will become an enormous outperformer for the rest of the decade. So, choose your entry points wisely.

Q: Do you think that housing is peaking out and will start to decline?

A: No, we still have a long-term structural shortage of 10 million homes in the US and I think we will flatline housing for years until we catch up with that shortfall.

Q: What are your thoughts on the Metaverse?

A: Too soon. Right now, the Metaverse involves spending only—no revenues. It could be years before you actually see any profits. So that’s why I'm avoiding Meta or Facebook (FB). But then, you could have made the same argument about the internet 25 years ago and semiconductors 50 years ago. If you waited long enough, however, you obviously made a fortune.

Q: China is hoarding 69% of their wheat reserves. Is this because they plan to invade Taiwan?

A: No, it’s because there’s a global food crisis going on. Many countries, like India, have banned exports of food to protect themselves. People miss this about China: China will never have a war or invade anybody, because the second they do, their food supplies get cut off by us, who are the world’s largest producer of food. Plus, their trade would get shut off to pay for it, so they can’t buy it from somewhere else, and that’s done with us also. So, they need to be in our good graces in order to eat. That's the bottom line and that’s why Taiwan will never get invaded. Russia’s economy can operate independently for a while, but China’s can’t.

Q: Is the baby food shortage further evidence of a food crisis?

A: No, the baby formula crisis is being caused by a monopoly of three companies that control 100% of the baby food market; and the largest of these companies, accounting for a 40% market share of the baby food making, is producing baby food that is poisonous. That's why they got shut down. This has been going on for years, and for some reason, they got a free pass on regulation and inspections by the previous administration, which is ending now, and all of a sudden we’re finding out that 40% of the country’s baby food is contaminated and is being pulled off the market. So, it really has nothing to do with the global food crisis. That’s more related to Climate change—surprise, surprise—as it’s not raining in the right places like California, the war in Ukraine, which removed 13% of the world’s calories practically overnight.

Q: Should I bet the farm here with the ARK Innovation Fund (ARKK)? I like Cathie Woods’ bet on innovation or five-year time horizon. It’s a great thing, don’t you think?

A: Not so great when you drop 70% in the last year. And it is a high-risk bet that of her ten largest holding companies, you only need one of them to work for the fund to bring in a decent return. Of course, you may have to write off nine other companies to do that. But yes, it’s a great thing to own on the way up, not so great on the way down. I know some people who started scaling into ARK in November and came to regret it. I would wait on it—this is your highest leverage technology play, and if you really want some punishment, there’s a hedge fund that’s bringing out a 2X long ARK fund in the next couple of months. Then it’s basically option money you’re throwing out. If you want to put some money in that, you could get a 10x on the 2x ETF if you’re playing a recovery in ARK. So watch it; don’t touch it now because ARK is having another heart attack today, but something to consider if you like gambling.

Q: I am full up with a thousand shares of PayPal (PYPL). It’s now down 76%. What should I do?

A: I recommend you learn the art of stop losses. I stopped out of this thing last fall, and it’s continued to go down virtually every day. Whenever you buy a new position, automatically enter into your spreadsheet your stop loss for that position. Because things can drop by 80 or 90% and you work too hard for your money to throw it away on these big losses.

Q: What do you think about Steve Wynn and Wynn Hotels?

A: I’d be buying down here down 62%; it was announced today that Steve Wynn has secretly been acting as an agent for the Chinese government where (WYNN) has a major part of its operations. Who knew? With all those high rollers being flown in on private jets from China, sitting at the tables in the closed rooms. So yes, this is a recovery play and it will do just as well as all other recovery plays, but remember it’s a China recovery play. And I think, in any case, his ex-wife owns a big part of the company anyway. So I don’t think Steve Wynn is that closely connected with Wynn hotels because of past transgressions with the female staff.

Q: Is it time to scale into Freeport-McMoRan (FCX)?

A: I’d say yes. On a longer-term view, I expect (FCX) to go to $100. And for those who have the May $32/$35 call spread that expires on Friday, my bet is that you get the max profit—but you may not sleep before then.

Q: What do you have to say about a post-Putin scenario and impact on the market?

A: The day Putin dies of a heart attack, you can count on the market being up 10%, if that happens right now—less if it happens at a later date. But it would be hugely bullish for the entire global stock market, and oil would also collapse, which is why I refuse to put on oil plays here. That is a risk. Putin can give up, have an accident, or get overthrown. When the Russian people see their standard of living decline by 90%, this is a country that has a long history of revolutions, putting their leaders in front of firing squads and throwing the bodies down wells. So, if I were Putin, I wouldn't be sleeping very well right now.

Q: What's the reason for air tickets (UAL), (ALK), (DAL) going up sharply?

A: 1. Shortage of airplanes 2. Soaring fuel costs 3. Labor shortages and strikes 4. It is all proof of an economy that is definitely NOT going into recession.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

With Lieutenant Uhuru

Global Market Comments

May 11, 2022

Fiat Lux

Featured Trade:

(JOIN ME ON CUNARD’S MS QUEEN VICTORIA

FOR MY JULY 9, 2022 SEMINAR AT SEA)

Global Market Comments

May 10, 2022

Fiat Lux

Featured Trade:

(MAY 4 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (ROM), (ARKK), (LMT), (RTN), (USO), (AAPL), (BRKB), (TLT), (TBT), (HYG), (AMZN)

Below please find subscribers’ Q&A for the May 4 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley.

Q: How confident are you to jump into stocks right now?

A: Not confident at all. If you look at all of my positions, they’re very deep in the money and fully hedged—I have longs offsetting my shorts—and everything I own expires in 12 days. So, I’m expecting a little rally still here—maybe 1,000 points after the Fed announcement, and then we could go back to new lows.

Q: Would you scale into ProShares Ultra Technology ETF (ROM) if you’ve been holding it for several years?

A: I would—in the $40s, the (ROM) is very tempting. On like a 5-year view, you could probably go from the $40s to $150 or $200. But don’t expect to sleep very much at night if you take this position, because this is volatile as all get out. It's not exactly clear whether we have bottomed out in tech or not, especially small tech, which the (ROM) owns a lot of.

Q: Is it time to buy the Ark Innovation ETF (ARKK) with the 5-year view?

A: Yes. I mentioned the math on that a couple of days ago in my hot tips. Out of 10 positions, you only need one to go up ten times to make the whole thing worth it, and you can write off everything else. Again, we’re looking at venture capital type math on these leverage tech plays, and that makes them very attractive; however I’m always trying to get the best possible price, so I haven’t done it yet.

Q: We’ve been hit hard with the tech trade alerts since March. Any thoughts?

A: Yes, we’re getting close to a bottom here. The short squeeze on the Chinese tech trade alerts that we had out was a one-day thing. However, when you get these ferocious short covering rallies at the bottom—we certainly got one on Monday in the S&P 500 (SPY) —it means we’re close to a bottom. So, we may go down maybe 4%-6% and test a couple more times and have 500- or 1000-point rallies right after that, which is a sign of a bottom. There’s a 50% chance the bottom was at $407 on Monday, and 50% chance we go down $27 more points to $380.

Q: Is the Roaring 20s hypothesis still on?

A: Yes absolutely; technology is still hyper-accelerating, and that is the driver of all of this. And while tech stocks may get cheap, the actual technology underlying the stocks is still increasing at an unbelievable rate. You just have to be here in Silicon Valley to see it happening.

Q: Do you like defense stocks?

A: Yes, because companies like Lockheed Martin (LMT) and Raytheon (RTN) operate on very long-term contracts that never go away—they basically have guaranteed income from the government—meeting the supply of F35 fighters for example, for 20 years. Certainly, the war in Ukraine has increased defense spending; not just the US but every country in the world that has a military. So all of a sudden, everybody is buying everything—especially the javelin missiles which are made in Florida, Georgia and Arizona. The Peace Dividend is over and all defense companies will benefit from that.

Q: Is Buffet wrong to go into energy right now? How will Berkshire Hathaway Inc. (BRK.B) perform if energy tanks?

A: Well first of all, energy is only a small part of his portfolio. Any losses in energy would be counterbalanced by big gains in his banking holdings, which are among his largest holdings, and in Apple (AAPL). Buffet does what I do, he cross-hedges positions and always has something that’s going up. I think Berkshire is still a buy. And he's not buying oil, per say; he is buying the energy producing companies which right now have record margins. Even if oil goes back down to $50 a barrel, these companies will still keep making money. However, he can wait 5 years for things to work for him and I can’t; I need them to work in 5 minutes.

Q: You must have suffered big oil (USO) losses in the past, right?

A: Actually I have not, but I have seen other people go bankrupt on faulty assumptions of what energy prices are going to do. In the 1990s Gulf War, someone made an enormous bet that oil would go up when the actual shooting started. But of course, it didn’t, it was a “buy the rumor, sell the news” situation. Energy prices collapsed and this hedge fund had a 100% loss in one day. That is what keeps me from going long energy at the top. And the other evidence that the energy companies themselves believe this is true is that they’re refusing to invest in their own businesses, they won’t expand capacity even though the government is begging them to do so.

Q: Why should we stay short the iShares 20 Plus Year Treasury Bond ETF (TLT) instead of selling out for a profit or holding on due to your statement that the TLT will go down to $105/$110?

A; If you have the December LEAPS, which most of you do, there’s still a 10% profit in that position running it seven more months. In this day and age, 7% is worth going for because there isn’t anything else to buy right now, except very aggressive, very short term, front month options, which I've been doing. So, the only reason to sell the TLT now and take a profit—even though it’s probably the biggest profit of your life—is that you found something better; and I doubt you're finding anything better to do right now than running your short Treasuries.

Q: Are you still short the TLT?

A: Yes, the front months, the Mays, expire in 8 days and I’m running them into expiration.

Q: What will Bitcoin do?

A: It will continue to bounce along a bottom, or maybe go lower as long as liquidity in the financial system is shrinking, which it is now at roughly a $90 billion/month rate. That’s not good for Bitcoin.

Q: Is now the time for Nvidia Corporation (NVDA)?

A: Yes, it’s definitely time to nibble here. It’s one of the best companies in the world that’s dropped more than 50%. I think we’d have a final bottom, and then we’re entering a new long term bull market where we’d go into 1-2 year LEAPS.

Q: What do you think of buying the iShares iBoxx $ High Yield Corporate Bond ETF (HYG) junk bond fund here for 6% dividend?

A: If you’re happy with that, I would go for it. But I think junk is going to have a higher dividend yet still. This thing had a dividend in the teens during the financial crisis; I don’t think we’ll get to the teens this time because we don’t have a financial crisis, but 7% or 8% are definitely doable. And then you want to look at the 2x long junk bond special ETFs, because you’re going to get a 16% return on a very boring junk bond fund to own.

Q: What do you think about Amazon (AMZN) at this level?

A: I think it’s too early and it goes lower. Not a good stock to own during recession worries. At some point it’ll be a good buy, but not yet.

Q: Energy is the best sector this year—how long can it keep going?

A: Until we get a recession. By the way, if you want evidence that we’re not in a recession, look at $100/barrel oil. When you get real recessions, oil goes down to 420 or $30….or negative $37 as it did in 2020. There’s a lot of conflicting data out in the market these days and a lot of conflicting price reactions so you have to learn which ones to ignore.

Q: Should we stay short the (TLT)?

A: Yes, we should. I’m looking for a 3.50% yield this year that should take us down to $105.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

May 9, 2022

Fiat Lux

Featured Trade:

(BUYER STRIKE HAS LEGS)

($COMPQ), (AMZN), (FB)

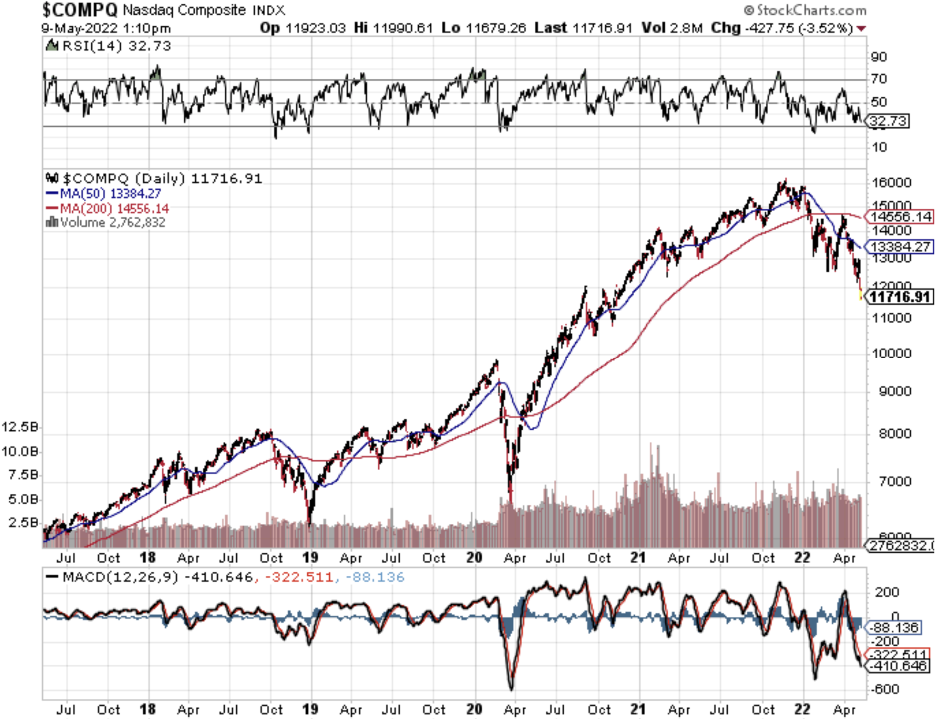

The buyer strike roars ahead as the 10-year U.S. treasure accelerates its rate of decline touching 3.2%.

We are dealing with a major deleveraging of the tech sector as a massive rotation flood into commodity-linked assets, the US dollar, and shorting bonds.

Sadly, we got another kick up the rear side when US Central Bank governor Jerome Powell committed yet another policy mistake by attempting to save the stock market.

Things could get ugly from here.

Many investors believed the Fed would self-correct after the “transitory” inflation nonsense.

It’s not so much the actual 3.2% rate today, but the velocity of the move which is creating many air pockets that are not being filled.

Why?

Investors are betting that Powell will most likely make a third policy mistake which could create another suicidal spiral downwards.

Investors have no incentive to buy stocks when the Fed has not only lost credibility but appears to not understand what is going on with real inflation tearing apart economic health.

This looks a lot like the 1970s just before former US Fed Chair Paul Volcker was brought in to slam the economy and raise interest rates to 18%.

Powell doesn’t seem like he has the guts to do that which is why the prolonging of this failed interest rate policy will mean a longer and more painful economic recession in the future.

I see many pundits going on record saying that the “risk reward has improved.”

Besides stating the obvious, this analysis doesn’t take into consideration that yields could go higher which would cause tech stocks to plummet further.

So yes, the risk reward has improved, but it can improve even more from here.

That doesn’t tell us much about anything.

All signs are now pointing to a souring paradigm shift among tech firms and dramatic changes under the hood.

Facebook (FB) is pausing hiring, a previously unthinkable prospect.

The company blamed macroeconomic challenges and Apple’s privacy changes for its slowest revenue growth in 10 years last quarter.

Almost 12 months after Apple launched App Tracking Transparency, a new analysis predicts its second year will still see big losses to advertisers on FB and YouTube and more collectively losing around $16 billion.

In total, FB will sink $10 billion into its new business with no revenue in 2022.

In February, Amazon (AMZN) announced it would raise its base pay cap from a maximum of $160,000 for most roles to $350,000.

The news comes after employees listed insufficient base pay as the second-most common reason they're looking to leave Amazon in an internal survey conducted last year.

I don’t have an issue with raising salaries, but AMZN had to boost it by far more than double showing readers the intense pressures on current expenses.

Even more problematic now is that new recruits won’t want to accept restricted stock options because of the tech selloff making their stock options less valuable.

Nobody wants to catch a falling knife, me included.

This will put more cash flow pressure on tech companies as new employees will reject stock options and demand a higher net cash salary.

The incremental micro negatives are causing tech companies to miss earnings and guide lower adding yet another negative layer to the grim outlook.

I would argue that even with earnings beats and positive guidance, the tech sector losses would be less.

However, we are experiencing a perfect storm of poor macro events and bad operational data.

Even though the risk reward has improved, it could improve more as the Fed will be forced to ratchet up rates more than expected to compensate for the latest policy mistake.

The market has sniffed this out and is unwilling to buy the dip until the Fed does what is necessary to seriously fight inflation.

The nonsense needs to stop.

Mad Hedge Technology Letter

May 6, 2022

Fiat Lux

Featured Trade:

(ECOMMERCE NOT AS EASY AS IT USED TO BE)

(AMZN), (FED)